IBM - NVE Corp.: Low Growth But Highly Profitable And Has The Cash To Pay Dividends

Summary

- NVE Corp. uses spintronic technology to make some of the world's smallest sensors to fit in the tiniest medical or industrial robots.

- On the other end of the spectrum, its profitability and cash flow metrics are higher than the median for the IT sector.

- I assess prospects for revenue growth in light of supply chain constraints and low Capex spent as a percentage of sales.

- I also elaborate on those enticing dividend yields.

- The stock is a buy in view of the tightening of monetary policy.

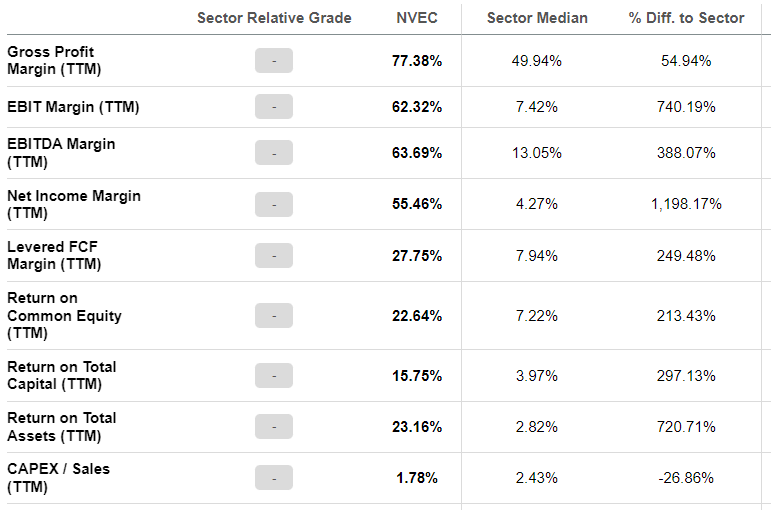

In my quest to look for companies that are better positioned to navigate through the period of acute tightening of monetary policy period which lies ahead, I came across NVE Corporation ( NVEC ). As seen in the table below, it has profitability metrics that, in some cases are superior to the median for the IT sector by more than 1000% as well as good free cash flow margins.

Profitability and Cash Metrics (www.seekingalpha.com)

{kind=link}

On the other hand, its Capex to Sales ratio which is the percentage of revenue spent on capital expense is lower than the sector median implying that it may not be investing sufficiently for growth. In this respect, I noted that revenue growth has decelerated in Q1-2023 (which ended in June 2022) to 2.56% compared to 14.6% in the March quarter.

Thus, in addition to shedding some light on growth, this thesis also aims to assess the ability of the company at sustaining its profitability. I start by providing some insights as to what differentiates NVEC as a semiconductor play.

Spintronics Vs Electronics

Most of you will have already been across the word electronics which is all about using the ability of electrons to charge and discharge rapidly in order to transport data in computers. Instead, spintronics, which is also known as magneto electronics uses the spin of the electron and the associated magnetic field it creates to transfer data. Now, the fact that this can be done in solid-state devices makes spintronics perfect for applications like sensors and couplers in robots and the Internet of Things (IoT). The company also manufactures some of the highest quality sensors used in MRI machines and pacemakers.

These devices are available in semiconductor format and are more stable (nonvolatile) with respect to charge-based electronics. With so many qualities, it is not surprising to see other companies commercializing related products, with prominent industry plays like Intel (NASDAQ: INTC ) and International Business Machines ( IBM ) collaborating with academia for research purposes.

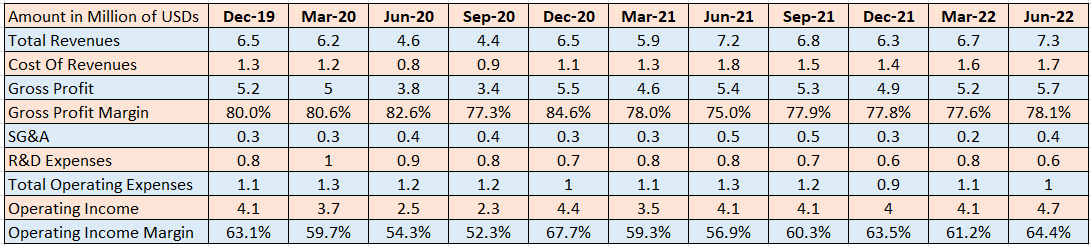

Here, one key factor which explains NVEC's high profitability is that, in addition to selling products, it also performs contract research, a segment that saw a 32% revenue increase in Q1-2023 (Q1) compared to last year. In comparison product sales increased by only 3%, but still accounted for 96.4% of total revenues. The reason for this is just like many other industry peers, the company's operations were impacted by supply chain shortages as from the second quarter of 2021, with gross margins falling to 75% for the June 2021 quarter as shown in the table below.

Quarterly revenues (www.seekingalpha.com)

{kind=link}

There have been signs of improvement as per the management during Q1's earnings call. Noteworthily, gross margins have been increasing steadily and should improve further as the company has been raising prices since the beginning of this year to offset the higher cost of revenues.

Continuing on Profitability, Cash, and Growth

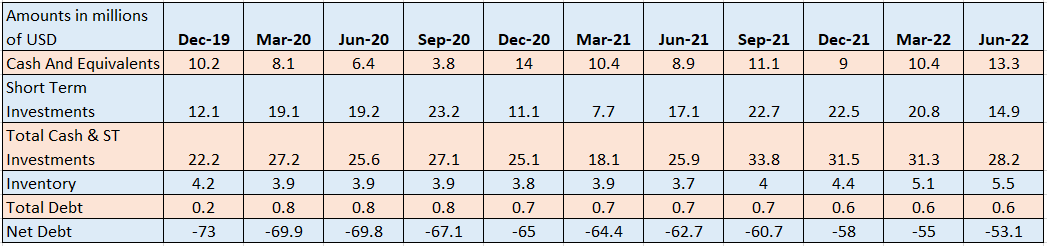

In order to mitigate against supply chain challenges, inventories have been scaled up to above $5 million as per the table below, or 20% more than at the beginning of 2021. This is the reason the cash position has deteriorated slightly.

Balance Sheet - Quarterly figures (www.seekingalpha.com)

{kind=link}

However, these higher inventories should deliver more cash from operations and therefore more growth in the coming quarters. Here, thanks to its ability to pass on costs to customers, NVEC should see higher gross margins, provided it can control operating expenses. In this respect, most probably due to its smaller size with employees being relatively more multi-skilled, the company appears to have some flexibility in moving them from one department to another.

In this way, there was a 26% reduction in R&D expenses as staff dedicated more time to revenue-generating activities in Q1. As a result, operating income margins actually increased to 64.4%. Now, this was also due to the timing of some staff incentive compensation, but, any future employee-related expenses should be offset by the uptrend in gross margins.

Another factor that can potentially bring more growth is an associated field of electron spinning research called MRAM (Magnetoresistive Random Access Memories) which can be envisioned as the next-generation memory technology, about 600 times faster than conventional ones. This technology should produce a faster and denser all-in-one single memory chip that can hold the data contained in several conventional ones used today. This is the reason NVEC has licensed it to Motorola ( MSI ), Cypress, and Honeywell International ( HON ).

However, it faces competition from Everspin Technologies (NASDAQ: MRAM ) with a market cap of $135 million and which grew revenues by 24% in the June quarter.

Risks and Valuations

Here, one of the risks for NVEC as a $232 million market cap company is a large billion dollar semiconductor play acquiring Everspin, or another competitor, thereby constituting a direct competitive threat for NVEC. Moreover, with technology evolving rapidly, there could be more competition from lower-priced sensors in a field where continuous development in PCB (printed circuit board) technology is leading to miniaturization or fewer components per square inch.

In response, in addition to quality, NVEC can rely on its rapidly evolving product pipeline which recently saw the introduction of a new Ultra miniature version of TMR (Tunneling Magnetoresistance) sensors which are two times smaller in size than the previous generation. Thus, the aim is to constantly innovate and maintain its niche status as a manufacturer of the smallest sensors to equip the tiniest medical or industrial robots, while keeping competitors at bay.

Consequently, the ingredients are present, not only to maintain but also to accelerate sales but, at a trailing price to sales of 8.59x , the growth metric has already been priced in. In this case and in line with the profitability rationale guiding this thesis, NVEC remains undervalued by around 30% when considering the trailing P/E of 15.5x. Adjusting accordingly, I obtain a target of about $61-62 (48.3 x 1.3) based on the current share price of $48.5.

Valuation metrics (www.seekingalpha.com)

In addition, the company has a lower price to cash flow metric despite paying these enticing dividend yields of above 8%.

Conclusion

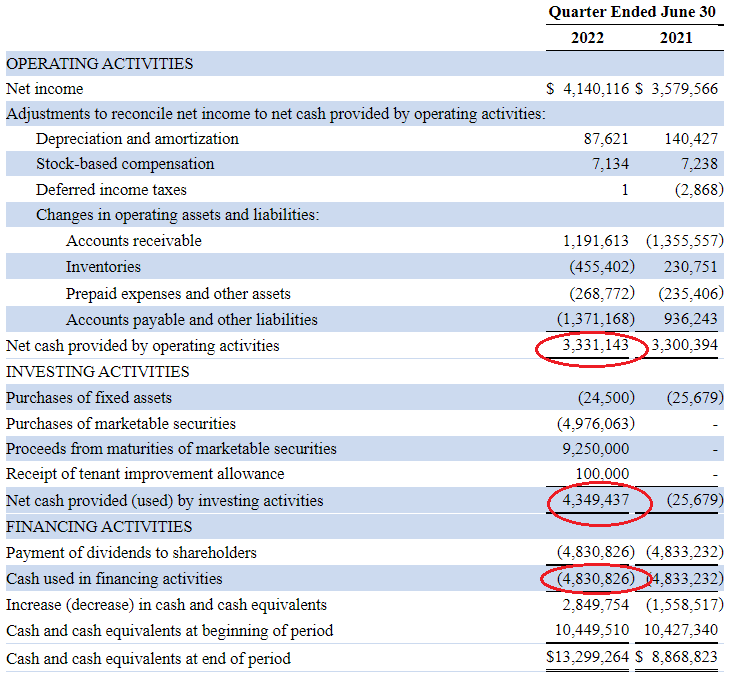

Now, the company paid $4.83 million in dividends to shareholders during the last reported quarter, which appears on the high side when considering that it generated only $3.33 million of cash. However, it produced $4.35 million from investing activities as shown in the table below. For this purpose, it earns interest income from securities as well as from the disposal of maturities. It has consistently paid quarterly dividends for the last ten years even during the pandemic.

{kind=link}

Looking deeper has a free cash flow margin of 27.75% (introductory table) which is excellent. Also, the company's profitability position is not under threat by the competition. On the contrary, with its shorter lead times, the spintronics play is gaining new customers from traditional electronics semiconductor companies as they face supply chain issues and want more innovative products.

Furthermore, coming back to the Capex/Sales metric, NVEC will invest around $1 million in additional production and testing equipment in the current fiscal year, which means that the percentage of its revenue spent as capital expenses should rise. In addition, as I mentioned above, it has built a large inventory and is seeing an improvement in its supply chain status.

Consequently, the factors which can generate more growth are present, but, when the effects of monetary tightening are felt more bitterly towards the beginning of 2023, it is more profitability and cash metrics that are likely to matter. Finally as shown in the balance sheet table above, NVEC has very little debt.

For further details see:

NVE Corp.: Low Growth, But Highly Profitable And Has The Cash To Pay Dividends