PACB - Pacific Biosciences' Revio And Onso Lead Looks Priced In For Now

2023-11-21 22:50:51 ET

Summary

- Pacific Biosciences of California is a biotechnology company specializing in genetic sequencing for healthcare, agriculture, and environmental science.

- PACB's acquisition of Apton Biosystems aims to integrate short-read technologies and capture a larger share of the sequencing market.

- Despite its promising outlook, PACB's aggressive valuation suggests limited upside or downside, leading to a "hold" rating.

Pacific Biosciences of California, Inc. ( PACB ) is a biotechnology company founded in 2004. After Illumina failed to acquire PACB, it has become a promising company in the Genomic sequencing market, specializing in long-read HiFi with the Revio device and short-read technologies with the Onso instrument. PacBio has made significant contributions to healthcare, agriculture, and environmental science. Being chosen in the Telomere-to-Telomere project underscores its potential to revolutionize precision medicine and genomic research. Recently, PACB announced the acquisition of Apton Biosystems to integrate both short-read technologies to create a billion reads per flow cell sequencer. The strategy aims to capture a larger share of the multi-billion-dollar sequencing market. Yet, PACB remains an unprofitable company. The best valuation approach is through an EV/Sales multiple. My valuation analysis suggests that most of PACB’s optimistic outlook is already baked into its valuation, leaving little room for upside or downside from that perspective. Hence, while I lean bullish, PACB’s aggressive valuation multiple leads me to rate it a “hold” at this juncture.

{kind=link}

Business Evolution and Overview

Pacific Biosciences, known as PacBio, specializes in genetic sequencing systems for accurate long-read and short-read technology to solve complex problems in healthcare, agriculture, and environmental science. PACB began in 2004 under the name of Nanofluidics, Inc. 2004, based on research done at Cornell University. In 2005, PACB changed its name to Pacific Biosciences of California, Inc., but has experienced significant changes since then. Particularly, in 2018, Illumina Inc. attempted to buy PACB for PACB)%20today%20announced,in%20an%20all%2Dcash%20transaction." > US$1.2 billion in a deal to be closed at the end of 2019. However, the Federal Trade Commission blocked the acquisition, alleging it would eliminate a competitor to Illumina’s monopoly in deciphering genetic material. The deal had to be abandoned in January 2020. Illumina agreed to pay PACN $98 million for the termination fee with extension payments of $28 million.

Today, PACB offers sequence devices and consumables. PACB has two sequencing platforms: sequencing by binding ((SBB)) chemistry with the Onso device and single-molecule real-time sequencing ((SMRT)) used in Revio . The Onso instrument provides short-read sequencing technology that delivers 500 million reads per run to process samples through sequencing by binding ((SBB)) chemistry for $259,000 per system, including a cluster generator. The Revio system can parse long strings of genetic code. It can simultaneously analyze up to four new single-molecule real-time cells ((SMRT)). The Revio system is available at $779,000, and a list pricing of $995 for a 30-fold HiFi human full genome coverage.

Source: PacBio AGBT Workshop 2023

Moreover, PACB announced the creation of the HiFi Solves consortium to join researchers from 11 countries and 15 research institutions in the area of genomics to study High-fidelity (HiFi)-based human genome sequencing applied to clinical research, aiming to accelerate global adoption of human ADN-HiFi sequencing through the sharing of best practices. HiFi sequencing offers longer and more accurate reads, allowing us to assemble better, understand the genome, and identify genetic variations. Through the HiFi Solves consortium, researchers will study many possible genetic mechanisms in rare diseases, and, in general, they will explore relevant genes in complex regions of the human genome.

PacBio's Competitive Profile and Strategic Development

Since 2020, after Illumina failed to acquire PACB, the company has continued developing its HiFi sequencing, delivering new devices like Revio with strong initial demand from research, clinical diagnostics, and agricultural genomics institutions. Initiatives like the HiFi Solves consortium help to achieve specific market penetration. The income generation is growing by selling its advanced sequencing systems and consumables needed for its operation. PACB is part of a new era where genetic information will play a key role in precision medicine as the adoption of the Revio systems is strong.

Notably, Illumina, Inc. ( ILMN ) is one of PACB's main competitors. Currently, ILMN also has long-read devices with a different approach than Revio. On the other hand, ILMN uses a sequencing technique that combines marked and unmarked data from standard short-read genome sequences to generate long-read sequences with N50 of 5-7 kb, with some reads exceeding 10 kb. PACB focuses on HiFi sequencing with circular consensus sequencing ((CCS)) that involves multiple passes over a single molecule to create long reads of up to tens of thousands of bases with high accuracy. Therefore, the approaches of both companies differ. ILMN combines long- and short-read technologies in the same instrument, while PACB focuses on delivering HiFi accuracy in long-read sequencing in the Revio system. It is worth noticing that PACB HiFi sequencing has an accuracy rate of over 99% and was the sequencing technology used in the Telomere-to-Telomere project to complete the human genome sequence.

Source: PacBio to Acquire Apton Biosystems presentation

Nevertheless, PACB has announced that it would acquire Apton Biosystems at approximately $110 million. Apton Biosystems specializes in short-read sequencing technology, and PACB plans to integrate its technology with the PACB´s SBB chemistry platform to create a billion reads per flow cell sequencer. The strategy aims to capture a larger share of the multi-billion-dollar sequencing market .

Valuation Analysis

Furthermore, it's important to note that the gene sequencing market will likely not be a “winner-takes-all” market. This means that PACB should be able to retain and grow its current market share. I speculate there’s a decent chance PACB will increase its market share due to its development of short-read sequencing technologies, particularly with its acquisition of Apton . This means that PACB’s competitive profile will be more comprehensive in the future, making it a tougher competitor against ILMN and others.

Source: Grandview Research.

Also, I'd like to point out that PACB operates within the healthcare sector and the medical devices sectors in broad terms. These two are expected to grow at a 4.0% and a 5.9% CAGR, respectively, representing broadly favorable secular tailwinds. However, this sector is expected to grow at a 16.5% CAGR until 2030, specifically within the genomics industry. These growth currents are extremely favorable tailwinds for PACB and suggest that its best years are yet to come. In fact, the company’s revenue CAGR has been about 19.6%, which means it’s gaining market share from its competitors because it surpasses the industry’s CAGR.

{kind=link}

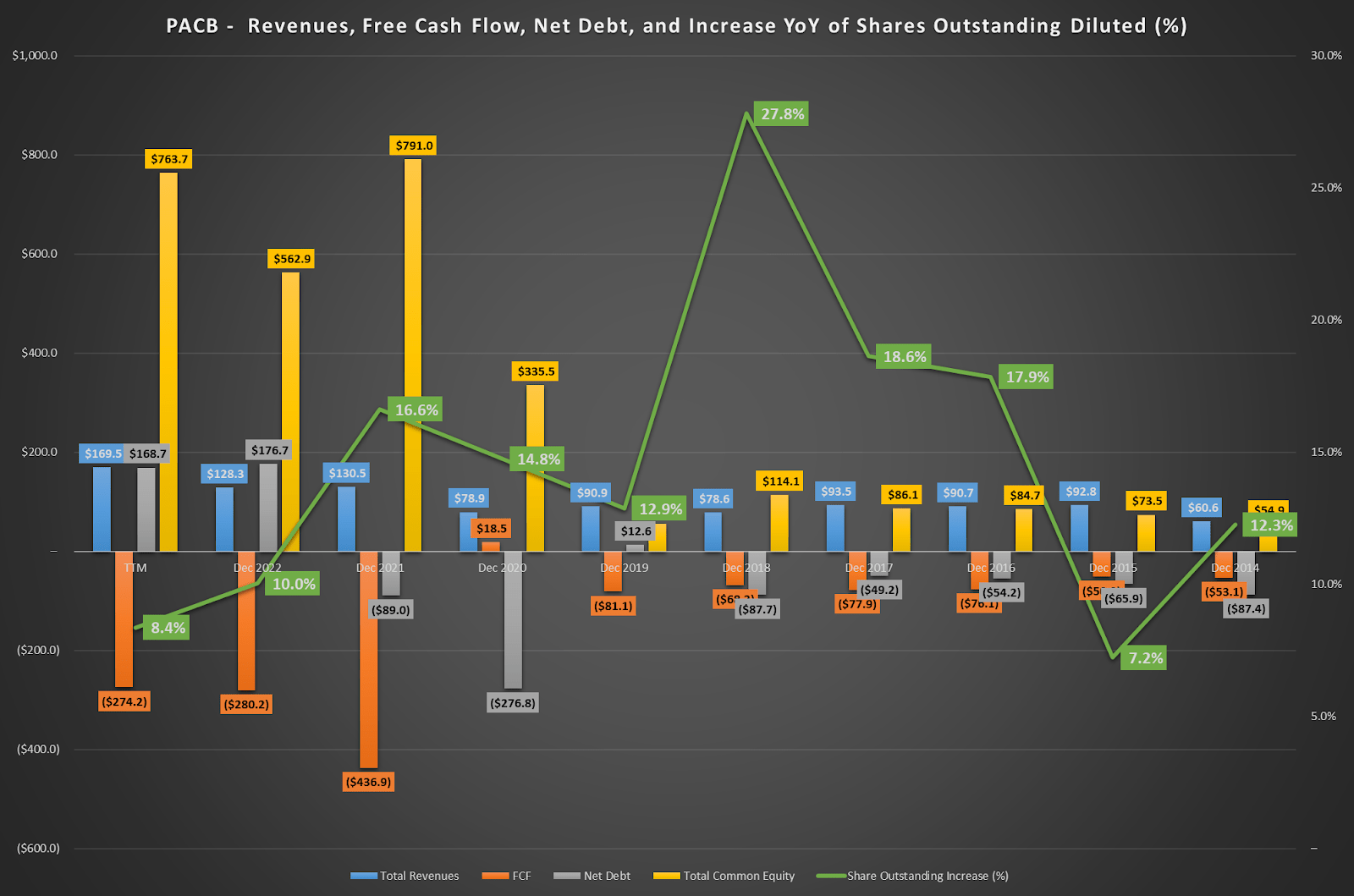

However, it’s also important to realize that the company has consistently issued shares to fund its operations since at least 2014. As you can see, on average, it increases its outstanding shares by 14.6% per year, though it has been slightly less in recent years. Still, the dilutive factor of PACB’s equity can’t be ignored. Moreover, over the years, the company has grown its revenues at a healthy CAGR of 19.6%, but its FCF hasn’t followed suit and remains deeply negative. In fact, the negative FCF has only deepened as revenues increased. This creates doubts about the company’s ability to translate into tangible cashflows and profits the additional revenues it’s generating. It raises concerns for investors expecting PACB to quickly turn the corner and become profitable. But overall, I’d argue this is congruent with a company still in its early stages. This, coupled with the rising debt , means that PACB should be valued using a multiples-based approach and its enterprise value figures.

With this in mind, let’s consider that by 2023 and 2024, analysts expect PACB to post $197.83 million and $261.49 million in revenues. This would imply a 54.2% and 32.2% YoY revenue growth, well above the sector’s CAGR of 16.5%. In fact, it’s 228.5% and 95.2% higher than the sector’s CAGR. This is important because we can use this to estimate the EV/Sales premium it should have over the rest of the industry.

Author's elaboration.

For context, the company’s sector’s EV/Sales multiple is 3.48 . But since we know PACB’s revenues are growing faster than the sector average, we should also assign a higher EV/Sales multiple. Using the previously calculated figures, I estimate an EV/Sales multiple in the range of 11.43 and 6.79. I got these figures by increasing the sector EV/Sales multiple by 228.5% and 95.2%, reflecting PACB's above-average revenue growth. Thus, using the 2024 revenue estimates of $261.49 million implies an enterprise value of $2.99 billion to $1.78 billion, respectively.

Author's elaboration.

Nonetheless, after accounting for this premium, PACB’s fair value looks roughly in line with its current market cap. Thus, I think it’s fair to conclude the company is priced right now, leaving little upside or downside from a valuation perspective. Naturally, this is not to say that the company’s stock can’t appreciate or depreciate from current levels. Still, given the current outlook, it does signal that its prospects appear fairly valued. Moreover, this is further corroborated after considering that PACB has been historically highly dilutive, so I think that, as a whole, it makes sense to give it a “hold” rating at this juncture because its valuation is already pricing in PACB’s higher than average revenue growth rate.

Q3 Developments

In Q3 , PACB shipped 52 Revio instruments for revenue, a record number in one quarter. PACB also sent the first Onso unit while receiving orders from 10 countries for various application types. PACB expects to continue increasing shipment numbers in the fourth quarter. The company also had Revio's consumable revenue of $9.3 million despite being just the second full quarter of the instrument in the market. This is because Revio use increased in Q3 compared to Q2, evidenced by the data generated. The continued adoption of Revio allows PACB to increase the 2023 revenue guidance; they expect full-year revenue to be between $195 million and $200 million.

Existing customers are expanding Revio capacity and have shared that the instrument has enabled them to obtain results in less time using HiFi sequencing than legacy tests. Additionally, PACB made a software update that optimizes the preload feature of Revio, which allows customers to load the next round while the sequencing is underway. In the fourth quarter, more updates and improvements to the platform. Moreover, PacBio has the vision to be a multi-omic company to understand the connection between the genome, epigenome, transcriptome, and proteome to have insights into multiple layers with information about biology and disease. Revio can be a multi-omic instrument, and various researchers are exploring this capacity.

So, indeed, PACB’s promising fundamentals deserve a premium. However, when we layer our multiples-based valuation on top of the technological developments, it appears that it’s mostly priced in already. This doesn’t make the stock bearish, but investors will likely get a reasonable CAPM-like return of 13.0% over the long term if they buy at these levels. Conversely, if your goal is to achieve alpha, you should likely wait for lower prices on PACB, such that you get excess returns on the CAPM.

Closing Thoughts

Overall, PACB’s technology in genetic sequencing appears to be extremely innovative and offers a more comprehensive perspective than simple short-read alternatives. Moreover, after the Apton acquisition, PACB’s prospects, even in short-read sequencing, will likely improve over time. As a result, it’s reasonable to anticipate faster-than-average revenue growth for PACB, and it’s likely to gain market share. However, from a valuation perspective, it appears that the market is already factoring in these optimistic assumptions, which leads to it being fairly valued at the time. Thus, as a whole, I lean bullish. However, despite the considerably favorable assumptions and uncertainties baked into PACB’s valuation, it still looks fairly valued. Thus, giving it a “hold” rating is prudent for now.

For further details see:

Pacific Biosciences' Revio And Onso Lead Looks Priced In For Now