PARAP - Paramount Global: A 'Wait-And-See' After Recent Plunge

2023-05-29 08:35:40 ET

Summary

- Paramount Global shares have fallen significantly, but a recent investment from BDT Capital Partners in National Amusements, Inc. has been perceived as a vote of confidence.

- The company has seen growth in its Paramount+ streaming service and Pluto TV platform, but struggles with debt and volatile profitability metrics.

- Despite the potential upside, the uncertainty surrounding the company's debt and cost-cutting initiatives make it a better 'hold' prospect than a bullish investment.

This month has not been particularly pleasant for shareholders of entertainment conglomerate Paramount Global ( PARA ) ( PARAA ). After reporting some rather painful news earlier in the month, shares of the company immediately plunged 28.4%. Since then, they have fallen another 14.1%. Fortunately, on May 26th, investors in the business were given something of a reprieve. Shares popped higher, closing up 5.9% for the day. This was based less on what the company did and more on what its controlling shareholder elected to do. And while I don't expect the maneuver itself to have a material impact on Paramount Global, I can understand that the market would perceive this development, justifiably so, as a vote of confidence in the business. What this did do for me, however, is prompt me to dive in and see if, after shares have fallen so far, the company offers any upside for investors. From a price perspective, I would argue that it very well could. But I also think that the company is far from riskless. And when you account for that risk, I would argue that the company makes right better ‘hold’ prospect than it does anything more bullish.

An interesting development

As the month of May began drawing to a close, some rather interesting news hit Paramount Global and its shareholders. The stock popped higher after news broke that NAI (National Amusements, Inc.), the legal entity that the Redstone family has historically used to control Viacom and CBS, received an investment from BDT Capital Partners in the amount of $125 million. The investment in question is set up as a preferred equity investment and it will allow NAI to reduce debt and reduce interest expense. An alternative approach to this would be for NAI to sell off some of their ownership of Paramount Global or other assets, but that would result in them reducing their control. Instead, NAI is essentially pledging some of its shares in Paramount Global as collateral in the event that they don't make good on paying off the debt.

For those who are not aware, NAI is a rather substantial company in terms of size. It boasts 837 movie screens spread across the US, UK, and Latin America. It has other assets as well. In addition, it currently owns 77.3% of the Class A voting shares of Paramount Global, as well as 5.2% of its Class B units. All combined, the company has a 9.8% equity interest in the firm. But it does essentially control the business through the aforementioned Class A stock. The fact that management prefers taking on a preferred equity investment as opposed to selling a rather small portion of their stock is a testament to how confident they are in the business moving forward. And that is what drove shares higher on May 26th.

Assessing Paramount Global

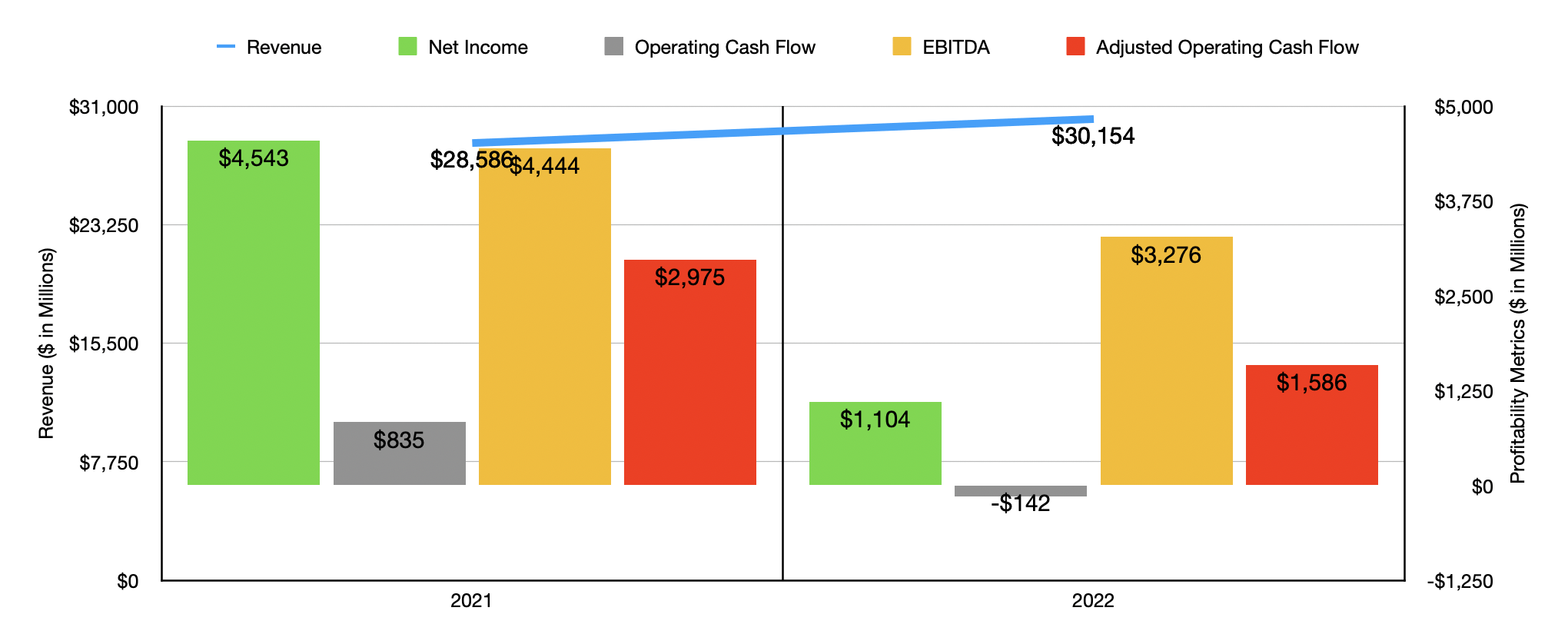

Operationally, Paramount Global is an interesting business. It's also quite large in the grand scheme of things, even though it's not really considered one of the majors in the streaming space. In 2022 , for instance, the firm generated revenue of $30.2 billion. That was up from the $28.6 billion the business reported one year earlier. While the overall revenue trajectory for the company has been positive, profits have been all over the map. Net income fell from $4.5 billion in 2021 to $1.1 billion last year. But a big portion of this decline was attributable to the fact that, in 2021, the company had $2.3 billion worth of net gains associated with asset sales.

{kind=link}

Other profitability metrics, however, have also been rather volatile. Operating cash flow, for instance, went from $835 million in 2021 to negative $142 million last year. When I analyze companies, I like to also look at a version of this that adjusts for changes in working capital. But for entertainment companies that are content-rich like this, a special adjustment needs to be made. You see, included in working capital is a significant reduction in inventories associated with content on the company's books. But this is only offset by an item that is not included in working capital adjustments. That would be the amortization of content costs and participation and residuals expense. Factoring this into the equation, we get a realistic adjusted operating cash flow figure of $1.6 billion. But that's roughly half the $3 billion generated in 2021. And finally, over that same window of time, EBITDA for the business fell from $4.4 billion to just under $3.3 billion.

{kind=link}

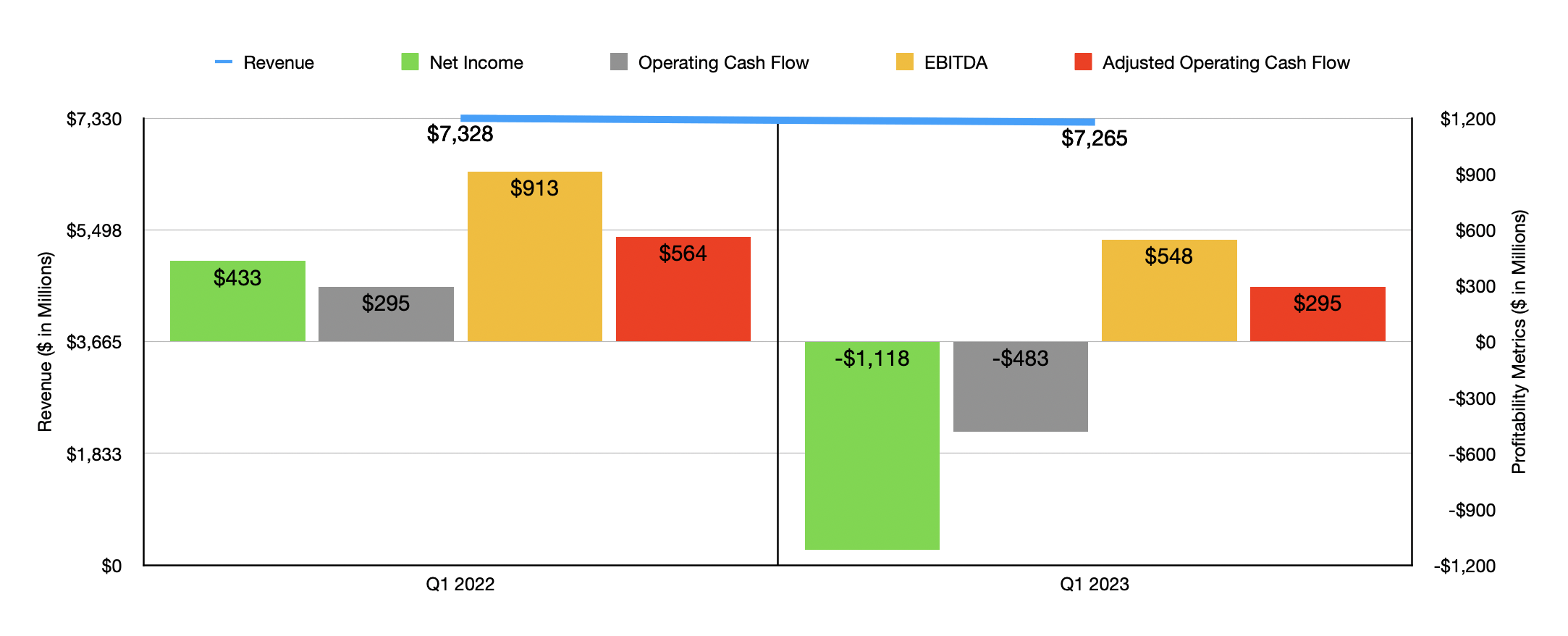

Clearly, Paramount Global has some cost issues to worry about. Those have continued into the 2023 fiscal year. As you can see in the chart above, revenue for the company dipped slightly in the first quarter of 2023 compared to the first quarter of 2022. However, the firm went from generating a net profit of $433 million to generating a net loss of $1.1 billion. Operating cash flow went from $295 million to negative $483 million, while the adjusted figure for this went from $564 million to $295 million. And finally, EBITDA fell from $913 million to $548 million.

To address these concerns, management has finally taken action. Though I would have liked to see that action come about earlier. Earlier this month, the company said that it was lying off approximately 25% of its staff in its domestic cable networks operations. Perhaps the greatest casualty of this development is MTV News. According to management, it is being shuttered completely. Shareholders are also being forced to take a haircut of sorts. When management announced financial results for the first quarter of its 2023 fiscal year, it said that it was reducing its dividend by 79%. That took the distribution from $0.24 per share down to only $0.05 per share. Based on my estimate, this should shave off about $534 million worth of cash flow that management can use to reduce debt. As of the end of the most recent quarter, the company had $13.7 billion in net debt on its books. This massive amount of debt translates to about $904 million of interest expense annually.

{kind=link}

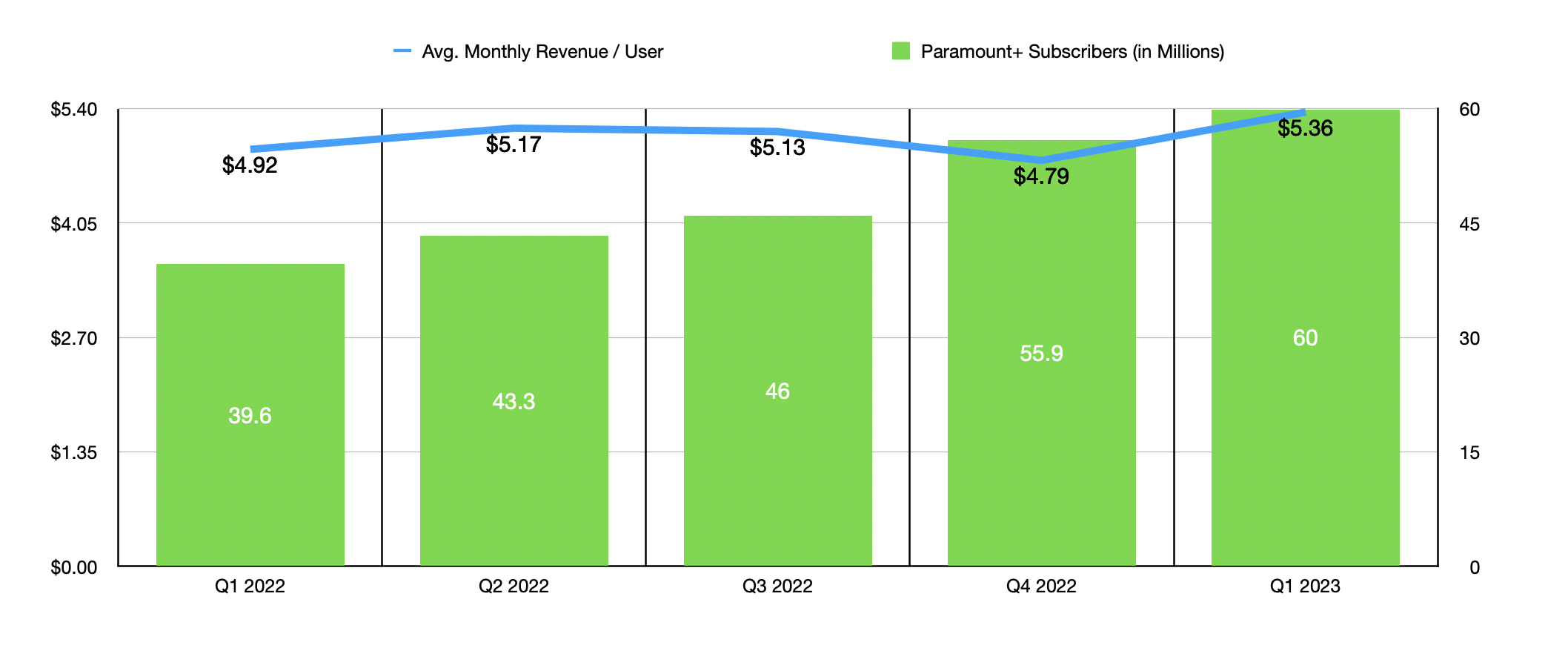

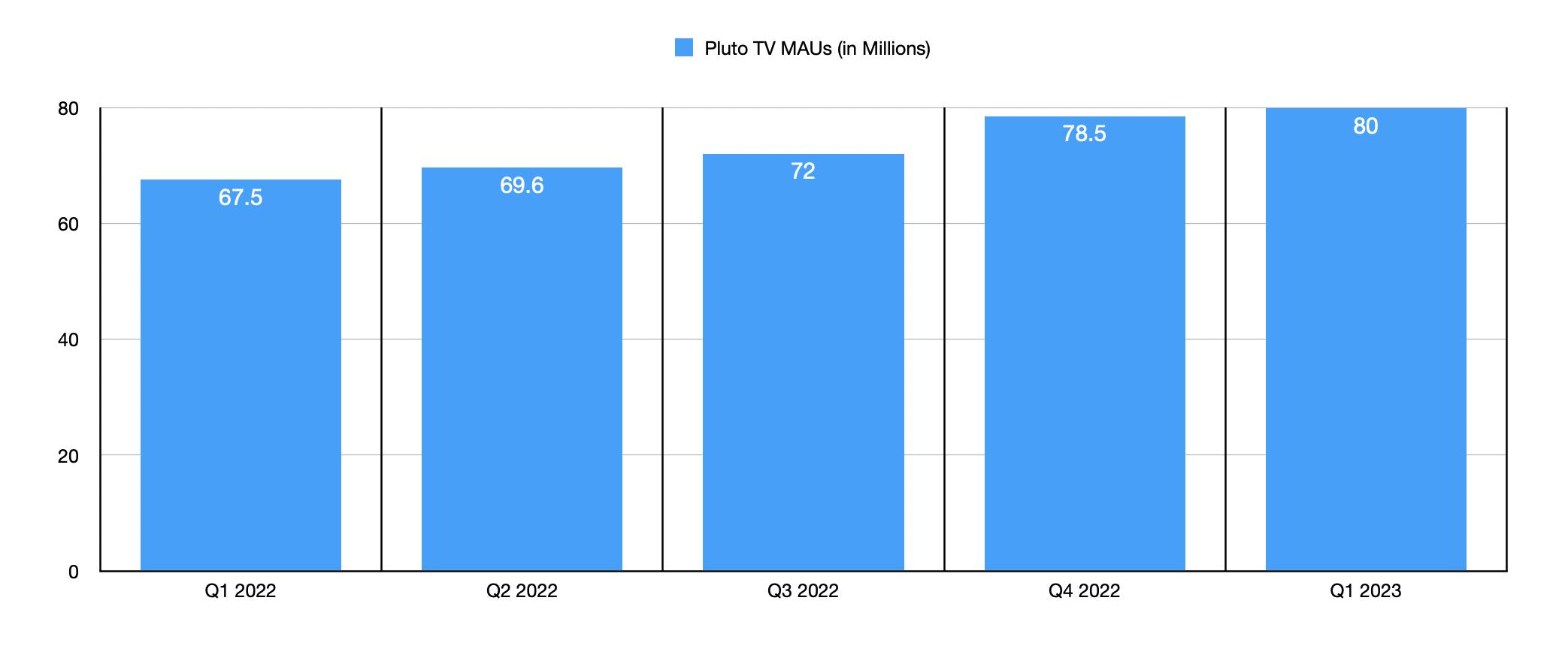

This is not to say that everything regarding the company is bad or broken. There have been some bright spots in recent years. In the chart above, for instance, you can see the growth in the company’s Paramount+ streaming service from the first quarter of 2022 through the first quarter of this year. The platform nearly doubled in size from 39.6 million paying users to 60 million. And over that window of time, the average revenue per user grew from $4.92 to $5.36. And in the chart below, you can see the growth in the MAUs (Monthly Active Users) that the company has on its Pluto TV platform. For those not aware, Pluto TV is a free TV streaming service that is largely supported by advertising revenue. At the end of the most recent quarter, it had 80 million MAUs. That represents an increase of 18.5% over the 67.5 million that it had one year earlier.

{kind=link}

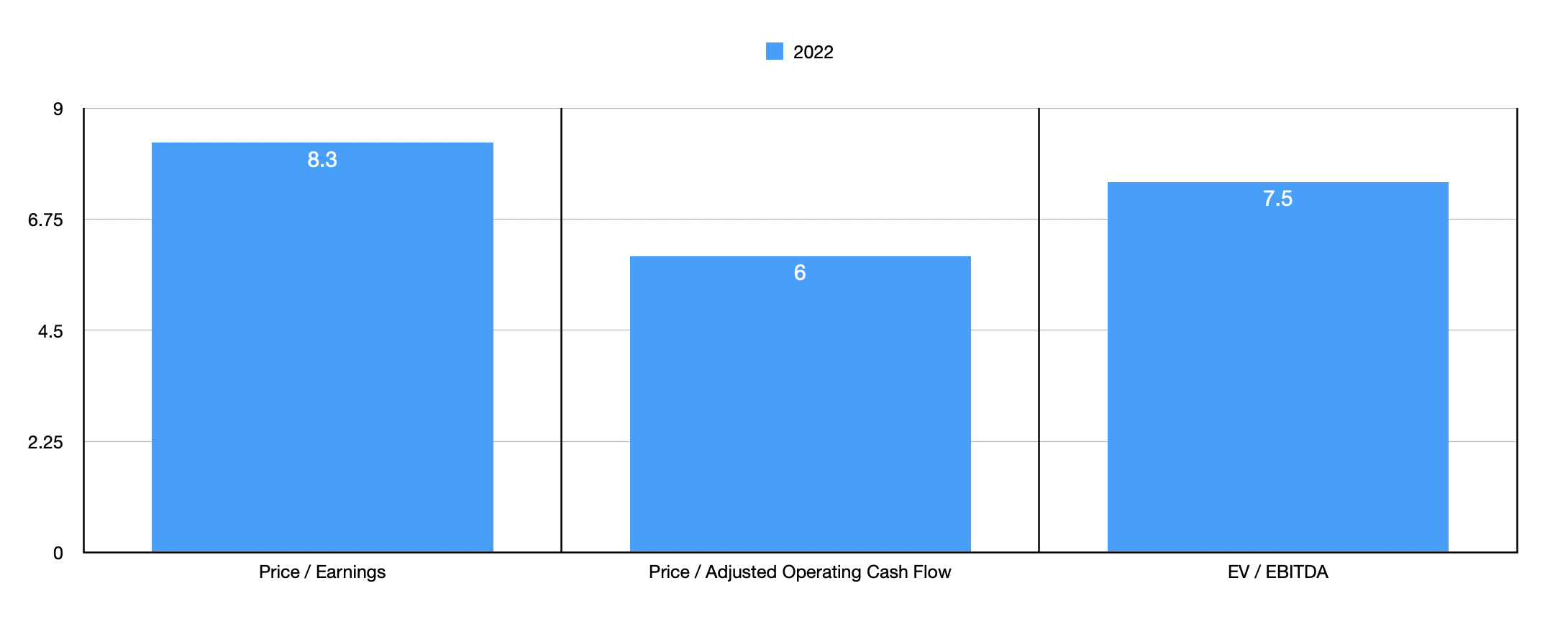

This consistent and attractive growth, especially at a time when the streaming market is showing mixed results, makes the company an intriguing prospect, especially when you consider how shares are priced at the moment. Using data from 2022, the firm is trading at a price to earnings multiple of 8.3. The price to adjusted operating cash flow multiple is only 6, while the EV to EBITDA multiple is 7.5.

{kind=link}

Takeaway

At this moment, Paramount Global is an interesting play for investors to consider. I like how cheap shares are. I like its streaming and free TV platform growth. I like that management is cutting costs and I appreciate their move to cut the distribution. Given the distribution cut, it also makes sense that NAI would bring on a preferred equity investment in order to cover some of the cash they are missing out on. They could have simply sold stock in the firm. But they definitely seem to believe in its potential from this point on. That is also a positive in and of itself. I do not like the amount of debt that Paramount Global is saddled with. I think its bottom line results over the past several quarters have been disappointing and it truly is a ‘show me’ story regarding cost cutting initiatives. One fear is that cutting costs too much could result in a decline in the quality of its assets. So that is something investors need to be very mindful of. Given all of this uncertainty in the air, and in spite of the fact that there are certain aspects about the company I do appreciate, I believe that a more appropriate approach to the business is to rate it a ‘hold’ and to wait to see what kind of developments take place over the next one or two quarters.

For further details see:

Paramount Global: A 'Wait-And-See' After Recent Plunge