CA - Osisko Mining: De-Risked Following Gold Fields Deal

2023-06-04 23:08:19 ET

Summary

- It's been a busy year for M&A in the gold sector thus far, with several deals already announced, including major acquisitions by B2Gold and Gold Fields.

- Notably, Osisko's partnership with Gold Fields on Windfall is a significant achievement, securing a high price for the sale of half the asset and ending the persistent share dilution.

- However, despite the positive developments, Osisko Mining's valuation remains high compared to other gold producers, and I see limited upside for the stock from current levels.

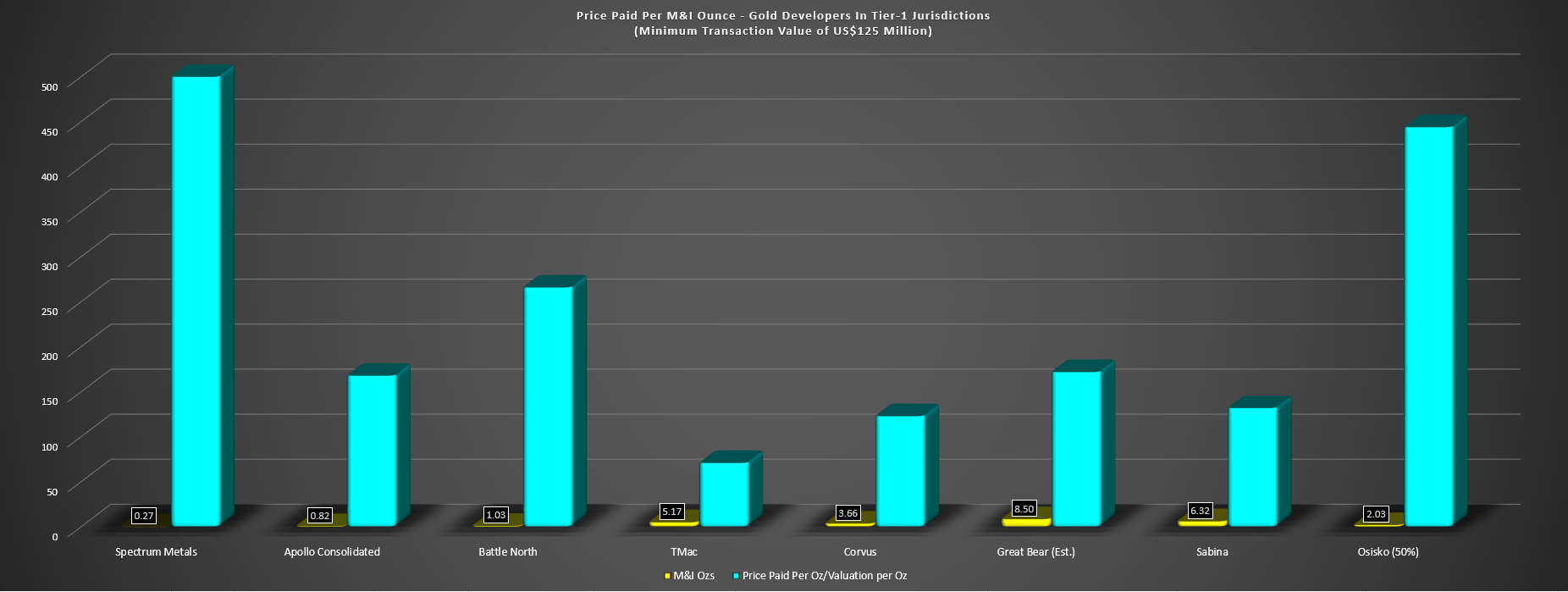

While the past two years were already quite busy from an M&A standpoint in the gold sector, with a few large deals in the producer space (Pretium, Kirkland Lake, Saracen) and a few mid-sized deals in the developer space (Corvus, Great Bear, Battle North, Spectrum), 2023 is looking like it could be a very busy year, with several deals announced already, and two major ones in Tier-1 ranked jurisdictions. These two included the acquisition of Sabina G&S by B2Gold ( BTG ) and the acquisition of half of Osisko's ( OBNNF ) Windfall Project by Gold Fields ( GFI ), a mega-deal with an implied value of ~$900 million or ~$444/oz on M&I resources, the highest price paid in years for a non-producing asset. In fact, if we assume Dixie can prove up the internal target of 8.5 million ounces, the price paid per ounce would be over 150% higher than what Kinross ( KGC ) paid to gain control of Dixie in Red Lake.

Price Paid Per M&I Ounce - Gold Developers in Tier-1 Ranked Jurisdictions (Company Filings, Author's Chart)

{kind=link}

This deal for Osisko Mining is a huge vote of confidence in this asset, and while Gold Fields is certainly paying a premium valuation, I would argue that the current resource and reserve base is conservative at ~7.4 million ounces and ~3.16 million ounces, respectively. So, if we assume 5.0 million ounces of reserves are ultimately proven up (7.0 million M&I ounces), the price paid for Gold Fields half of the project becomes a more palatable ~$258/oz ($902 million / 3.5 million attributable M&I ounces), which while still a premium, is justified for an asset of this caliber (ultra high-grade) in a Tier-1 ranked jurisdiction. That said, while this deal is positive for Osisko Mining, I don't see it helping from a valuation standpoint, even with a reduction in its discount rate from 8% to 6% now that Windfall is fully-funded. Let's take look below:

All figures are in United States Dollars unless otherwise noted at a 0.75 CAD/USD exchange rate.

Gold Fields Partners On Windfall

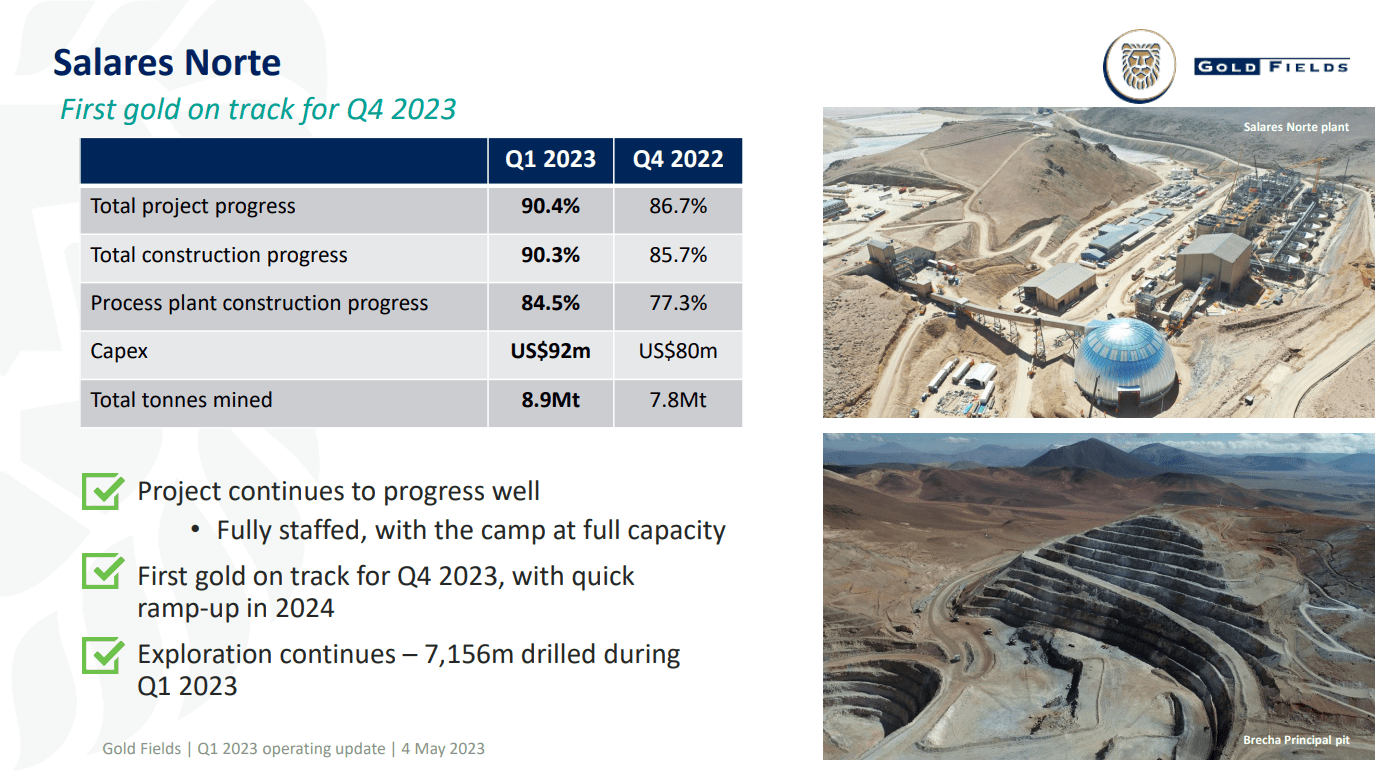

Gold Fields had a hectic year in 2022, constructing its massive Salares Norte Project in Chile, carefully relocating a finicky group of chinchillas from the intended mine site as part of commitments in its Salares Norte EIA, all while working to persuade its investors to vote in favor of a deal to acquire Yamana Gold, one that many shareholders didn't love and felt that they were over-paying. While Salares Norte is progressing on schedule for first gold pour by year-end, Agnico Eagle ( AEM ) and Pan American ( PAAS ) thwarted the Yamana deal when they swept in with a sweetened offer and while it was a disappointment, things have certainly worked out in Gold Fields' favor. This is because the company benefited from the $300 million Yamana deal break-fee and deployed this cash towards acquiring a 50% interest in Windfall last month for an implied value of ~$902 million. Read my previous coverage on OBNNF here.

Salares Norte (Gold Fields Presentation)

{kind=link}

Under the terms of the agreement, Gold Fields and Osisko Mining ("Osisko") will have a 50/50 joint-venture on the Windfall Project in James Bay, Quebec, with Gold Fields agreeing to pay $225 million up front, a deferred payment of $225 million when permits are in place, ~$26 million in two separate cash payments to reimburse Osisko for pre-construction spend, and an agreement to share all pre-construction and construction costs, estimated at ~$780 million on a 100% basis, or what I believe to be a more conservative estimate of ~$810 million given low to mid single-digit inflation sector-wide. Plus, Osisko will also benefit from Gold Fields funding up to ~$56 million in regional exploration, with Osisko and Gold Fields sharing exploration spending once ~$56 million is spent on a 50/50 basis.

For a company has spent hundreds of millions drilling, developing and de-risking the Windfall Project, this allows Osisko Mining investors to breathe a sigh of relief, with the cash injections moving Osisko to fully-funded vs. a previous outlook of taking on significant debt and potential another small equity raise to fund Windfall construction on its own. Plus, it's also validated the acquisition of this property by Osisko near the bottom of the cycle, with the Osisko team going 2/2 on scooping up unappreciated assets in periods of gold price weakness and turning them into future mines (Canadian Malartic was #1 before it was acquired) with a top-5 producer paying a premium to share in this asset's bright future.

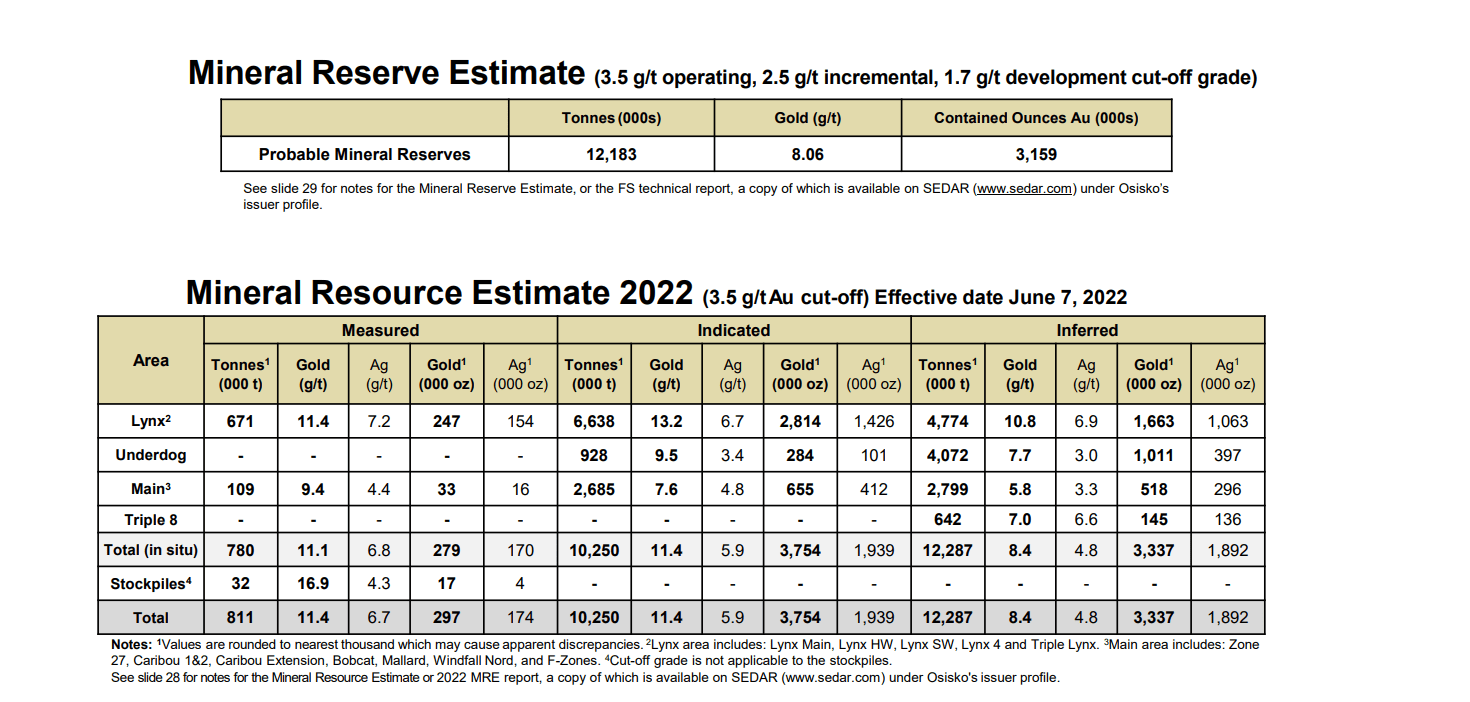

Windfall Project - Reserves & Resources (Osisko Presentation)

{kind=link}

As for Gold Fields, this is a brilliant move, especially with the benefit of the Yamana break-fee to help pay for this acquisition. Not only does the company add a second high-margin asset to its portfolio with two mines set to have sub $850/oz all-in sustaining costs (Salares Norte, Windfall 50%), but it increases Gold Fields' exposure to Tier-1 jurisdictions, with this margin expansion and better jurisdictional profile likely to translate to multiple expansion once Windfall heads into commercial production. Plus, Gold Fields will see a meaningful boost in reserves and production per share with this being a cash deal, as well as an improvement in its overall reserve grade from ~2.7 grams per tonne of gold to closer to 3.0 grams per tonne of gold assuming continued reserve growth at Windfall which looks likely.

Some investors might assume that this should lead to a re-rating in Osisko's share price, with the project now fully-funded with a very well-capitalized partner, and the project on track to pour first gold by late 2025 assuming the timely receipt of permits. However, despite the high price paid for the shared interest in Windfall (~$444/oz on current M&I resources vs. ~$207/oz since 2020), my fair value estimate on a per share basis for Osisko has stayed the same, even if it has de-risked the stock and put a backstop on future share dilution. The reason is that I was not expecting another dilutive financing in Q1 2023, with ~32.2 million shares sold at US$2.33 with half warrants at US$3.00, increasing the share count by over 10%. And this is not the first financing at unfavorable prices, with ~14.7 million shares sold near a cyclical low for gold at ~US$1.40.

To summarize, I see the two real winners here being Osisko Gold Royalties ( OR ) and Gold Fields, with the former having a clear path to this asset being developed with a top-5 operator by size that will lead to an increase in the exploration budget and added technical expertise. For those unfamiliar, Osisko Gold Royalties holds a 2-3% NSR on Windfall and a significant royalty on land outside of the main mining area, including a 3.0% NSR for most of the land package including Lynx extensions, a 1.5% NSR just southwest of Underdog (southwest most deposit), and a potential 3.0% NSR on Golden Bear if this deposit is extended further to the north. For Gold Fields, the benefits are obvious, with future margin expansion once Windfall is developed with a fair price paid. Let's dig into the valuation below and why I struggle to see much upside for Osisko Mining from current levels:

Valuation

Based on 460 million fully diluted shares and a share price of US$2.50, Osisko Mining trades at a market cap of $1.15 billion, making it one of the highest valued gold developers sector-wide. Given that Windfall is arguably one of the top-5 undeveloped gold projects globally in a Tier-1 jurisdiction next to Mallina ( DGMLF ) and a couple of others, a premium is certainly justified, and this is especially true now that Osisko has teamed up with a top-5 gold producer by scale on the asset. However, when we factor in most of the payments (~$476 million) going to pre-construction costs (estimated $100 million attributable), construction costs (estimated at $310 million attributable) and Osisko now only having a 50% interest in Windfall and the surrounding land package, I would argue that we've seen a slight downgrade in valuation.

As for Osisko's attributable ownership in Windfall, I see a fair value of ~$710 million (50% basis) at a $1,925/oz gold price. I have made the following assumptions over the mine life and the discount rate when calculating this NPV figure:

- 5% positive grade reconciliation

- higher throughput starting in 2030 of 4,000 tonnes per day

- 6% discount rate

These assumptions incorporate converting new/existing resources into reserves with a 15-year mine life, a $620 million build cost, and more conservative estimates for mining costs given that commercial production won't start until at least 2026 (we continue to see low to mid single-digit inflation and sticky labor costs sector-wide). A 6% discount rate vs. the 8% discount rate used previously is warranted in my view given that Windfall is fully financed, but is not yet permitted. Plus, while I expect Windfall to perform as envisioned, the fact is that this isn't an operating mine yet where a 5% discount rate would be more appropriate.

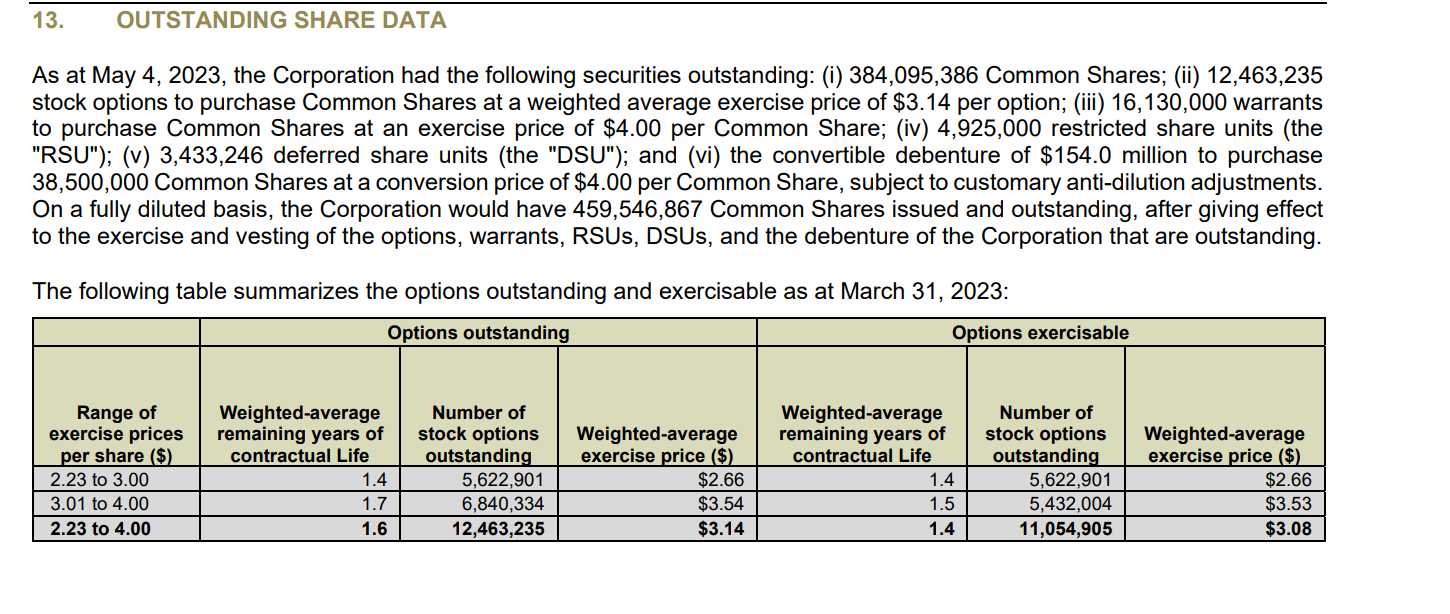

Share Count & Options (Company Filings)

{kind=link}

Using this assumption and an estimated pro-forma cash position of ~$590 million and adding $300 million in exploration upside for regional targets and its vast land package, this would translate to a fair value of $1.60 billion (1.0x NPV), or $1.71 billion using a 1.15x P/NPV multiple given that Windfall is a world-class asset. However, Osisko will need to spend ~$410 million to recognize cash flow from this asset (pre-construction costs/construction costs), reducing its cash position to ~$180 million. Plus, given that Osisko is not being bought out and will be a shared operator of the mine over its future mine life, we need to subtract corporate G&A from its NPV estimate. For this reason, I have given no value to proceeds from warrant/option exercise, given that corporate G&A will more than offset these proceeds. In fact, corporate G&A should far exceed the proceeds from its warrants/options (~$70 million) with what will likely be higher annual costs once it graduates to producer status (2026), but we'll assume a clean offset of warrant/option proceeds vs. future corporate G&A to keep things simple.

Exploration upside for Osisko assumes the discovery of 1.50 million new M&I ounces at a value of $200/oz on an attributable basis (3.0 million ounces on a 100% basis). This may appear too conservative but, as noted, I have already assumed a ~5.0 million ounce reserve base in the modeled mine plan and extended the mine life out to 15 years with a moderate throughput expansion, so a large portion of ounces drilled off in mineral resource inventory and a 500,000 ounce mineral reserve at Golden Bear are already included in the NPV (6%) figure.

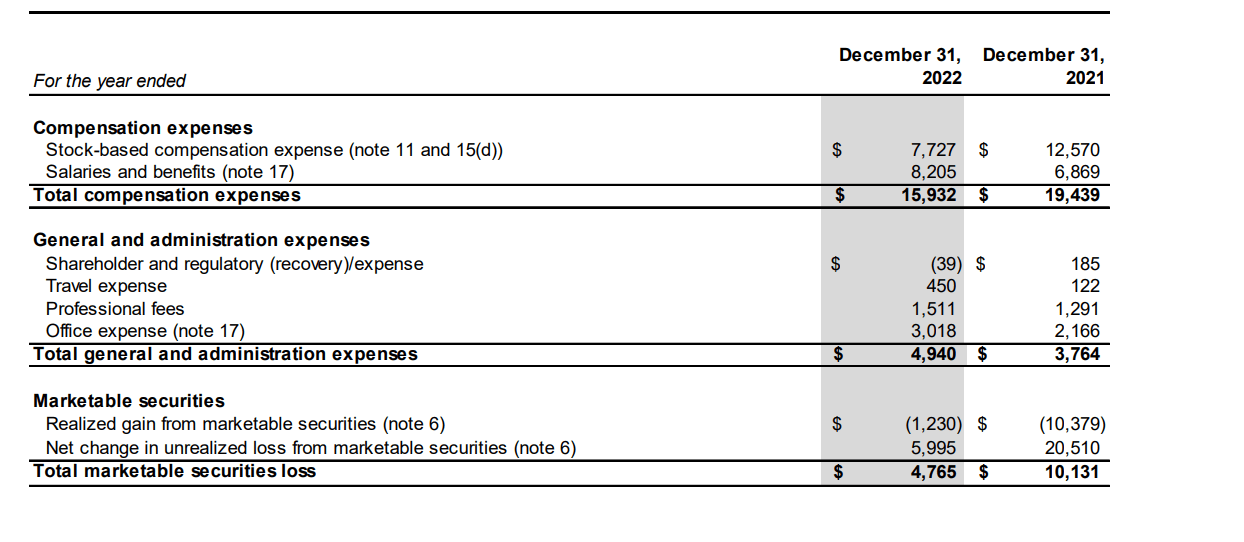

Corporate G&A/Compensation 2022 vs. 2021 (Company Filings)

{kind=link}

This leaves us with the following fair value assumptions:

- Windfall Project (50% ownership) NPV (6%) with 1.15x NAV multiple: $710 million ($710 million x 1.15 P/NPV = $817 million)

- Exploration Upside (50% ownership): $300 million

- Cash Position (following Gold Fields payments): $590 million

= $1,707 million

- [-] Pre-Construction/Upfront Capex: $410 million

= $1,297 million

/ 460 million fully diluted shares

= US$2.82

As shown above, this translates to a fair value for Osisko of ~$1.3 billion, and after dividing by 460 million fully diluted shares, this points to a share price of US$2.82 per share. Investors might believe this is far too conservative of an assumption, but this valuation is actually quite similar to what we see from Gold Road Resources ( ELKMF ) today, which is in arguably a very similar position to Osisko with 50% ownership of the Gruyere Project in Australia that it shares with Gold Fields. The mine has a slightly higher annual production profile of ~350,000 ounces, sub $980/oz all-in sustaining costs, but Gold Road also holds a ~20% interest in De Grey Mining (valued at ~$270 million), a significant exploration portfolio with ~2,800 square kilometers of 100% owned land (Southern Project Area near Gruyere), and 180 square kilometers of shared land in a joint-venture, and it's in production today, not an unpermitted (albeit advanced) developer like Osisko. Today, Gold Road trades at a market cap of $1.35 billion, in line with what I believe to be a fair value for Osisko.

Gruyere Mine - Gold Road/Gold Fields (Gold Road Presentation)

{kind=link}

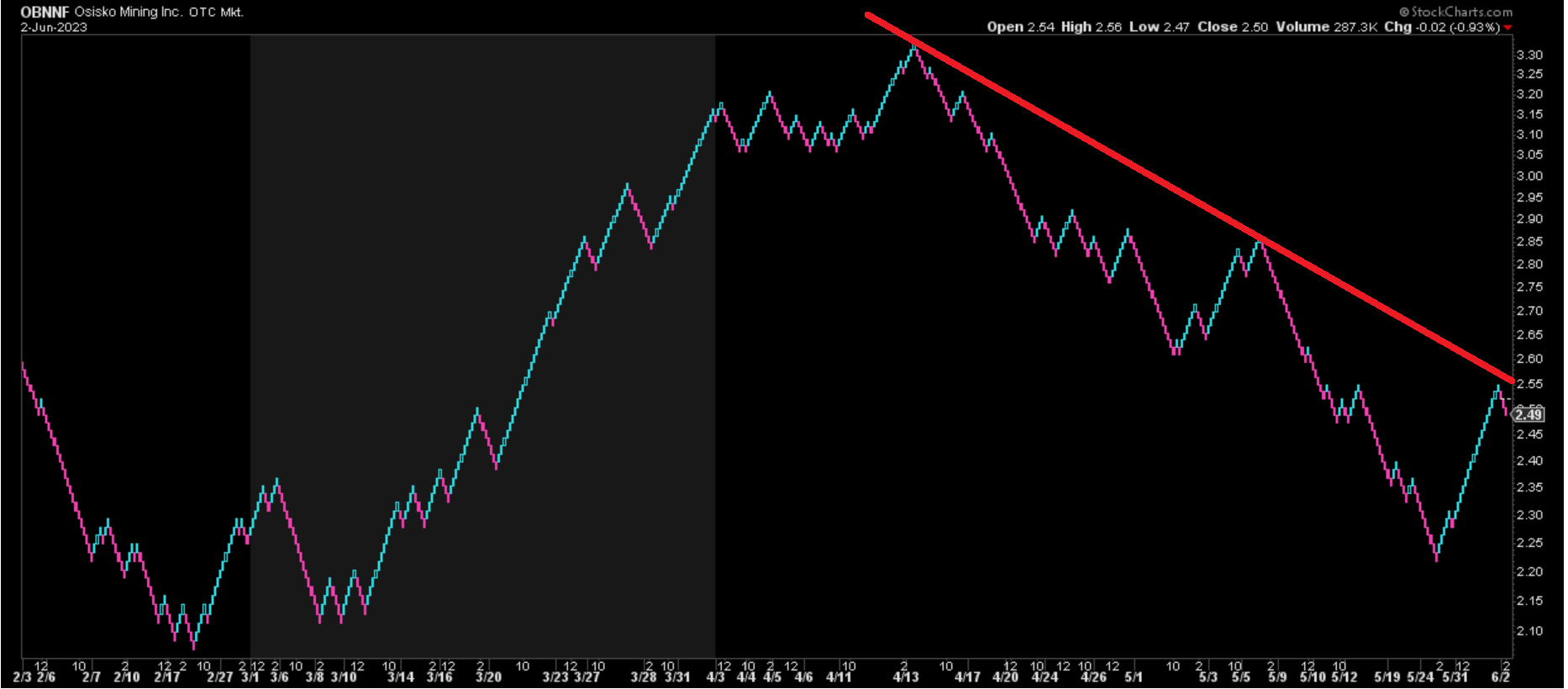

Although a fair value estimate of US$2.82 might point to a 13% upside from here, I require a large margin of safety when starting new positions in gold developers, with a typical margin of safety requirement of 40% (meaning a 40% discount to fair value). In Osisko Mining's case, I believe a 30% discount is appropriate given its partnership with Gold Fields and the fact that it's fully-funded. However, even if we apply this lower discount to an estimated fair value of US$2.82, the ideal buy zone for Osisko Mining comes in at US$1.98 per share or lower, suggesting the stock is nowhere near a low-risk buy zone currently. This is corroborated by the technical picture, with the stock rallying straight into a broken downtrend line, and its renko chart flipping back to a bearish alignment as of Friday's close.

Osisko Mining - 4- Month Chart (StockCharts.com)

{kind=link}

Summary

Osisko's success partnering with a top-5 gold producer on Windfall is a significant achievement and it will put an end to the continued share dilution we've seen over the years that has been partially offset resource growth, explaining the persistent underperformance of the stock since 2016. And Osisko certainly got a solid price for its sale of half of this asset, and also secured a setup where Gold Fields has agreed to spend a significant amount on regional exploration (up to $56 million) to speed up resource growth and provide more clarity on the regional potential of this land package. Plus, Gold Fields paid the highest price in the past three years to gain a shared interest in Windfall at an implied value of ~$444/oz.

That said, the project is still not yet permitted and full construction has not begun, yet Osisko trades at a valuation above that of many 150,000+ ounce low-cost gold producers that are in production today and generating meaningful free cash flow. And while I am confident that it will be permitted, there is risk to delays to realizing commercial production as permits rarely ever arrive ahead of schedule and there are risks to cost creep if inflationary pressures persist, and I've modeled only a 5% miss on capex ($620 million vs. $590 million). Hence, while a premium valuation is warranted and I would argue that the mine plan is very conservative, I struggle to see much upside even after accounting for a more robust mine plan. To summarize, I don't see any margin of safety in Osisko Mining at current levels, and I see several more attractive bets from a relative value standpoint elsewhere in the market.

For further details see:

Osisko Mining: De-Risked Following Gold Fields Deal