AMZN - One REIT To Buy For The Office Property Recovery And One I Would Avoid

2024-01-21 08:00:00 ET

Summary

- In this article, I discuss one office REIT to avoid Easterly Government Properties and one to buy Cousins Properties Incorporated.

- Using FFO, Core FFO, and AFFO metrics, DEA's payout ratios are well above 90%, putting the dividend at risk.

- Cousins Properties' properties are in fast-growing cities in the Sun Belt market and the REIT boasts on the lowest payout ratios in the sector.

- If interest rates remain elevated, this will continue to suppress office REIT prices in the meantime.

- Because of office property REIT headwinds, both are currently trading at attractive valuations, indicating they're undervalued.

Introduction

The pandemic in 2020 changed a lot of things. The way we as consumers look at everyday life to the way companies conduct everyday operations. One of the most notable things COVID changed was the work landscape, especially for office REITs. Some have recovered somewhat but are still down because of the uncertainty surrounding the work environment.

Some businesses have required their people back to work while some have adopted a hybrid work schedule for their employees. I've read that some companies are requiring employees back to a normal office work schedule in the next 12-14 months, discussed later in the article.

On the other hand, I've also spoken to some friends and family who are still on the hybrid schedule and have no time frame in sight for returning to the office full-time. Until there's more clarity, I think office REITs will continue to see suppressed share prices.

Because of this, there are some that are very attractive if you believe in their long-term outlook. But all are not created equal. In this article, I give you one to consider and one to avoid.

Avoid: Easterly Government Properties ( DEA )

I can understand why some may think Easterly Government Properties is a safe bet for the office REIT recovery. I mean they lease office spaces to the government! And nothing is safer than renting to Uncle Sam, right?

That's somewhat false. DEA leases to laboratories, VA outpatient clinics, courthouses, different military branches, and the FBI. While the government is probably safer than renting to some unknown, less credible tenants, they also have a lot of bargaining power being the government.

I can tell you as a government employee for 21 years, we have a lot of bargaining power. We're likely to pay our rent on time, but we have no problem getting up and moving at the drop of a dime. And it's easy because we have no problem finding someone willing to lease to us.

We also are culprits of cost-cutting. The government will cut costs quickly to free up capital and one way it does this usually is by downsizing, moving, and leasing cheaper buildings, even if it's not better suited. In short, the government is cheap, especially when it comes to things like this.

If you've had the luxury of seeing/visiting a lot of military bases, quite a bit of them is in not-so-great areas. That's because the real estate is cheap there, and we just need something for the time being to get the job done. So, it's not as safe as you may think.

Something Positive

The good thing about DEA is that they do rent to the government and 97.5% of their properties were leased at the end of Q3. Additionally, their portfolio was 100% occupied and their lease agreements are typically longer. Their debt maturities are also well-laddered with a minimal amount of debt maturing this year. This also had a weighted average interest of 4.05% which is not bad considering current interest rates are higher. One hundred percent of their debt is also fixed-rate.

{kind=link}

Highly Leveraged

Even with their well-laddered debt maturities DEA is highly leveraged at 6.7x. Although REITs use a lot of debt to fund growth, this is quite high for a REIT. A good measure is around 5.5x or lower, which I prefer to see. To give them credit, they have been focusing on deleveraging over the fiscal year. This stood at 7.1x in Q1 so they have been decreasing quarter-over-quarter.

Slow Dividend Growth

Easterly Government Properties' dividend growth has also been disappointing over the years. Although they didn't cut during the pandemic, the dividend has only grown from $0.25 to $0.2650. One reason for this is likely the high payout ratio DEA currently has, and the main reason I think the REIT is one to avoid.

However, they did raise full-year FFO guidance by a penny to $1.13 to $1.15. Furthermore, FFO has been flat all year at $0.29. At the end of Q3, DEA's FFO for the year was $89.1 million and dividends paid were nearly $83.8 million. Although REITs pay out a lot of their cash in dividends, this gives DEA a payout ratio of nearly 94%.

This means the company retains less cash to reinvest back into itself. Some prefer to use AFFO or adjusted funds from operations while some prefer to use FFO. AFFO is considered the better metric because it subtracts CAPEX and straight-line rents.

But some don't prefer to use AFFO as a measurement because it's also subject to manipulation. But as a quality company, it's in the best interest of the REIT to report correct numbers. Even if you used AFFO or core FFO, DEA's payout ratios would still be elevated at 96% and 93% respectively.

Buy: Cousins Properties Incorporated ( CUZ )

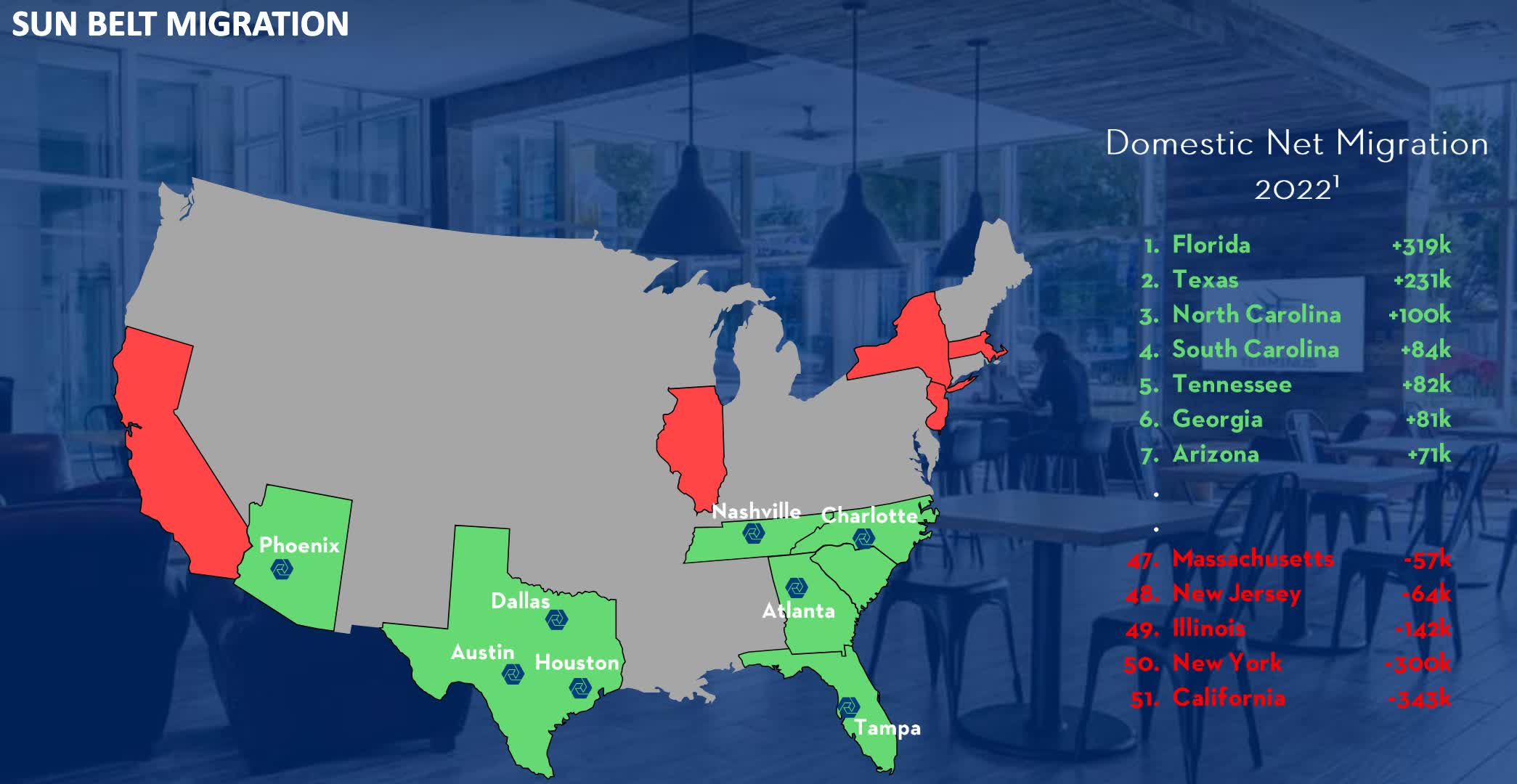

One REIT I think is poised for a nice rebound after the office property recovery is Cousins Properties. The office REIT leases office properties in the attractive Sun Belt market in growing states like Texas, Florida, and Georgia.

Some of their tenants include powerhouses like Amazon ( AMZN ), Meta Platforms ( META ), and Bank of America ( BAC ) to name a few. Because CUZ owns properties in the growing Sun Belt region, the REIT has benefitted from this growth over the years with the influx of jobs and residents.

More recently residents have been migrating from expensive places like California and New York to less expensive cities in states like Texas, Florida, & Arizona and cities like Charlotte and Nashville.

{kind=link}

Something investors may find to be a deterrent is the company's decline in occupancy. In Q3 they did see a small decline in occupancy ratings from 87.3% to 87.2%. But despite this, earnings remained strong for Cousins Properties. They even raised full-year guidance to $2.60 to $2.64, up from $2.57 to $2.65. This was driven by the sale of 10.4 acres of land outside of Atlanta where the REIT made more than a $500k gain.

The office REIT's balance sheet is also impressive with a net debt to EBITDA of just 5.0x. This did increase from 4.93x at the end of 2022 but is still within a safe range for REITs. This is in comparison to Realty Income's ( O ) 5.0x and NNN REIT's ( NNN ) 5.4x, two of the highest-quality REITs in the sector.

Unlike DEA, CUZ does have some floating-rate debt whereas the former's debt is 100% fixed. 17% of Cousins Property debt is floating rate and the remaining 83% is fixed-rate. They also have more debt maturing this year with $420.8 million due and $751.5 million in 2025.

{kind=link}

Impressive Dividend Growth

Over the past 5 years, CUZ has grown the dividend by 33%. Since 2017 this has grown from $0.24 to the current $0.32. One of the things that impressed me the most about Cousins Properties is the very low payout ratio of roughly 48%. Now you can see why Quant gives them a dividend safety grade of A as this is very low for REITs. For the first nine months, the REIT brought in $300 million in FFO and paid out nearly $146 million in dividends.

Using the FAD or funds available for distribution of $211.5 million, this is still safe at just 69%. Compared to 2022's FFO of $408.7 million, I do expect this year's full-year FFO to be down slightly, but still safely cover the dividend. As far as FAD, I expect this to be in or around last year's amount of $274.5 million.

Valuation

Both REITs are trading at very attractive valuations currently for obvious reasons. Both also offer some upside to their price targets so investors could be buying both at great entries right now. DEA's forward P/FFO and AFFO ratios are both below the sector median while CUZ also trades below indicating they're both undervalued right now.

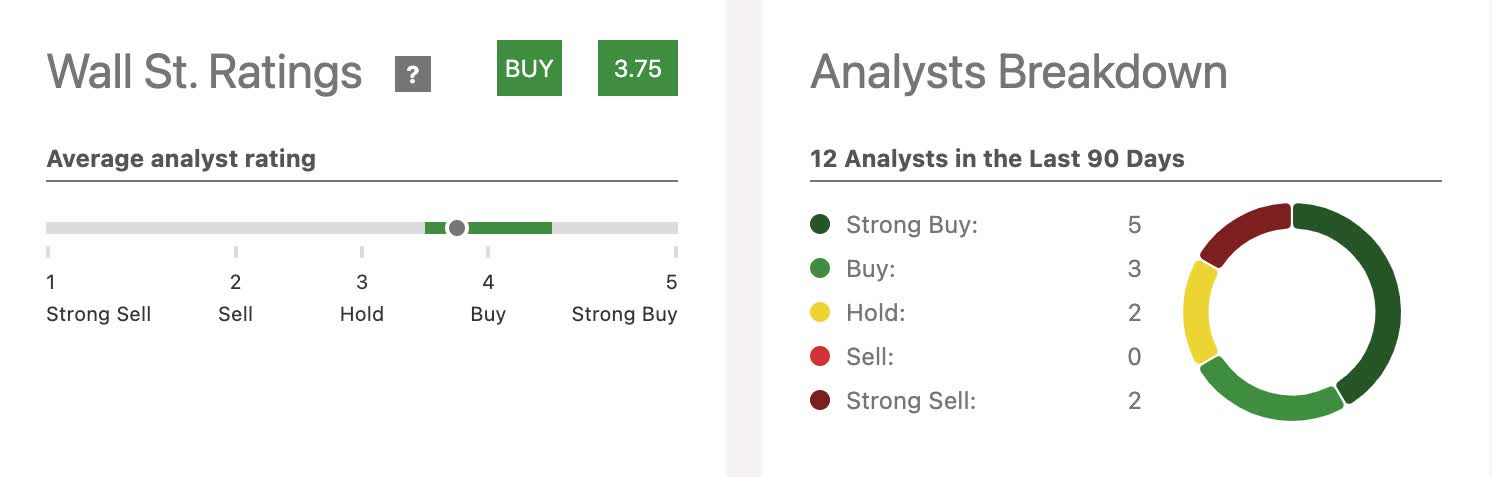

However, Wall Street rates DEA a hold while rating CUZ a buy. And due to the reasons explained in this article, I think it's safe to say why.

{kind=link}

Cousins Property is rated a buy with 5 strong buys and 3 buys compared to just 1 strong buy and 0 buys for Easterly Government Properties.

{kind=link}

Using the Dividend Discount Model or DDM, both REITs do offer some upside by the end of this year. DEA has had a lower growth rate of just 1% over the past 5 years. But with interest rates likely declining, and the sector historically performing better after rate hikes, I decided to use a higher growth rate for both but still on the conservative side.

{kind=link}

Below you can see I use a 3% growth rate for CUZ because of their better 5-year growth rate and higher quality. This gives me a price target of nearly $26. That's if rates do indeed decline and the office sector posts higher occupancy in the coming quarters.

{kind=link}

Risk Factors

Two risks for both companies are obviously a higher for longer rate environment, but also the delay for employees going back to the office. There still is a lot of uncertainty around whether the hybrid work environment is here to stay for good. Some CEOs have mentioned before that requiring employees back in the office is better for production, engagement, and mentorship.

Another office REIT, American Asset Trust's COO briefly discussed during their earnings call that a study found that 90% of companies support requiring people back into the office in the next 12-14 months. This remains to be seen if it will happen, but this could suppress both REITs' financials going forward, essentially putting strain on the dividend. It can also lead to further declines in occupancy ratings.

High interest rates or even a recession will likely make it tougher for both companies to find and make accretive acquisitions. The macro environment has been tough for REITs, especially with cap rates not being as attractive as before, decreasing spreads in the meantime. However, I do think this will get better in the near future as I suspect rates will fall, but this is something investors should keep an eye on going forward.

Bottom Line

The office sector as a whole has experienced a lot of volatility and many REITs are now trading well below the sector median and their 5-year averages. If you have a long-term outlook and think the sector will eventually recover, then now may be a good time to get paid while you sit and wait.

However, all REITs in the sector are not created equal and investors could end up getting burned if DEA is forced to cut the dividend because of their elevated payout ratio. Especially if the work-from-home environment is here to stay for good. So, this is one REIT I would warn investors against. Yes, they do lease to the government, but for reasons listed in this article, I would suggest looking elsewhere in higher-quality REITs like Cousins Property Incorporated.

For further details see:

One REIT To Buy For The Office Property Recovery And One I Would Avoid