NTG - NTG: Despite The Fall In Natural Gas Prices This CEF Is A Buy

2023-12-18 18:10:24 ET

Summary

- Natural gas prices have fallen over 30% since October, creating buying opportunities in the natural gas transportation sector.

- High production and a warm winter have contributed to the collapse in natural gas prices.

- The Tortoise Midstream Energy Fund is a closed-end fund focused on natural gas transportation companies.

- The fund's discount has widened as a response to the commodity price action.

- The CEF will see a bid from a share repurchase action initiated by the manager.

Thesis

With natural gas prices down over -30% since their October highs, one must wonder where the opportunities lie in the sector:

Nat Gas Px (tradingview)

Natural gas is a very volatile asset class, also called a 'widow maker' by many market participants. There are two distinct sectors in the natural gas market, namely producers and transporters. Producers are those companies that engage in the exploration and production of natural gas, and they have a very high correlation in their share price with net prices. Transporters on the other hand are usually incorporated as MLPs or C-corps, and have a much lower correlation in their share price to net commodity levels.

The reason behind this segregation is the necessity to transport the commodity irrespective of the net pricing. In addition, transporters usually have multi-year contracts in place with minimum transportation levels, insulating their businesses to the vagaries of seasonality and performance in the underlying commodity prices.

In this article we are going to re-visit the Tortoise Midstream Energy Fund ( NTG ), a CEF which we have covered before. The fund specializes in the equity of natural gas transportation companies:

Portfolio (Fund Fact Sheet)

We feel the violent fall in natural gas prices has negatively affected transporters, with a buying opportunity in NTG currently.

Why did we see such a collapse in natural gas prices?

High production coupled with a warm winter so far have brought down prices:

Lower 48 production (HFIR)

As per HFIR Research's data, the lower 48 production this year is above recent production years, with supply outstripping demand. The production increase is due to the resurgence of US shale production , with gas being a by-product in many wells. As long as production keeps increasing and the consumption is not there, prices will be kept in check. Furthermore this winter has been unseasonably warm so far, both in the U.S and Europe:

EU Storage Levels (Oxford Econ)

European gas storage levels are at record highs, on the back of a conservative build and milder weather. Europe has been very pro-active in weaning itself off Russian gas, with higher storage levels and conservative consumption in many areas. LNG demand out of Europe is thus affected by the current oversupply.

Performance

The fund is up on a total return basis this year:

The vehicle experienced a -6% drawdown during the regional banking crisis in March/April, but recovered subsequently. A regional banking crisis that would have resulted in a prolonged recession would have been a negative for the entire oil and gas industry.

More importantly though the CEF exhibits the traits of a healthy investment vehicle, with a stable NAV:

Despite the bouts of volatility, the fund's NAV is almost unchanged on a 1-year lookback, translating into investors clipping the yield on the underlying assets.

Premium/Discount to NAV

The CEF has settled in a -20% to -15% discount to NAV range since the post Covid period:

With the latest weakness in natural gas prices, the fund is now towards the bottom of its discount range at -18.76%. Expect a 3% to 5% tightening in the discount once there is a firming up in natural gas prices.

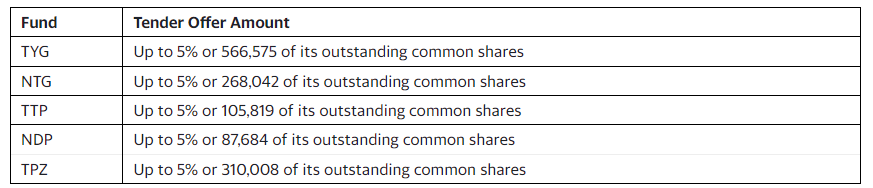

New tender offer announced

Tortoise has been fairly active in the past few years in terms of doing tender offers for its CEFs in order to close out the significant discounts to NAV. This year is no different, with a new corporate action announced :

OVERLAND PARK, KS / ACCESSWIRE / October 2, 2023 / Tortoise announced today the commencement of cash tender offers for each of the following Funds.

Each tender offer will be conducted at a price equal to 98% of each Fund's net asset value per share as of the close of regular trading on the New York Stock Exchange (NYSE) on the date the tender offer expires. Each tender offer will expire at 5:00 P.M., Eastern Time on November 1, 2023, or on such later date to which the offer is extended.

{kind=link}

The tender offer will simply put a larger bid in the market for the CEF, thus ensuring the fund's discount to NAV does not exceed its recent historic range of -20%.

Active corporate actions like this one are a positive sign in terms of the CEF performance and its management team, with active approaches to dealing with discounts being preferred to passive ones.

Saba wins - activist investor on the prowl

Saba is an activist hedge fund that has done a significant amount of work in the closed end fund space in order to generate profits. In a nutshell Saba identifies CEFs with very large discounts in market value over NAV and takes positions in the respective CEFs looking to close-out that arbitrage gap. As a reminder, given its structure, the shares of a CEF can trade below market value. Such an instance can present instantaneous gains if managers liquidate the funds or transform them into ETFs. By liquidating a fund or moving the structure to an ETF the market price will converge to NAV. CEF managers do not like to undertake such actions because CEF management fees are very high in comparison to other vehicles, thus they prefer to keep the status quo.

Saba has taken significant positions in CEF, but has found out that they cannot nominate board members because of fund management actions. As a result they entered into litigation . Tortoise was one of the fund managers targeted by Saba. Two weeks ago the United States District Court for the Southern District of New York ruled in Saba's favor:

December 07, 2023 08:00 AM Eastern Standard Time

U.S. District Court for the Southern District of New York Rules That Certain Closed-End Funds, Including Funds Advised by BlackRock, Violated the Investment Company Act of 1940

NEW YORK--Saba Capital Management, L.P. (“Saba” or “we”) today commented on the outcome of the lawsuit brought in the United States District Court for the Southern District of New York (the “Court”) against 16 closed-end funds (the “Funds”) including those managed by BlackRock, Inc. (“BlackRock”) and its Trustees (R. Glenn Hubbard, W. Carl Kester, Cynthia L. Egan, Frank J. Fabozzi, Lorenzo A. Flores, Stayce D. Harris, J. Phillip Holloman, Catherine A. Lynch, Robert Fairbairn and John M. Perlowski).

Saba filed its lawsuit in the Court on June 29, 2023 after the BlackRock trustees disclosed they would strip shareholders’ votes, in violation of the Investment Company Act of 1940 (the “ICA”), at their 2023 Annual Meeting. Despite the Funds filing various motions to dismiss the lawsuit, the Court ruled in favor of Saba, finding that the actions of the BlackRock Fund and its trustees violated federal law.

This ruling translates into NTG having a higher probability of a significant narrowing in its discount to NAV on the back of potential activist actions by Saba. The win is not going to translate into an instantaneous change in the discount, but over time holders will be favored to see improvements in the discount to NAV.

Conclusion

NTG is a closed end fund focused on equities from natural gas transportation and infrastructure companies. Natural gas as a commodity is down over -30% since October, resulting in a negative impact on the fund's discount to NAV. The portfolio companies in this CEF have a very low correlation to actual prices, with their transportation contracts being multi-year and with minimum volume levels. While E&P companies are directly affected by seasonal swings in prices, transportation enterprises work on a cycle basis.

NTG will also benefit from an annual share repurchase program undertaken by the manager and the favorable ruling in a lawsuit initiated by the activist fund Saba. NTG represents the correct play on the recent drop in natural gas prices, with an estimated 12% return in the next year, stemming from the fund's 9% dividend yield and predicted narrowing of its discount to NAV.

For further details see:

NTG: Despite The Fall In Natural Gas Prices, This CEF Is A Buy