AZN - Organon Q2 2023 Earnings Review: Incremental Growth With A Slather Of Risk

2023-08-10 11:01:31 ET

Summary

- Organon & Co. posted its Q2 2023 earnings on 8th August.

- The Merck spinouts' 3 main divisions are Women's Health, Biosimilars, and Established Brands.

- Total revenues were $1.6bn - up 4% ex-FX fluctuations - and diluted EPS was $0.95 - both outperformed analysts' expectations, leading to a small jump in the share price.

- With a forward price to sales ratio of <1x and forward price to earnings potentially <5x, the buy signals are there.

- Much depends on Established Brands sales holding up while the business focuses on growing key products like Nexplanon, and Humira biosimilar Hadlima. Debt is another risk factor.

Investment Overview - Organon: Sinking Ship, Or Rising Tide?

Organon & Co. ( OGN ), formed via Merck & Co.'s ( MRK ) spinout of its Established Brands, Women's Health and Biosimilars divisions, reported its Q2 2023 earnings on 8th August.

Spinouts are all the rage amongst "Big Pharma" companies, with Pfizer ( PFE ) having spun out its Established Brands division into a new entity, Viatris ( VTRS ), via a merger with generics giant Mylan, and GSK having spun out its Consumer Health division into new entity Haleon ( HLN ) this year.

Johnson & Johnson ( JNJ ) has followed suit, jettisoning its Consumer Health division which began trading under new name, Kenvue (KVUE), in May, via the largest IPO in the U.S. since 2021, which raised ~$2.8bn at $22 per share.

French Pharma Sanofi ( SNY ) spun out its drug ingredients business into a new business, EUROAPI, last year, and there have been rumors that AstraZeneca ( AZN ) plans to spin out its China business to shield it from political tensions.

Each Pharma company's reasons for completing a spin-out is different, although one common trend to consider are that drug development / pharmaceuticals is generally perceived as the most lucrative, high margin space to be in, hence companies are keen to stop marketing and selling patent expired drugs, or consumer health products, and focus instead on new products whose prices they can control given patent protection gives them market exclusivity.

Another is tax efficiency and the ability to raise funds - Pfizer was able to raise $12bn on the back of the Viatris spinout, leaving the spinout saddled with the debt, and Merck did something similar, completing a tax free dividend worth $8bn, and meaning Organon began life as a listed entity in May 2021, with ~$9bn of debt.

What's good for the parent company - ditching its dead wood and underperforming business divisions while raising billions of dollars to spend on business development and share buybacks - is much more challenging for the spun out companies. A portfolio of assets whose best sales years are long behind them, the challenge of turning around failing business divisions, and a mountain of debt.

The market's reaction has been to apply almost absurdly low valuations to the spun out companies. Viatris, for example, trades at a price to sales ratio of <1x, and a forward price to earnings ratio of ~7x - very attractive ratios, the only problem being that the company is more likely to grow than shrink, owing to the age of its main revenue generating assets.

Organon has the same problem - the company's FY23 revenue guidance is for $6.25bn - $6.45bn, which is higher than its current market valuation of $5.9bn. This is rare for the pharmaceutical industry - amongst the 15 largest Pharma companies by market cap, the average P/S ratio is ~7x. Organon is profitable, too - the company expects to generate $1bn of free cash flow before one-time charges this year - and pays a handsome dividend of $0.28 per quarter, which currently provides a yield of nearly 5%.

The key question for investors to consider is whether Organon management can generate sufficient growth from its Women's Health and Biosimilars division to offset the slowly declining sales of its established brands divisions, whilst paying down debt. If it can, then its modest market cap valuation is almost certain to rise significantly reflecting a growing business, but if it cannot, the valuation will become increasingly tied to the shrinking Established brands division, and will steadily erode.

In the following review of Organon's Q2 2023 earnings , and H123 earnings, I'll provide some ways of thinking about which scenario is the more likely, and why I believe the investment case for Organon is based on the possibility of driving consistent, incremental growth, versus the threat of key products underperforming in the marketplace, and the valuation unravelling as a result.

Organon Q2 2023 Earnings Review

First, let's study Q2 2023 company-wide performance in more detail, beginning with the headline figures.

Total revenues were $1.6bn - up 4% year-on-year excluding currency fluctuations. Adjusted EBITDA was $530m, diluted earnings per share ("EPS") $0.95, and adjusted diluted EPS $1.31. Revenue - by $51m, and EPS - by $0.32 and $0.09 - exceeded analysts expectations , and the stock price enjoyed a spike in response, rising from ~$21, to $24 - current traded price is $23.

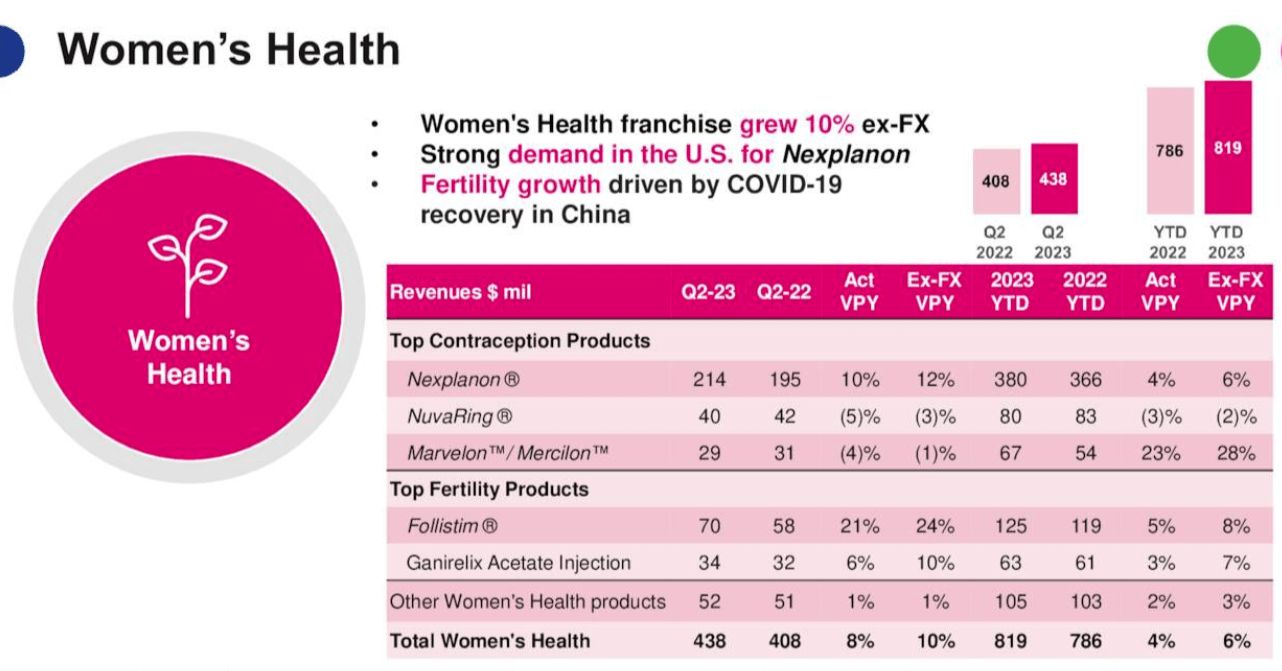

Women's Health - Nexplanon Remains Key Asset

Organon - Women's Health performance (earnings presentation)

{kind=link}

As we can see above, Organon's Women's Health division grew revenues by 10% year-on-year ex-FX in Q2 2023, and by 6% ex-FX in H123. This was a division that failed to fire when part of parent company Merck, but as part of the Organon it has been revitalized with some new acquisitions, as I discussed in a previous note on the company:

Organon has paid $240m to acquire Alydia Health and its 510k cleared JADA system, which is indicated for postpartum hemorrhage - and $75m, plus up to $870m of development and commercial milestone payments, for Forendo, whose lead asset is FOR-6219 - an experimental oral inhibitor of 17?-hydroxysteroid dehydrogenase type 1 (HSD17B1) being developed to treat endometriosis.

Marvelon and Mercilon are combinations of progestin and estrogen used as daily pills to prevent pregnancy, and most recently, Organon has agreed a licensing deal for Xaciato, targeting bacterial vaginosis.

The new acquisitions - other than a >$65m contribution from Marvelon / Mercilin - have not made much impact to date, although management did state on its Q2 2023 earnings call in relation to JADA that it is "fast approaching a threshold where we'll start to disclose its revenue in our product table."

The key asset in this division is still Nexplanon - a long-acting reversible contraceptive, which management believes will achieve blockbuster (>$1bn per annum) sales by 2025. The product accounted for >13% of Organon's total revenues last quarter, with revenues increasing 19% sequentially in the U.S., whilst management says that markets in Latin America and Asia are increasingly opening up.

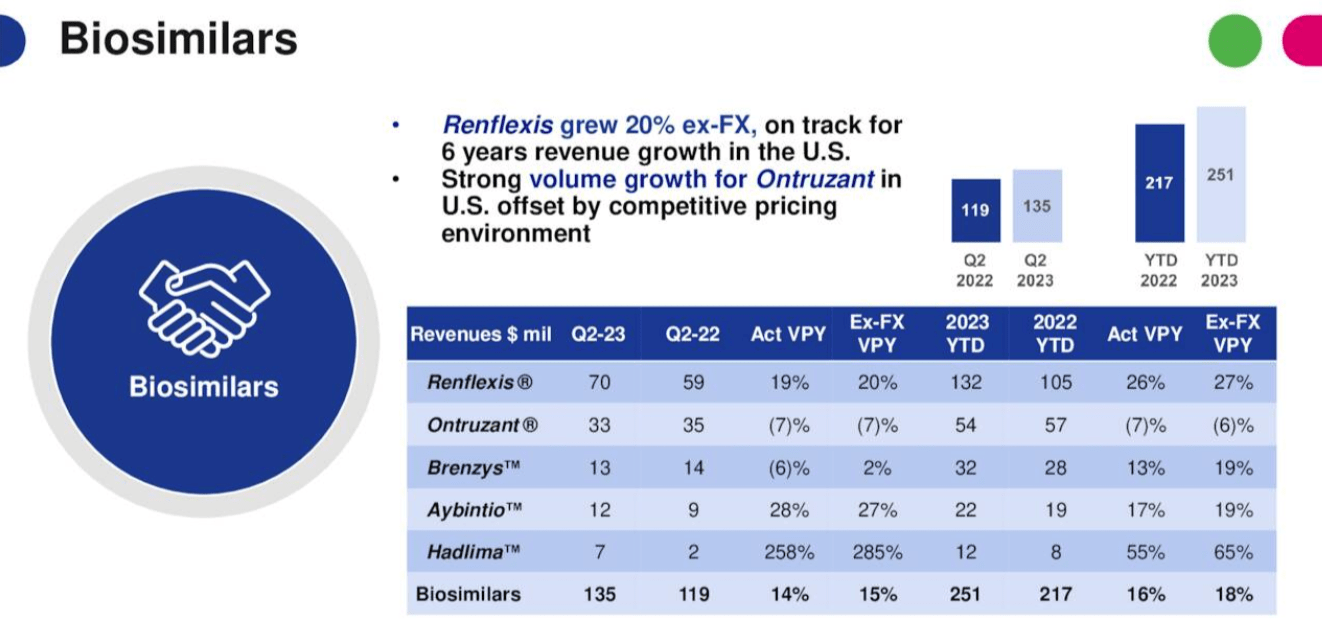

Biosimilars - Hadlima Central To Longer-Term Performance

Organon Biosimilars Q223 performance (earnings presentation)

{kind=link}

As discussed in a prior note, within Organon's biosimilars division:

Renflexis, Ontruzant and Brenzys are biosimilars for autoimmune conditions, breast cancer therapy trastuzumab, and plaque psoriasis respectively, while Aybintio is a biosimilar for Bevacizumab - marketed and sold by Roche ( RHHBY ) as Avastin, and indicated for solid tumor cancers and certain Ophthalmic conditions such as advanced macular degeneration.

As we can see in the slide above - from Organon's Q2 2023 earnings presentation - Organon's smallest division has shown some encouraging growth, led by Renflexis, offset somewhat by declines for Ontruzant and Brenzys. The most important asset in this portfolio today however is Hadlima, a biosimilar for AbbVie's autoimmune mega-blockbuster Humira, which was driving revenues of >$20bn per annum prior to its patent expiry this year.

No fewer than 8 biosimilar versions of Humira will launch this year, and it is very hard to predict which will succeed in a crowded marketplace and which will not, and even what the size of the market place will look like. Humira, as the established, trusted brand, may still command a large market share even at a premium price, with physicians reluctant to switch patients to products they do not know much about.

Organon has opted to price Hadlima at an 85% discount to Humira, with a list price of ~$1k for 2 prefilled pens or syringes, although it should be noted that rebate programs mean patients rarely pay full price for Humira. Hadlima's delivery technology has won awards, and it is running a patient support program, although the drug lacks the valuable "interchangeability" tag, which essentially means it is regarded as identical to Humira, enabling it to be swapped with Humira at pharmacy counters - only Boehringer Ingelheim's Cyltezo has earned this valuable label, although Organon and partner Samsung are working on an interchangeable version.

Hadlima has the ability to kick start Organon's nascent biosimilars division, but if it doesn't succeed commercially, it will be a significant blow for Organon. The jury is still out on the biosimilar market - only 4 biosimilar drugs have earned the interchangeability tag to date, and there may be concerns about profitability, with pricing wars likely to break out between new market entrants - although Organon CEO Kevin Ali sounded a bullish note on the company's earnings call:

The U.S. healthcare system needs biosimilars to be successful. They fill a significant gap in more affordable options for some of the most chronic diseases people face. We're proud of our market positioning and pricing. We're very pleased and encouraged by the signals we are getting so far, and we believe we'll be able to secure further access as this market continues to develop.

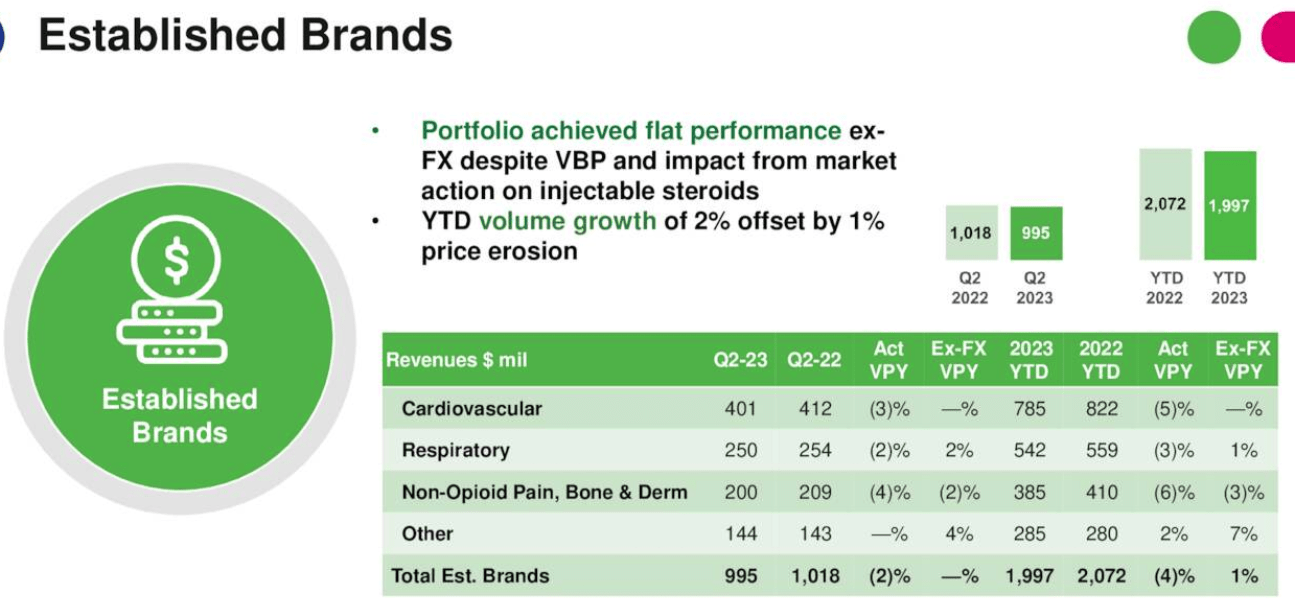

Established Brands - Still Holding Key To Valuation

Despite its flat-to-falling year-on-year performance, Established Brands is still by some distance Organon's most valuable, and arguably important division.

{kind=link}

Established Brands remains Organon's reliable breadwinner, and management trumpeted the division's performance on its earnings call, with CEO Ali commenting that "we've encountered skepticism around how a portfolio of off-patent brands can demonstrate that kind of continued stability," but highlighting the outperformance of brands like cholesterol lowering Atozet, and respiratory therapy Nasonex owing to improved manufacturing capabilities.

No fewer than 6 products earned revenue in the triple-digit millions across the first half of 2023, and the beauty of these products is that they have stood the test of time - unlike new product launches, which can be hit or miss, the demand for these products is well established and trusted.

Concluding Thoughts - Organon Still In Stasis - Share Price Inertia Likely

To summarize Q2 2023 performance and 1H23 performance, it is hard to make a strong case that Organon is either out-performing or under-performing.

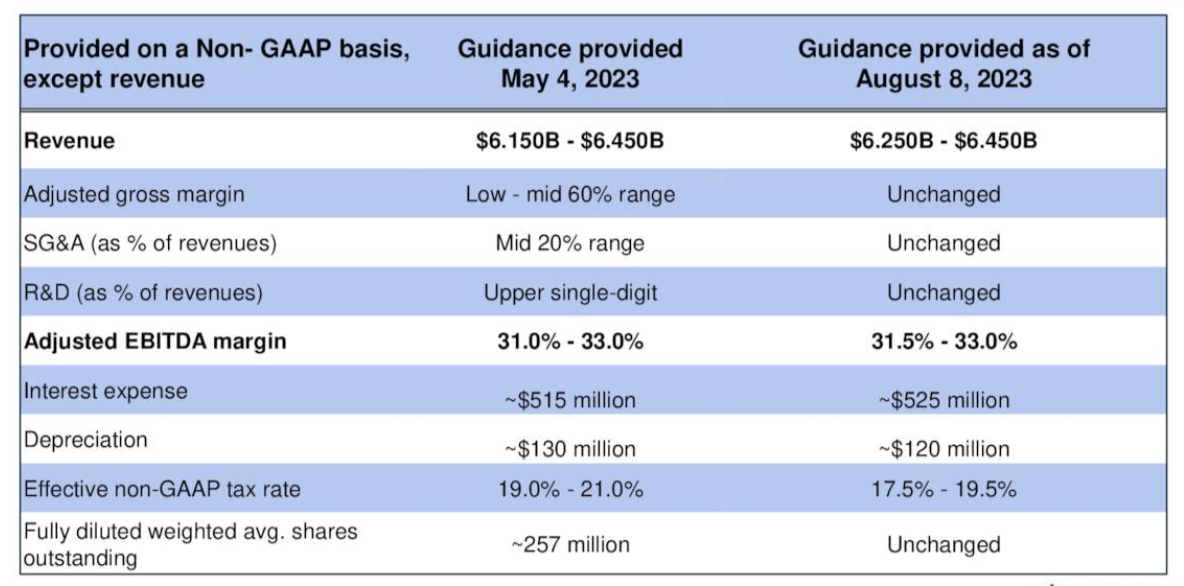

In FY22, the company reported revenues of $6.2bn, EBITDA of ~$1.1bn, and EPS of $3.61. Organon is forecasting for revenues of $6.35bn at the midpoint of expectations in FY23 - a modest improvement - and an EBITDA margin of 31.5% - 33%.

{kind=link}

Teasing out the guidance provided above, on an adjusted basis I arrive a FY23 EPS figure of >$4.5, for a forward P/E of ~5x, which would generally be considered a reasonably strong buy signal. Management also reminded analysts on its earnings call that:

in 2022, we generated just over 75% of our annual cash flow in the second half of the year, and we expect this year to follow that same pattern

An improved performance across the second half of the year, marginal revenue growth, a generous dividend payout ratio, and good profitability are all significant boxes ticked by Organon on the "Buy" side of the ledger, but there are some concerns to consider.

Significantly, it seems Organon has not made much of an inroad into its significant debt pile. Net debt as of June 2023 was $8.4bn, more or less the same as it was in December 2021. As we can see above, Organon will pay an interest expense of >$500m in FY23 - surely this is an area that needs to be addressed if the company wants to drive better bottom line performance, keep paying a good dividend, and perhaps begin a share buyback program to reward shareholders?

A free cash flow figure of >$1bn per annum represents good performance, but it might be a good idea to divert some of this figure into paying down debt. Much depends on the performance of key products such as Nexplanon and Hadlima, both of which are potential blockbuster assets in a best case scenario, but potential underperformers in a worst.

If they do outperform, Organon will have less need to spend its cash on M&A to drive growth, creating a virtuous circle in which more debt can be paid off, interest expense reduced, and shareholders rewarded. If they do not, Organon becomes overly reliant on an established brands division that will almost inevitably shrink in size revenues wise, even if the pace of decline is slower than anticipated.

Ultimately, in my book, Organon - a company I have invested in - remains a "wait and see." I was attracted by the heavily discounted valuation and the dividend, but as explained in my intro, there are good reasons why Organon was valued as low as it was by the market, and they continue to remain central to the company's valuation today - reflecting the fact the business was initially dealt a poor hand by parent company Merck.

Organon is no small company, with ~3.85k employees and manufacturing facilities located in Belgium, Brazil, Indonesia, Mexico, the Netherlands and the United Kingdom. While progress has been incrementally positive since launch operationally, the share price has decreased in value by >25%, and the major concern remains whether the biosimilars and Women's Health divisions are strong enough to supplant Established Brands long-term.

Organon may opt to do as Viatris has done and attempt to divest some assets, shrinking the company in the short term to give itself more strategic options for the long term. That would be one way of addressing what feels like a slight sense of inertia at the company, although it would be a risky strategy, especially when Established Brands continues to perform well.

I plan to keep holding my Organon stock for now, especially with improved performance forecast for the second half of the year, with greater cash flow generation. I'll be watching Hadlima and Nexplanon sales closely and hoping that Organon has some positive surprises within a pipeline that feels under-discussed, that could avert the requirement for further M&A spending.

For further details see:

Organon Q2 2023 Earnings Review: Incremental Growth With A Slather Of Risk