CA - Osisko Mining: Valuation Starting To Improve

2023-12-18 11:51:45 ET

Summary

- Osisko Mining has underperformed its peers recently despite de-risking Windfall, and is now barely two years from first pour assuming successful receipt of permits in Q4/24.

- Meanwhile, it has made significant development progress on the Windfall Project and Lynx continues to churn out world-class intercepts, including 8.0 meters at 413 G/T of gold.

- In this update we'll dig into the updated valuation following the drop, recent developments, and whether the stock is approaching a low-risk buy zone.

Just over six months ago, I wrote on Osisko Mining ( OTCPK:OBNNF ), noting that there was limited margin of safety in the stock at US$3.15 with the stock trading at a ~$1.4 billion fully diluted market cap which left it trading at a premium to P/NPV with it still at least three years away from commercial production. Since then, Osisko has underperformed its peer group and corrected by 40%, and we've seen multiple developments including a ~$225 million cash injection from Gold Fields ( GFI ) with more to come, Osisko Gold Royalties ( OR ) selling its stake last week, wildfires that slowed summer drilling plans, and an update with multiple world-class intercepts that continue to suggest Windfall is likely to enjoy positive grade reconciliation vs. its estimated fully diluted head grade of 8.1 grams per tonne of gold.

In this update we'll dig into the updated valuation following the drop, recent developments, and whether the stock is approaching a low-risk buy zone.

{kind=link}

Windfall Project - Company Website

Recent Developments

Aside from major news which included a partnership on Windfall between Gold Fields and Osisko Mining ("Windfall Partnership"), it's been a busy year for Osisko and the joint-venture partnership. This has included the submission of the EIA in late March with permits expected to be granted by Q4 2024, a definitive agreement with Miyuukaa (wholly-owned corporation of the Cree First Nation) for the ~85 kilometer powerline to provide hydroelectric power to the Windfall Project (powerline over 50% complete), and continued progress developing the asset for an a potential first gold pour by Q1 2026 (estimated 12-month construction period added onto estimated receipt of permits by late 2024). As the image below shows, the Windfall Project already has over 13 kilometers of underground development completed, so it has made significant development progress even if permits are not in hand yet.

"I think in terms of the partnership with Osisko Mining to develop the project in Windfall, the EIA was submitted in March. We expect that to come to fruition towards the back end of next year or very early 2025. In that period, we're going to continue with pre-construction activities."

- Gold Fields, Q3 2023 Conference Call

{kind=link}

Powerline to Windfall Camp, Underground Development - Osisko Website

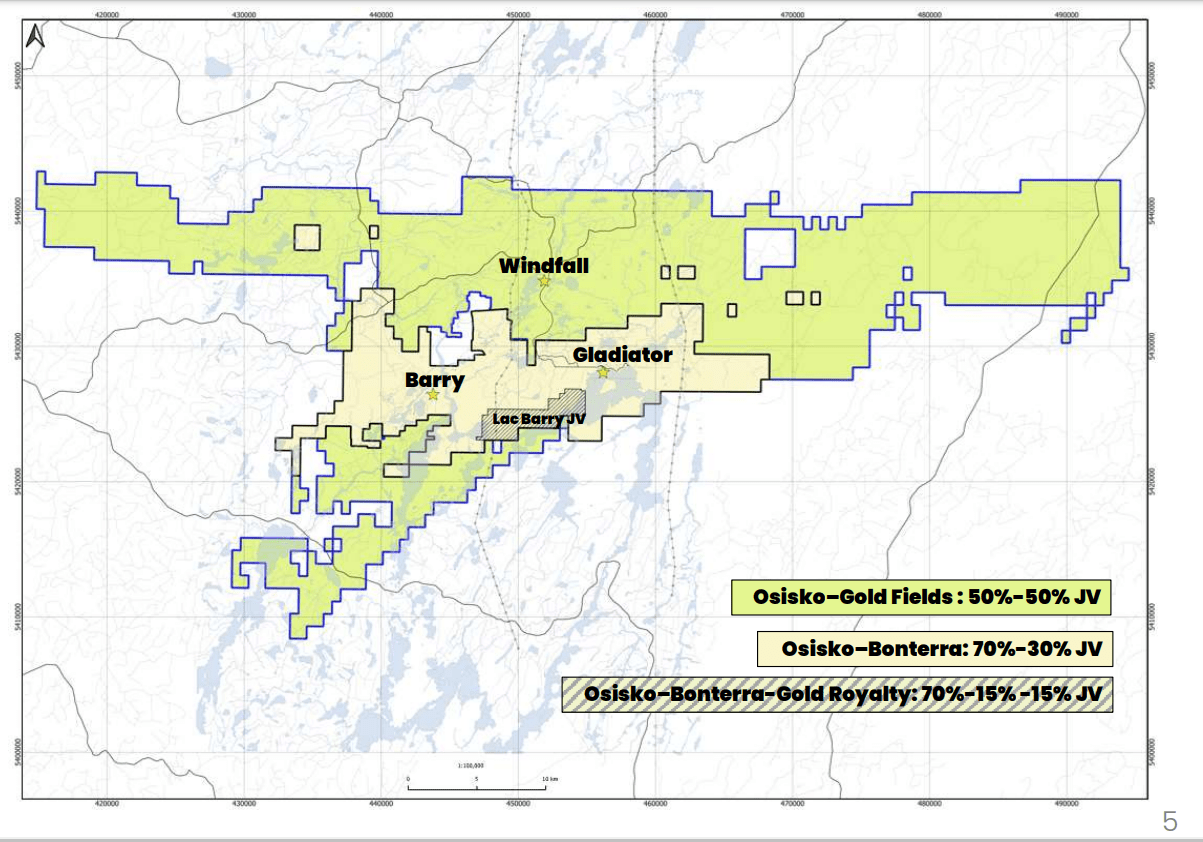

As for other smaller developments, Osisko announced a non-binding agreement with Bonterra ( OTCQX:BONXF ) for a 70% exploration earn-in and joint-venture on its massive land package in the Eeyou Istchee James Bay region of Quebec. These properties total over 22,000 hectares, and Osisko will pay ~$4.0 million in cash and will have the opportunity to earn a 70% undivided interest in the properties if it spends ~$22.5 million over a three-year period. This gives Osisko a very inexpensive option to potentially significant grow its resource base south of its already massive Windfall Project that's home to ~7.4 million ounces or ~3.7 million ounces on an attributable basis.

{kind=link}

Osisko-Bonterra Joint-Venture + Osisko/Gold Fields Joint-Venture - Bonterra Presentation

Moving over to work and plans with the Windfall Partnership, the planned budget from October 2023 to December 2024 will be ~$19 million per month (48% property, plant, and equipment and 52% exploration on a 50/50 basis through monthly cash calls focused on underground definition drilling (primarily Lynx, Triple Lynx, Lynx 4), and regional exploration. As for development progress to date, two vent raises have been completed in the high-grade Lynx Zone, and the company has begun construction on a new pumping station of the 460-meter level, with completion by year-end, as well as a new water treatment plant. Finally, a permit has been received for what will be the fourth bulk sample since Osisko scooped up the project, and the results of the Lynx 4 bulk sample should be interesting given the 70%+ average positive grade reconciliation in past bulk samples.

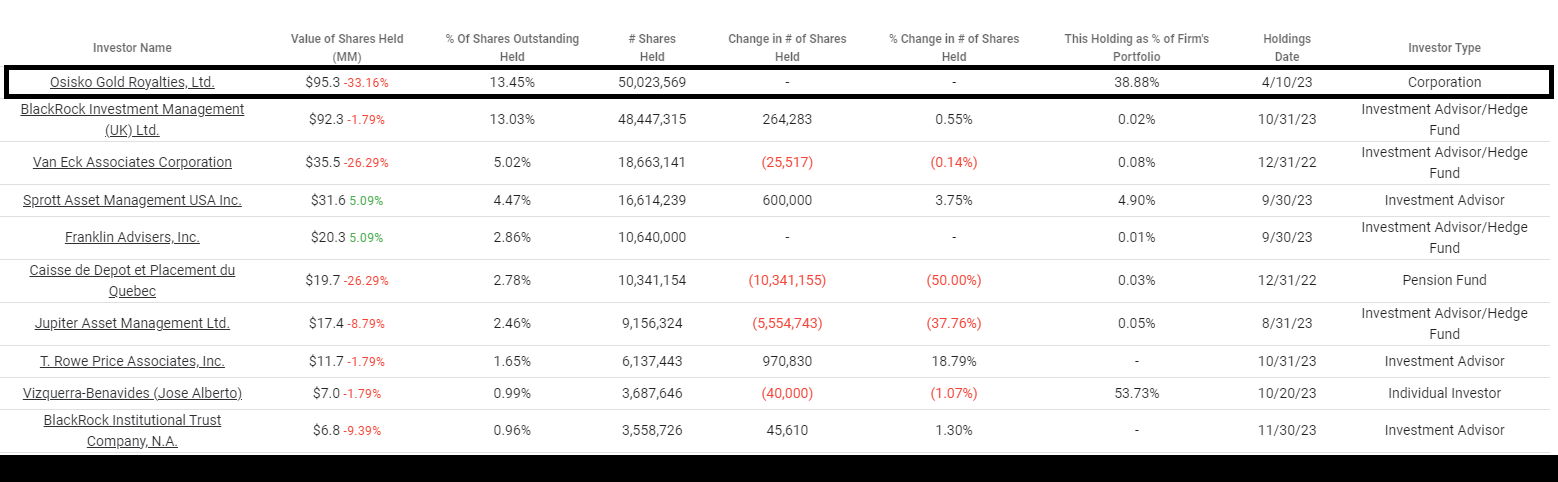

Finally, as for updates in share ownership, Osisko has continued to repurchase shares at prices ranging from ~US$1.90 to ~US$2.86 over the past year, and while buybacks make sense, it would be preferable to see these executed more opportunistically vs. near the highs in May at US$2.50 - US$2.86. Meanwhile, we saw Osisko Gold Royalties exit its position with ~50.0 million shares sold for proceeds of $99 million. This has little to do with Osisko's view on the value of Windfall and Osisko Mining shares, and more to do with it making more sense to potentially use proceeds to pay down debt (guaranteed returns from an interest expense standpoint) vs. speculating on the value of Osisko Mining shares. Plus, the company already has ample exposure with a 2-3% NSR on the project. Overall, I see this as a positive development with it taking the overhang off the stock, with this being a potential worry previously given the size of this position.

{kind=link}

Osisko Mining Shareholders - TIKR.com

Drilling Highlights

As for drilling highlights, it's been a quieter year given the prohibitions related to forest access on Crown lands and closed forestry roads in early June announced by Quebec's Ministry of Natural Resource and Forests related to wildfires. However, these access restrictions were removed in late July and the Windfall Partner has still managed to drill ~95,000 meters focused on the Lynx deposit with a goal of upgrading inferred resources to measured and indicated resources. In addition, regional exploration restarted in August on the Osborne-Bell Project (inferred resource of ~510,000 ounces of gold at 6.13 grams per tonne of gold), and drilling outside of Windfall Main in the Urban-Barry volcanic belt will take place from Q4 2023 through 2024 with 25,000 meters planned.

Some highlight intercepts from this year's drill program at Windfall include:

- 8.0 meters at 413 grams per tonne of gold

- 7.0 meters at 124 grams per tonne of gold

- 3.5 meters at 444 grams per tonne of gold

- 3.1 meters at 171 grams per tonne of gold

- 3.0 meters at 283 grams per tonne of gold

- 2.8 meters at 322 grams per tonne of gold

- 2.7 meters at 692 grams per tonne of gold

- 2.4 meters at 498 grams per tonne of gold

- 2.2 meters at 224 grams per tonne of gold

- 2.0 meters at 305 grams per tonne of gold

Although these hits may not measure up to some of the best drill results from Kirkland Lake Gold at Fosterville in 2017/2018, with highlight intercepts like 16 meters at 404 grams per tonne of gold, 7.4 meters at 976 grams per tonne of gold, 6.4 meters at 933 grams per tonne of gold, and 6.8 meters at 416 grams per tonne of gold, Osisko's drill results are consistently world-class, and among the best drilled sector-wide over the past several years. To date, Osisko's results at Windfall easily stand up next to other high-grade deposits like Fourmile (25.6 meters at 83 grams per tonne of gold), Brucejack (1.0 meter of 7,360 grams per tonne of gold), Macassa (14.5 meters at 254 grams per tonne of gold), and Hod Maden (85 meters at 84 grams per tonne of gold and ~6% copper).

{kind=link}

Fosterville Mineralization & Swan Zone - Kirkland Lake Gold

Plus, Osisko continues to hold the top intercept with 2 meters at ~13,600 grams per tonne of gold, and is unique among the list of top gram-meter intercepts since 2017 as it's the one deposit not majority owned by a major producer like Fosterville, Macassa, Brucejack, and Fourmile (Cortez Complex). Given the consistent number of drill results above 20 grams per tonne of gold and several 100+ gram per tonne gold intercepts, I would argue that there's certainly a high probability of positive grade reconciliation.

Even assuming what I would consider at a conservative average 0.3 grams per tonne of gold positive grade reconciliation and the planned ~3,400 tonne per day processing would result in an extra ~5,500 ounces of attributable gold per annum (50% Osisko ownership), suggesting the possibility of a bonus ~1,400 ounces per quarter in some quarters once Windfall is in production, and potentially lumpier bonus ounces in some high-grade pockets of this future mine. And in the case that Windfall significantly outperforms and can average 1.0 gram per tonne (with three bulk samples completed certainly surprising to the upside to date), bonus ounces attributable to Osisko per annum would be ~18,600 ounces or an additional ~$36 million in revenue.

{kind=link}

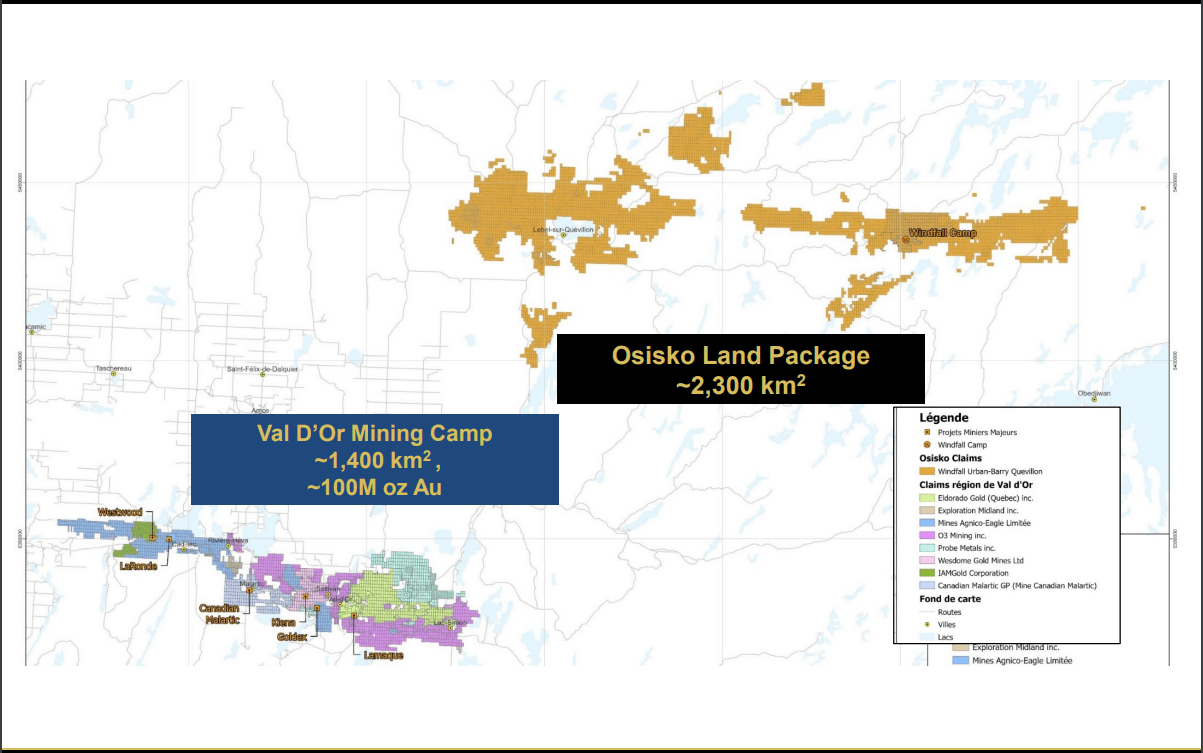

Osisko Land Package - Company Presentation

As for upcoming catalysts, future drill results from the regional program are certainly something to look forward to, with the Windfall Partnership's land package dwarfing that of the highly productive Val D'Or Camp. The Val D'or Camp which includes Canadian Malartic (~15 million ounces of gold produced) and LaRonde (~11 million ounces of gold produced), with these two mines producing nearly 30 million ounces combined, and Canadian Malartic still has a 12+ million ounce resource base and growing with the addition of Odyssey Underground. So, while there's no guarantee that Osisko's total resources grow, it certainly has probabilities on its side of making a second discovery given the size of its land package, and is still has upside at depth below 1,200 meters at Windfall, and to the north with the Golden Bear discovery. The bonus is that Gold Fields will sole fund regional exploration up to a maximum of $56 million, with expenditures shared thereafter.

Let's look at Osisko's valuation and see how the stock stacks up relative to peers.

Valuation

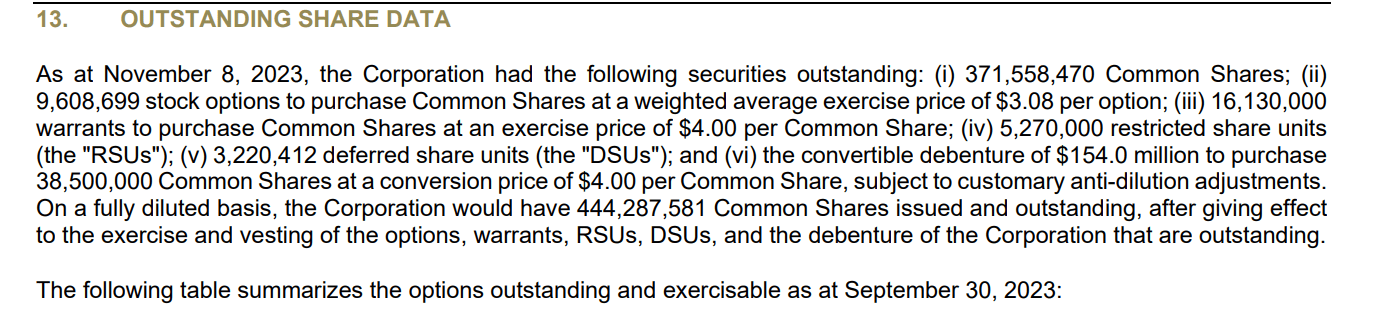

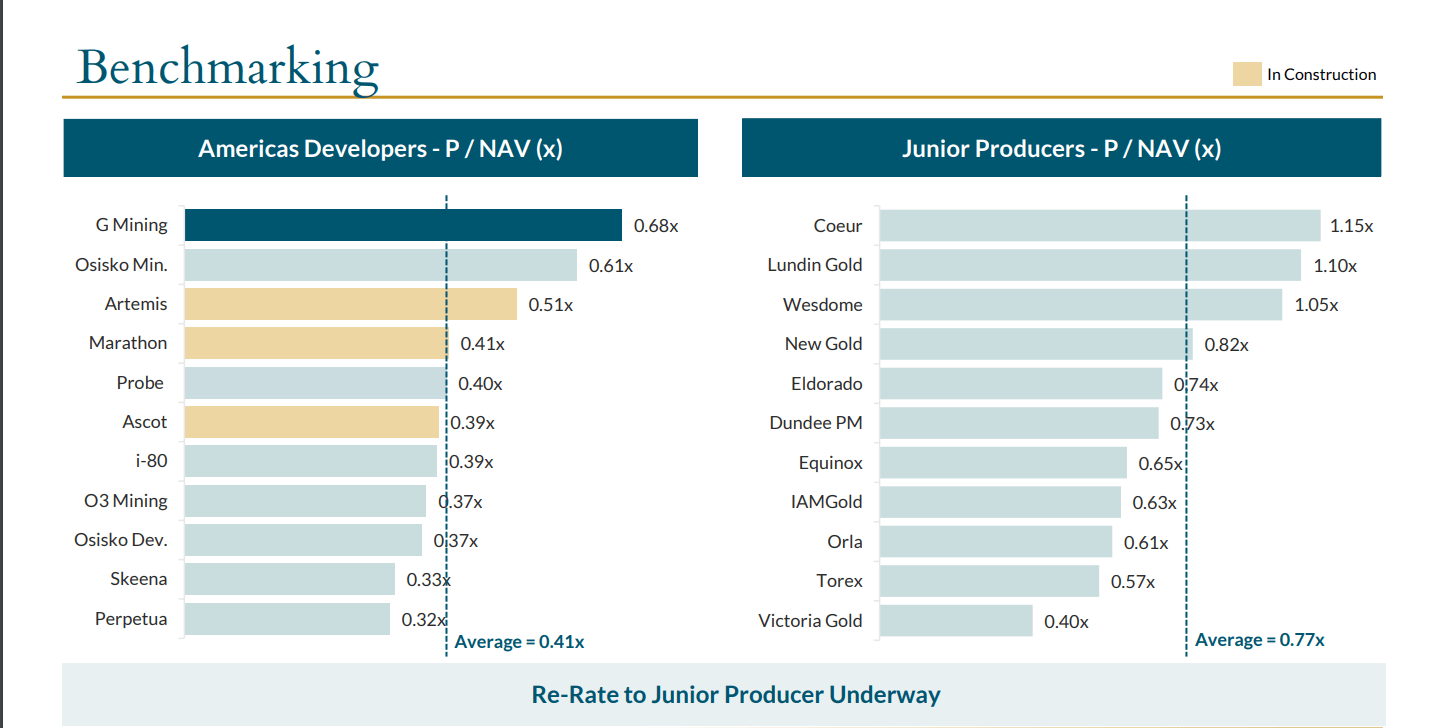

Based on ~430 million fully diluted shares (excludes out of the money warrants at US$3.00) and a share price of US$1.90, Osisko trades at a market cap of ~$820 million and an enterprise value of $540 million based on its ~$280 million cash position. Notably, the current enterprise value does not include an additional ~$235 million owed to Osisko on the receipt of permits and a final separate cash payment of $17 million due at year-end to reimburse Osisko for capital spent on pre-construction activities. And even if we account for additional drilling and pre-construction expenses, this enterprise value leaves Osisko trading at a fraction of its estimated attributable NPV (6%) at Windfall of ~$1.04 billion, which might make it look like the cheapest advanced developer in Canada today on an enterprise value per ounce and P/NAV standpoint.

{kind=link}

Osisko Shares Outstanding/Diluted - Company Filings

However, it's important to note that upfront capex for Windfall is expected to come in at ~$600 million based on 2022 estimates, and given the mid-single-digit inflation experienced this year (with labor inflation remaining high in prolific mining jurisdictions), a more conservative assumption for upfront capital would be $660 million or $330 million attributable to Osisko Mining. Therefore, I would expect most of Osisko's ~$500 million cash balance (current cash/cash equivalents [+] receivables to be depleted when combined with its continued share buybacks, recent investments, corporate G&A and continued drilling and development costs. For this reason, I think valuing the company on a market cap basis is more appropriate given that cash flow at Windfall can't be realized without considerable upfront expenditures.

{kind=link}

P/NAV Multiples (Developers & Junior Producers) - FactSet & Company Filings, G Mining Ventures Presentation

So, what's a fair value for the stock?

Based on an estimated attributable NPV (6%) of ~$1.04 billion for its share of Windfall and what I believe to be a fair multiple of 1.1x for an asset of this quality, the fair value on an upside case mine plan is at ~$1,144 million [US$2.66]. To this figure, I think it's fair to add $200 million in attributable exploration upside, and a $100 million in cash once construction is complete [US$0.70]. If we then subtract out an estimated $160 million in corporate G&A over the mine life, this translates to a fair value for Osisko of ~$1,284 million [US$2.99]. And if we measure from a current share price of US$1.90, this translates to a 57% upside from current levels.

The Windfall Project's estimated NPV (6%) of ~$2.08 billion on a 100% basis or what I see as the "upside case" vs. the base case presented in October 2022 includes some positive grade reconciliation, a longer mine life based on successful resource conversion, and a slight increase in throughput above planned 3,400 tonne per day levels post-2030.

Although this represents a significant upside from current levels for a company offering exposure to a massive unexplored gold camp and 50% of one of the highest-grade undeveloped projects globally, I am looking for a 45% to 50% discount to fair value to justify starting new positions in developers to justify their higher-risk vs. diversified producers that are already generating consistent cash flow. And even if we use the lower end of this minimum discount range (45%) to ensure a margin of safety, Osisko's ideal buy zone comes in at US$1.65 or lower, with the stock still outside of its low-risk buy zone. Obviously, waiting for lower prices could be an opportunity cost, and Osisko may bottom out here. Still, I continue to see more attractive bets elsewhere from a valuation standpoint.

{kind=link}

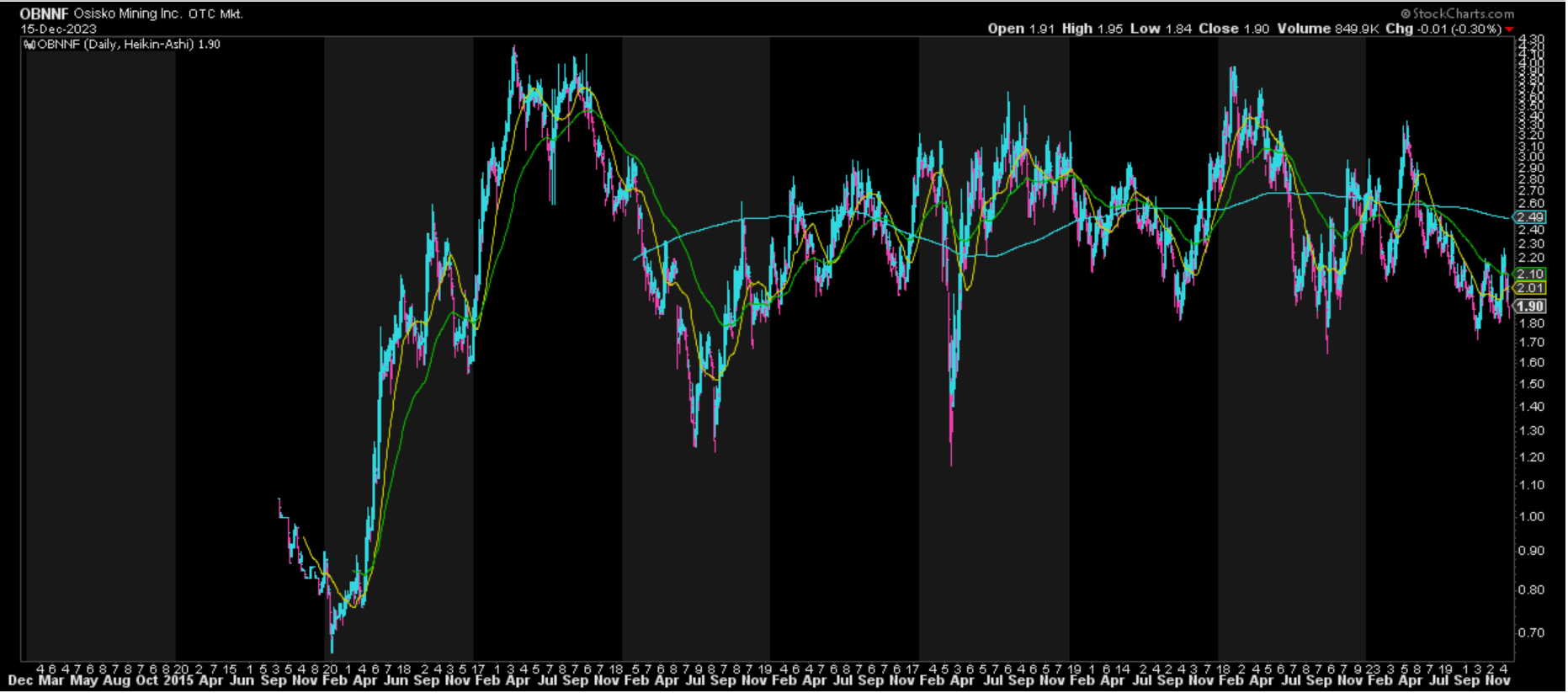

Osisko Mining Long-Term Chart - StockCharts.com

One name that stands out with a more attractive reward/risk is K92 Mining ( OTCQX:KNTNF ), with it trading at just ~3x FY2026 EV/FCF and a similar market cap today with a mine that has roughly triple the production profile (~470,000 GEOs), and similar projected all-in sustaining costs of $750/oz. However, K92 Mining has 100% of the asset vs. 50% for Osisko at Windfall, less risk of a capex overrun as this is a brownfields expansion (94% of K92 Mining's Stage 3 plant capex has been fixed, and the twin incline to increase mining rates is over 95% complete), and it's already fully permitted and a producer today. Hence, despite similar market caps, K92 Mining will have triple the production profile post-2026 (460,000+ GEOs) and at similar margins vs. Osisko at 150,000 to 160,000 ounces based on its 50% ownership at Windfall, and K92 will generate significantly more free cash flow in 2027 (~$370 million vs. ~$140 million).

Summary

Osisko Mining has succeeded in de-risking Windfall by bringing in a partner to put a halt to continued share dilution, and the company's mine plan looks conservative given the level of drilling (well over 1.0 million meters), and multiple bulk samples completed to date with very positive grade reconciliation. In addition, the current reserve base represents less than half of total resources, and Windfall ultimately looks like it could be a 18+ year mine life even without the Golden Bear discovery to the north with resource conversion and upside at depth. Hence, if I were looking for a Tier-1 jurisdiction developer to increase gold exposure in my portfolio, I would view any pullbacks below US$1.65 on Osisko Mining as buying opportunities.

For further details see:

Osisko Mining: Valuation Starting To Improve