CA - Open Text Corporation Unlikely To See Cost Synergies Until Fiscal 2024

2023-07-26 16:46:01 ET

Summary

- Open Text Corporation provides a wide range of information management software to organizations worldwide.

- Management says organic revenue growth is "1% to 2%" and that the company won't see major cost synergies from its Micro Focus acquisition until fiscal 2024.

- Although Open Text Corporation stock has rebounded in recent quarters, we really won't know how well the new combination is doing until 2024, so I remain Neutral [Hold].

A Quick Take On Open Text Corporation

Open Text Corporation ( OTEX ) offers a range of digital transformation software capabilities to organizations worldwide.

I previously wrote about Open Text with a Hold outlook, based on a heavy debt load and organic growth slowdown caution.

Despite increased market comfort with the Micro Focus combination, we won’t see the results of the cost synergies and combined organic growth trajectory until fiscal 2024, so I’m Neutral [Hold] on Open Text Corporation until we get more visibility into the integrated company's actual performance.

Open Text Overview

Waterloo, Canada-based Open Text was founded to provide a range of services related to information management, including strategic planning, domain expertise, and customer service solutions.

The firm is headed by CEO and Chief Technology Officer Mark Barranechea, who has been with the firm since 2012 and was previously president and CEO of SGI and Rackable Systems.

The company’s primary offerings include:

-

Information management

-

Content cloud

-

Business network cloud

-

Security cloud

-

Experience cloud

-

Developer cloud

-

AI & Analytics

-

Process automation.

The firm acquires customers through its in-house direct sales, marketing and business development efforts as well as through strategic partners and solution extension partners.

Open Text’s Market & Competition

According to a 2022 market research report by Grand View Research, the global market for information management was estimated at $89.3 billion in 2022 and is forecast to reach $223 billion by 2030.

This represents a forecast CAGR of 12.1% from 2023 to 2030.

The main drivers for this expected growth are growing information security requirements, the need for ongoing risk management and the rising volume of data.

Also, the chart below shows the historical and projected future growth trajectory of the U.S. enterprise data management market:

U.S. Enterprise Data Management Market (Grand View Research)

Major competitive or other industry participants include:

-

International Business Corp.

-

Oracle Corp.

-

SAP SE

-

Cloudera, Inc.

-

Amazon Web Services, Inc.

-

Teradata

-

MindTree Ltd.

-

Broadcom (Symantec)

-

Informatica.

Open Text’s Recent Financial Trends

-

Total revenue by quarter has risen due to its recent Micro Focus acquisition; Operating income by quarter has dropped in the most recent quarter.

Total Revenue and Operating Income (Seeking Alpha)

-

Gross profit margin by quarter has remained flat; Selling, G&A expenses as a percentage of total revenue by quarter have trended higher in recent quarters, with a material increase in the most recent quarter.

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

-

Earnings per share (Diluted) have been volatile in recent quarters.

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

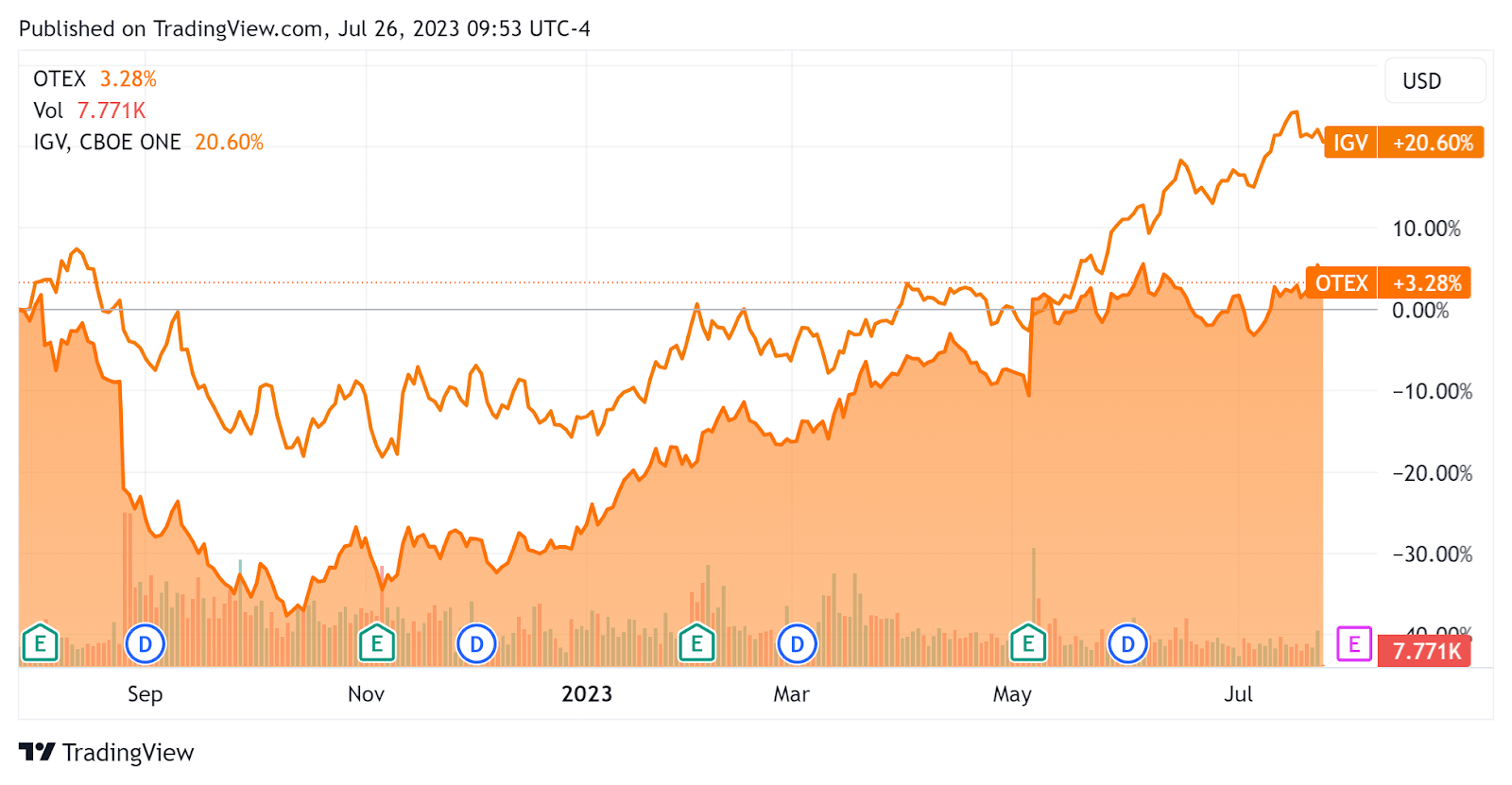

In the past 12 months, OTEX’s stock price has risen only 3.28% vs. that of the iShares Expanded Technology-Software ETF’s (IGV) rise of 20.6%, as the chart indicates below.

52-Week Stock Price Comparison (Seeking Alpha)

{kind=link}

For the balance sheet , the firm ended the quarter with $1.4 billion in cash, equivalents and short-term investments and $9.06 billion in total debt, of which $495.9 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $777.9 million, during which capital expenditures were $137.9 million. The company paid $112.9 million in stock-based compensation in the last four quarters, the highest trailing twelve-month run rate in the past eleven quarters.

Valuation And Other Metrics For Open Text

Below is a table of relevant capitalization and valuation figures for the company.

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 5.0 |

| Enterprise Value / EBITDA |

| 19.3 |

| Price / Sales |

| 3.0 |

| Revenue Growth Rate |

| 11.8% |

| Net Income Margin |

| 7.7% |

| EBITDA % |

| 26.1% |

| Net Debt To Annual EBITDA |

| 7.5 |

| Market Capitalization |

| $11,540,000,000 |

| Enterprise Value |

| $19,590,000,000 |

| Operating Cash Flow |

| $915,840,000 |

| Earnings Per Share (Fully Diluted) |

| $1.12 |

(Source - Seeking Alpha)

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings.

Discounted Cash Flow Calculation - OTEX (Guru Focus)

Assuming generous DCF parameters, the firm’s shares would be valued at approximately $41.14 versus the current price of $42.21, indicating they are potentially currently fully valued, with the given earnings, growth, and discount rate assumptions of the DCF.

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

OTEX’s most recent unadjusted Rule of 40 calculation was 37.9% as of FQ3 2023’s results, so the firm has improved sequentially in this regard, per the table below.

| Rule of 40 Performance (Unadjusted) |

| FQ2 2023 |

| FQ3 2023 |

| Revenue Growth % |

| 2.9% |

| 11.8% |

| EBITDA % |

| 27.5% |

| 26.1% |

| Total |

| 30.4% |

| 37.9% |

(Source - Seeking Alpha.)

Commentary On Open Text

In its last earnings call ( Source - Seeking Alpha ), covering FQ3 2023’s results , management highlighted the positive organic revenue growth of "1% to 2%" and its ninth consecutive quarter of organic revenue growth.

However, Cloud segment bookings were flat, while noting "Micro Focus wins in enterprise security, mainframe migrations and IT operations management. Government transportation and high-tech firms were top of the demand curve."

The firm completed its Project Titanium, its 2nd generation private cloud and API platform and reports "strong customer adoption from companies such as ANXe, Close Brothers, Stericycle and SolarisBank."

Management didn’t disclose any company, customer or revenue retention rate metrics.

Total revenue for FQ3 2023 rose by 41.1% year-over-year on the effects of the Micro Focus acquisition and gross profit margin increased 1.1%.

Selling, G&A expenses as a percentage of revenue increased 1.4% YoY while operating income fell by 2.7%.

The company's financial position features a large increase in debt due to the Micro Focus acquisition, which was an all-cash deal.

OTEX’s Rule of 40 performance has improved sequentially.

Looking ahead, management expects to produce $400 million in annual savings from the Micro Focus integration and other headcount reductions, but they won’t begin to show in the financials until fiscal 2024.

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below.

Earnings Transcript Key Terms Frequency (Seeking Alpha)

I’m most interested in the frequency of potentially negative terms, so management or analyst questions cited "Uncertain" two times and "Macro" four times.

Analysts questioned company leadership about the progress with the Micro Focus acquisition. Management responded that "it’s as we had theorized."

Regarding valuation, my discounted cash flow calculation suggests the stock may be fully valued given the assumptions of the DCF.

However, the DCF has limitations that are difficult to model with such a significant acquisition as Micro Focus’s effect on the future trajectory of OTEX, for good or bad.

Until we see organic growth of the combined firms, which will take at least a year from the first full quarter after transaction close, it’s anybody’s guess as to what the combination’s net results will be.

Since the May 2023 earnings announcement, the firm's EV/EBITDA valuation multiple has jumped, as the chart from Seeking Alpha shows below.

EV/EBITDA Multiple History (Seeking Alpha)

{kind=link}

So, it appears investors like what they see from the combined companies, at least at this early stage of integration and collective efforts.

But, we won’t see the results of the cost synergies and organic growth trajectory until fiscal 2024, so I’m Neutral [Hold] on OTEX until we get more visibility into the integrated company.

For further details see:

Open Text Corporation Unlikely To See Cost Synergies Until Fiscal 2024