DIS - Paramount Global: A Long-Term Play

2023-03-06 07:23:32 ET

Summary

- Paramount Global is spending billions on new content, keeping FCF negative and EPS depressed.

- The spending is necessary to remain relevant and competitive for the long term rather than fade away.

- All this spending is to drive profitability in the future, but it means the dividend is rather precarious for now.

- I also share a recent covered call trade that expired worthless, though am cautious to not have shares called away.

Written by Nick Ackerman. This was included originally in a post to members of Cash Builder Opportunities on March 4th, 2023.

Paramount Global ( PARA ) is working through a difficult period in which they need to adapt to streaming and have it work or risk fading away. Traditional TV media continues to decline and can't be relied upon going forward. People do not watch TV as they used to. Personally, I'm not even a cord-cutter; I'm a cord-nevers.

That's especially true with an anticipated recession coming up and companies looking to cut back on spending. An easy place to cut back on spending is advertising. That can be particularly true of the larger brands that spend the most money, where people won't forget about their brands if it isn't flashed in front of our faces for a while.

Streaming And Earnings

Streaming isn't an easy business. It costs billions to make movies and shows that people want to watch. Cut back on spending, and you risk losing subscribers, of which PARA has been increasing subscribers at a healthy clip.

On the other hand, other streaming services are also spending billions, and a smaller company such as PARA can have difficulty keeping up with Netflix ( NFLX ) or Disney ( DIS ).

To help combat that, they will be integrating Showtime into Paramount+ to give Paramount+ a big boost in additional content for streaming. They believe that will help drive top-line growth to get them on the path of streaming profitability. When asked about the next 1 to 2-year goals in the Deutsche Bank Media, Internet & Telecom conference call , here is what they had to say.

Our focus now is going from that top line growth to starting to deliver on the path to profitability for streaming. And that means that we have to do a couple of things. Number one, we're very focused on continued revenue and particularly ARPU growth. There's a variety of levers that we will be executing against over the course of the next few quarters to drive that. I'm sure we'll talk about some of those.

And then we're also focused on the expense side of the equation and really starting to drive leverage against the investments that we've been making in content, marketing and the like. And that includes doing things like integrating Showtime and Paramount+, which unlocks opportunity, frankly, on both the top end and the bottom line.

In looking at their direct-to-consumer or "DTC," they have continued to experience significant growth in revenue. DTC includes Paramount+ but also their other less popular services.

PARA DTC Services (Paramount Global)

However, that hasn't resulted in positive adjusted operating income before depreciation and amortization or "OIBDA." Here's a breakdown of the DTC segment

PARA DTC Earnings (Paramount Global)

{kind=link}

That was despite the 30% or $1.4 billion in increased revenue off of ~77 million global DTC subscribers. Paramount+ accounts for 56 million of those subscribers, which was an increase of 9.9 million in the latest quarter alone. The Paramount+ service also experienced 81% year-over-year revenue e growth. As we can see, though, despite that, the adjusted OIBDA decreased substantially as expenses rose to $2.4 billion. That's spending on content and expansion of the service internationally.

Turning to their TV Media segment, here was the results.

PARA TV Media Earnings (Paramount Global)

{kind=link}

This highlights why they need to find growth from elsewhere as advertising, affiliate and subscription and licensing, and others are all in decline. TV Media is the largest part of their business, as it accounted for $21.732 billion in revenue. That's why changes in that segment have such an outsized impact on the company's results as a whole.

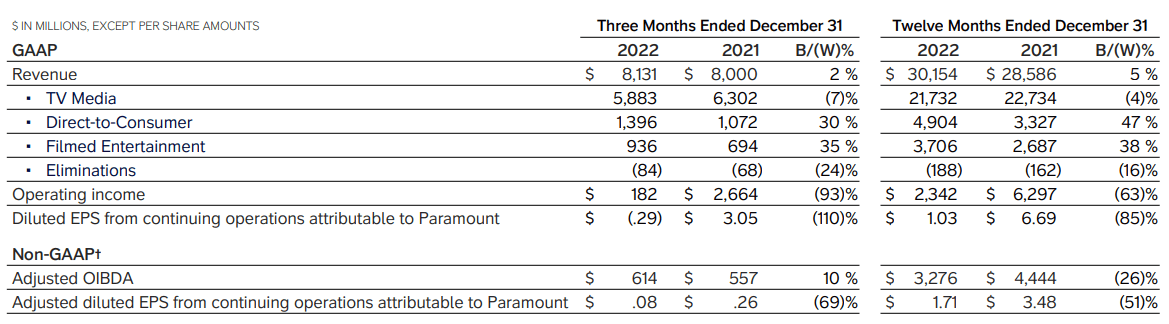

Here's a breakdown of each of their divisions, including filmed entertainment. Filmed entertainment can be inconsistent, as movies can really be hit or miss. That being said, it certainly helps deliver some monster cash flows on occasion when a hit really hits.

PARA Overall Earnings (Paramount Global)

{kind=link}

With $1.71 in adjusted diluted EPS for the prior year, it was a drop of nearly half from the prior year. They also aren't cash flow positive, so that's where the dividend can come in jeopardy. However, they know that they can pull some levers and become profitable, but they are choosing (I feel wisely) to try to grow their streaming service.

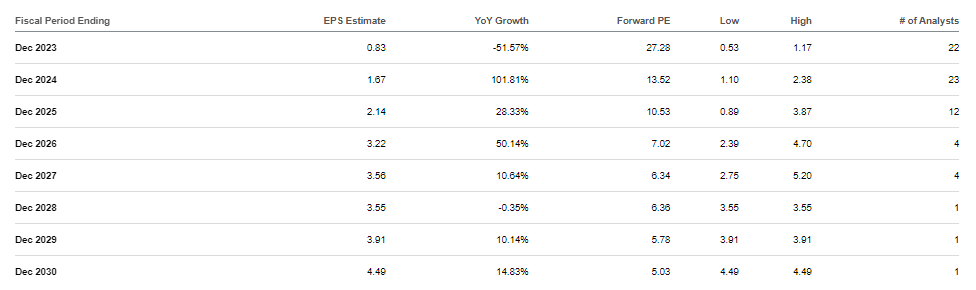

Analysts are expecting their earnings to drop sharply in the next year as well before ramping up significantly. So I wouldn't expect any great earnings coming into this next fiscal year.

PARA EPS Estimates (Seeking Alpha)

{kind=link}

Dividend, Dividend, Where Art Thou Dividend?

While their dividend isn't as sacrosanct compared to other companies, they indicate that they continue to expect to pay dividends in some capacity.

Here's from their 10K :

We currently expect to continue to pay regular cash dividends.

Here's their response to a question in a recent conference call:

Q: Maybe let's talk about free cash flow and dividends for a second. Some market participants have concerns about the lack of free cash flow generation currently and your leverage ratio being elevated as you're investing. And that includes some concerns over the sustainability of the dividend. Can you just maybe address these concerns, talk about liquidity, the outlook for improvement in free cash flow and also how the balance sheet will de-leverage from here?

A: ...Now at the same time, we do pay attention to our balance sheet. We care about our credit rating, we care about being. And when I look at that lens, we're in a good position. We've got -- we finished 2022 with over $3 billion of cash on the balance sheet. We have no near-term debt maturities, and we got a $3.5 billion revolver that remains completely undrawn.

So to the extent that we have to bridge anything in the short term, we've got the flexibility to do that. And we continue to be very thoughtful about capital allocation and making sure that we're balancing all of those objectives in a way that makes sense.

In the response, they didn't directly address the question but skirted around it. So I believe it could mean that they are looking to reduce the dividend potentially but still will pay something. I think that's a reasonable assumption, as they are more focused on growth rather than returning capital to shareholders.

Then finally, in their earnings call , they had this to say about their dividend payout:

And then I think the last part of your question related to the dividend and what I'd say there is that our capital allocation strategy is well aligned with our operating plan. Yes, cash flow will be negative in 2023. That's sort of the nature of some of the context we're operating in, including the fact that we're going to be at peak losses for D2C in 2023, and there are some ad headwinds. But both of those things are short-term in nature.

We're going to start to grow D2C earnings next year, and we do expect the ad market to recover starting in the back half of 2023, which means that we're going to see significant improvement in OIBDA and free cash flow in 2024. And in the interim, we've got a very strong balance sheet that includes over $3 billion of cash on the balance sheet.

By this time last year, the Q1 dividend was already declared, the ex-div came in mid-March, and the pay date was the first of April. In fact, that's been the case for the last ten years. I haven't seen any news yet, which is another reason that makes me uncertain that the current dividend will remain. Dividend schedules are subject to change, but a company that has other dividend red flags can mean something. Only time will tell on this front, but when considering PARA, I wouldn't be investing solely for the dividend here.

Valuation

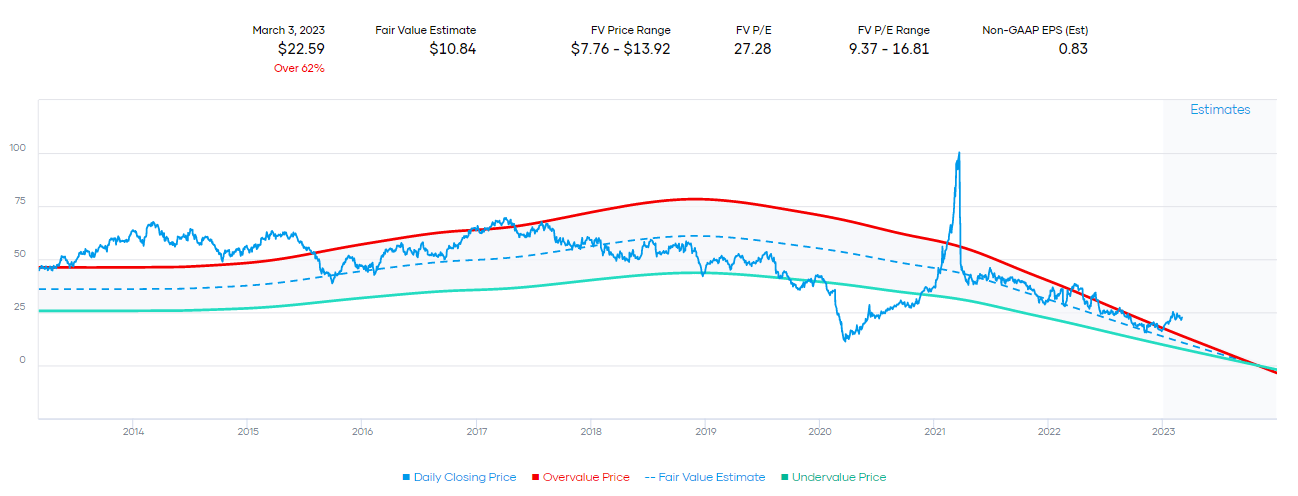

With a lack of earnings, it becomes quite difficult to value the company. It becomes more about expectations in the future. As we can see now, the forward P/E is off the chart, and that's pushing shares of PARA into an overvalued level.

PARA Fair Value P/E Estimate (Portfolio Insight)

{kind=link}

This is directly related to them spending billions on content, though. They could easily let the earnings come back up if they let off the spending. However, that would stifle future growth and leave them in a worse position over the long term, in my opinion.

So are the share cheap or not? This is a difficult question to answer. Based on the near-term earnings, yes, shares look quite extended. However, if you have a bit longer time frame of two or three years, things look much better. That is, of course, assuming things work out as expected and the streaming becomes profitable.

Recent Covered Call Trade

PARA is a little bit different from our AT&T ( T ) position because I view T as more of a specific options play. T is another covered call trade we had expire in the latest weekly options expiration. I view PARA as a longer-term holding. Where with T, I don't mind holding, and it might be a long-term hold before having shares be called away, but I'd be less concerned if it's called away.

Despite that, we've still had a couple of opportunities to write covered calls conservatively in this name. The latest was our trade expiring on March 3rd, 2023 . We had written calls at $25 and collected $0.32 in option premium. This trade expired worthless, which followed the same path as the covered calls we wrote and had expired in December too. At that time, we collected $0.25

Both amounts seem small but are actually larger than the dividends that PARA pays out. In this case, it's equivalent to 1.333x of the $0.24 quarterly amount. Since we've accomplished that in 39 days, it also means we are collecting it at a greater frequency. The potential annualized return or 'yield' is nearly 12%. Since this was a position we previously accepted an assignment at for $21, it actually works out to a 14.26% PAR based on that assignment price.

Admittedly, what I thought was a fairly conservative covered call trade that didn't 'risk' having the position called away turned out to breach the $25 strike price briefly. At the time the calls were written, it required a 19.05% increase to hit that level. However, shares fell back after that and never reached that level again during the duration of the trade.

Ycharts

We originally were put shares at the end of September. During that time, we collected the Q4 dividend.

Conclusion

PARA is a higher-risk play, in my opinion, but I believe shows promise. They have been spending billions for streaming content that is unprofitable, but I believe that is better than standing still and letting their TV Media business fade away. During this time, I believe the dividend is precarious, but they've indicated they are continuing to expect to pay some dividends through this period of heavy spending.

For further details see:

Paramount Global: A Long-Term Play