AEVA - Ouster Sets A Course Towards Profitability

2023-11-12 07:06:40 ET

Summary

- Ouster has delivered on its promises, showcasing substantial cost reductions and surpassing its original gross margin expectations in Q3.

- The company has established a gross margin range of 35 to 40% and offers modest expectations for growing the business over the next 18 months.

- Ouster's dominance in revenue surpasses all other participants in the lidar industry, accounting for 46% of the group's total revenue year-to-date.

Q3 Narrative

Six months have passed since I exclusively focused on Ouster ( OUST ), touting it as the prime lidar choice of 2023. Despite the disappointment in share price, the company has remarkably delivered its initial promises.

True to their word, the third quarter provided a glimpse into the future, showcasing substantial cost reductions, culminating in a $120M trim from the combined expenses of the two merging companies. Following the acquisition of Velodyne and the financial integration, the company has expanded its software revenue with unified Gemini and Blue City packages, presenting a comprehensive suite alongside its hardware, surpassing its original gross margin expectations.

Consequently, the company has established a gross margin range of 35 to 40%, with Q3 delivering a non-GAAP result of 33%. Furthermore, Ouster offers modest expectations for growing the business over the next 18 months, within the 30 to 50% range.

The third quarter bore almost a transformative quality. It delineated, perhaps for the first time to a broader audience, Ouster's ability to achieve growth and glimpse profitability while operating within verticals collectively known as the non-ADAS category. These verticals, long highlighted by CEO Angus Pacala, have been earmarked as holding the potential for billions in revenue.

As a bedrock of the future, OS sensors are now supported by robust software applications fortified by performance-improving deep learning AI perception models, resulting in booking millions of sales on their own.

According to reports, Ouster's DF sensors designed for consumer ADAS are currently undergoing evaluation. The company has maintained its tradition of revealing limited details and avoiding name-calling. However, this development is believed to be a major upside catalyst for future business growth, as the slide below indicates.

Ouster Inc., Q3 2023 Presentation

{kind=link}

Undeniably, Ouster has established its dominance in revenue, surpassing all other participants by accounting for 46% of the group's total revenue year-to-date. The company has reported $58.8M for the year so far. It has projected a Q4 range of $23M to $25M to exceed the average consensus of $81.4M and secure its position as this year's revenue leader among Western-based companies. I believe that Q4 has the potential to perform better than currently projected, considering the seasonality hinted at the start of the year.

2024 Forecast

As highlighted in sector insights , reductions in 2024 forecasts have materialized for Luminar ( LAZR ) and Aeva ( AEVA ). In contrast, Innoviz ( INVZ ) appears poised to maintain its projections unchanged for 2025 and 2026. Analysts have reduced estimates for Ouster by $3M in 2024 and $11M in 2025.

After thoroughly analyzing the bookings and reviewing the sequential additions, I find the reported amount of $131M somewhat conservative. The company has secured over $184M in new business, which includes figures from the previous year. Out of this, $100M has been converted into revenue, with $41M realized in 2022. A projected $25M for Q4 will leave approximately $59M for 2024. If the company maintains the average of the last two quarters and secures an additional $40M in Q4, Ouster will have around $100 million in bookings as it steps into 2024.

Adopting 2023 bookings, which currently stand at $114M, for the estimate for the first three quarters of 2024, the company would have accumulated $214M by Q3 2024—efficiently supporting the reported $131M. This flatline projection is for estimation purposes, but I also anticipate bookings to have a growth trajectory.

Cash Burn

In Q3, Ouster reduced its cash burn from Q1 by 52%, bringing it down to $27.2M. This was made possible by a gross profit of $3.09M. If not for this contribution, the operational cash burn would have been $30.2M. It is worth noting that the gross margin achieved was 14%, but it could have been 33% had the obsolete expense of $3.2M not been incurred. The company's total cash on hand was reduced by $23.9M, but a modest ATM draw of $2.9M helped boost it, resulting in an ending balance of $202.2M, including restricted cash.

It is important to note that the cash used in operating activities included a $3.5M litigation expense, which was likely used at least in part to protect its intellectual property in the ongoing dispute with the Chinese competitor Hesai ( HSAI ).

To break down the figures, if I remove the one-time expenses, the hypothetical cash burn for Q3 would be calculated as follows: the initial $30.2M operational cash burn minus the $3.5M litigation expense, resulting in an operating cash burn of $26.8M. Assuming a $6.3M gross profit from a 33% gross margin, the projected cash used in operating activities would be around $20.5M. Considering the ATM draw, the cash reduction would have been $17.5M.

Q4 Cost Analysis

The results from Q3 provide a valuable map into the company's potential performance in the upcoming quarter, and it seems that Q4 will outshine the dynamics observed in Q3.

First, let's consider the cash burn, reduced by litigation expense and excluding the gross profit contribution, which amounts to $26.8M. With an estimated 35% of $25M, this would yield a gross profit of $8.8M. Consequently, the cash used in operating activities would be approximately $18M.

If I speculate that the company utilizes an ATM draw of $3M, the total cash reduction would be around $15M, leaving it with $187M in cash as it enters 2024. Additionally, if my revenue projection for Q4 proves accurate, we can anticipate a more substantial gross profit increment.

Cash Runway

Referring to a longer time frame, I'll employ updated SA estimates for 2024, 2025, and 2026. The 2024 estimate slightly surpasses the company's projection by reaching $130.9M.

LIDAR Cash Runway Model Q4 2023- 2026 (in thousands) (Author, SA Estimates, Companies' Financial Results)

{kind=link}

Notably, the estimates have seen significant reductions for Luminar and Aeva, whereas Innoviz has remained unchanged for 2025 and 2026. According to Luminar's CFO's guidance , I've adjusted Luminar's 2026 gross margin to 35% and reduced its cash in operating activities to $50M for 2024. In setting the stage for 2024, I've considered a cash position of $300M.

Based on the conference call , I anticipate Innoviz could receive an income of $21M in NREs in Q4, potentially providing the company with $157M to start 2024. However, I faced the challenge of assuming margins for Innoviz and Aeva, as these companies have not explicitly provided expectations in this category.

Aligning with the model's prediction two weeks ago, it's becoming evident that Innoviz and Aeva necessitate substantial cash injections to sustain their growth. Aeva has already organized a preferred equity issuance of $125M to meet this need. The wholesome amount of NREs expected for Innoviz will potentially avoid it. If not, Innoviz will be heading to the market.

Investment Considerations

So, where does this leave an investor interested in the space? I will refer to the valuation statistics from my quarterly review, updated to account for the cash in Q4.

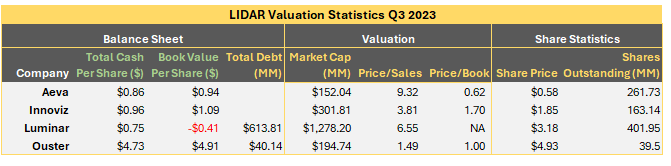

LIDAR Valuation Statistics Q3 2023 (Author, Companies' Financial Data)

{kind=link}

The data unequivocally underscores Ouster's strong financial position. Ouster boasts $4.73 cash per share, more than any companies included in this comparison. Furthermore, with a book value of $4.91, as per the Q3 balance sheet, the ratio is impressive 1 to the closing price on Friday at $4.93.

Finally, when considering the price/sales ratio, it's evident that Ouster occupies the lowest end of the spectrum. It's increasingly glaring how share prices in the sector appear disconnected, with sky-high valuations for some companies lacking support, while a company like Ouster, with significant intrinsic value, remains undervalued.

Mobileye ( MBLY ), often regarded as a stalwart in the sector, trades at a price-to-sales ratio of 14.99. The group in the table averages five, suggesting that Ouster's share value should exceed $16.

Conclusion

In my review, Ouster is profoundly undervalued in light of its remarkable performance. Its intelligent business strategy provides a solid foundation for achieving sustained profitability. Notably, the potential of consumer ADAS, though not explicitly reflected in the 2024 model, is expected to contribute significantly to the forecasts for 2025 and 2026, in my opinion, beyond the given projections.

Ouster has set itself apart by offering a sense of predictability, sparing investors from the uncertainty of awaiting final contractual awards, a common occurrence for others. While Luminar does have a place in my model, it's important to note that Luminar's elevated status within the industry and its association with renowned brands contribute significantly to its share price already, which stands at four times the value of Ouster when considering the price-to-sales ratio. Luminar and Innoviz pose higher investment risk than Ouster. Aeva's financing model carries 100% dilution risk and less revenue visibility, making it a less attractive option than everyone else.

Based on the Q3 results, I rate Ouster as a strong buy, with a price target of $12 for the next 12 months, a book-to-price ratio of 2.4, and a price-to-sales ratio of 3.6, predicated on $131M in revenue for 2024. Anticipating a more robust Q4 performance, surpassing the top end of the $25M guidance, further bolstered by my bookings analysis, I believe that Ouster can potentially increase the current estimate of $131M to $150M.

In my opinion, the market will eventually realize the actual value of Ouster. Institutional coverage will follow once Wall Street looks closer at this opportunity. However, for now, retail investors have a unique chance to invest in this fact-based and hype-free company before the institutions catch on.

For further details see:

Ouster Sets A Course Towards Profitability