XLU - Northwest Natural: Another Dividend Increase And Undervalued Shares Make It A Buy

2023-10-16 01:43:48 ET

Summary

- Northwest Natural is a holding company with three divisions: gas utility, water and wastewater utility, and biogas business.

- The dividend yield was just raised to 5.0%, the 68th year it has been increased.

- NWN has been making acquisitions and expanding its water and renewable energy businesses, which have the potential for long-term growth. It acquired yet another water utility this quarter.

- I estimate the current share price of $39.17 to be 10-15% undervalued.

Northwest Natural ( NWN ) is a holding company headquartered in Portland, Oregon, and it has been in existence in various forms for 160 years. NWN has three divisions: 1) Northwest Natural, a gas utility, 2) Northwest Natural Water, a water and wastewater utility, and 3) NW Natural Renewables, a biogas business creating purified gas from decomposed organic matter. The gas utility is by far the largest revenue generator with over 90.0% of the company's income, per the 2022 Annual Report . Recent years have been strong and on October 12th, the company announced a dividend increase of 0.5%. This will be the 68th consecutive year of increases, and at current share prices, the yield is an attractive 5.0%.

I believe NWN's shares are undervalued at the current price of $39.17, down some 27.9% from the May 2022 peak of $54.29. The stock's current beta of 0.59 indicates that it is less volatile than the overall market. If you are an income investor with a long-term horizon, I believe a share price under $40 is an attractive entry point, and the stock has been under that price since late September. While the dividend grows slowly, the long-term upside with Northwest Natural will be the company's new businesses and recent streak of acquisitions, including another this month. The current Standard & Poor's credit rating is "AA," or high investment grade. Below is a five-year history of the stock.

Share Price History (Seeking Alpha Charting)

{kind=link}

Growth Areas for the Future

Northwest Natural Water (and wastewater) began in 2018 through an acquisition, starting with less than 10,000 connections. Today I estimate there are about 79,900 water connections after recent acquisitions. In early 2023 there were the acquisitions of Hiland Water Corporation and King Water Company in Washington and Oregon State that added some 15,000 connections. In October 2023, NWN made another acquisition with Rose Valley Water Company, serving approximately 2,400 connections in Peoria, Arizona, a major suburb northwest of Phoenix. There are also customers in Idaho, Southern Arizona (Truxton Canyon Water and Cerbat Water) and Texas (Everett Square) from prior purchases in 2022. The cumulative water investment to date is substantial, and customers have grown at a compound annual rate of 46.7%. NWN Water has also increased its ownership stake in Avion Water Company, an investor-owned utility in central Oregon, to 40.3%. I would not be surprised if this stake is increased further and I think the water management business, in particular, has long-term potential to improve growth at NWN.

Water Customer Growth (NWN 2022 Annual Report)

Northwest Natural Renewables was started in 2021 with a $50 million investment in two renewable natural gas production facilities. It was partnered with EDL Energy and the plants just came online in May of 2023. They are expected to generate enough gas to serve 5,400 connections. These investments were made possible through Oregon Senate Bill 98, which supports renewable energy procurement and investment by natural gas utilities. It will take time to know how profitable this division will be, but NW Natural Renewables and EDL plan to have a 20-year supply of renewable natural gas from this project. The revenues associated with it have just started coming in and should be factored into the 2023 report.

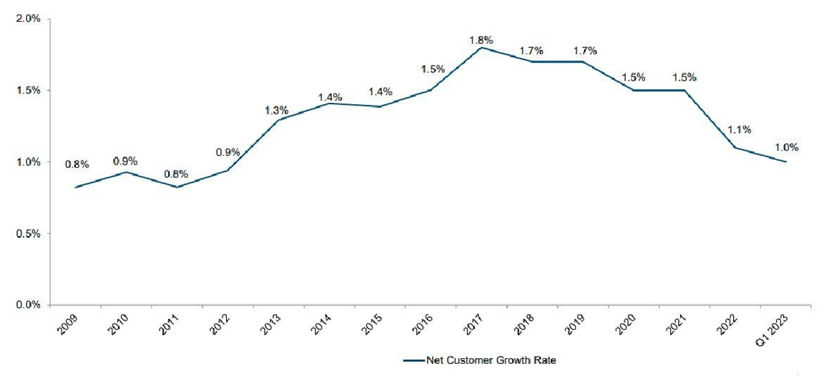

The Core Gas Business, NW Natural, is a local distribution company that currently provides natural gas service to approximately 2.5 million people through more than 795,000 meters. About 88.0% of its gas customers are located in Oregon and 12.0% in Washington, and about 60% of end users are residential, the balance industrial. This business is growing the number of its connections organically at about 1.1% to 1.5% per year, as illustrated in the chart below. In 2015, it was one of the first gas utilities in the U.S. to replace all cast iron and bare steel pipelines with modern polyethylene and "cathodically protected" pipes. These are reported to be highly resistant to corrosion, perform better in seismic events and keep more gas in the pipes. They also have a life expectancy, in theory, of 100 years. So this costly infrastructure expense is an item in the past. The demand drivers in this segment moving forward will be population growth in Oregon and Washington, but there is always the possibility of some acquisitions.

Organic Gas Customer Growth (June 2023 Investor Presentation)

{kind=link}

NWN's 2022-2023 Performance

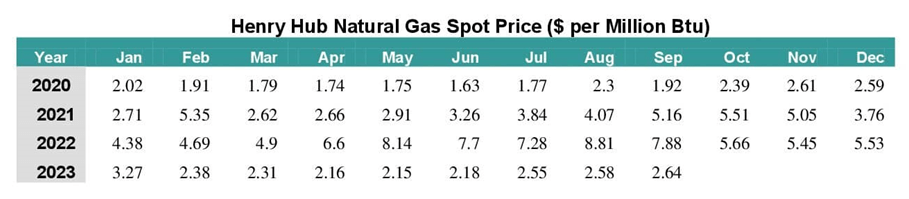

2022 and 2023 have been strong years for NWN. Operating revenues increased from $860 million in 2021 to $1.04 billion in 2022. Earnings per share were generally steady at $2.56 in 2021 and $2.54 in 2022, the latter lowered by share dilution, as outlined in the 2022 Annual Report . 2022 also saw tighter margins due to the increased price of natural gas, which peaked at $8.81 per Btu in August of that year.

Updated Gas Spot Price Variation (US Energy Information Administration)

{kind=link}

Northwest Natural handily beat earnings estimates for the first two quarters of 2023. Much of this was due to new regulatory rates. For first half of 2023, the company reported net income of $72.9 million, compared to earnings of $58.0 million for the same period in 2022. It also added nearly 6,400 natural gas meters for a growth rate of 0.8% in that sector this year. 2023 EPS guidance was affirmed in the range of $2.55 to $2.75 per share, an increase of 8.3% over last year's numbers. The Natural Gas Distribution segment net income increased some $16.1 million this year reflecting new increased rates in Oregon and Washington that went into effect on Nov. 1, 2022, partially offset by higher operating expenses. Also March weather was colder than average.

NW Natural Renewables' new project began operations in the first half of 2023 and Northwest Natural Water expanded in Arizona, Oregon and Washington during this time frame. It had already closed seven water and wastewater utility transactions in 2022. The full impact of these operations on the bottom line won't be known for another year, but I suspect it should generate a meaningful increase. Water revenues grew from $17.3 million in 2021 to $23.0 million in 2022, an increase of 32.9%. In 2020, revenues were only $14.9 million from this segment. For 2023, I would expect water revenues to be significantly higher from acquisitions, though we will have an idea of how much higher when third quarter results are released on November 3.

As for the natural gas segment, the main driver in the future will be population growth. Overall, the industry is expecting earnings per share to increase by 6% in each of the next two years. This is affirmed by Institutional Investor which forecast 6.0% EPS growth on average across utilities.

Notes on Rate Structures and Debt

Northwest Natural Gas is the most regulated of the three business segments. All its customers are located in Oregon and southwest Washington. It has an exclusive service territory granted by the Oregon Public Utility Commission (OPUC) and Washington Utilities and Transportation Commission (WUTC), which includes the Portland metropolitan area, and portions of western Washington along the Columbia River. Since 2002, NW Natural in Oregon has operated under a rate structure called "partial decoupling." In this structure, the company is allowed to keep a fixed amount for each residential and commercial customer. If it receives more or less than that fixed amount each year, customer rates are adjusted for the difference. In October 2022, NW Natural received approval for an Oregon rate change, with a $59.4 million increase in the revenue requirement and rate base of $1.76 billion. This was a positive change of 14.4%. In Washington, the second year of a multiyear rate plan went into effect, increasing that revenue by $3.0 million. These increases were evident in the Second Quarter EPS results.

As for water rates, operations are seasonal in nature with peak demand during warmer summer months. Wastewater is less seasonal and more consistent. NWN's recent acquisitions operate in exclusive service territories with no direct competitors, but they are regulated by state utility commissions. Wastewater services are partly state regulated and partly unregulated depending on location, whether Idaho, Texas, Oregon or Arizona. The Renewable Natural Gas sector is non-regulated.

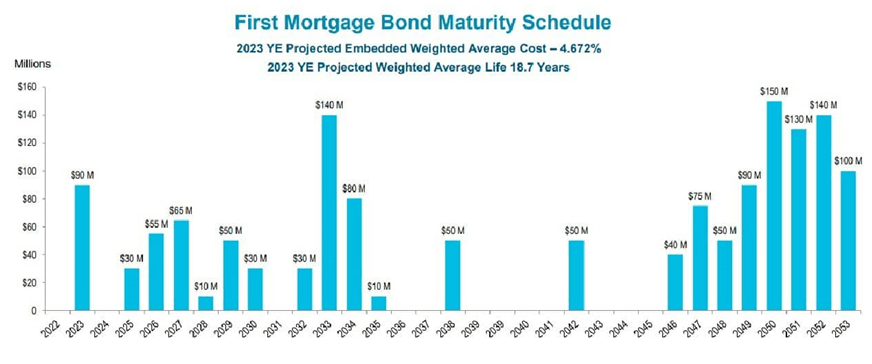

NWN Long Term Debt (2023 Investor Presentation)

{kind=link}

As for debt, NW Natural continues to monitor interest rates and financing options for all three businesses. Interest rates have increased in 2022 and 2023, from actions taken by the U.S. Federal Reserve to counter inflation, which remains elevated. Generally, NW Natural recovers interest expenses on its long-term debt through its regulator-authorized cost of capital. According to the company "certain working capital items, such as the cost of gas, are deferred and accrue interest in Oregon and Washington…and short term debt is incorporated in the capital structure in Washington." NW Natural Water's regulated water and wastewater utilities recover the interest cost of long-term debt through their authorized cost of capital as well. NWN believes that the impact of rising interest rates is mitigated by its predominately fixed-rate debt. It also has a manageable debt repayment schedule (above) with no significant maturities in any particular year.

Updated Dividend History

NWN just raised its dividend from $0.485 to $0.4875 per quarter, an increase of 0.5%. The company hasn't missed a regular dividend since its first dividend payment in 1956 and it has increased its dividend every year since then. NWN is not a member of the S&P 500 Dividend Aristocrats , where members have increased their dividends for a minimum of 25 years. That list requires a minimum float-adjusted market cap of $3.0 billion and the market cap of Northwest Natural is $1.4 billion. This is not a restriction for the Dividend Kings list, however, which has the chief requirement that companies have raised their dividend every year for the last 50 years. You can find the 2023 list here .

NW Natural moved from the NASDAQ stock market to a listing on the New York Stock Exchange under the symbol NWN in 2000. Since that time it has raised its annual dividend from $0.31 to $0.4875, an increase of 57.3 percent, or about 2.0% per year. For many years this was above the rate of inflation; now it is not and recent increases have been along the lines of $0.0025 per share. So, the dividend is slow growing, but currently at an attractive rate. At the current share price of $39.17, this would make the dividend yield 5.0%.

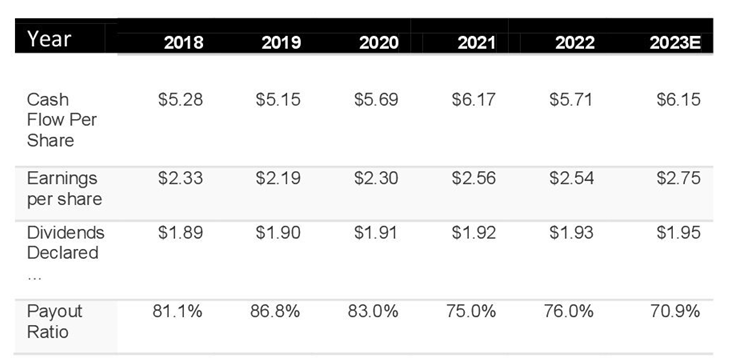

The estimated 2023 payout ratio for NWN is 70.9%. The payout ratio over the last six years is presented below. This assumes 2023 income reaches the upper consensus number of $2.75 per share; with the recent increase, we now know the dividend is $1.95. S&P cites average utility payout ratios as 63%, but they vary widely with companies like ConEd ( ED ) at 45.9%, to American Electric Power ( AEP ) at 76.6% and Dominion Energy ( D ) at 98.9%. NWN's payout seems to be in the middle of the pack.

Updated Payout Ratios (Author sourced and calculated)

{kind=link}

Utility shares have been trending lower lately, boosting yields across the board. You can compare the current 5.0% yield at NWN to other utility stocks such as Southern Company ( SO ) at 4.20%, Consolidated Edison at 3.71%, American Electric Power at 4.52%, and Spire Inc. ( SR ) at 5.0%. It is also worth comparing with an index like ProShares Ultra Utilities (UPW), with a current dividend yield of 2.89%, or Utilities Select Sector SPDR Fund ( XLU ) at 3.6%.

Updated Share Valuation, DCF and P/E Ratio

I estimate the current value of NWN shares to be US $45.56. I have used a discounted cash flow cash to value the company's shares. This involved taking the new 2023 estimated earnings per share of $2.75, and then projecting forward. In this case I have used a 5-year projection period. This required a discount rate to adjust for time and risk, a growth rate projection, and a capitalization rate for the final year reversion. For the discount rate, I looked at the average annual return of the S&P 500. The long term average is about 9.25% while over the last 10 years it has been 10.4%. I have elected to use a discount rate of 9.25%, at the lower end of the range, discounting beginning in the second year. I chose this rate because NWN is a regulated utility, with more stable returns. Because this estimate is based on art, rather than science, I have valued the company very conservatively.

Below are NWN's annual earnings since 2018. Between 2018 and 2023 the compound annual growth rate in earnings per share was 1.7%, or about 2.0%. However the RNG segment only came online in the second half of 2023, and the number of water customers nearly doubled in 2022. There will also be more organic growth from the natural gas division which expands customers by 1.1 to 1.5% per year. Because of these factors, I am increasing the growth rate in EPS to a still conservative 4.0% per year. This seems easily supported by Institutional Investor , which has projected 6.0% per year growth for utilities over the next three years.

Earnings Per Share (Q2 2023 Report)

{kind=link}

I have valued the shares starting with NWN's projected EPS of $2.75 in 2023, then a 4.0% growth rate in net income each year over the next five years. I have estimated a reversion rate of 6.5%, given the new growth profile of the company with water and biogas.

Updated Discounted Cash Flow (Author calculated)

{kind=link}

Based on my calculations, I estimate the updated value of the shares listed on the NYSE to be worth US $45.56. They are being discounted today along with other shares in the utility sector. According to Institutional Investor , U.S. utilities have returned an average 8.6% annually in the last 30 years, and posted double-digit returns in 18 of those years. However, this all changed in 2020 when volatility entered the sector.

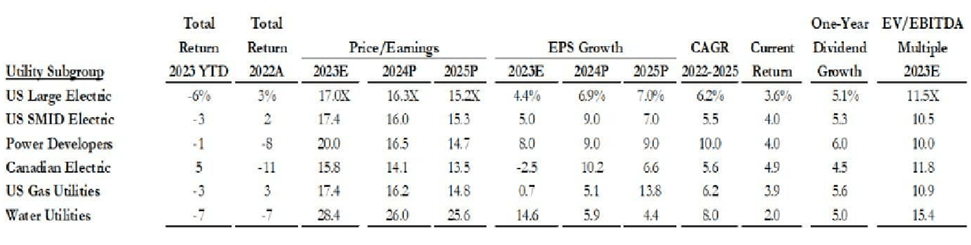

As a cross-check to the DCF valuation, I have valued NWN shares using a traditional P/E ratio calculation for gas utility companies. Gabelli Funds has a useful chart indicating that the average US Gas Utility Ratio for 2024 would be 16.2. Applying this to the estimated 2023 earnings per share, the value would be $2.75 x 16.2 = $44.55. Given the current price of $39.17 and these two similar value estimates, shares are 10-15% undervalued.

Utility P/E Ratios by Segment (Gabelli Funds)

{kind=link}

Risks to Outlook

In its service areas, the Northwest Natural Gas has no direct competition from other natural gas distributors. However, as management points out, it does compete with other forms of energy. The natural gas segment is seasonal and demand increases during the colder winter months. Of course a warm winter means less usage, and this may be impacted by climate change. However, I suspect that rising population in Oregon and Washington will offset this usage risk.

Water distribution operations are also seasonal and have their peak demand during the summer months, while wastewater is not seasonal. The new water service utilities generally operate in exclusive territories with no direct competitors. However, water distribution customer rates are regulated by state utility commissions. The wastewater business has some state-regulated systems and some that are not rate-regulated. The renewable natural gas segment is not regulated but should be considered a startup that will take longer to come online than the water business, which consists of already in-operation acquisitions. Finally, natural gas itself is subjected to political and supply risks, part of what caused the price spike of 2022. Higher gas prices actually squeeze Northwest natural's margins, rather than improving them.

Conclusion

NWN is a Dividend King with a superb now 68-year streak of rising dividends. Although the annual increases may be small, I believe there is room here for some share price appreciation, especially with two new divisions created in the last five years and increasing geographic diversity with water operations in Texas, Arizona, and Idaho, and likely more acquisitions to come. I believe the market has not fully considered these changes in company strategy. I estimate (with updated calculations above) that the current share price of $39.17 is 10-15% undervalued. NWN appears to be at a below-market price, and along with other utilities, the shares have gone down as yields on other investments rise. With the recent increase, and dip in price, the dividend looks more attractive. I think this is a strong long-term dividend play, with some potential share price upside in the future.

For further details see:

Northwest Natural: Another Dividend Increase And Undervalued Shares Make It A Buy