OSH - Oak Street Health And CVS Health: Potential Strategic Merger

Summary

- This is about a potential takeover in the primary healthcare space.

- Recently, media reports appeared that CVS Health Corporation is in talks to acquire primary care provider Oak Street Health, Inc.

- The transaction might be likely given broader industry consolidation trends, CVS Health’s strong interest in the primary care space, and Oak Street’s growth prospects.

- Meanwhile, Oak Street’s largest equity holders might be willing sellers given the company’s potential liquidity issues in the worsening macroeconomic environment.

- The reported target price is $40/share, implying a 33% upside from current levels.

Oak Street Health, Inc. ( OSH ) owns and operates primary care centers in the U.S. Late last year, the company appeared at the center of takeover rumors , with CVS Health Corporation ( CVS ) speculated to be among the potential buyers. This week, acquisition chatter resurfaced , as Bloomberg reported that CVS is exploring an acquisition of the primary care provider. Talks between both sides are reportedly ongoing and the agreement could be reached within weeks. The rumored price tag is $10bn including debt, implying $40 for each OSH share. OSH stock has jumped 33% since the rumors appeared, however, a substantial 33% upside to the target price remains.

While the setup is quite speculative and entails several risks (discussed below), there are several interesting aspects here suggesting the company sale might eventually materialize:

-

Buyout rumors come amid broader healthcare industry consolidation trends as healthcare insurers are scooping up healthcare providers. The healthcare industry has been increasingly shifting towards value-based-care model where healthcare providers are paid based on patient health outcomes. This contrasts with the traditional fee-for service model where patients pay for services provided. What’s important here is that, unlike in the traditional fee-for-service model, in value-based-care insurers (which pay for medical costs) have the same incentives as healthcare providers. This has naturally driven a number of mergers between healthcare providers and insurers. Recent examples include UnitedHealth (NYSE: UNH ) scooping up home care provider LHC Group (Mar’22), CVS buying healthcare platform-focused Signify Health (Sep’22) and Humana (NYSE: HUM ) acquiring home healthcare provider Kindred at Home (Aug’21). Given these industry dynamics, a potential merger would seem highly strategic for CVS Health. The acquisition would allow CVS to vertically integrate OSH’s primary care with the company’s health insurance, pharmacy retail and pharmacy benefits management businesses. Moreover, the primary care space has seen increasing M&A activity from retail-focused companies, including Amazon (NASDAQ: AMZN ) buying primary care provider One Medical (Jul’22) and pharmacy chain giant Walgreens Boots Alliance (NASDAQ: WBA ) acquiring majority stake in primary care-focused VillageMD (Oct’21). In Nov’22, Walgreens-controlled VillageMD bought primary/specialty/urgent care provider Summit Health.

- CVS has explicitly stated intentions to expand in the primary care space. As noted by CVS’ CEO during last week’s investor conference (emphasis added):

What I would say, I think we're very committed to that longitudinal relationship with customers. We believe that over the long term, having that -- primary care wields significant influence over the entire health care continuum, and we believe it's an asset that we want in our portfolio.

Worth noting that CVS previously raised three strategic expansion vectors, including primary care, provider enablement, and home healthcare. Apparently, with the acquisition of Signify Health, the company has significantly progressed towards completion of the latter two goals, suggesting a primary care-focused acquisition might be next. CVS’ CFO speaking about potential strategic deals in Nov’22 (emphasis added):

I would say it would most likely be something that had the primary care or the clinical care capacity to it. It could have other elements of home and things like that. But again, if you go back to those 3 boxes, we've at least checked in some way, 2 of them. And I think that would be the third leg of the stool and thus has a lot of prioritization. Now going forward, we could do other deals in those other areas as well. But when I really think about kind of the gating element and moving the strategy forward. It's really more in the clinical care primary care area.

As an indication of CVS’s interest in the space, the company recently announced a $100m investment in primary/urgent care provider Carbon Health. It is worth noting that OSH is one of the few independent large value-based primary care providers in the US, thus narrowing down the range of potential M&A targets for CVS.

- OSH might be an attractive acquisition target for CVS given its large expected growth runway. While OSH has compounded its topline at a solid 58-75% annually since 2017, significant further growth is likely to continue. OSH still captures a small (<1%) market share in the large ( $356bn TAM ) Medicare market which is still predominantly based on the legacy fee-for-service model. As noted by OSH’s CEO (emphasis added):

I think some of the keys to what we do here at Oak Street Health is it is still a large and unpenetrated market opportunity. And obviously, over the last couple of years, there has been more and more value-based care entrance into the space. But the reality is the vast majority of older adults are still cared for by kind of more traditional doctor's office or frankly going to the emergency room for care because they can't find a doctor. And so we feel like we're still in the very early innings of our broader industry, and certainly, Oak Street growing, building out and scaling.

- OSH’s largest shareholders might be willing sellers here, given recent macroeconomic headwinds coupled with the business’ significant cash burn. Since 2015, two private equity firms General Atlantic (26% ownership stake) and Newlight Partners (17%) have been OSH’s largest shareholders. Worth noting that these PE firms have already trimmed their stakes from 32% and 21% respectively in 2021. Meanwhile, OSH is still unprofitable on EBITDA level and the management expects to reach break even only in 2025. OSH has shown significant operating losses recently - $414m in 2021 and $334m 2022 YTD. The company currently has $562m in gross cash + marketable securities while having $977m in long-term debt. These facts suggest OSH might very well need to pursue another equity and/or debt financing in the foreseeable future. Given the toughening financing environment and large liquidity resources of CVS ($41bn in gross cash + investments as of Q3’22), the two PE equity holders might not oppose the company sale.

A quick glance at relative valuation shows the acquisition at the reported price would value OSH quite generously. At $40/share, OSH would fetch a 4.7x 2022E revenue multiple - this compares to the current 3.6x. For reference, a similarly-sized competitor AGL currently trades at 2.6x 2022E sales. Another data point is Amazon’s acquisition of One Medical, valuing the target at 3.5x. Worth noting that OSH has been the fastest growing among the bunch, with 58-75% growth since 2019 compared to 50-53% for AGL and 30-64% for ONEM. Having said that, OSH’s business is somewhat of a black box to me and the valuation premium might in fact be warranted.

Business

Oak Street Health owns and operates 169 primary care centers. The company provides healthcare services to older adults, with a focus on Medicare population. Most of OSH’s revenues come as a percentage of premiums paid by insurers to the US Center for Medicare and Medicaid Services (abbreviated CMS). The company works with a number of insurers (i.e. payers), with the largest revenue share coming from Humana, WellCare/Meridian and Cigna HealthSpring (62% of capitated revenue in 2021). Worth noting that OSH boasts a highly recurring revenue base given multi-year contracts with health insurers.

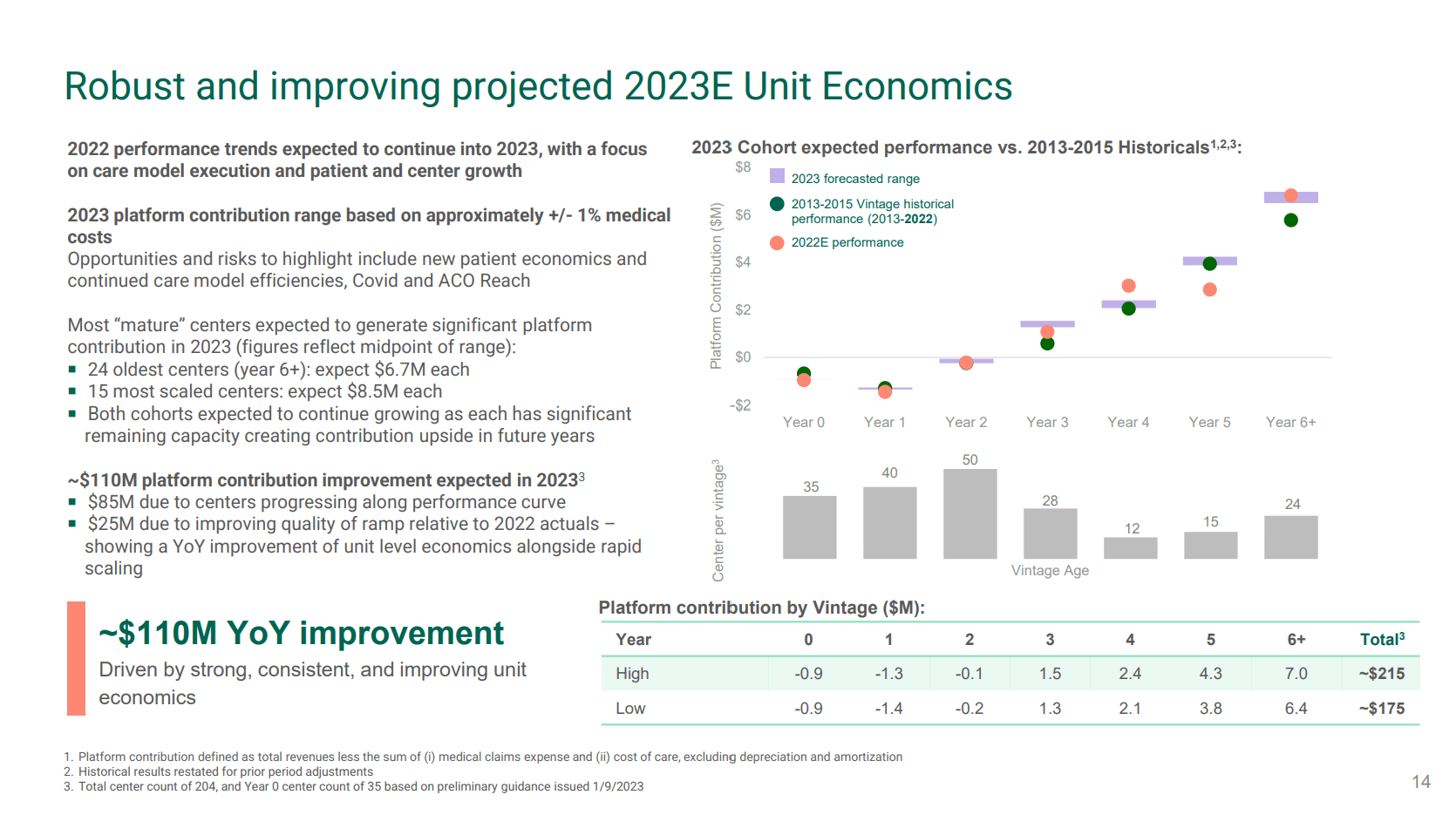

The management has noted that profitability of each center improves as they mature (which the company states is 6+ years). This is achieved as OSH provides sufficient level of healthcare to patients in early years which then allows for lower medical costs in later on. In other words, by investing more in keeping patients’ health upfront, the company is later able to avoid expensive hospitalization expenses. This allows each center to bring more in what the company refers to as “platform contribution” (total revenues per center less medical claims expenses and cost of care) as they mature, leading to higher margins and profitability. The management has estimated the embedded adjusted EBITDA - which displays how much earnings primary care centers are expected to generate once they mature - at $1.4bn at the end of 2023. This assumption is based on $8.5m in platform contribution from each center less $1.5m in SG&A per center multiplied by 204 - the expected number of primary care centers operating by the end of 2023.

Oak Street Health, J.P. Morgan Healthcare Conference, January 9, 2022 Oak Street Health, J.P. Morgan Healthcare Conference, January 9, 2022

{kind=link}

{kind=link}

Risks

Downside to pre-announcement prices is 25%. Below are main situation-related risks:

- A potential transaction would likely be tightly scrutinized by antitrust regulators, including the FTC and/or DOJ. Having said that, OSH occupies only a negligible share of the US Medicare Advantage market. Meanwhile, CVS’s presence in the primary care space is still insignificant. As discussed in my analysis of the SWIR-SMTC merger, the regulators have mostly blocked mergers on horizontal overlap grounds, with only a handful of transactions blocked on vertical integration basis. Nevertheless, any regulatory pushback might prolong potential merger closing timeline.

- Given that CVS walked away from CANO acquisition, there is a similar uncertainty regarding the insurer’s talks with OSH, potentially implying a significant downside in case the takeover talks break. However, CANO acquisition talks might have been terminated due to the right of first refusal held by one of CVS’ competitors, Humana - something that does not apply to OSH.

- There is a risk of OSH’s management not agreeing to a company sale. During the previous round of rumors, OSH’s CMO came out , arguing that the company had no interest in a potential takeover. However, given a potential substantial premium to current price and the deteriorating macroeconomic environment, OSH’s leadership might potentially be willing sellers.

For further details see:

Oak Street Health And CVS Health: Potential Strategic Merger