OTIS - Otis: The Better Elevator Stock As Confirmed By Strong H1 Results

Summary

- Otis stock has fallen by 20%+ in the past year after elevator companies have been hit by the slowdown in China and higher input costs.

- Otis has lower exposure to China than main rival Kone and is still expecting to grow its EPS by 4-7% this year despite FX headwinds.

- Otis' all-important Maintenance revenues are growing at mid single digits and accelerating, and it is gaining share in New Equipment.

- We believe Otis will achieve an EPS CAGR of just under 10% in 2021-25, while the stock is too cheap at 23x guided 2022 EPS.

- With shares at $72.72, we expect an exit price of $127 and a total return of 81% (19.9% annualized) by 2025 year-end. Buy.

Introduction

We review our Otis Worldwide Corporation ( OTIS ) investment case after shares have fallen by more than 20% since peaking almost exactly a year ago:

| Librarian Capital Otis Rating History vs. Share Price (Last 1 Year) Source: Seeking Alpha (01-Sep-21). |

{kind=link}

We initiated our Buy rating on Otis in July 2020 . While shares have gained 32% (including dividends) in the two years since, more than two thirds of this gain occurred in 2020, and their recent weakness present an opportunity.

The elevator sector has good structural dynamics but has recently been impacted by the slowdown in Chinese construction and rising input costs. Otis is our preferred elevator stock, thanks to its lower exposure to China and better operational performance. Its all-important Maintenance revenues are growing at mid single digits and accelerating, Modernization demand is rising and Otis is gaining share in New Equipment. Management targets a 10%+ EPS CAGR in the medium term and, despite current headwinds, expects positive EPS growth in 2022. Otis shares are too cheap at 23x 2022 EPS, and our updated forecasts indicate a total return of 81% (19.9% annualized) by 2025 year-end. Buy.

Otis Buy Case Recap

Otis is the largest player by sales in the global elevator and escalator industry. We believe Otis and its peers to be high-quality businesses, thanks to the structural growth in demand from urbanization and connected services, recurring Maintenance and Modernization services (which generate most of the profits, except in China), a highly consolidated competitive landscape, and a capital-light manufacturing model that sources components from a network of suppliers.

Otis is different from its main competitor Kone ( KNYJF ) (also Buy-rated and reviewed recently) in important ways:

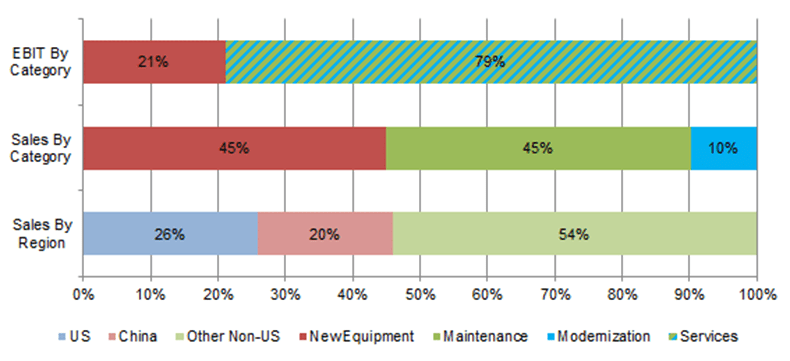

- Much lower exposure to China (20% of 2021 Net Sales, vs. Kone's 35%)

- Lower exposure to New Equipment (45% vs. 53%)

- More explicit EBIT margin expansion targets

- Ongoing program to lower its effective tax rate

- More optimized capital structure, with net debt and buybacks

{kind=link}

These differences, especially the lower exposure to the slowing Chinese construction market, mean Otis now has much better medium-term earnings growth potential than Kone.

10%+ Medium EPS CAGR Target

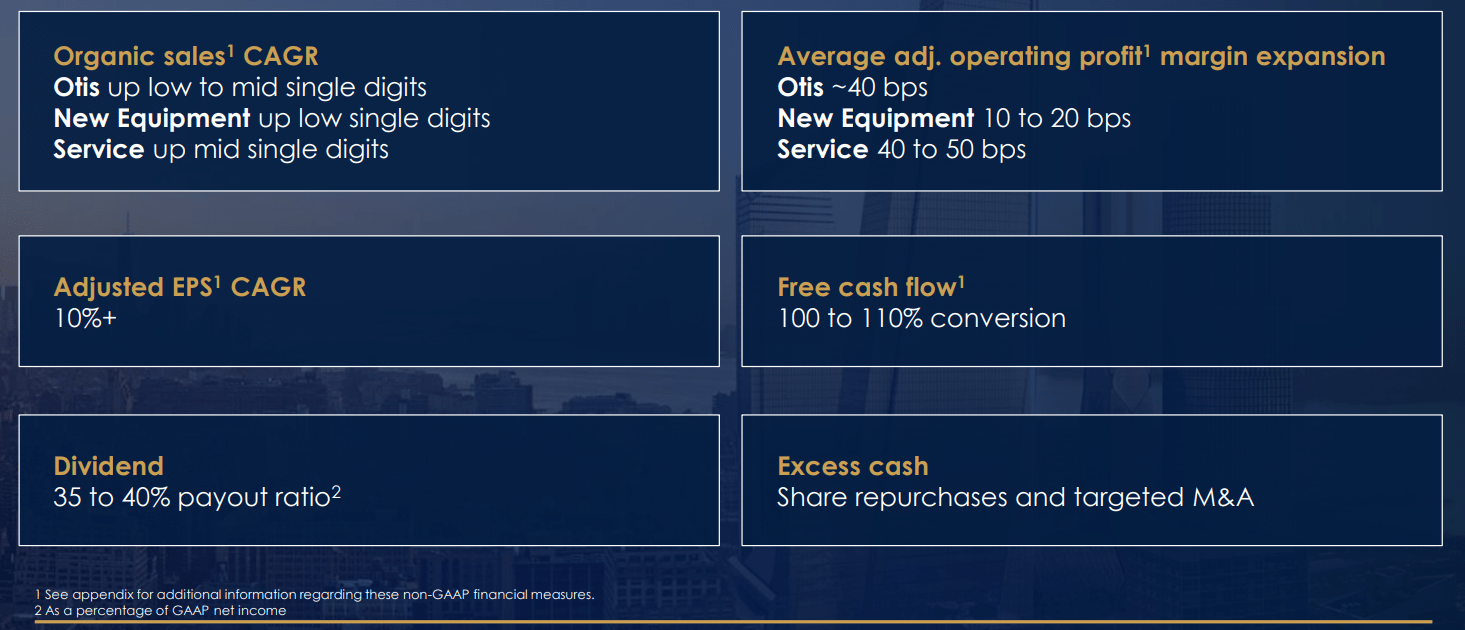

Otis has set out new, more ambitious medium targets at its investor day in February, including a 10%+ EPS CAGR:

{kind=link}

The 10%+ EPS CAGR is expected to be generated by an organic sales CAGR in the low-to-mid single-digits and an average Adjusted EBIT margin expansion of 40 bps annually. Service is expected to be the main profit driver, with an organic sales CAGR in mid single digits and an annual margin expansion of 40-50 bps; New Equipment is expected to only grow sales at low-single-digits and expand its margin at 10-20 bps annually. Management also expects to reduce Otis' effective tax rate from 28.5% in 2021 to 25.0-27.0% in the medium term. In addition, Otis aims to return most of the Free Cash Flow ("FCF") generated to shareholders in dividends and buybacks.

These targets are supported by Otis' recent track record and quarterly results during 2022.

Otis' Recent Growth Track Record

Otis has delivered a strong growth record since being spun out of United Technologies in an IPO in April 2020, despite volatility in parts of its revenues and disruption by COVID-19 since 2020:

| Otis Key Financials (2020-22E) Source: Otis company filings. |

Maintenance & Repair sales fell by a relatively small 0.9% organically in 2020 and quickly returned to mid single-digit growth, at 4.5% in 2021 and 5.2% in H1 2022, and guided to 5.5-6.0% for full-year 2022. A key driver of this growth is an ever-expanding install base, which grew by 2% in units in 2020, 3% in 2021 and 3.5% year-on-year as of Q2 2022; this has included a high-teens growth in China for the past 4 consecutive quarters.

Modernization sales similarly was resilient in 2020 with an organic growth of 0.1%, followed by 2.5% in 2021 and is expected to accelerate to 6.0-9.0% in 2022 (having already grown by 6.7% in H1). Modernization growth is helped by latent demand from an aging install base, which at Otis is already one third over 20 years old.

New Equipment ("NE") sales are more volatile, falling by 4.0% organically in 2020, rebounded by 15.5% in 2021 and was down 3.2% in H1 2022 (though expected to decline only 0.5-1.0% for the full year). However, outside China (which was 35% of Otis' NE sales), NE sales are low-margin and much of the sales decline in 2022 is believed to have be sales deferred (by, for example, labour shortages) rather than lost.

Adjusted EBIT Margin has continued to expand, from 15.0% in 2020 to 15.3% in 2021 and an expected 15.7% in 2022 (it was 15.8% in H1), despite rising input costs. As well as price increases, Otis has been able to offset rising input costs through cost savings and, while Cost of Sales margin has risen, this has been more than offset by a reduction in SG&A cost margin (while R&D cost margin has been kept roughly flat).

H1 2022 has been affected by currency headwinds and an exit from Russia after the invasion of Ukraine, offset by a small benefit from buying out minority shareholders Otis Zardoya, formerly Otis' listed subsidiary in Spain. H1 2022 sales grew 1.6% year-on-year organically but fell 2.4% including currency and Zardoya (or 2.9% if also including Russia); Adjusted EBIT grew 4.6% organically but fell 0.6% including currency and Zardoya (or 2.4% if also including Russia).

Otis H1 2022 Results Headlines

Otis EPS grew 10.4% in USD year-on-year in H1, despite the 0.6% decline in Adjusted EBIT once currency is included, showing the benefits from the reduction in Otis's tax rate, buybacks and the buy-out of Otis Zardoya:

| Otis Adjusted P&L (H1 2022 vs. Prior Year) Source: Otis results release (Q2 2022). NB. Contribution from Russia excluded from both periods. |

Pre-Tax Income fell by1.3% year-on-year in H1, more than EBIT, due to higher interest expense from additional debt from the Zardoya buyout. However, Income Tax Expense fell by 13.4%, as the effective tax rate fell from 28.5% to 24.9%, which meant Net Income actually rose 8.7%. With a 1.6% lower share count, Adjusted EPS rose 10.4%.

Overall, the $0.15 year-on-year EPS growth in H1 2022 consisted approximately of $0.08 from tax, $0.05 from operations, $0.03 from buybacks and $0.04 from the Zardoya buy-out, offset by $0.06 from currency - showing the multiple drivers behind Otis' expected EPS CAGR in the medium term.

Otis' H1 results were far better than that at Kone, which reported an organic sales decline of 8.5% (2.7% in EUR, where currency was a tailwind), an 35% decline in Adjusted EBIT and a 45% decline in Reported EPS.

The picture for Q2 2022, more affected by the slowdown in China and higher input costs than Q1, was similar. A 3.7% ($21m) Adjusted EBIT year-on-year decline, was due to $37m of currency headwind and led to an EPS growth of 11.9%:

| Otis Adjusted P&L (Q2 2022 vs. Prior Year) Source: Otis results release (Q2 2022). NB. Contribution from Russia excluded from both periods. |

The same drivers are expected to generate good EPS growth for Otis in the medium term, including in 2022.

Otis Full-Year 2022 Outlook

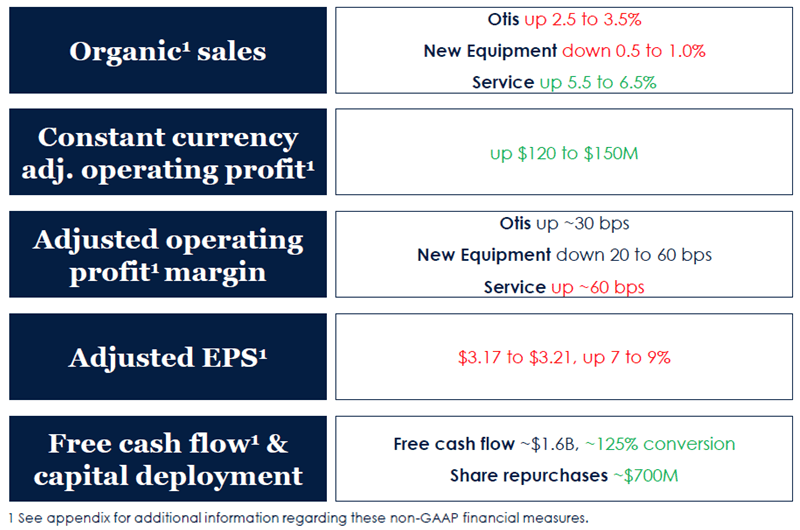

At constant currency and excluding Russia, Otis expects to deliver an Adjusted EPS growth of 7-9% in 2022:

{kind=link}

Including currency and Russia, Adjusted EPS is expected to grow by 4-7%. This is much lower than the 10.4% achieved for H1, largely due to Q1 having a weaker prior-year comparable and headwinds having started in Q2.

Current-neutral Adjusted EPS growth is expected to be driven by organic sales growth of 2.5-3.5% (primarily driven by Services) and Adjusted EBIT margin expansion of approximately 30 bps (also driven by Services).

The 0.5 to 1.0% organic decline in NE sales is expected to consist of flat sales in the Americas, growth of low-to-mid single-digits in EMEA, and a low-single-digit decline in Asia (primarily due to China). And this sales decline coincided with growth in orders and market share gains, which suggest it is just temporary.

Otis Order Growth & Market Share Gains

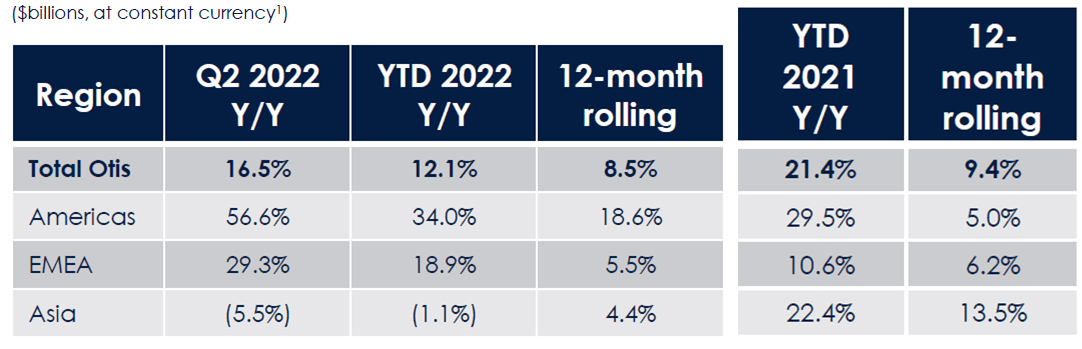

Otis NE orders have continued to grow. In H1 2022, they were up 12.1% year-on-year in constant currency, after an already strong prior-year period when they were up 21.4%:

{kind=link}

By region, NE orders were up 34.0% in the Americas and 18.9% in Europe in H1 2022; they were down 1.1% in Asia, primarily due to China, where they were up 3% in Q1 but down low-teens in Q2.

Pricing on NE orders were up low-single-digits globally, being up mid single digits outside China (helping to offset higher input costs) and down low-single-digits in China (where to input costs fell and the pricing decline was cost-neutral).

As of Q2 2022, Otis' NE backlog was up 5% year-on-year in constant currency.

Otis has also been gaining share in NE, especially in China. Globally, management estimated that Otis gained 1 ppt of share in NE orders n Q2, with its NE orders growing 16.5% globally when the market was down mid single digits. In China, Otis NE orders were down low-teens when the market was down 20%.

Otis' market share gain in China appeared to have come from a genuine improvement in its competitiveness, especially in distribution. While Otis benefited from Kone's COVID-related production disruption in Q2 (Otis' factories "never shut down" while Kone's Kunshan factory was shut entirely for several weeks in April), management stated that Otis has been gaining "for multiple quarters" even before the latest restrictions.

Otis' strong orders and share gains will help power medium-term growth, including in Service.

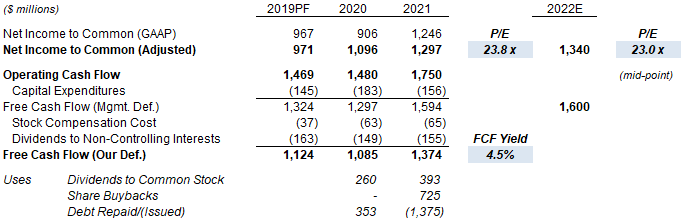

Valuation - Are Otis Shares Overvalued?

At $72.72, with respect to 2021, Otis shares are trading at a 23.8x P/E and a 4.5% FCF Yield; relative to the 2022 outlook, the P/E is 23.0x (at mid-point) and we believe the FCF Yield is likely to be close to 5%, as FCF (management definition) is expected to be similar but dividends to non-controlling interests should be much lower (they were 65% lower year-on-year in Q2) after the buyout of minority shareholders in Otis Zardoya:

{kind=link}

Otis pays a dividend of $0.29 per share (raised 21% in April), or $1.16 annualized, equivalent to a 1.6% Dividend Yield. Management targets a Payout Ratio of 35-40% (relative to GAAP Net Income, but this is similar to Adjusted).

Share buybacks have totaled $400m in H1 and are expected to reach $700m for the full year, the latter equivalent to 2.3% of the current market capitalization.

We expect buybacks to increase over time. Compared to $1.6bn of expected FCF in 2022, the dividend currently costs approximately $500m, bolt-on M&A is expected to cost $50-100m each year and some dividends are paid to minority interests ($8m in Q2 and $41m in H1). Otis also spent $500m to pay down debt in H1, but Net Debt / EBITDA is down to 2.3x LTM EBITDA, and expected to be "just over 2x" at year-end, where 2x has been described by management as "a good number" at the investor day in February, implying no further paydowns are expected after this year.

Otis Stock Forecasts

We have updated our forecasts and extend them by a year to 2025. Our assumptions now include:

- 2022 Net Income of $1,341m (was $1,364m)

- 2022 EPS of $3.19 (was $3.17)

- 2023 Net Income growth of 10.5% (was 13.0%)

- From 2024, Net Income growth of 8.0% (unchanged)

- From 2023, share count to fall by 2.0% each year (unchanged)

- 2022 dividend of $1.16 (was $1.11)

- From 2022, dividends to be based on a Payout Ratio of 35% (unchanged)

- 2025 year-end P/E multiple of 29.0x (was 32.5x) (compared with 28.0x for Kone)

We are assuming a long-term Net Income growth was 8.0%. A long-term sales growth of 4% and margin expansion of 35 bps annually (from around 16%), slightly lower than management medium-term targets, would result in Adjusted EBIT growth of approximately 6.5% annually. We expect financial leverage and a reduction in Otis' tax rate to translate this to Adjusted Net Income growth of 8.0% annually. 2023 Net Income growth is expected to be 2.5 ppt higher, due to accretion from the Zardoya buyout and a slight reversal in the currency headwind experienced in 2022.

Our new 2024 EPS estimate of $3.96 is 2% lower than before ($4.03). The implied 2021-25 EPS CAGR from our forecasts is 9.8%, also slightly below management's medium-term target of 10%+:

| Otis Illustrative Return Forecasts Source: Librarian Capital estimates. |

With shares at $72.72, we expect an exit price of $127 and a total return of 81% (19.9% annualized) by 2025 year-end.

Is Otis Stock A Buy? Conclusion

We reiterate our Buy rating on Otis Worldwide Corporation stock.

For further details see:

Otis: The Better Elevator Stock, As Confirmed By Strong H1 Results