NEX - Oil States International: The Macro Backdrop Is Strong But Q2 Execution Was Poor

2023-07-28 14:26:11 ET

Summary

- Oil States posted disappointing earnings, attributing it to execution issues and one-time events.

- The company's backlog has increased and the macro backdrop remains favorable, especially offshore.

- I will look to Q3 for an update, but in the meantime, I think Oil States is no longer a strong buy.

Investment Thesis

Oil States International ( OIS ) posted disappointing earnings and the market's reaction was harsh:

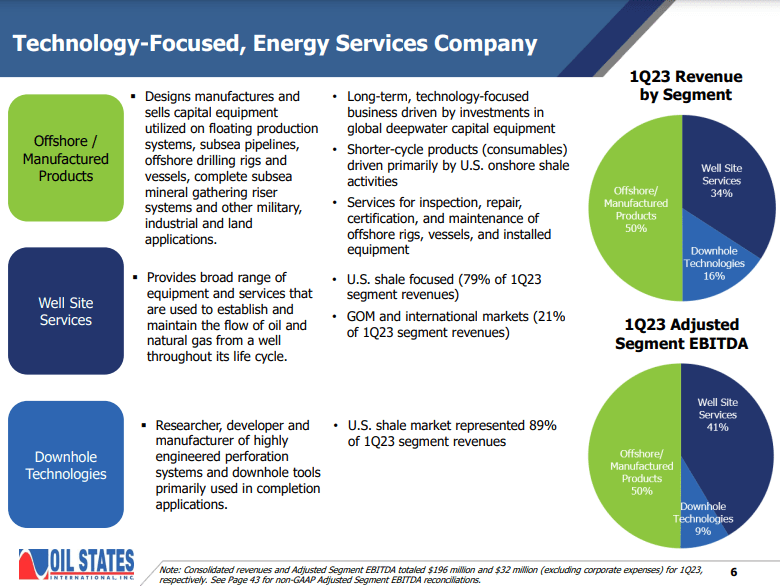

The macro backdrop remains strong as the company is more than 50% exposed to the offshore sector, which is undergoing a secular bull market :

{kind=link}

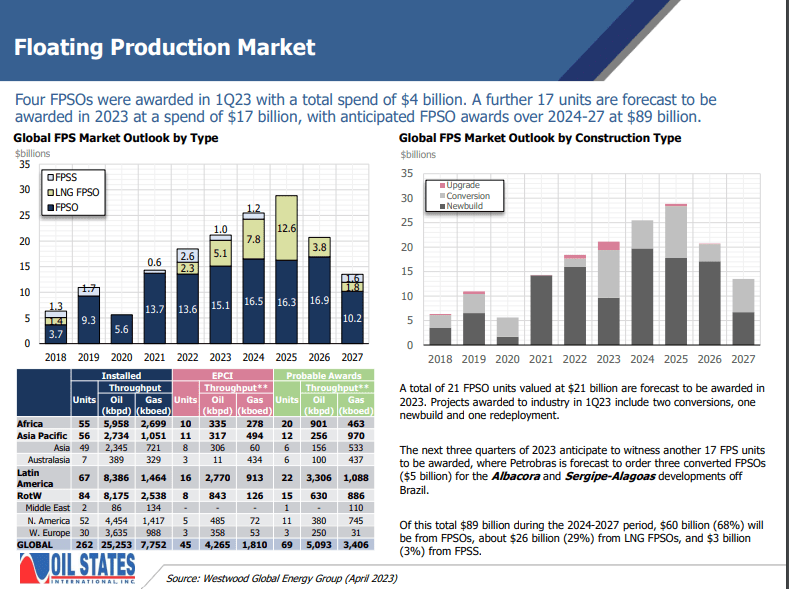

Floating production systems are an important driver for Oil States' revenue and the pipeline looks strong:

{kind=link}

In fact, OIS increased its offshore backlog in Q2:

Backlog totaled $338 million as of June 30, 2023, an increase of $12 million, or 4%, from March 31, 2023 and $97 million, or 40%, from June 30, 2022. The current quarter-end backlog is at its highest level since December 31, 2015. Second quarter 2023 bookings totaled $106 million, yielding a quarterly book-to-bill ratio of 1.1x (1.2x year-to-date).

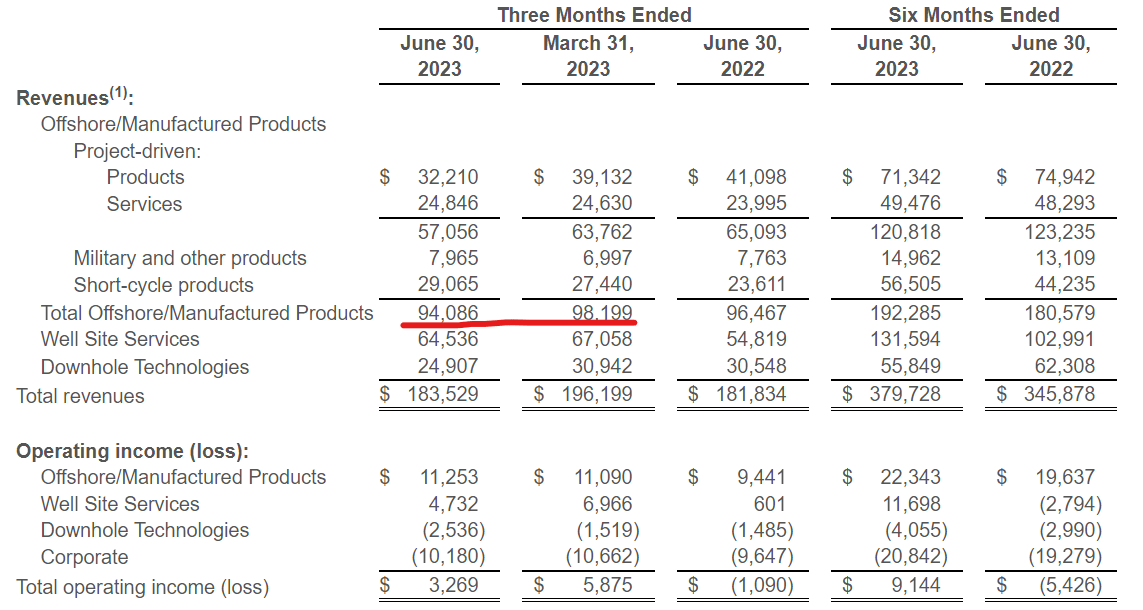

However, management failed to convert the backlog into revenue:

{kind=link}

Despite all offshore bullishness from oilfield services bellwethers SLB ( SLB ), Baker Hughes ( BKR ) and Halliburton ( HAL ), Oil States managed to post a sequential decline; offshore revenue was even below Q2 2022. Management essentially attributed this to execution issues.

For now, I remain bullish on the company given the strong macro backdrop and management's reiteration of its 2023 EBITDA guidance of up to $100 million. However, I think it's appropriate to adjust my rating from "strong buy" to "buy." I will wait until the Q3 update to decide if OIS will remain a long-term investment for me.

The Good: Strong Macro Backdrop

Oil States' management largely agrees with the bullish sentiment in offshore and international markets:

We have begun to see an inflection upward in international and offshore markets, which will further support our product and service offerings in regions outside of the United States.

Like SLB, BKR and HAL, Oil States is at the start of a multi-year capex cycle:

We are now experiencing an increase in investments in long lead time projects in international markets and deepwater basins around the world based upon the longer-range outlook for commodity prices. Strong macro fundamentals are pointing to a multiyear up cycle which will drive growth in revenues, earnings and free cash flow generation.

This aligns nicely to Oil States' competencies and OIS also benefits from alternative energy investments in offshore wind:

We continue to bid on potential opportunities supporting our traditional subsea, floating and fixed production systems, drilling and military customers while also bidding to support multiple new customers and projects involved in development such as subsea minerals gathering fixed and floating offshore wind developments and other renewable and clean tech energy systems globally.

Similarly to what other oilfield services names are reporting, OIS also ran into headwinds in North America onshore. While CEO Cindy Taylor didn't go as far as pressure pumpers Liberty ( LBRT ) or NexTier ( NEX ) to "call a bottom", she did suggest the worst may be over:

Obviously, we've had softer rig count down about 13% on land with completion comp down about 8% or so. And so we're really not projecting a recovery off of that of the second half of the year at this point in time. Although based on customer conversations, we do sense that there's really not a leg down from here, in our view.

However, unlike other onshore services providers who were flat or modestly down on sequential basis, Oil States' Downhole Technologies revenue (U.S. shale is 89% of this segment) collapsed by 20% QoQ and is also 20% down from Q2 2022.

The Bad: Execution Problems

Management attributed the disappointment to various execution problems that ultimately prevented the company from converting backlog into revenue.

On the offshore side:

Activity in the Gulf of Mexico this quarter was tempered by several third-party intervention vessels temporarily out of service due to dry docking with one returning to service in the second quarter and one is scheduled to return to service in the third quarter.

Sounds like management is blaming a third-party. Unfortunately, not much detail was disclosed, but it looks like a project where OIS is one of several suppliers to the customer and another supplier's delays bottlenecked OIS' ability to deliver. If management's version is correct, we should see Q3 make up for the delayed revenue.

Apart from the U.S. GoM, OIS did mention improvement though:

On a positive note, results for the segment's international operations improved sequentially driven by higher customer activity levels.

On the onshore side:

And to some degree, our softer Q2 for Well Site I could say it's somewhat timing in the sense that we had a large customer in the Northeast. We went from a 12-well large multi-well pad and then you have transition times between a new pad.

Here management blames "timing." It sounded like the idle transition time wasn't due to Oil States' fault, but again, not much detail was shared.

Both on the offshore and onshore side, the revenue slowdown appears to be due to one-time events. Management implied these events were beyond its control. I don't have information to conclude otherwise, but if Management's explanation is correct, we should see this being made up for in Q3.

OIS also stands by its earlier EBITDA guidance, despite these mishaps:

Despite sequentially weaker second quarter revenues and EBITDA, we confirm our full year guidance of $92 million to $100 million of EBITDA based upon expected contributions from the ongoing recovery in offshore and international drilling and development.

For further details see:

Oil States International: The Macro Backdrop Is Strong But Q2 Execution Was Poor