IFNNY - ON Semiconductor: Successful Transformation And SiC Rollout Make It A Buy

2023-09-22 10:16:29 ET

Summary

- Following a slim down of the business, ON Semiconductor is excellently positioned to capitalize on high-growth opportunities in automotive and industrial end markets benefiting from several megatrends.

- Strong margin expansion since Management takeover, high trajectory in the rollout of 3rd generation SiC chips and best-in-class financial metrics give ON an edge against competitors.

- FAB LITE model and positioning in more resilient end markets have enabled the company to navigate the downcycle and inventory buildup in semiconductor markets to a better extent than competition.

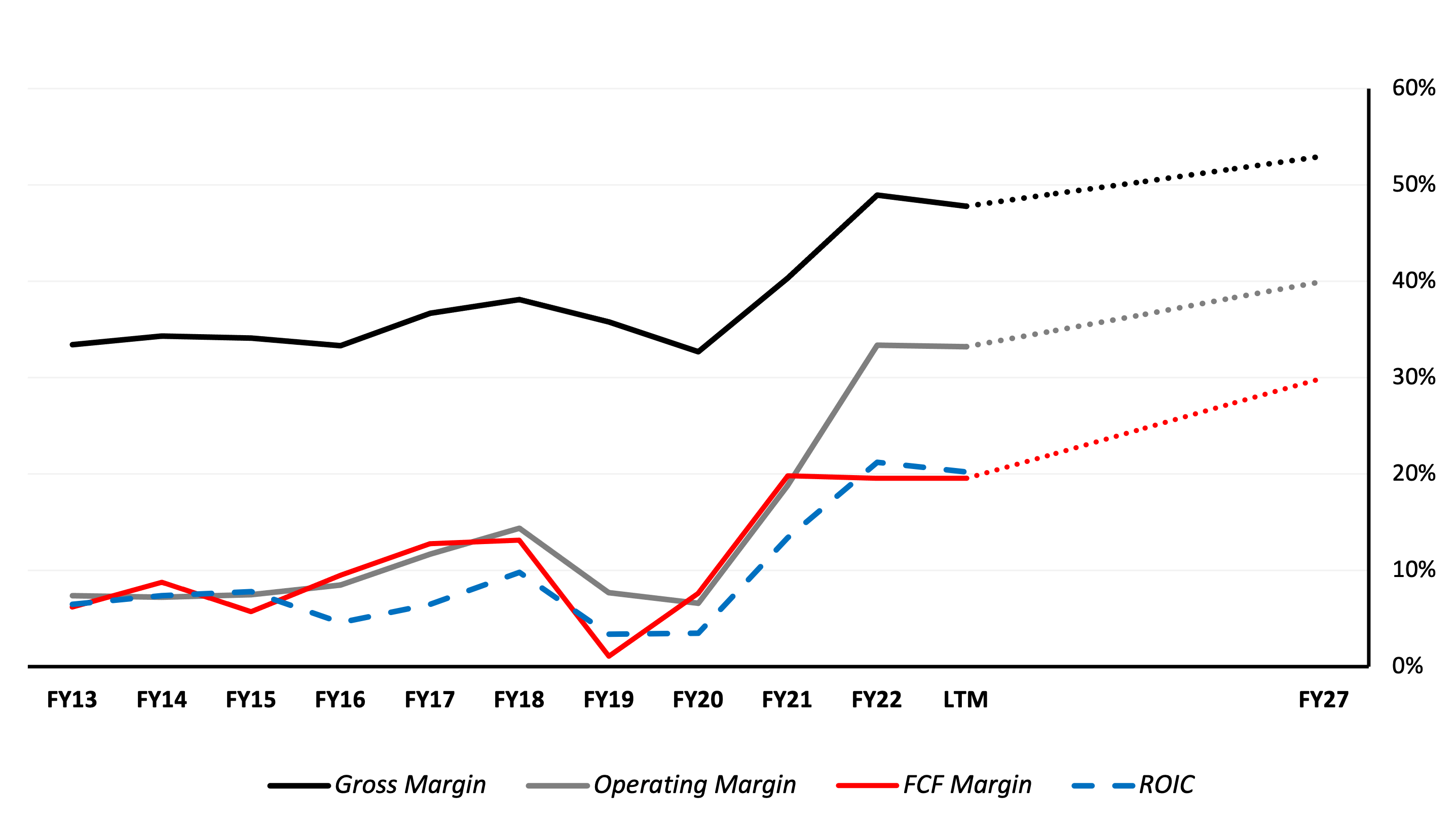

As part of their 2023 Analyst Day, ON Semiconductor ( ON ) management has revealed their new midterm guidance until FY27. In terms of revenue, management aims to grow at a CAGR of 12%-10%. Significant margin expansion of the last years is to be continued with gross margins reaching 53%-50% (FY22: 49%), operating margins rising to 40%-35% (FY22: 33.4%) and FCF margins climbing to 30%-25% (FY22: 19.6%). Although this will certainly present a challenge, I am confident in management to achieve these targets given the strong competitive position and high growth potential, they have navigated ON into and therefore rate it a BUY with a Price Target of $118.

Key Investment Thesis

Successful strategic Transition with Focus on strongest Market Opportunities to achieve above Market Growth

Since management changed in 2020, ON underwent a gradual transformation to a leaner business model focusing on high-value-add innovation in automotive (50% of revenue) and industrial (28%) end markets which are projected to have the strongest and most resilient growth. Divesting non-core lower margin business such as volatile consumer together with strong post-Covid demand lead to a strong expansion in margins and industry leading Returns on Equity, Assets and total Invested Capital, this transition is still ongoing and will help drive further margin expansion.

Reuters Eikon / ON Financial Results ON vs. Peers (Calculated by the Author using data from ON's Financial Results)

{kind=link}

Automotive - Semiconductor count in EV more than double that of an ICE due to chip adoption in power electronics including Onboard Chargers, Converters and Battery Management Systems. Additional tailwinds comes from sensing solutions and ADAS systems, a segment where ON currently holds 46% market share making it the #1 globally. Various independent research firms estimate growth CAGRs of around 10- 15% .

Industrial - Machine Vision, Automation and Industry 4.0 as well as new green energy infrastructure are ON's key areas of focus here. Once again the company can directly benefit from the IRA which allocated enormous resources to the expansion of US sustainable grid infrastructure.

Across all end markets, I find ON management guidance of 10-12% of revenue growth CAGR to be realistic and achievable given the high growth trajectory that these markets are in, barring any unforeseen events.

FAB LITE model enables higher Margins and Cash Generation

Since 2020, management has implemented a FAB LITE model which focuses on efficiency and lower costs. Underperforming fabs were divested and focus on high ROIC ones provides ON with higher margins and more resilience in cycle downtimes due to less fixed costs and a leaner asset base. To ensure demand flexibility through the cycle, non-propriety tech can be outsourced to flex capacity while internal fabs are aimed to be constantly operating at max utilization. After the successful launch and completion of the FAB LITE model, ON is currently transitioning to a FAB RITE model which includes strategic brownfield expansions in various countries (incl. the US, Europe and Korea) to drive SiC rollout. Brownfield model (which refers to capacity expansion in an existing asset rather than constructing a new asset from scratch, referrerd to as Greenfield) allows for less upfront capital spending and faster time to market (about 2Y). In setting up these projects, ON has been successful in negotiating a high share of customer co-investment to further lower own risk and enhance ROIC. Once again, ON will be a direct benefactor of the CHIPS act and its equivalents in the US, EU and Korea that provide attractive subsidies for chip manufacturers to incentivize domestic manufacturing and protect crucial technology IP.

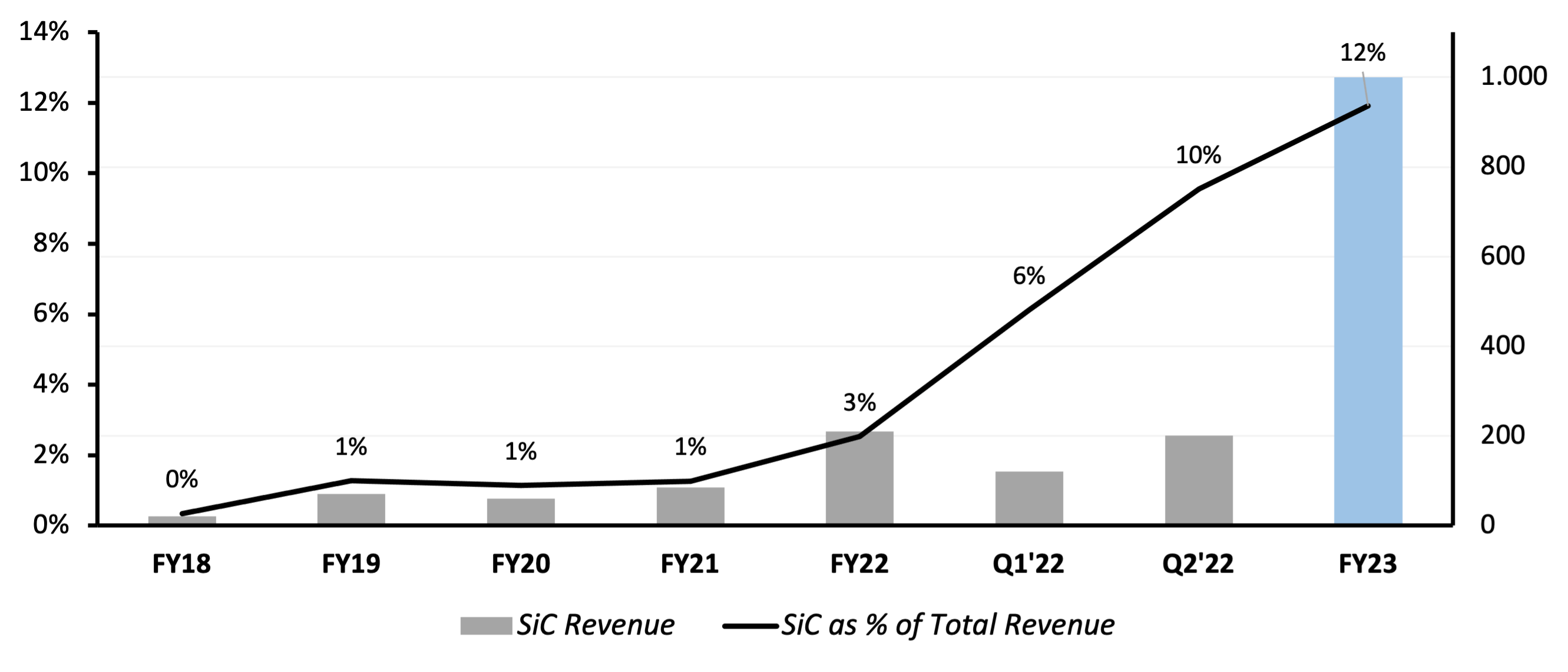

Global Leadership in new Generation SiC Chips to expand Margins going forward

Management's strategy aims to capitalize on innovation in SiC chips in which ON is already one of the global leaders at 14% market share, targeting a 2027 market share of 40%. Silicon carbide (SiC) is a 3rd generation semiconductor material which, compared to 1st and 2nd gen has a much better profile when operating at high voltages and powers, making it ideal for application in power electronics and grid electrification appliances. Per ON's guidance, 50% of wafer material for SiC chip manufacturing is to be internally sourced which is poised to benefit margins as scale effects and overall higher margin SiC chip rollout expands at rapid pace (management expects SiC market to grow at a CAGR of 33% until 2027 to then represent around 30-40% of total semiconductor market share).

Calculated by the Author using Data from ON's Financial Results

{kind=link}

The company is currently on track to reach and possibly exceed its SiC revenue target of $1bn in FY23, customers are highly confident (during Q2’23 $3bn of LTSA signed including $1.9bn Visteon and $1bn BorgWarner contracts for total SiC LTSA amount of $11bn currently accounting for more than half of total LTSA volume).

Furthermore, recent LTSA wins with high end OEMS (BMW, Mercedes Benz, Jaguar Land Rover) with higher margins and semiconductor volume per car as well as rapidly growing Chinese EV players ((BYD)) give ON an edge against SiC competition winning entry level EV contracts (i.e. STMicroelectronics ( STM ) and Infineon ( IFNNY ) with Hyundai and GM).

Experienced, Shareholder committed Management Team and good Resource Allocation

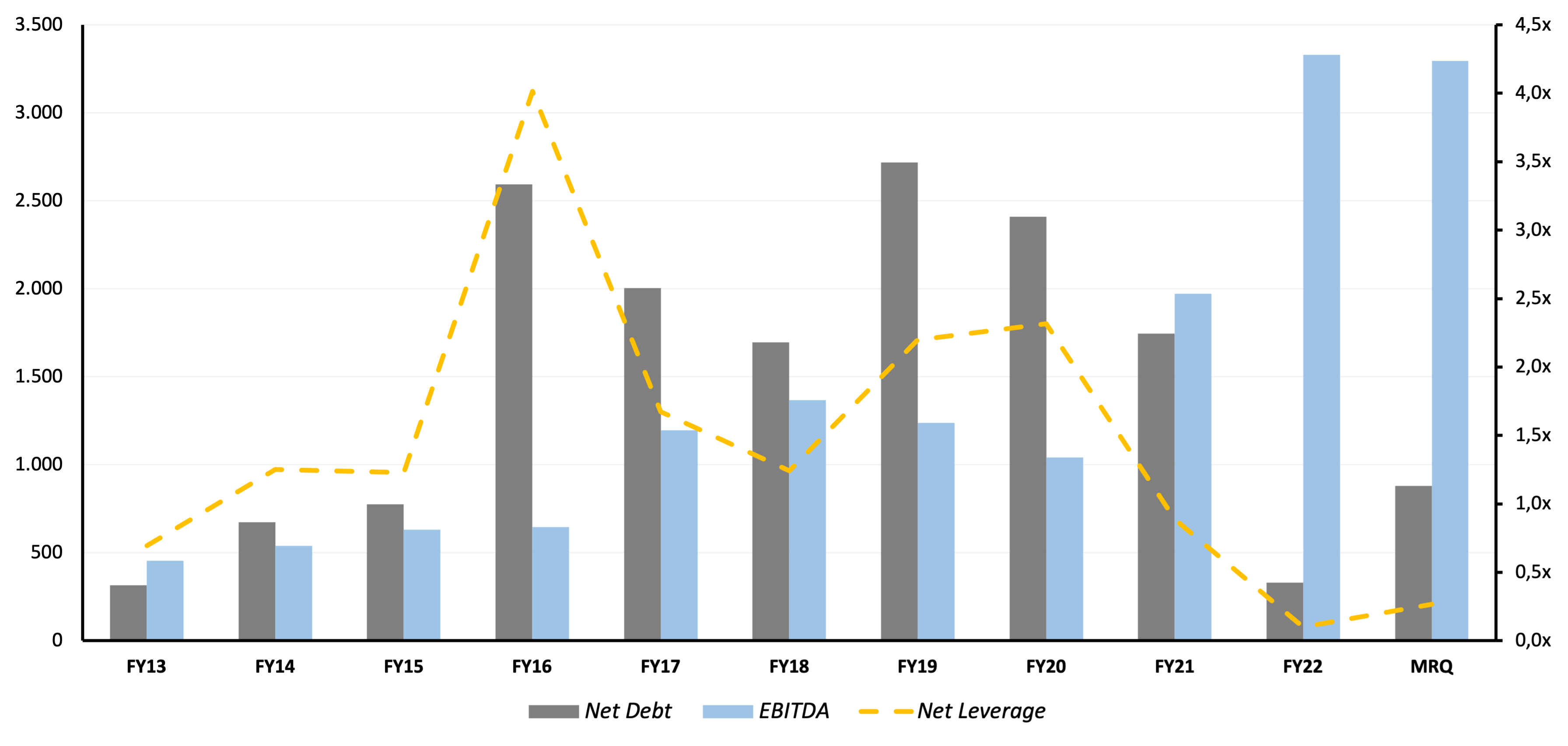

ON currently has a net leverage of 0.3x with a BB+/Ba1 credit rating. Strong cash generation following Covid-19 was strategically used to delever and buy back shares. Midterm guidance aims for 50% of FCF to be returned to shareholders with share buybacks of $3bn authorized until 2025. The company does currently not pay out a dividend which I do not see as a problem given the high amount of buybacks. Especially for players like ON which operate in highly cyclical markets and disruptive technologies, I feel this is the better approach of distributing money to shareholders given the higher flexibility of share buybacks compared to fixed quarterly dividends.

Calculated by the Author using data from ON's Financial Results

{kind=link}

S&P 500 and NASDAQ 100 inclusion provides Visibility

Recent inclusion in US benchmark indices provides higher visibility to both investors and potential customers as well as additional flow of capital via passive index tracking products.

Possible Risks

China Risk

China is a significant factor in ON's business with a significant amount of sales there and several key customers located there (ON does not report China sales directly, I estimate it to be around 20%). Further sanctions could hurt ON’s business there significantly, however, the company does not face a serious production risk related to China given that only 6% of firms assets are located there and almost all of its manufacturing and designing capacity is located in the US or its allies.

Exit of GaN Business can hurt Revenue in the long Term if GaN proves superior to SiC

ON sold its GaN business in 2022 while competitor Infineon has just announced to acquire GaN systems for a total value of $830MM. Should GaN based semiconductors prove to be more efficient, ON might face the need for high catchup M&A or R&D costs. However, as of current, GaN application seems more headed towards consumer making ON’s exit aligned with their market focus. This does remain something to be monitored however as both technologies are still in their early stages and thus it cannot be ruled out that other significant opportunities related to them might arise.

Current Downcycle and Inventory Buildup in Semiconductor Markets due to global Economic Downturn

By nature, ON has a relatively cyclical business model, although it has so far been able to navigate current times better than some of its peers due its FAB LITE model and its main sectors of exposure (i.e. 2022/23 saw a weak consumer but automotive and industrial end markets continued to be strong).

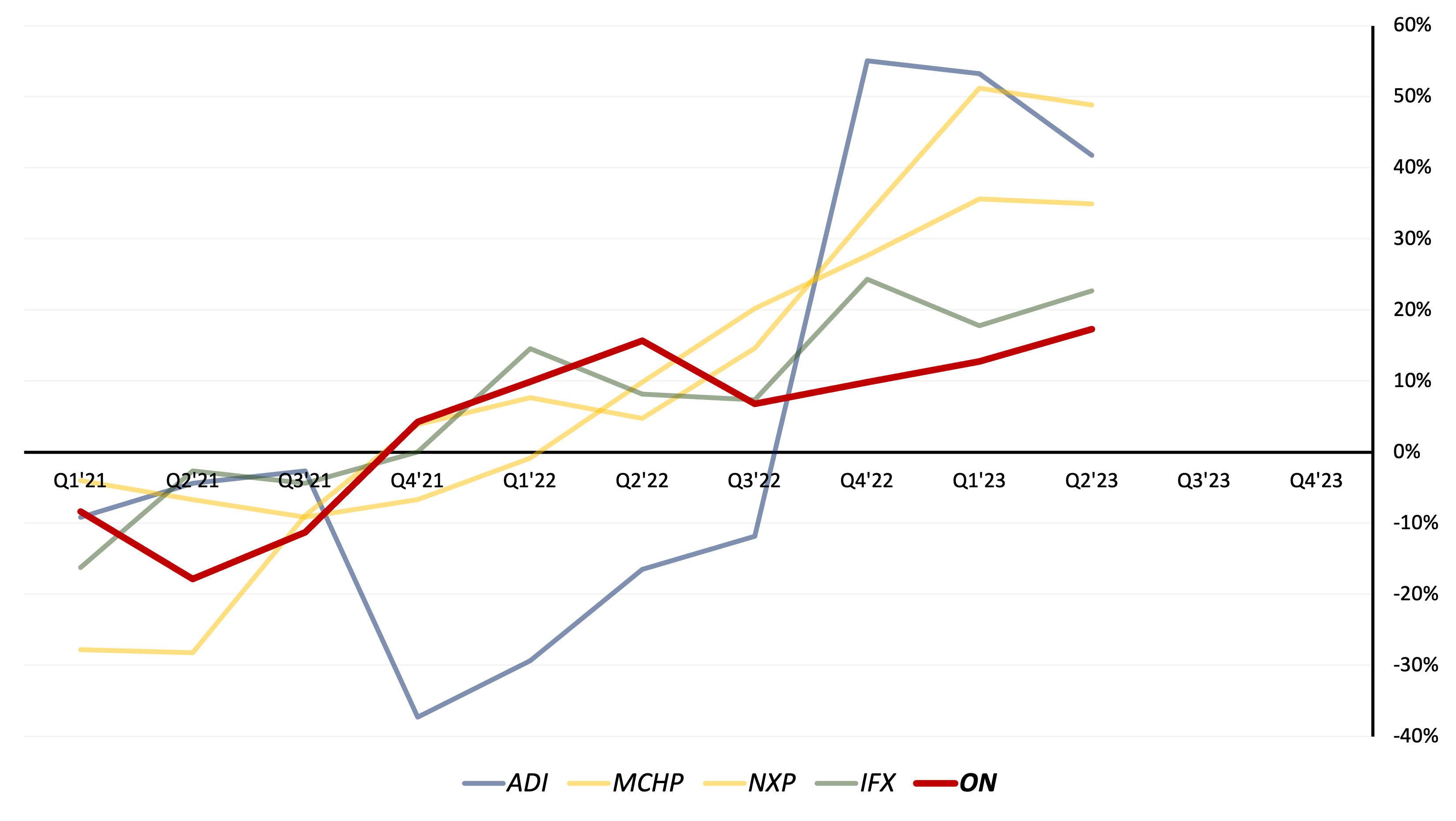

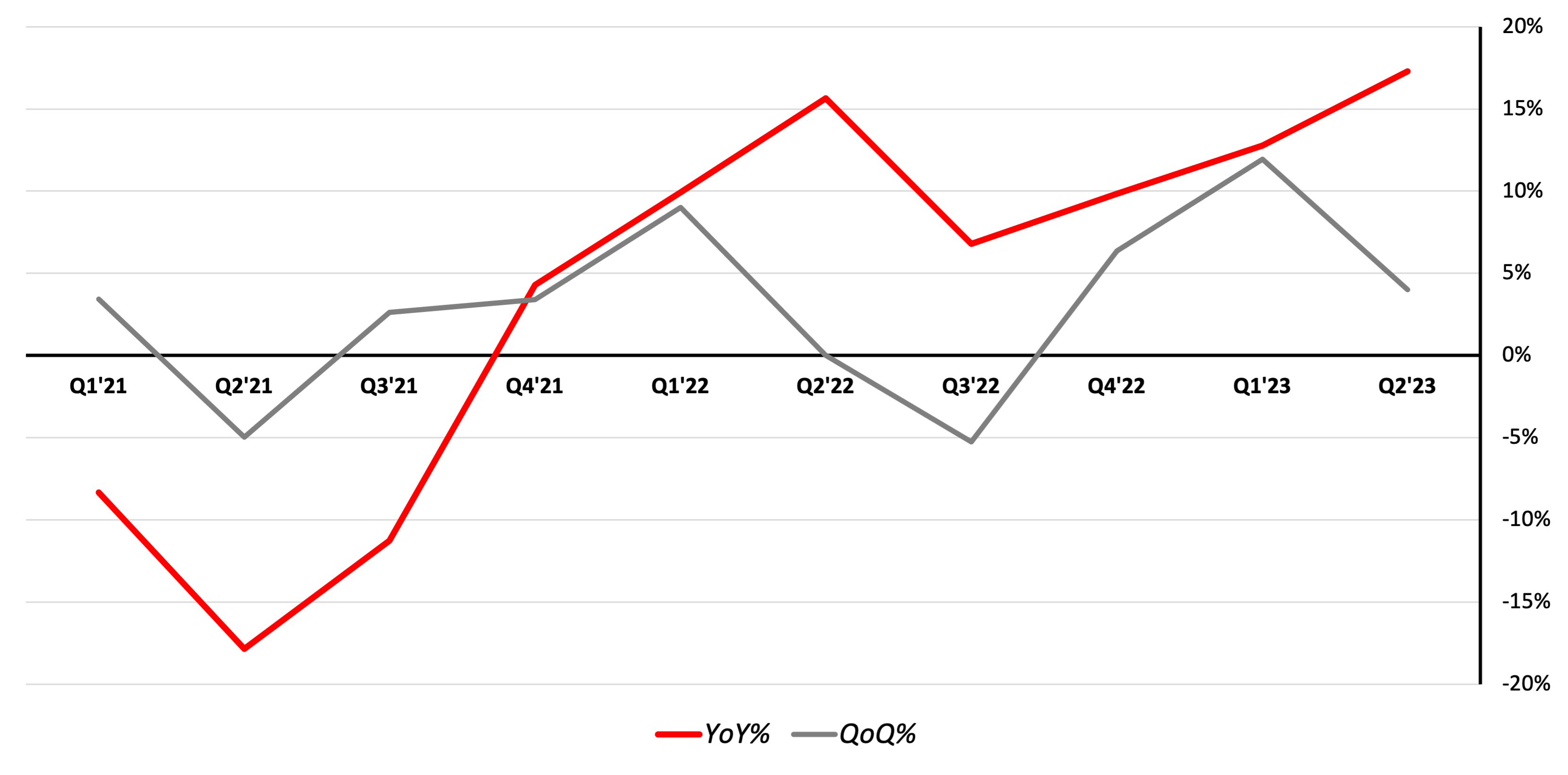

Inventory buildup continues to be an issue in the semi industry after customers overordered into an economic downturn due to supply chain issues following covid lockdowns. ON had less buildup in inventory vs peers, however YoY change has not peaked yet as for some competitors, QoQ shows deceleration supporting estimates of current inventory correction having peaked in most markets with US economy less likely to enter recession and PBOC stimulus raising hopes for China recovery.

QoQ% in Days Inventory Outstanding for ON and Peers (Calculated by the Author using data from ON's Financial Results) ON QoQ% and YoY% in DIO (Calculated by the Author using data from ON's Financial Results)

{kind=link}

{kind=link}

Despite ON showing a lower surge in inventory buildup compared to peers, a sudden worsening in global economic conditions including continued weak data from China poses the most significant risk to my investment case in the near term.

Valuation

I value ON using a 5Y-DCF model with three Scenarios, reflecting upper, mid, and lower end of management FY27 guidance with linear growth in revenue and margins until FY27 assumed and midpoint of guidance as base case. For depreciation I assume a rise from currently 6% to 8% of revenues p.a. reflecting the current FAB RITE expansion.

I use a WACC of 12.4% (calculated with ß of 1.75 and current interest rates and MRP for the US) and a conservative exit EV/EBITDA multiple of 11.5x FY27 (ON 5Y TTM average). I opted for an Exit Multiple approach instead of an infinite growth method due to high level of disruption in the Industry which I feel makes an infinite planning horizon inadequate. Scenarios are weighted at Base 40%, Bull 40% and Bear 20% respectively and result in $116, $128 and $105 of fair value per share. Taking the blended average I obtain a fair value of $118 per share implying a roughly 27% upside to current (Sep 15) price level.

ON Semi DCF (Company Filings and Authors Projections)

Multiples analysis of ON and peers shows that the company is currently trading at a premium in both P/E and EV/EBITDA except for ADI . This in my opinion is justified however given ON’s strong recent growth in attractive and resilient end markets, fortress balance sheet and best-in-class ROIC along with a management that has a strong track record of delivering since taking over in 2020. When also taking into account growth estimates, ON trades at highly attractive growth adjusted multiples compared to its peers, indicating a current undervaluation relative to the sector, especially considering its advantage in profitability.

Calculated by the Author using data from ON's Financial Results (Note: Growth Rate reflects Analyst Consensus)

Wrap-Up and Outlook

As laid out above, I think ON provides investors with a highly attractive business model that focuses on above-average growth markets and disruption in 3rd generation semiconductors. Recent management initiatives have benefitted profitability sustainably and brought down leverage to the lowest in years, suggesting a high degree of financial flexibility. Still, investors should closely monitor macroeconomic conditions and related inventory management at ON as despite having experienced a less steep buildup than peers, YoY does not seem to have peaked yet.

As for upcoming Q3 earnings on October 29, in my opinion there are 2 key areas investors want to focus on:

- Growth in SiC - Actual vs Estimate, margin development (profitable in Q2, is this temporary or sustainable?), FY24 guidance

- Inventory Buildup - This is perhaps even more crucial, we have seen a decline in QoQ% for Q2, if this is a continuing trend it could mean that YoY% might peak soon. Similarly, another uptick could signal pain ahead for investors.

For further details see:

ON Semiconductor: Successful Transformation And SiC Rollout Make It A Buy