CA - Osisko Mining: Limited Margin Of Safety At Current Levels

2023-04-09 07:11:41 ET

Summary

- Osisko Mining has been one of the best-performing gold juniors year-to-date, up 23% for the year following three years of share-price consolidation.

- The recent outperformance can be attributed to excitement surrounding Windfall's first gold pour (2026?), and the recent bid under the gold price, which has improved sector-wide sentiment.

- However, following additional share dilution combined with the recent rally, Osisko's fully diluted market cap is pushing ~$1.45 billion, placing the stock at a premium to net asset value.

- Given that Windfall is one of a kind, a premium is warranted, but the reward/risk isn't nearly as favorable today, making it tough to justify starting new positions above US$3.15.

It's been a rough two years for the Gold Juniors Index ( GDXJ ), and especially the ASA Gold&Precious Metals Fund ( ASA ) which holds more development-stage names. This is evidenced by a 39% decline for the Gold Juniors Index since its July 2020 peak and a 35% decline for the ASA Gold & Precious Metals Fund in the same period. Not only have these returns massively underperformed the Nasdaq Composite ( QQQ ) despite it just suffering its worst year in a decade, but the indexes have also underperformed the commodity that investors in these funds have been bullish on, gold ( GLD ), by roughly 4000 basis points.

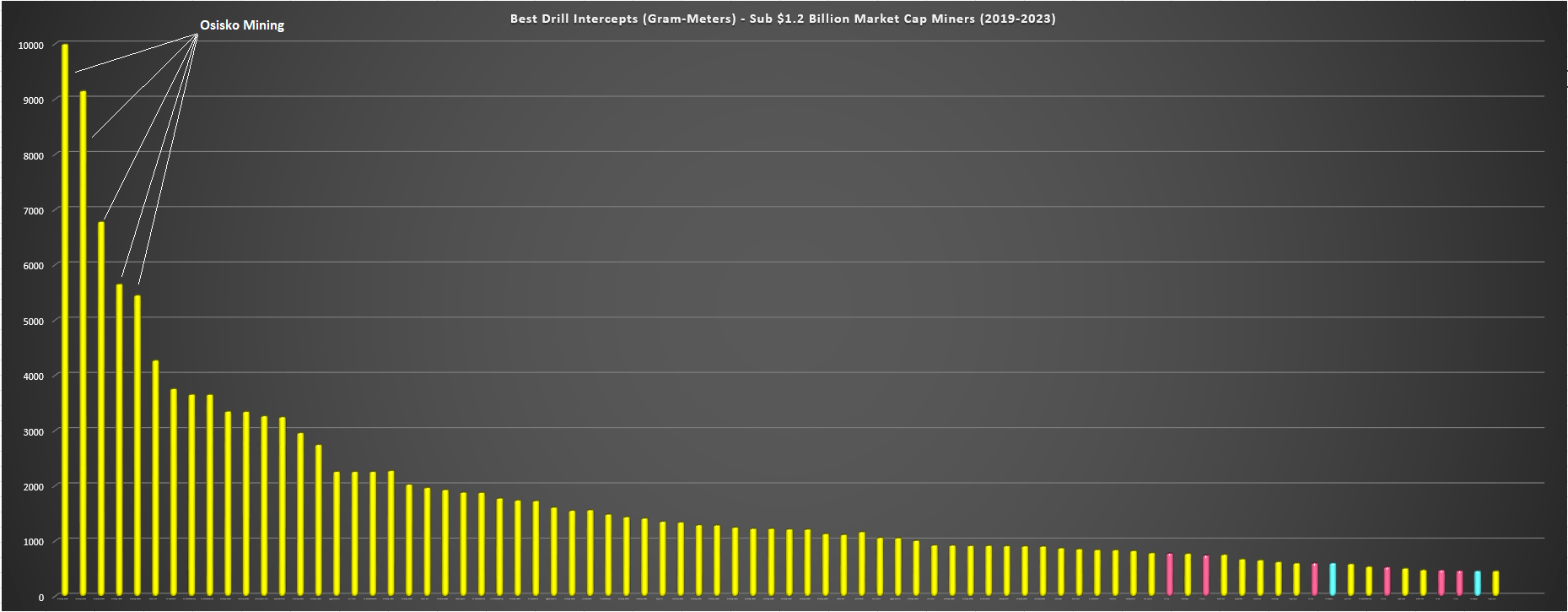

Top Drill Intercepts (2019-2013) - Gram-Meters Basis, Sub $1.2 Billion Market Cap Miners (Company Filings, Author's Chart)

{kind=link}

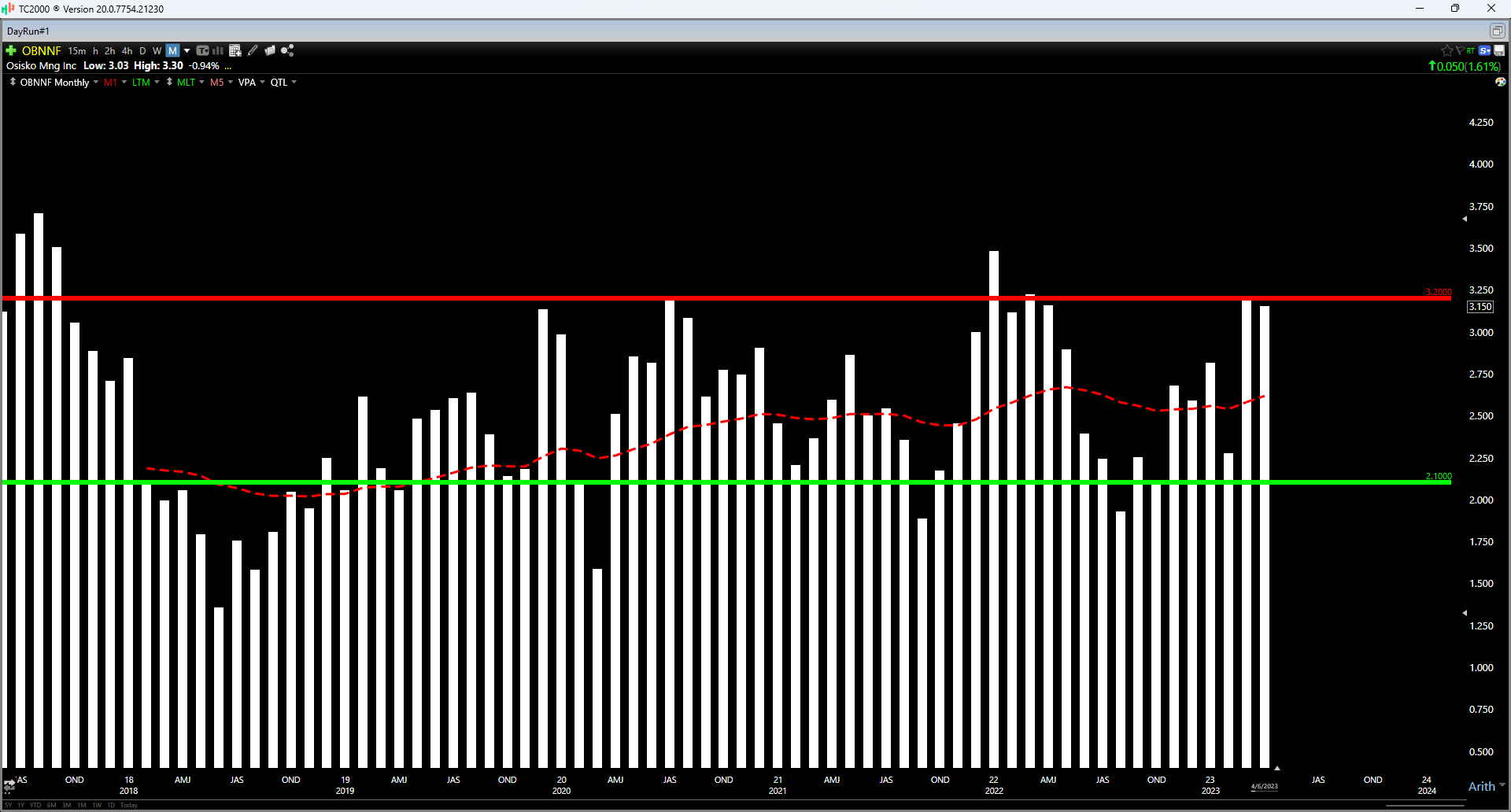

Despite blockbuster drill results over the past two years, with Osisko Mining ( OBNNF ) holding 30 spots (including the top spot among 80) for best holes drilled on a gram-meter basis in the gold space (sub $1.2 billion market caps), Osisko's share price has struggled immensely, with sharp rallies running into selling pressure. This can be partially attributed to continued share dilution, resulting in the stock's valuation increasing even as it stagnates, with the latest deal adding ~11% share dilution only slightly above multi-year lows at US$2.30 (plus half warrant). So, while I see Osisko Mining one of the few juniors that is investable at the right price, the recent rally and share dilution has led to a less favorable reward/risk setup here at US$3.15.

All figures are in United States Dollars with a CAD/USD exchange rate of 0.75 to 1.0 unless otherwise noted.

Recent Developments

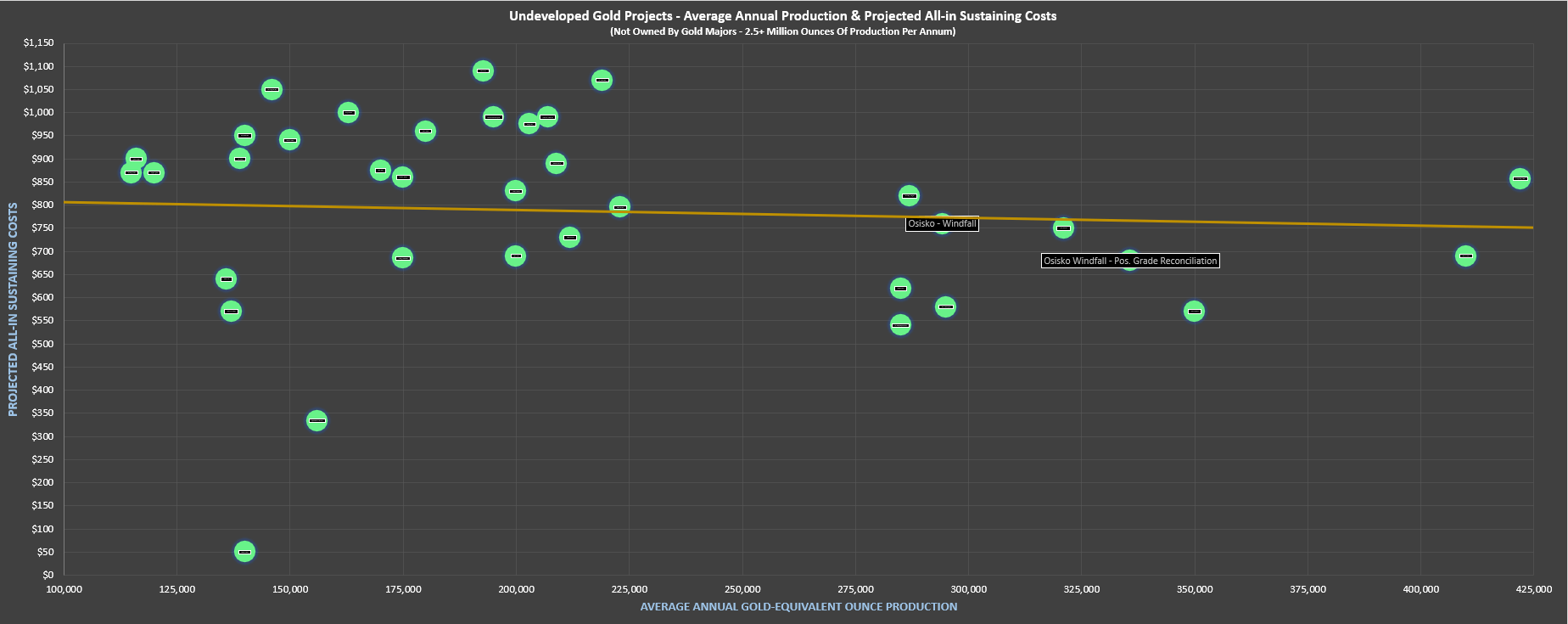

Osisko Mining has had a busy few months since my previous update , with the first major release of the year being the filing of its most recent Feasibility Study, which has highlighted a project capable of being one of the highest-margin and highest-grade gold mines globally. This is based on Osisko's Windfall having the potential to produce over 300,000 ounces of gold per annum on average (peak production of ~374,000 ounces in Year 2), at all-in sustaining costs below $800/oz. However, if we see positive grade reconciliation, this could end up being a ~325,000+ ounce per annum asset, with peak production knocking on the door of 400,000 ounces per year. This makes Osisko a rarity in the sector, and one of the undeveloped projects that nearly meets Barrick's "Tier One" definition.

According to Barrick's rigid criteria , a Tier One gold asset is one "with a reserve potential to deliver a minimum 10-year mine life, annual production of at least 500,000 ounces of gold, and total cash costs in the lower half of the industry cost curve ." While Osisko's Windfall two criteria (estimated cash costs of ~$590/oz & a 10+ year mine life even without considering depth extensions), it doesn't quite meet the 500,000 ounce per annum threshold, with average production likely to come in closer to 325,000 to 330,000 ounces even with positive grade reconciliation. That said, in the hands of a major that might explore hoisting ore with a shaft plus ramp access (assuming the resource continues to grow) or increasing mining rates with a satellite deposit like Golden Bear plus Windfall Main, this could meet Tier One criterion.

{kind=link}

Plus, as we can see from the chart below, even if Osisko's Windfall doesn't quite meet the Tier One definition, it is a phenomenal asset. As we can see below, there are only a few deposits with this scale and even fewer with a combination of 300,000 ounces of potential gold production per annum plus sub $800/oz all-in sustaining costs [AISC]. So, with industry average all-in sustaining costs rising to $1,300/oz and even some majors now flagging costs above $1,300/oz despite economies of scale, Windfall is one project that would complement the portfolio of nearly any producer from a margin standpoint, and even the highest-margin producers like Lundin Gold ( LUGDF ). Finally, while capex isn't cheap, it is manageable at ~$590 million, or ~$630 million if we assume some cost creep which wouldn't shock me given the inflationary environment.

Osisko Mining - Windfall + Windfall Positive Grade Reconciliation vs. Other Undeveloped Gold Projects (Company Filings, Author's Chart)

{kind=link}

In addition to highlighting a robust project that could be a top-10 mine in Canada by scale (similar to Island Gold P3+ and behind Detour Lake, Canadian Malartic, Cote, Greenstone, Meliadine, Blackwater, Hope Bay), Osisko announced a definitive agreement with Miyuukaa Corporation for construction and delivery of hydro-electric power to Windfall. The 69 kV transmission line will be constructed, owned and operated by Miyuukaa (wholly-owned subsidiary of the Cree First Nation) from the Waswanipi sub-station and the hook-up to Windfall could be as early as March 2024, reducing upfront capex for Osisko and providing low-cost power directly to site, an enviable position to be in similar to most of Agnico Eagle’s Canadian operations.

Finally, Osisko announced the submission of its Environmental Impact Assessment Report to the Environmental and Social Impact Review Committee. If approved, Windfall would contribute ~$2.0 billion to Quebec’s GDP by 2035, nearly $3.0 billion in total investment for construction, sustaining capital, and operations, and result in the creation of ~17,000 direct and indirect jobs. Given the considerable benefits and the limited environmental footprint (low-volume, high-grade underground operation) in a remote area in northern Quebec, I would expect minimal opposition and the project to be green-lighted next year. Hence, the only two major hurdles left are permitting and financing the project, and with a rapid payback at a $1,900/oz gold price, financing with mostly debt shouldn’t be an issue.

Unfortunately, this positive news was overshadowed by another significant capital raise (with half warrants attached), resulting in another ~48 million shares being added to the share count assuming all warrants are exercised. This has resulted in 11% dilution, meaning that even at a static share price, the stock has become nearly 12% more expensive. And if we combine this with a more than 40% rally in the share price off the lows, Osisko is short-term overbought and nowhere near as attractively valued. Let’s take a closer look below:

Valuation

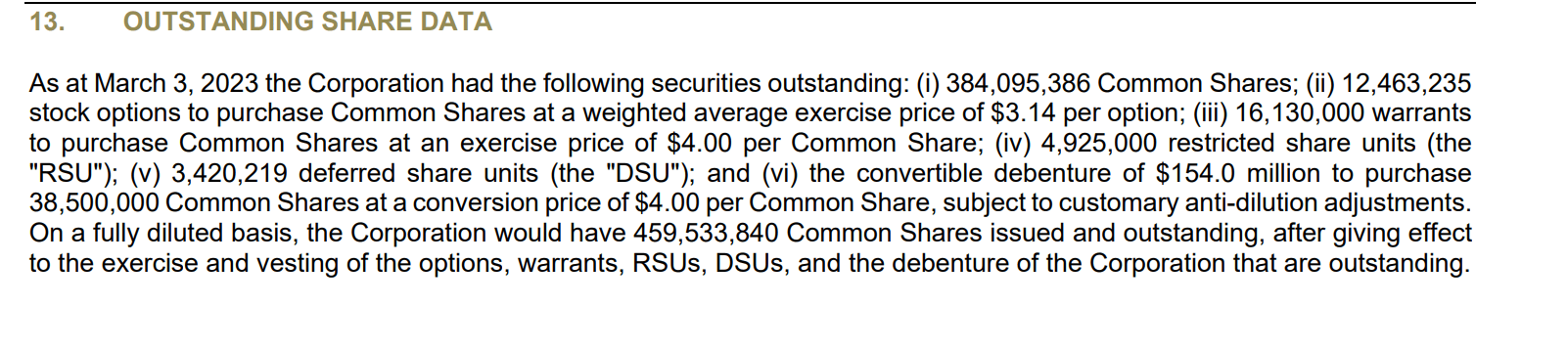

Based on an estimated ~462 million fully diluted shares at year-end and a share price of US$3.15, Osisko trades at a market cap of US$1.46 billion, a figure that dwarfs the valuation of even some producers. This premium relative to some producers is warranted, given that this is arguably one of the top-10 unmined deposits globally from a grade and margin standpoint, and expected head grades look to be conservative. That said, we've now reached the point where the stock looks to be getting a little ahead of itself, especially when factoring in the recent ~11% share dilution that was well above what I was expecting because of capital being raised at unfavorable prices yet again. Unfortunately, this wasn't the first time we've seen dilutive financings at unfavorable prices.

Osisko Mining - Outstanding/Diluted Shares (Company Filings)

{kind=link}

The other painful capital raises that contributed to share dilution were ~14.7 million shares at US$1.31 in 2018 to Kirkland Lake Gold, ~9.3 million shares at US$2.15, and ~26.1 million flow-through shares at US$1.95 also in 2018, all near a major cyclical low for the sector.

Using an 8% discount rate, which I believe is more suitable today for gold developers (higher-risk) building in an inflationary environment, especially with where interest rates sit today, and assuming some cost creep vs. the expected ~$590 million build cost and baking in high single-digit positive grade reconciliation plus an $1,850/oz gold price, this translates to an estimated NPV (8%) of ~$890 million. After adding in $390 million for exploration upside (2.6 million M&I ounces added at $150/oz), we arrive at a fair value for Osisko of ~$1.32 billion. If we divide this figure by ~462 million fully diluted shares (year-end share count) and apply a 1.1x P/NPV multiple given that this is a top-10 project globally, I see an updated fair value for Osisko Mining of ~$1.37 billion [US$2.96].

If one prefers to use a 5% discount rate to value Osisko Mining and we apply the same exploration upside and use the same gold price, Osisko's estimated NPV (5%) would increase to $1.28 billion, with a fair value of ~$1.67 billion when including exploration upside, or ~$1.8 billion in fair value [US$3.90] at a 1.1x P/NPV multiple. Although this points to a 24% upside from current levels, I am looking for a minimum 40% discount to fair value when buying gold developers, even if they own of one of the richest ore bodies globally in a Tier-1 jurisdiction. After applying this 40% discount, the ideal buy zone would come in at US$2.35 or lower, significantly below current levels.

Osisko Mining - September 14th, 2022 Article (Seeking Alpha Premium/PRO)

{kind=link}

An investor can choose how they wish to value Osisko Mining, but with the stock being fully valued using a more appropriate 8% discount rate and only having 21% upside to fair value using a less conservative 5% discount rate, I no longer see the reward/risk being nearly as attractive as it was when I highlighted the stock as a Buy below US$2.20 in September. That said, a rising tide (gold price) could lift all boats, and with this being one of the better stories sector-wide, I certainly wouldn't rule out further upside. However, for starting new positions, I see an unfavorable reward/risk setup here short-term at US$3.15 and the stock is heading into a potential resistance zone at US$3.20, hence why I am moving back to Neutral.

{kind=link}

Finally, regarding a potential takeover, the most likely suitor would be Barrick ( GOLD ) with tax pools and this fitting their Tier-2 criteria, but I imagine Osisko is looking for top dollar after having Canadian Malartic stolen from them last decade. Given that Barrick's CEO Mark Bristow is about as disciplined as it gets, I don't see Osisko as nearly as likely as a takeover target as it was at its recent lows when a 40% plus premium still would have been a steal for a suitor. Hence, while Osisko's Windfall certainly has all the attributes that would place it in high demand by potential suitors, I would imagine fewer suitors are interested at this valuation, and the two that were the most likely to transact due to tax benefits have done other major deals (Great Bear) or are more focused on organic growth, and only M&A at bargain prices.

Summary

Osisko Mining is truly a unicorn in the gold developer space, with an asset that could boast 10.0+ gram per tonne head grades in a Tier-1 jurisdiction (assuming positive grade reconciliation) and produce ~300,000 ounces per annum at sub $750/oz all-in sustaining costs. This would place its margins over 90% above the industry average ($1,100/oz vs. $560/oz) at an $1,850/oz gold price, and this is certainly the type of project that producers of all sizes would love to have in their portfolio. However, as Joel Greenblatt states, "there's no investing without valuation" , and with a market cap of ~$1.45 billion with what's likely to be at least 30 months until the first gold pour, I now see more relative value elsewhere. One example is Marathon Gold ( MGDPF ), a beaten-up developer trading for well below fair value.

For further details see:

Osisko Mining: Limited Margin Of Safety At Current Levels