KAR - Openlane: Attractive Valuation Warrants A Buy

2023-11-15 09:40:05 ET

Summary

- Openlane is given a Buy rating due to its strong performance in the dealer-to-dealer segment, stable operating margins, and undervaluation compared to peers.

- The company's gross profit margins have improved, driven by higher transportation margins and increased fees for platform services.

- Openlane reported strong Q3 results with sales growth and resilience in the marketplace segment, although the finance segment saw a decline in adjusted EBITDA.

Investment Thesis

We ascribe Openlane ( KAR ) with a Buy rating primarily driven by:

1) strength in its dealer-to-dealer segment which also generates higher margins as evidenced in its strong gross margin expansion over the past quarters

2) strong risk management leading to stable operating margins and loss rates

3) absolute and relative undervaluation compared to peers and

4) strong earnings momentum and clean beat in YTD 2023

Company Background

Openlane is a leading digital marketplace for used vehicles connecting buyers and sellers as well as a leader in digital dealer-to-dealer wholesale marketplace and off-lease remarketing. The company sold off its ADESA U.S. physical auction business to Carvana in mid-2022, which included all auction sales and operations in the US. In addition, it offers short-term financing secured through its inventory to a wide range of used vehicle dealers with over 1.6 mn loan transactions annually. KAR also provides a wide range of solutions including ADESA simulcast (live bidding software for bids on the marketplace), Backlot Cars (dealer-to-dealer wholesale platform for buying and selling of inventory), and TradeRev (platform to facilitate 45-minute live bidding as well as vehicle inspection services).

Recent Financial Trends

Marketplace Segment

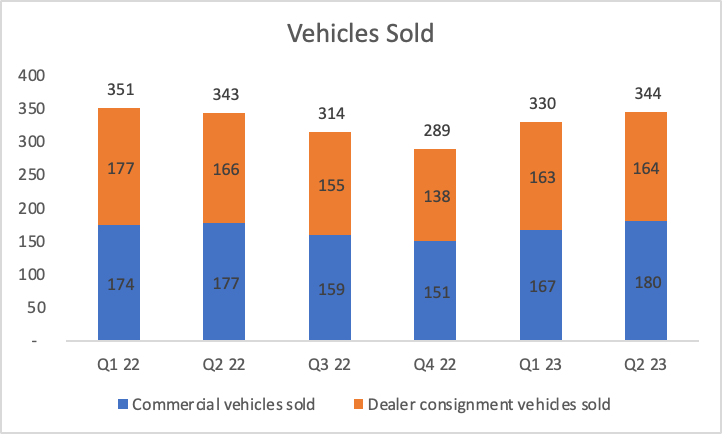

The total number of vehicles sold remains pressured as a result of continued weakness in the overall used car vehicle market. The recent performance in 2023 was driven by strength in dealer-to-dealer wholesale sales along with a general improvement in used vehicle sales.

{kind=link}

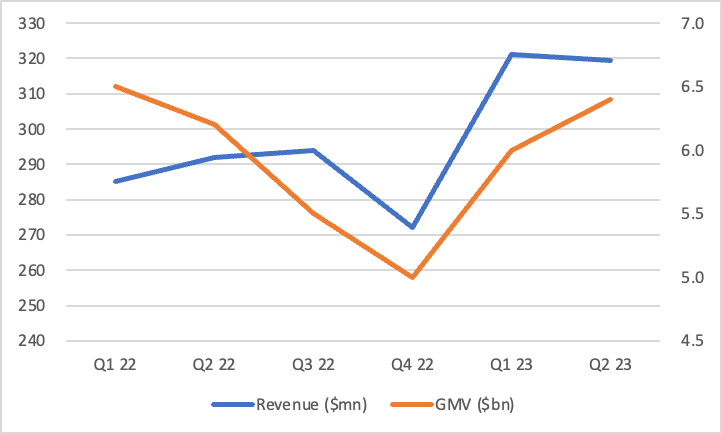

Despite relatively high volatility in the GMV volumes, total marketplace revenues remained relatively stable driven by the relatively higher contribution and resilience of its service business.

{kind=link}

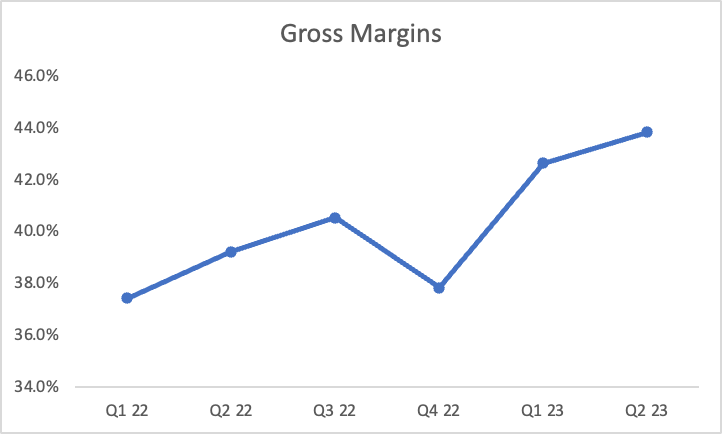

Gross profit margins showed significant strength and improved due to higher transportation margin, improved margins on vehicles sold on dealer-to-dealer platforms, and an increase in third-party fees for platform services.

{kind=link}

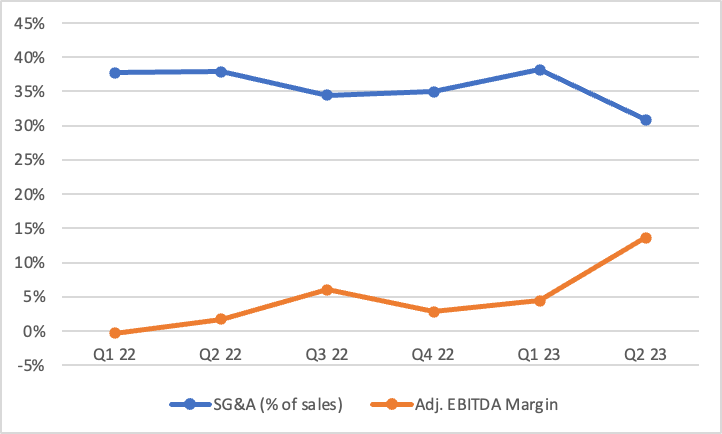

Robust gross margin expansion driven by improving contribution from its high-margin service business and strong cost control leading to significantly lower SG&A expenses as % of sales (dropped to ~31% in Q2 2023 from an average of 38% in the past quarters). This led to a strong EBITDA margin expansion, driven by robust gross margins and strong cost control.

{kind=link}

Finance Segment

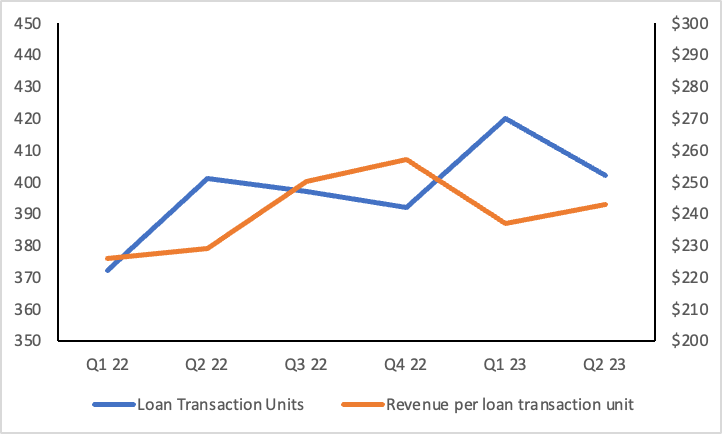

Loan transaction units continue to remain resilient at around 400 per quarter while revenue per loan transaction unit remains volatile, although inching up primarily driven by an increase in the Federal Reserve rates leading to higher interests.

{kind=link}

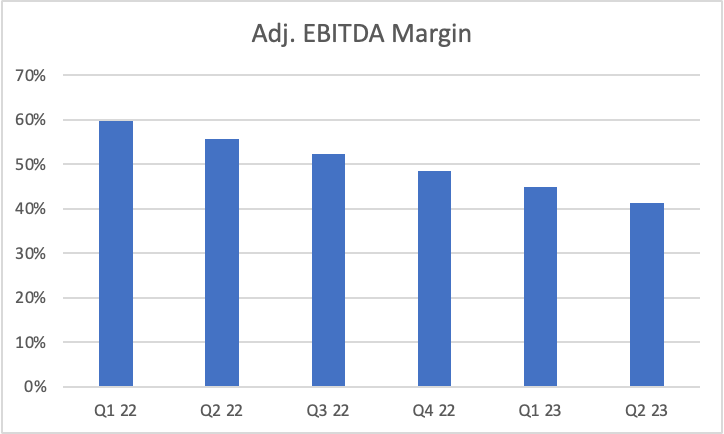

However, adj. EBITDA margins declined sharply as a result of higher provision for credit losses amidst the current inflationary headwinds and macroeconomic pressures which spiked up to 2% of average managed receivables compared to <0.5% in the year-ago period. Management guided that provision for credit losses is likely to be around the 2% mark amidst the current economic downturn. The 2% credit loss provision also remains at the higher end of the pre-COVID levels.

{kind=link}

Strong Q3 Results

KAR reported a strong Q3 with sales growth of 6% YoY at $416 mn, ahead of the consensus expectation pegged at $410 mn. The growth was driven by a strong uptick within the marketplace segment with revenues growing 8% YoY while finance revenue remained stable.

Marketplace Segment

Marketplace volumes remained resilient at 339k units, up 8% YoY and down 1% QoQ with dealer consignment volumes (of which digital dealer-to-dealer comprised over two-thirds of sales) growing 3% YoY but down 3% sequentially while commercial volumes grew 13% YoY but flat sequentially. Auction fees per vehicle sold increased by 6% YoY primarily as a result of an increase in the used vehicle prices along with the introduction of new auction-related services. Service revenues declined about 3% YoY primarily as a result of a slight decline in transportation revenues but still remained resilient. Purchased vehicle sales grew by 32% YoY driven by an increase in vehicles sold along with a higher average vehicle price in Europe.

Gross profit per unit grew by 8% YoY benefiting from a higher commercial volume mix that garnered relatively higher GPU compared to dealer consignment transactions. This led to gross margins, excluding purchased vehicles, increase by 530 bps YoY as well as 200 bps sequentially at robust gross margins of 45.8% for the quarter. SG&A expenses as % of sales inched up sequentially by 650 bps as well as by 290 bps on YoY basis to ~37% primarily showing that Q2 was essentially a one-off as a result of seasonality and timing issues. Adj. EBITDA margins although came in strong at 8.5%, up 240 bps YoY, however, down by about 6 percentage points sequentially.

Finance Segment

AFC revenues came in slightly higher than expected at $100 mn, up 1% YoY, vs consensus expectation of flattish growth. The minor beat was driven by higher loan transaction volumes at 406k loans in Q3 2023 (vs 390k loans last year) coupled with stronger than anticipated finance ARPU at $246, which was still down marginally on a YoY basis as a result of a decline in average loan value. Net provisions for credit losses increased to 2% of the average managed receivables compared to 0.2% in the year-ago period. Adjusted EBITDA declined by 22% YoY to $40.7 mn with Adj. EBITDA margins declined by 11 percentage points to 40.8% primarily driven by a sharp jump in credit losses as well as a marginal dip on a QoQ basis.

On a consolidated basis, the company reiterated its Adj. EBITDA guidance of $250-$270 mn, implying an Adj EBITDA of $39-$59 mn for Q4. In addition, the company expects Adj. EPS to be at $0.6-$0.8, implying an Adj. EPS of $0.04-$0.24. We believe the company is likely to be at the higher end of the guidance driven by resilience in the finance segment with sustained loan volumes and stability in the loan loss ratios which still remain at the higher end of the pre-pandemic average. In addition, Q4 was the softest quarter last year which coincided with the overall market meltdown of the used car vehicle market. We believe the company is likely to post above 300k units sold and an improvement in average vehicle price will drive a double-digit revenue growth. We further expect EBITDA margins to range around 6-8% in line with historical averages driven by stable gross margins at 40%+ and cost control.

Valuation

We compare Openlane with other Used Car vehicle retailers which also have operations in dealer-to-dealer business. Openlane appears to be relatively cheaper trading at just 6.4x EV/Fwd EBITDA and appears at the bottom end of the quartile. The peer set also includes ACV Auctions ( ACVA ), however, given its negative Fwd EBITDA, the ratio is non-material. KAR also trades at a discount to its own long-term average of ~9.5x, and we believe that, despite the near-term uncertainty, it does not warrant a significant discount. We value KAR at 8.0x EV/Fwd EBITDA, a 20% discount to its long-term average to reflect near-term uncertainty and ascribe a target price of $20. Initiate at Buy.

Risks to Rating

Risks to rating include:

1) Potential elevated losses in the financing segment above the current rate of 2% amidst rising defaults in the current macroeconomic downturn

2) Competitive intensity within the dealer-to-dealer segment intensifies leading to declining operating margins and higher promotional spends

3) Slower recovery within the commercial off-lease segment

4) Management's inability to contain SG&A spends which can lead to suppressed EBITDA margins as evidenced during the recent quarter (Q2 margins of 14% being a one-off)

Final Thoughts

Openlane had reported a clean beat along with green shoots of improvement going forward driven by stability in its financing segment managing the risk well and containing loss ratios along with volume uptick in the marketplace segment. This coupled with strong balance sheet flexibility (net leverage ratio of only 0.5x) and relative undervaluation on absolute as well as relative terms provides a margin of safety and favorable risk-reward. We initiate at a Buy and target price of $20 (at 8.0x EV/Fwd EBITDA).

For further details see:

Openlane: Attractive Valuation Warrants A Buy