REIT - Opportunities In Listed REITs Today

2023-09-15 10:10:00 ET

Summary

- Amidst the bearish sentiment towards real estate, a compelling opportunity to own REITs has emerged.

- The deeply discounted REIT market has largely priced in the challenges for real estate of higher rates and tighter credit markets.

- Areas of concern for real estate - office properties or too much leverage - are well-contained in public REIT markets. REITs generally possess high-quality balance sheets and have minimal exposure to traditional office space.

By Kelly Rush, CEO, Public Real Assets & CIO, Real Estate Securities, Principal Asset Management, and Todd Kellenberger, CFA, Client Portfolio Manager, Real Estate Securities, Principal Asset Management

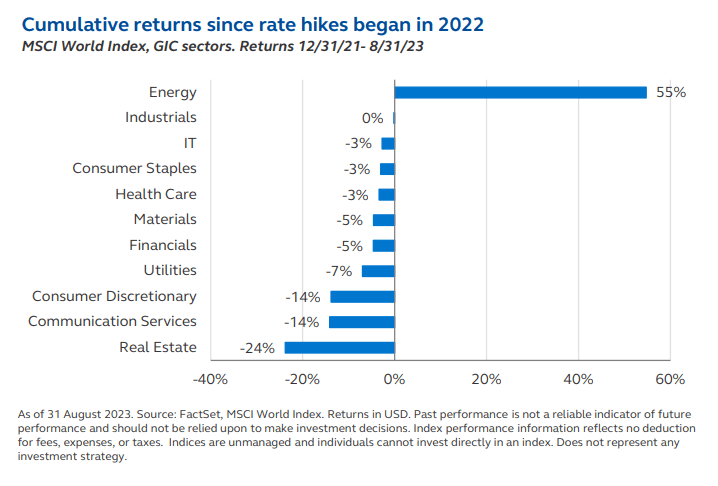

Listed REITs have faced headwinds the past 18 months, with stickier-than-anticipated inflation requiring continued hawkish bank rhetoric, increasing upward pressure on bond yields and negative pressure on real estate values and REIT stock prices. The prospect of a banking crisis-driven credit crunch has added to the pressure on the capital-intensive real estate sector.

Amidst the bearish sentiment towards real estate, a compelling opportunity to own REITs has emerged. The deeply discounted REIT market has largely priced in the challenges for real estate of higher rates and tighter credit markets.

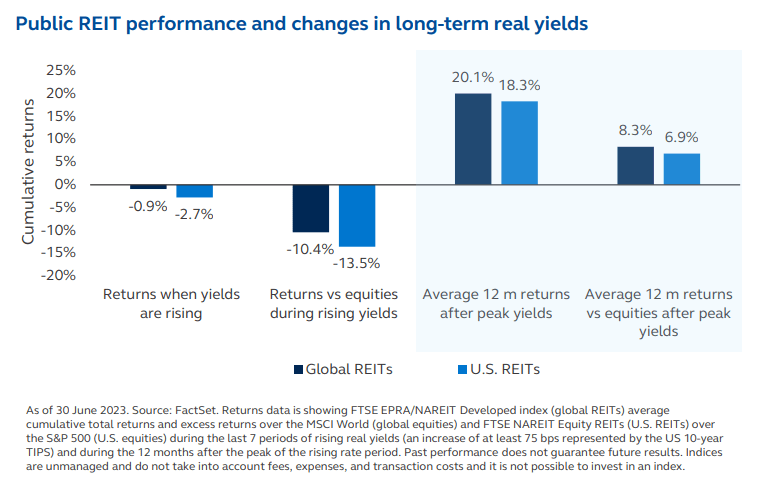

Peaking or falling yields have historically been the catalyst for strong REIT market outperformance. REITs are often beneficiaries of investor rotation into long-duration, defensive assets when yield increases subside.

Areas of concern for real estate - office properties or too much leverage - are well-contained in public REIT markets. REITs generally possess high-quality balance sheets and have minimal exposure to traditional office space.

Property sectors with resilient, structurally-driven demand dominate REIT markets. These sectors are meeting the demands of a changing economy and society and offer attractive long-term growth.

Extreme bearishness towards REITs and a large valuation discount is creating a compelling entry point for investors

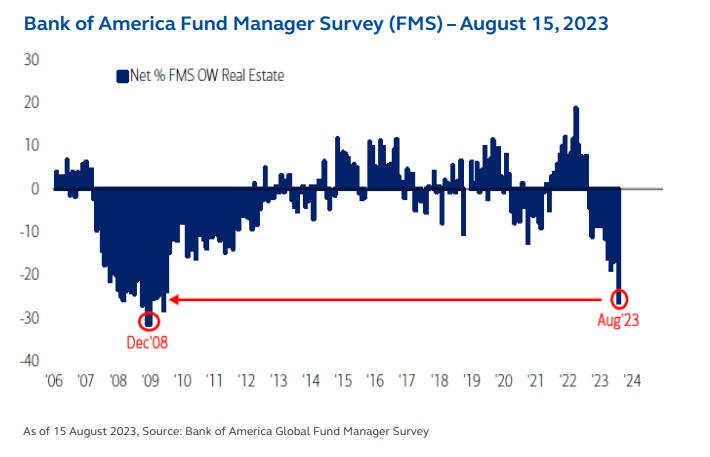

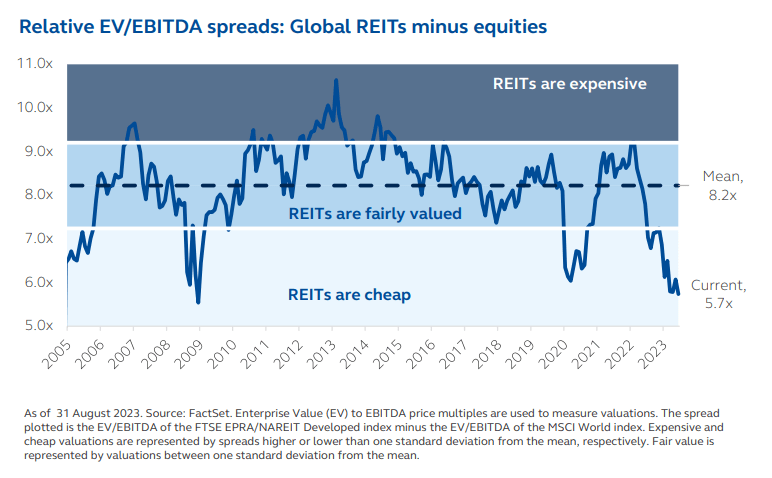

As Warren Buffett once famously wrote, “... be fearful when others are greedy and be greedy only when others are fearful.” In our view, investors should be greedy when it comes to REITs. According to the Bank of America Fund Manger Survey (see chart below), the current 26% net underweight by survey respondents is the lowest allocation to real estate since March 2009 and 2.2 standard deviations below its long-term average. The relative valuation of REITs versus equities (see chart below) tells a very similar story.

It appears contrarian to favor REITs today compared to the negative news headlines about real estate, but these challenges are well-understood in REIT markets. When sentiment does shift back in favor and relative valuations are too cheap to ignore, REITs are poised for potentially strong fund inflows. After all, the number of potential buyers is outnumbering the remaining sellers by a bigger margin every day.

{kind=link}

{kind=link}

Public REITs present an opportunity to buy discounted real estate now

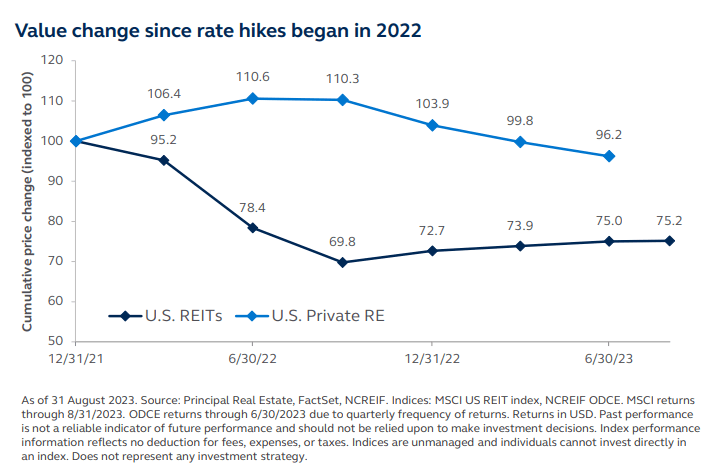

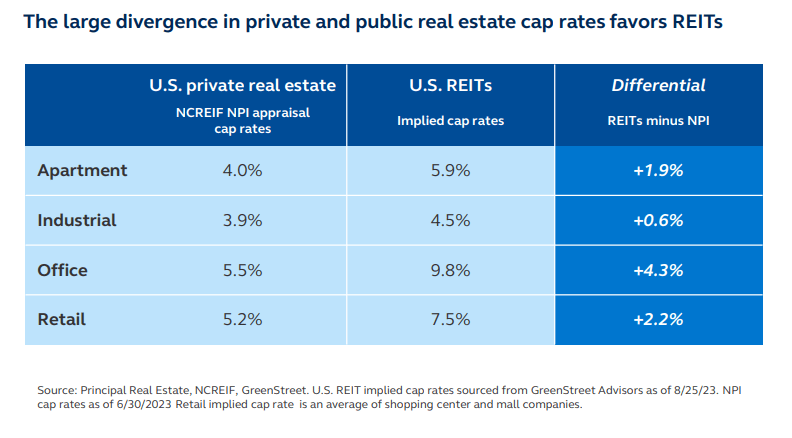

The challenges for real estate have been visible for a while now, and markets have priced it in for REITs given their liquid, public nature. Change in valuations for private real estate have been slower given appraisal-based methodologies and limited price discovery in today’s transaction markets. The declines REITs have experienced since the Fed started hiking rates are significant compared to private real estate, and current REIT implied cap rates suggest REITs offer an attractive return premium over private real estate.

Looking to the future, the valuation gap between public and private markets means the convergence trade that favors public REITs is very attractive, in our opinion. While the absolute direction of REITs and private real estate is less certain given the variety of macro scenarios that could unfold, there is conviction in our belief that, on a relative basis, public REITs have a strong headstart at these valuation levels.

{kind=link}

{kind=link}

The end of central bank tightening and rising yields is historically a strong catalyst for REIT outperformance

A strong economy and global central bank war on inflation has increased upward pressure on bond yields and negative pressure on REIT stocks.

The good news for REITs is markets are starting to believe the end of rising rates is soon coming to an end. The arrival of peak rates has been deferred, but recent soft data (survey based leading indicators) suggest a slowing economy ahead as the lagged impact of monetary tightening works its way through.

This event - peaking or falling long-term yields - is just the catalyst a deeply discounted REIT market needs to potentially start a new return cycle upwards. Historically, REITs have delivered strong positive returns and against equities in the 12 months after real yields have peaked.

{kind=link}

{kind=link}

Real estate debt markets are challenging, but we believe REITs can weather the lending slowdown

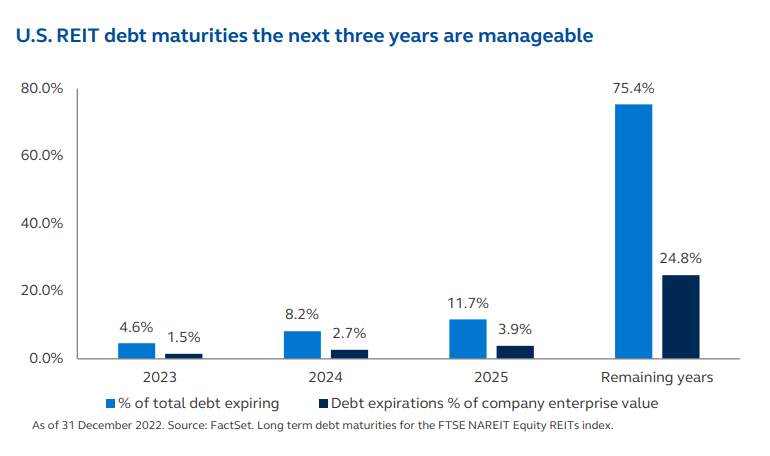

The prospect of a banking crisis-driven credit crunch has added to the pressure on the capital-intensive real estate sector this year. Looking forward, we expect tight lending conditions and less-available capital could persist until bank balance sheet issues are resolved. Until then, we expect sluggish real estate transaction markets, pressure on capital values in the private market, and higher loan default risk for overleveraged properties.

REITs should be well-insulated from these issues, and current share prices already reflect many of the concerns. Most public REITs are low leveraged with manageable debt maturities and diversified sources of capital. We believe this will provide support to weather today’s tighter credit conditions and potentially allow REITs to capitalize on opportunities. Looking ahead, we believe any emerging signals of improving real estate capital markets to be a positive upside catalyst for REITs.

{kind=link}

Office exposure doesn’t move the needle for public REITs

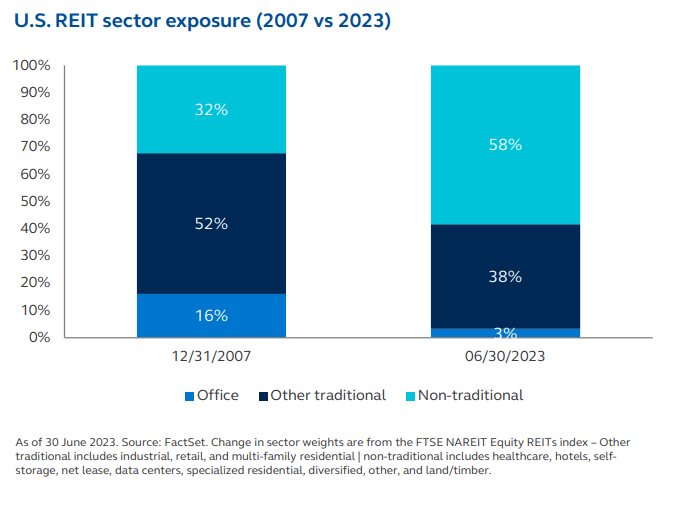

Office REITs have experienced significant declines in market values in a new environment of work-from-home and hybrid arrangements. The public market values of these companies reflect a future of significantly lower values for office assets and higher cost of capital. The traditional office sector is now only approximately 3% of the U.S. market and 6% of the global market, while many non-traditional property types with structural drivers (e.g. single-family rental, healthcare, data centers) represent the majority of REIT exposures.

{kind=link}

Property sectors with resilient, structurally driven demand drive REIT markets

The public REIT market has experienced significant transformation over the last 10-15 years. The market is no longer dominated by traditional sectors such as office and retail, but instead, a proliferation of non-traditional sectors has taken over. This can often be explained by structural changes in our economy, demographics, technology, and other factors that have created new and growing demands for different types of real estate space.

These structural changes are creating resilient and predictable demand trends that are expected to drive above average long-term cash flow growth for these properties. This profile has attracted significant interest from investors, and we expect many of these property types to be beneficiaries of strong capital inflows. Better cash flow prospects and large capital inflows should be tailwinds to support property prices.

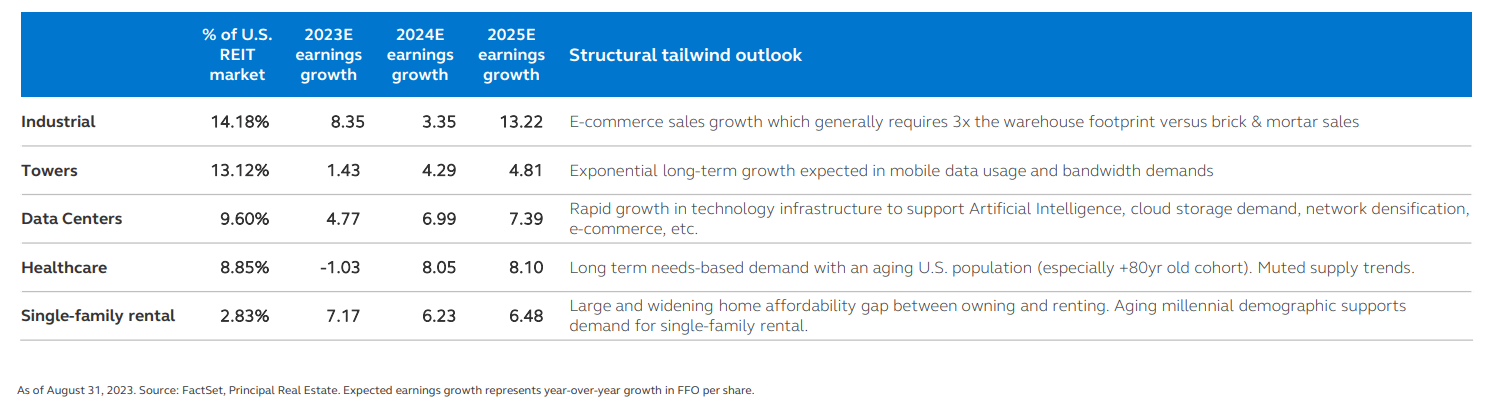

A few examples of property types experiencing favorable structural demand drivers

{kind=link}

Opportunities we’re seeing within the REIT market

Preference for demand resiliency and structural growth drivers

Our investment approach within listed real assets emphasizes resiliency for what we expect to be tougher macroeconomic conditions ahead. We are expressing a preference for businesses with resilient pricing power, lower economic sensitivity, and/or favorable exposure to structural growth drivers. Our emphasis on bottom-up stock-picking does lead to certain sector preferences.

In listed REITs, the non-traditional residential sectors are a favorite given home ownership is expensive, forcing many individuals to rent when they would otherwise buy. In healthcare, senior housing enjoys demographic tailwinds and niche life science office is more immune from work-from-home trends. Long-term growth in mobile data usage is a big structural driver for tower REITs.

{kind=link}

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Opportunities In Listed REITs Today