OPRX - OptimizeRx Aims For Growth After Swoon

2023-07-21 13:47:01 ET

Summary

- OptimizeRx Corporation provides communication technologies between pharma firms, healthcare providers, and patients.

- The company has seen material operating headwinds as the U.S. healthcare industry exited the pandemic and FDA approvals slowed.

- Until we see improving operating metrics and faster FDA approvals, I'm Neutral [Hold] on OptimizeRx Corporation.

A Quick Take On OptimizeRx

OptimizeRx Corporation (OPRX) provides a variety of patient and provider communications functions for the pharmaceutical and healthcare industries in the U.S.

The firm's results have been hampered by end-of-pandemic industry volatility and slowing FDA approvals for new products.

My outlook for OPRX is Neutral [Hold] until we see improvements in its retention rates and FDA approval activity.

OptimizeRx Overview

Rochester, Michigan-based OptimizeRx was founded in 2006 to enhance patient engagement and provider engagement throughout the therapy lifecycle.

The firm is headed by Chief Executive Officer Will Febbo, who has been with the firm since February 2016 and was previously co-founder and CEO of Digital Capital Network and COO of Merriman Capital.

The company's primary offerings include the following:

-

Physician engagement

-

Patient engagement

-

Banner messaging

-

Financial messaging

-

Therapy initiation workflows.

OptimizeRx acquires customers through its direct sales and marketing efforts as well as through strategic alliances and partner referrals.

OptimizeRx's Market & Competition

According to a 2023 market research report by Grand View Research, the global market for patient engagement solutions was an estimated $19.5 billion in 2022 and is forecast to reach $71 billion by 2030.

This represents a forecast very strong CAGR of 17.54% from 2023 to 2030.

The main drivers for this expected growth are increasing usage of electronic health records and the willingness of both patients and caregivers to interact via online means.

Also, the continued adoption of mobile health devices will add to the sector's growth potential. Below is a chart showing the North American patient engagement solutions market's historical and projected future growth trajectory through 2030:

N. American Patient Engagement Solutions Market (Grand View Research)

Major competitive or other industry participants include:

-

Traditional IT companies with healthcare services

-

CROs

-

Healthcare consulting companies

-

Healthcare big data solution specialists.

The company also operates in the physician engagement and biopharmaceutical communications markets.

OptimizeRx's Recent Financial Trends

-

Total revenue by quarter has flattened recently; Operating income by quarter has dropped further into negative territory.

Total Revenue and Operating Income (Seeking Alpha)

-

Gross profit margin by quarter has trended higher more recently; Selling, G&A expenses as a percentage of total revenue by quarter have been volatile in the past 12 months.

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

-

Earnings per share (Diluted) have worsened further into negative territory in recent quarters.

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

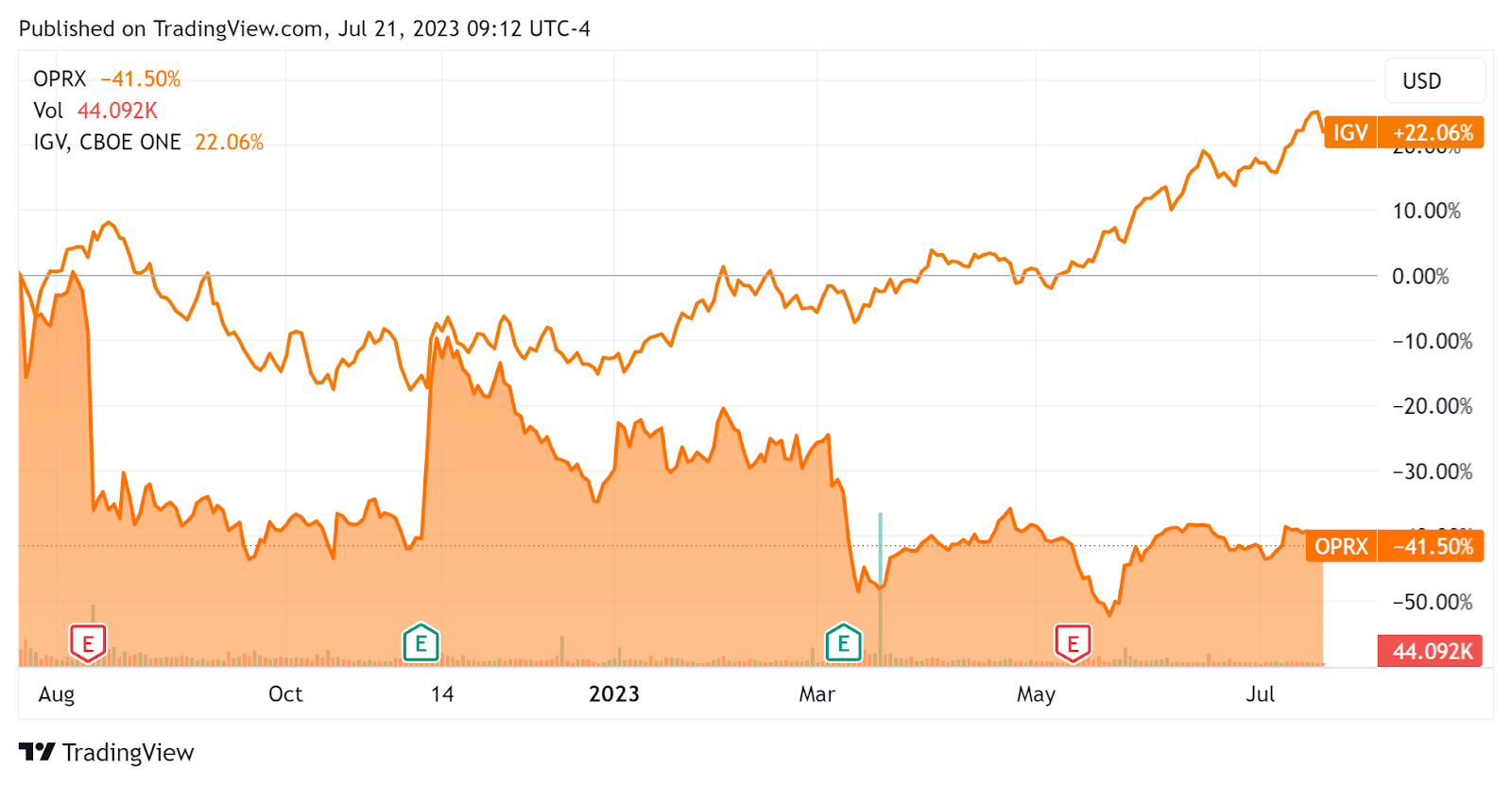

In the past 12 months, OPRX's stock price has fallen 41.5% vs. that of the iShares Expanded Technology-Software ETF's ( IGV ) rise of 22.06%, as the chart indicates below.

{kind=link}

For the balance sheet , the firm ended the quarter with $73.7 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash flow was $6.4 million, during which capital expenditures were $0.1 million. The company paid a hefty $17.0 million in stock-based compensation ("SBC") in the last four quarters, the highest trailing twelve-month figure in the past eleven quarters.

Valuation And Other Metrics For OptimizeRx

Below is a table of relevant capitalization and valuation figures for the company.

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 2.9 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 4.2 |

| Revenue Growth Rate |

| -3.3% |

| Net Income Margin |

| -22.8% |

| EBITDA % |

| -22.0% |

| Net Debt To Annual EBITDA |

| 5.4 |

| Market Capitalization |

| $252,460,000 |

| Enterprise Value |

| $178,970,000 |

| Operating Cash Flow |

| $6,490,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.79 |

(Source - Seeking Alpha.)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

OPRX's most recent Rule of 40 calculation was negative (25.2%) as of Q1 2023's results, so the firm has performed poorly for this metric, per the table below.

| Rule of 40 Performance |

| Q1 2023 |

| Revenue Growth % |

| -3.3% |

| EBITDA % |

| -22.0% |

| Total |

| -25.2% |

(Source - Seeking Alpha.)

Commentary On OptimizeRx

In its last earnings call ( Source - Seeking Alpha ), covering Q1 2023's results , management highlighted its belief that the macro headwinds the firm has faced in recent quarters have begun to abate.

Those headwinds included a reduction in FDA drug approval rates, a higher turnover of pharma firm executives after the end of the pandemic and longer sales cycles due to that turnover as well as an increase in competitive intensity.

Leadership says it is "seeing modest improvements to tactical sales" and expects various parts of its business continue to improve going forward.

However, the company's net revenue retention rate dropped to 86%, a poor and worsening result compared to the previous year.

Total revenue for Q1 2023 fell 5.1% year-over-year and gross profit margin slid 2.2%.

Selling, G&A expenses as a percentage of revenue jumped 24.5% YoY and operating losses increased by 86.8%.

The company's financial position is strong, with ample liquidity, no debt and positive free cash flow.

OPRX's Rule of 40 performance has been quite poor, with negative revenue growth and substantial operating losses.

Looking ahead, management reiterated full-year 2023 revenue guidance growth of 10% YoY.

From management's most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below.

Earnings Transcript Key Terms Frequency (Seeking Alpha)

I'm most interested in the frequency of potentially negative terms, so management or analyst questions cited "Macro" eight times and "Drop" twice.

Analysts questioned company leadership about its expansion plans and management indicated it plans to expand beyond the EHR to provide technology solutions for all the various touch points that healthcare providers interact with throughout their day.

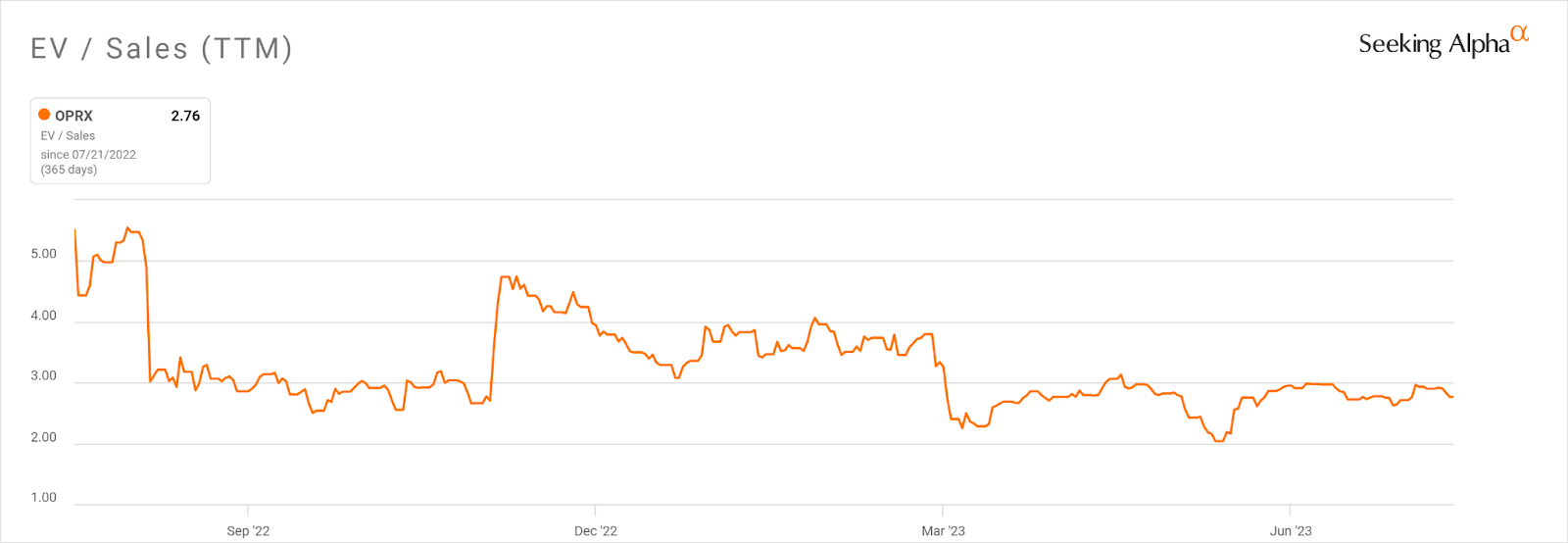

Regarding valuation, the market is valuing OPRX at an EV/Sales multiple of around 2.9x versus the average of the Seeking Alpha Healthcare Technology index multiple of approximately 7x.

In the past twelve months, the firm's EV/Sales valuation multiple has fallen 50%, as the chart from Seeking Alpha shows below.

{kind=link}

A potential upside catalyst to the stock could include continued improvement in FDA approval rates, reduced competitive activity and Pharma firm decision-making delays.

However, given OptimizeRx Corporation's worsening retention rate and the unlikely prospect of the FDA increasing its approval rates after receiving significant criticism in 2022 for possibly moving too fast on some drug approvals, I'm cautious on OPRX in the near term.

My outlook for OPRX is Neutral [Hold] until we see improvements in its retention rates and FDA approval activity.

For further details see:

OptimizeRx Aims For Growth After Swoon