CA - Osisko Mining Receives A Windfall

2023-06-14 11:00:17 ET

Summary

- Osisko Mining Inc. has announced it concluded a 50/50 joint venture agreement with Gold Fields Limited on Osisko's Windfall gold project in Canada.

- Osisko Mining is receiving US$475 million (or C$634 million) of cash from Gold Fields + C$75 million of exploration spending is covered by Gold Fields. The Feasibility Study is only the starting point.

- Using a conservative valuation analysis, Osisko Mining is trading at 0.65x NAV. When using assumptions from Osisko, the stock is trading at just over 0.5x NAV.

- The short-term outlook for the stock is more difficult to predict, but if gold breaks out, I plan to be very long Osisko Mining. When using a longer-term time horizon, there is enough value that buying at current levels could be considered prudent.

Last month, Osisko Mining Inc. (OBNNF) announced it had concluded a 50/50 joint venture agreement with Gold Fields Limited (GFI) on Osisko's Windfall gold project in Canada.

In return, OBNNF receives the following:

- GFI made an initial cash payment to Osisko of US$225 million (C$300 million) on signing.

- GFI will make another cash payment of US$225 million (C$300 million) to Osisko on the " issuance of the applicable permits authorizing the construction, operation and mining of the Windfall Project. "

- Gold Fields will fund all regional exploration of up to C$75 million over the first seven years at the Urban Barry and Que?villon district exploration camps. After which, exploration spend will be shared 50/50.

{kind=link}

4. Finally, Gold Fields will make two additional cash payments - each US$12.75 million (C$17 million) - to Osisko this year for reimbursement of part of the pre-construction spend incurred by Osisko.

=

~US$475 million (or C$634 million) of cash from GFI

+

C$75 million of exploration spending is covered by Gold Fields

The two JV partners will share all pre-construction costs (US$187.5 million/C$250 million) and construction costs (US$591.75 million/C$789 million) on a 50/50 basis going forward.

This is incredibly bullish news for OBNNF for a host of reasons:

- The company is now fully funded for its portion of CapEx.

- It will not have to take on any debt to build Windfall, giving it an enormous advantage over other developers and a boon for shareholders, as OBNNF will exit the construction period with net cash (assuming CapEx comes in line with budget).

- The risk of more dilution for OBNNF has dropped considerably.

- GFI is funding a substantial amount of regional exploration.

- GFI is a proven mine builder and operator and gives Windfall even more credibility than it had before. With GFI as a partner, Windfall will be fast-tracked and its full-steam ahead.

However, the stock declined materially the day the news was announced and has underperformed the sector since then.

Why?

Because investors apparently were looking at Osisko's US$1.1 billion market cap at the time and thinking it meant the stock was overvalued and this deal somehow limits the upside. These assumptions are way off base.

The market cap of OBNNF is now around US$925 million. The ~US$475 million of cash from GFI and ~US$32 million of net cash at the end of March 31, 2023 (not including marketable securities and investments in associates) effectively gives it a pro forma EV of US$418 million.

The value of Windfall at current gold prices and exchange rates is ~$1.3 billion, or ~US$650 million for Osisko's 50% share. That already implies OBNNF is undervalued. However, Windfall contains over 7 million ounces of gold, and the Feasibility Study ("FS") only considered less than half of those ounces. Additional valuation drivers could also drastically increase the NPV of Windfall.

Why The Feasibility Study Is Only A Starting Point For The Valuation

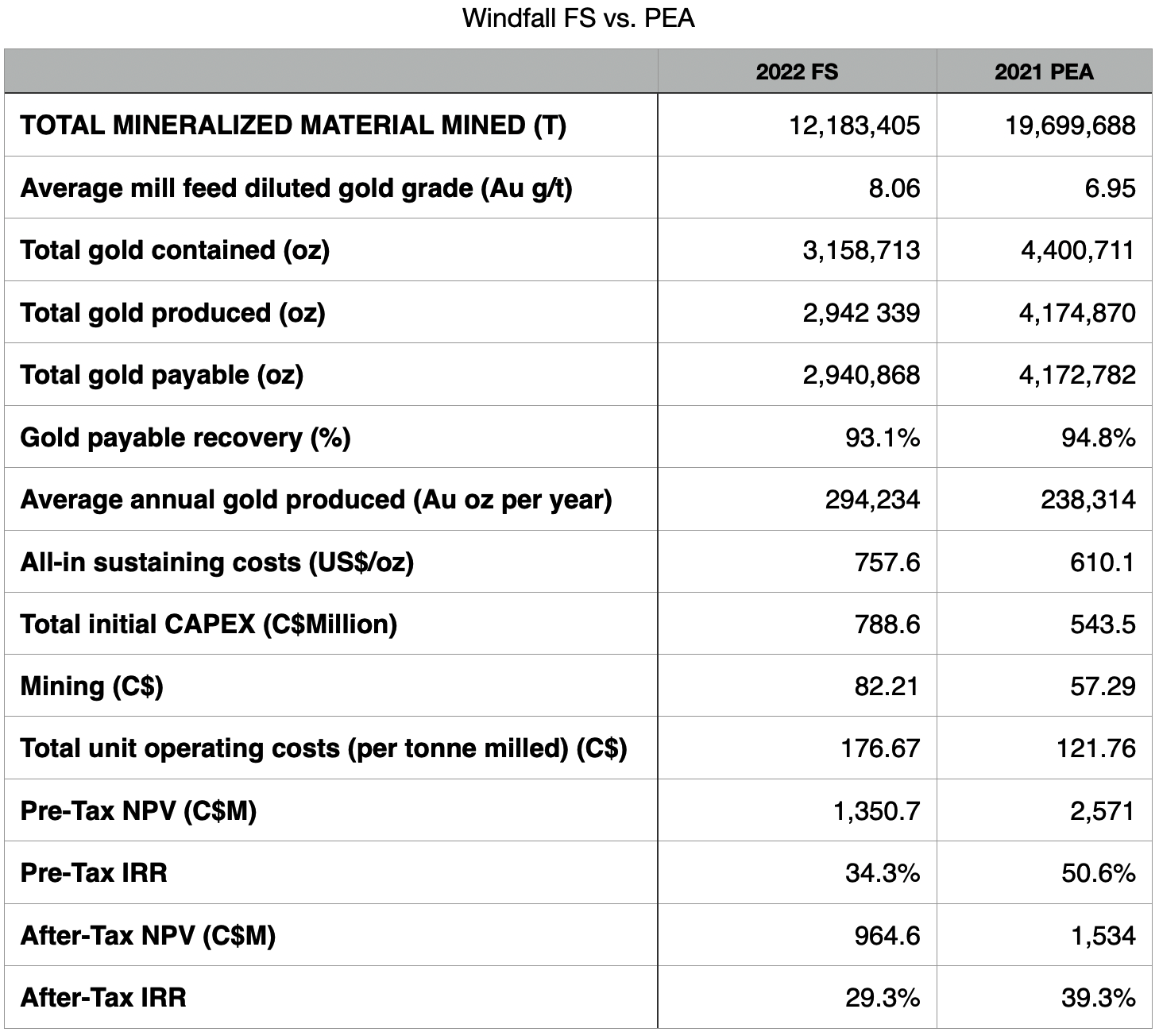

I've compiled a table comparing the 2022 Feasibility to the 2021 Preliminary Economic Assessment ("PEA"). I've only included the key operating and financial metrics (e.g., gold produced, average annual production, AISC, initial CapEx, and NPV and IRR), and there are notable differences between the two studies.

The PEA contemplated mining much more mineralized material, with total production estimated at almost 4.2 million ounces of gold. Compare that to the FS, which estimated just over 2.9 million ounces, or 30% less than the PEA. Gold recovery is still quite strong in the FS, although slightly lower vs. the prior study. The average annual gold production is dramatically higher in the FS, but that's because the mine life has been shortened to 10 years compared to 18 years in the PEA. AISC increased by ~25%, but on a per-ounce basis, it's only a US$150 increase.

That's quite good news, because costs for many companies in the sector have increased significantly since 2020, and an AISC of just $758 per ounce would still make Windfall one of the lowest-cost gold mines in the world. Even at $1,600 gold, margins are exceptional. An increase in initial CapEx was also expected due to inflation, with the budget now C$788.6 million, or a 45% increase compared to the PEA. While it's a meaningful bump up, it could've been worse, as some projects in the sector are experiencing 75-100% surges in CapEx vs. previous studies conducted in 2020-2021. The paste backfill plant is also now part of the initial CapEx instead of sustaining, so the higher CapEx wasn't all due to inflation. When you account for some sustaining moving to the initial CapEx column, the overall increase in construction capital wasn't exorbitant.

What helps Windfall is its grade and that it's an underground mine (i.e., less tonnage), as that means a smaller plant is needed and, overall, a smaller footprint for the entire above-ground infrastructure. Speaking of grade, that did jump in the FS, as Windfall will be one of the higher-grade gold mines in Canada (and the world, for that matter) when it enters production. The bottom of the table focuses on the NPV and IRR of the project and is based on a $1,500 gold price. It reflects how the lower production, higher Capex, and higher OpEx, all negatively impacted the economics of the FS.

{kind=link}

However, the two studies' total material mined, production, and NPV/IRR metrics aren't an apples-to-apples comparison. When you dig deeper, there is a reason for the differences, and the actual production from Windfall could exceed not just what was estimated in the FS but what was estimated in the PEA, which would substantially improve the overall return of the project.

The Feasibility Study Only Includes Reserves

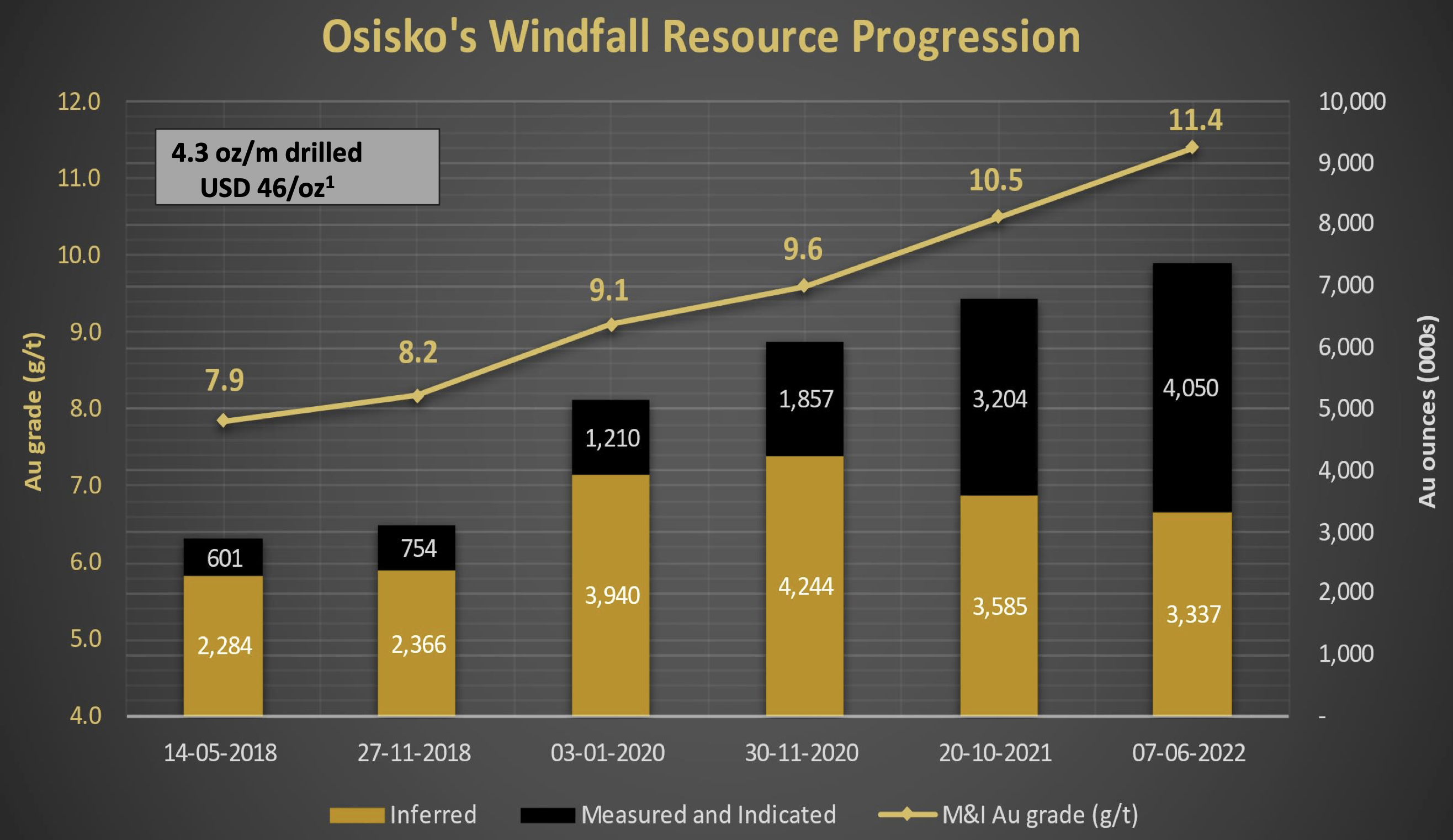

Let's start with the total resource base and its progression over the last four years.

Since 2018, Windfall's gold resource has increased from 2.9 million to 7.4 million ounces. At the same time, the grade has risen sharply to 11.4 g/t. It's unusual to see both ounces and grade climb by this degree. It's reminiscent of Alamos Gold's (AGI) Island Gold mine in Canada. There were "only" 6.1 million ounces of gold resources at Windfall when the PEA was released and at a much lower overall grade compared to today. So why is the FS worse? It all comes down to what type of resources/reserves can be included in an FS vs. a PEA.

{kind=link}

A Preliminary Economic Assessment is an early-stage study that can include Inferred resources, and Osisko's 2021 PEA was based on a substantial amount of Inferred ounces. An FS is based on reserves, and only 3.2 million ounces of reserves have been proven up at Windfall since the last mineral resource estimate (or MRE). However, there are 3.3 million ounces of Inferred gold resources at Windfall at a grade of 8.4 g/t. In other words, if you include about half of the Inferred material, the total production in the FS would be even higher than what was contemplated in the PEA. The NPV might not exceed that of the PEA - as the higher CapEx and OpEx would offset some of this additional value - but it would be similar to that of the previous study. Conservatively, there is another US$1 billion of NPV if you include ~50% of the Inferred resources.

Additional Potential At Depth

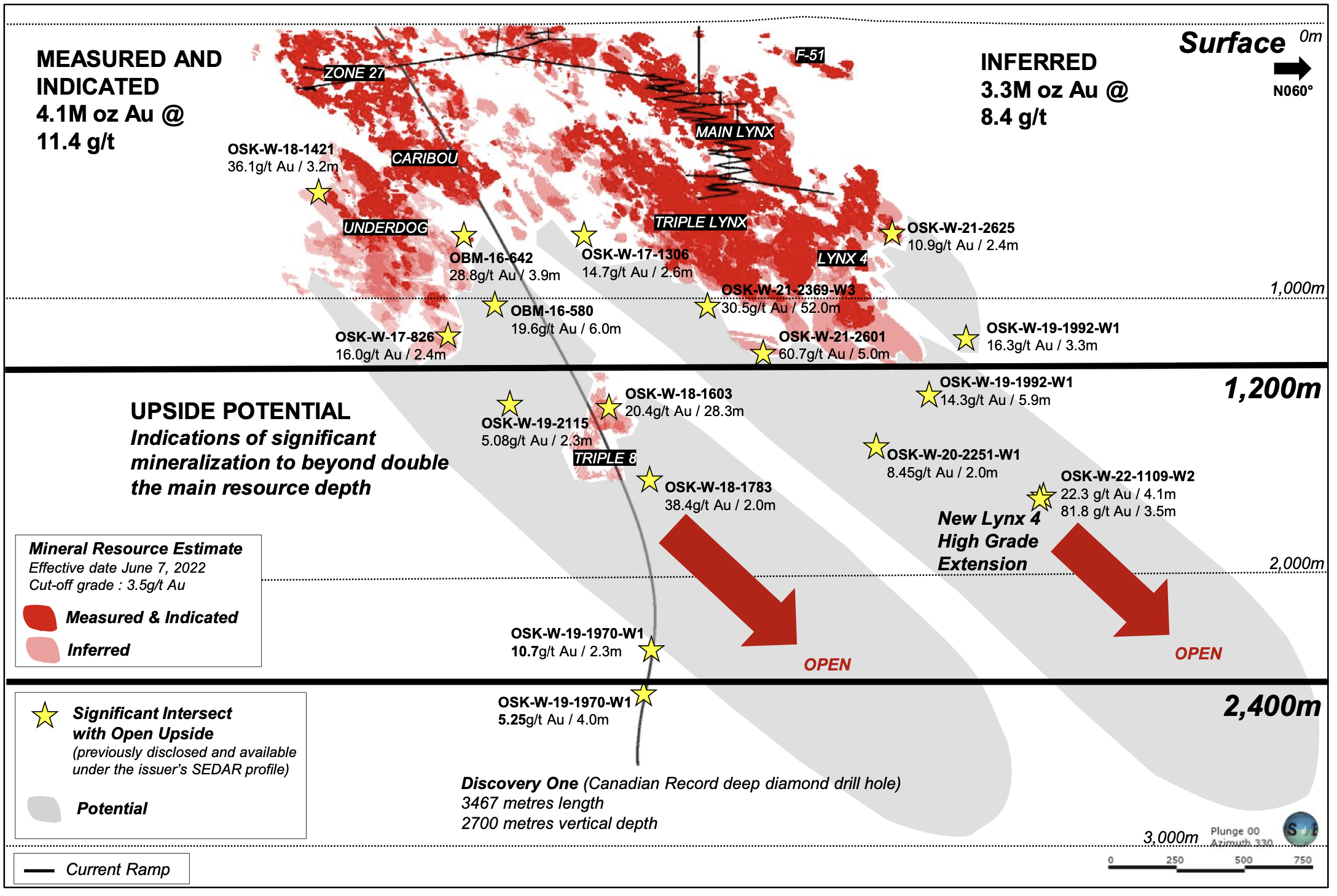

Let's now take a closer look at the Windfall deposit.

I've established that the current resources that aren't included in the Feasibility are enough to result in a mega boost in the NPV of the project. But that's just the proverbial "tip of the iceberg." The resource base will likely expand significantly over the next decade, as the vast majority of the currently defined resource is from surface to the 1,200-meter level. Yet, Osisko is hitting high-grade gold over minable widths down to 2,400 meters. The large mineralized zone on the right is called Lynx, and the grade gets even better down plunge, with ultra-high grade intercepts. The entire system is open at depth and has the potential to double in size. Osisko and Gold Fields will be focused on development and getting the mine into production in the short term, but both companies see the tremendous near-mine potential at greater depths.

{kind=link}

Low Hanging Fruit = Even More Potential Upside

Zero Value For Inferred Ounces Mined

I do want to note that the FS mine plan includes 1.3 million tonnes of inferred mineral resources, as they are located within mineral reserve blocks. However, these resources were assigned a zero-grade value, which means these ounces aren't included in the economics of the FS even though they technically exist and will be mined. Osisko believes more drilling could convert this Inferred material to 160,000 - 250,000 ounces of gold at a grade that is similar to the reserve grade.

As Osisko states :

We added some inferred material in there that we're obliged to mine through as part of the development. We counted it as zero. We know it's not zero. It's actually about the same resource reserve grade, subject to more drilling before we can add it to the M&I categories.

If these ounces are included, it will add another ~20,000 ounces of gold production per year.

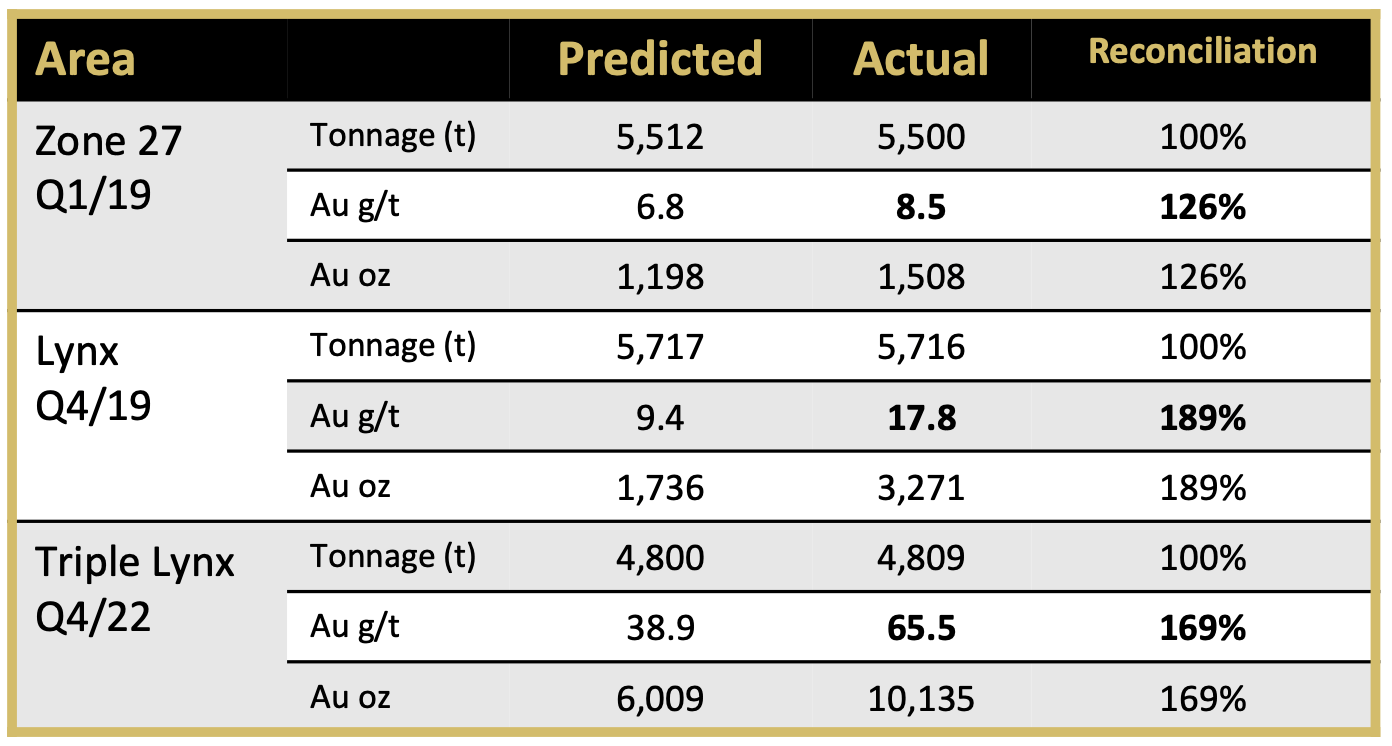

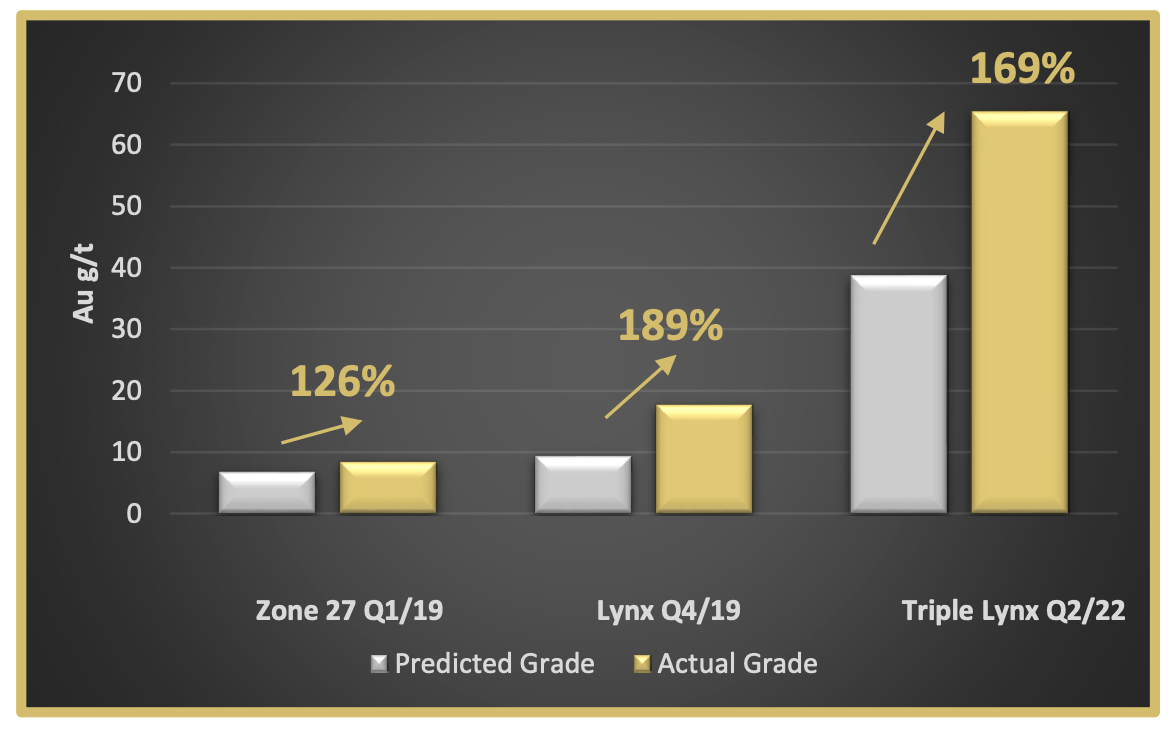

Bulk Samples Show Positive Grade Reconciliation

The project has been thoroughly de-risked now that it's at the FS stage, and the bulk sample work over the last few years has de-risked it even further.

If you notice in the map above, there are currently a few ramps at Windfall, with the one at Lynx extending down to 635 meters. Osisko has taken bulk samples from two zones at Lynx and another from the main zone. Results show significant positive grade reconciliation for all of these bulk samples. For example, in the 2022 bulk sample, the predicted grade and amount of gold contained were 38.9 g/t and 6,009 ounces, respectively. The actual grade was 65.5 g/t (169% positive grade reconciliation), and the sample contained 10,135 ounces of gold. The two other bulk samples were done on lower-grade sections and also saw substantial positive grade reconciliation.

In other words, the current resource base may be underestimating the number of ounces, at least in some of the zones. Either way, these results increase confidence that the overall grade will, at minimum, hold up throughout the mine life. Still, when it comes to grade reconciliation, nothing is 100% certain until you start mining.

{kind=link}

{kind=link}

Osisko estimates that every 1 gram of additional grade mined would add another 35,000 ounces of gold production annually.

When you combine the inferred ounces mined but not included in the FS and the potential positive grade reconciliation, Windfall is getting near 400,000 ounces of production annually. That's just the low-hanging fruit.

What Gold Fields Said About The Upside Potential Of Windfall

Gold Fields stated the following in its press release announcing the deal (emphasis added):

Having carried out extensive due diligence, management interaction and site visits for just over a year, Gold Fields believes the Windfall Project is on track to become a high-quality, low-cost underground gold mine with a relatively small surface footprint and considerable growth prospects along strike and down plunge, well beyond delineated Mineral Reserves and the current 10 year projected mine life set out in Osisko's December 2022 Windfall Feasibility Study.

Gold Fields believes the projected 10-year LOM (based only on stated Mineral Reserves in the Windfall Feasibility Study) to be conservative. The average projected all-in-sustaining-cost (AISC), as per the Feasibility Study, of US$758/oz (C$985/oz) is expected to position Windfall as one of the lowest cost mines in our portfolio, thus enhancing the average asset quality of the Gold Fields portfolio. Further, a producing mine in Canada enhances the jurisdictional quality of our global footprint.

The life extension upside, both within the Windfall mine footprint through resource conversion and expected onsite exploration success, together with significant regional exploration potential on the Exploration Properties is anticipated to provide a range of additional opportunities to Gold Fields' pipeline. None of these upside opportunities form part of the Windfall Feasibility Study.

While investors might have been disappointed with the price GFI paid for its 50% stake in the joint venture, it's unrealistic to expect a JV partner to pay 1x NAV (or more than that if pricing in upside to the LOM). GFI is taking risks, and there has to be some incentive and benefit for the company.

I think this is a fantastic transaction for Osisko, and it solidifies Windfall as one of the best projects in development.

CapEx Deflation And Other Cost Reductions?

When Osisko released the Feasibility late last year, inflation was at its peak, and half of the elevated pricing was supply chain related as quotes were coming in high due to supply/demand imbalances. But the pressure has come down greatly since then.

In the conference call discussing the joint venture, the company stated that it's seeing some reduction in the C$789 million construction costs. Quote:

We have seen some cost reduction in the past three to four months as we move through detailed engineering. We're currently about 30% to 40% through the detailed engineering. We're looking for like $720 million Canadian as capex costs. That includes about $50 million Canadian of contingency.

The company is also working closely with Gold Fields' team and finding ways to improve the mine and plant design, which could result in additional CapEx savings.

As for the US$758 AISC, Osisko mentioned that adding those inferred ounces that were excluded and counted as zero, plus if it's correct about the additional grade coming in, they expect AISC to "drop below $700."

A Conservative Valuation Analysis

As mentioned earlier, the NPV of Osisko's 50% JV stake in Windfall at current gold prices and exchange rates is ~US$650 million, or US$658 million, to be more precise.

That doesn't include any additional ounces from inferred resources that will be mined and processed or positive grade reconciliation. I would rather be conservative and assume no benefit from either over the life of mine.

I'm also assuming no reduction in CapEx and OpEx, even though Osisko believes those will come in lower than budget.

While the company had US$32 million of net cash at the end of last quarter, that's because of the change in fair value of the C$154 million convertible debenture. I'm being conservative again and putting net cash at zero, assuming cash fully offsets the current debt, which gives Osisko ~US$475 million of pro forma net cash.

As a side note, whether the debt converts into shares or Osisko repays the debt will have the same overall impact; I'm just choosing debt repayment (given the cash windfall) and have factored that into my calculations.

Another note, and this one very important, is that the NPV already accounts for the construction cost of the project, so the cash received from GFI should be added to the NPV, not subtracted, as subtracting is double counting construction CapEx. This is a mistake some are making in their valuation analysis, which results in severely underestimating the company's NAV.

The only item we need to back out/subtract is Osisko's portion of pre-construction costs (US$93.75 million/C$125 million).

So, that's ~US$1.04 billion of net cash and assets vs. a market cap of ~US$925 million.

If we add five years of mine life at 300,000 ounces per year (or 1.5 million ounces of gold in total), that's an additional US$450-$500 million of after-tax NPV for Osisko at current gold prices, and it assumes additional development capital. This is realistic potential as it only requires converting about half of the existing Inferred resources into reserves or adding more resources/reserves down plunge.

In total, that's ~US$1.52 billion of value vs. a $925 million market cap.

If we count all of the warrants and options (including those that are out-of-the-money), it's ~$1.43 billion of value or $3.39 per share, which means Osisko is trading at 0.65x NAV on a fully diluted basis.

Many gold developers are trading at similar or even lower valuations, but Windfall is a special project in a terrific jurisdiction, Osisko's portion of CapEx is fully funded without taking on debt (a huge, huge advantage over other developers), and again, I was conservative on all aspects (i.e., assumed no positive grade reconciliation, no additional ounces from inferred resources that will be mined, and no reduction in CapEx or AISC).

If we use the updated assumptions from Osisko Mining, such as a $50 million savings on CapEx, a $50 per ounce decrease in the life of mine AISC, and potentially 50,000 ounces of additional production per year from the inferred ounces mined and positive grade reconciliation, that's another US$350-$400 million of after-tax NPV for Osisko's 50% stake, which would mean OBNNF is trading at just over 0.5x NAV and fair value would be $4.28 per share.

How I Expect OBNNF To Perform

There is lower risk in OBNNF between now and production, especially with the company fully funded. Permitting should be straightforward (which will take about 18 months), then about 12 months of construction.

The company and its partner will be busy with all aspects of development over the next few years, and that will be the main focus. As a result, I'm not expecting a considerable increase in reserves/resources unless there's another major discovery.

It also seems less likely now that somebody will come along and make a bid for OBNNF.

There aren't many bullish catalysts over the next ~12 months. Therefore, the short-term outlook for the stock is more difficult to predict.

With all of the positives discussed above, and considering the recent underperformance of OBNNF, there is now a greater chance that the shares will outperform the sector over the near term. But unless gold breaks out, I believe the shares will remain range bound for the foreseeable future, and I would consider them at the lower end of the range now. I'm not certain that Osisko has bottomed, especially given the bearish sentiment in the mining stocks.

If OBNNF falls further, it will be an opportunity to get more aggressive on the long side, but I'm watching the short-term uptrend support line at around $2.20, which is also the recent low. If that breaks, the technicals will turn bearish. In that scenario, I plan to either wait for another 10-20% drop before buying more or for the stock to rebound above support.

StockCharts.com

To summarize, I'm not expecting fireworks in OBBNF in the short term unless gold breaks out, but there is still the potential for outperformance. As shown in this article, there's enough value that buying at current levels could be considered prudent when using a longer-term time horizon.

If gold breaks out in the next 6-12 months, then OBNNF will be one of the best options for those looking for leverage and exposure to the sector. OBNNF could see new all-time highs with gold solidly above $2,000. This is one stock I will be very long if/when gold hits new highs.

Over the medium to long term, once Windfall is close to completion or in production, I expect Osisko Mining Inc. will trade close to its fair value or maybe even at a premium to its NAV. It won't need help from gold at that point to generate strong shareholder returns.

For further details see:

Osisko Mining Receives A Windfall