DIS - Paramount Global: The Mission Impossible Of Selling At Fair Value

2023-12-11 18:00:00 ET

Summary

- Paramount Global's Q3-2023 results showed strong revenue growth in its direct-to-consumer area but advertising continued its weak trend.

- Peak losses was one of the reasons the stock rallied hard.

- We tell you what stands in the way of achieving a sale at fair value and also weigh in on the convertible shares sporting a 25% yield.

It has been a long and painful journey for Paramount Global ( PARA ) ( PARAA ) shareholders. Since the 2021 momentum bubble, driven by nothing but hot air and one hedge fund leveraging funds to the max, things have looked glum.

That chart should bring to the forefront the popular saying that exponentially rising stocks go further than you think, but never correct by going sideways. For our part, we sidestepped the entire bubble phase, and started to get involved under $30. Repeated covered call selling and some "buying of the dip" has gotten us to an approximate $20 adjusted cost basis. With all the news of a potential buy out in the wings, we decided to see if we might finally get a return on our capital (or even a return of our capital). Let us first look at the Q3-2023 results and see if PARA is finally turning the corner on its loss making ventures.

Q3-2023

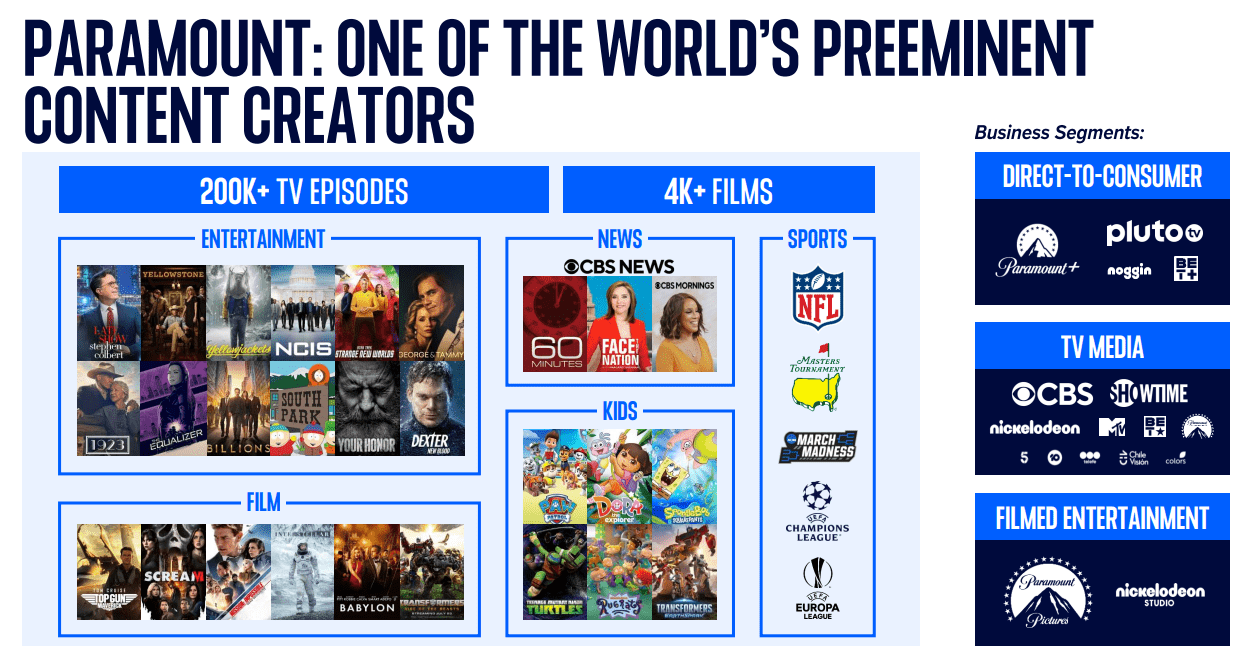

While the financial numbers may or may not impress investors, there remains no doubt that PARA is the king of content. Whether you gauge it by TV episodes or movies made, PARA holds some of the strongest assets in the business.

{kind=link}

PARA Q3-2023 Presentation

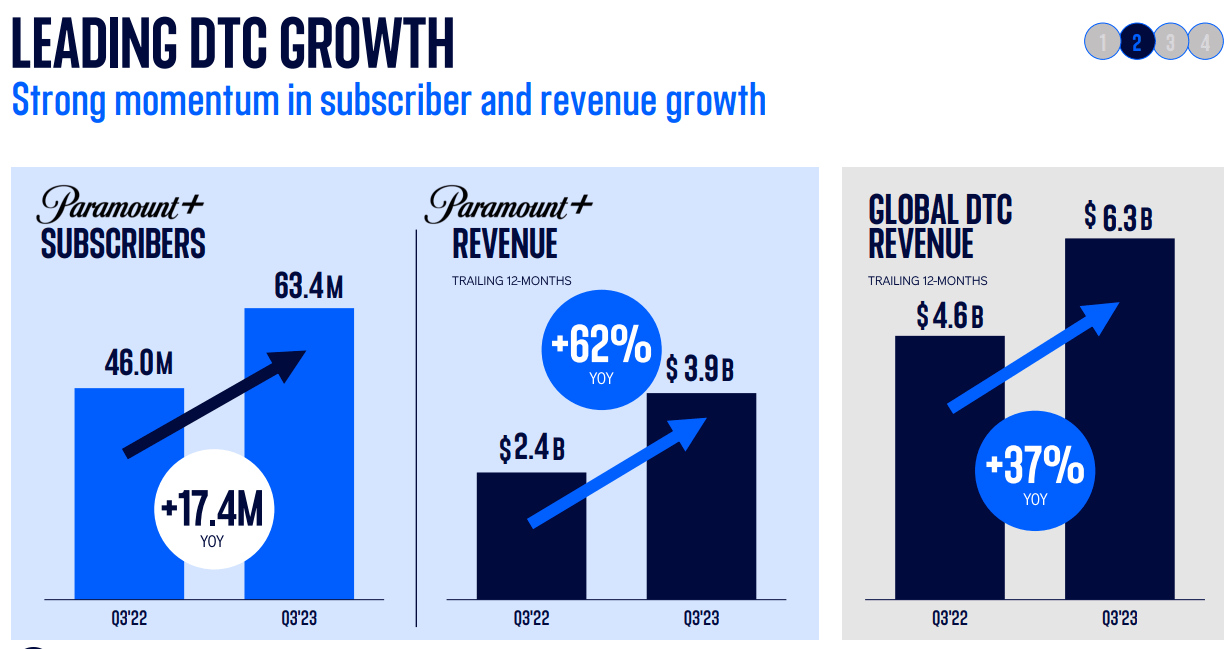

Their direct to consumer area increased revenues by 62% year over year in the US and total global revenues were up 37%.

{kind=link}

PARA Q3-2023 Presentation

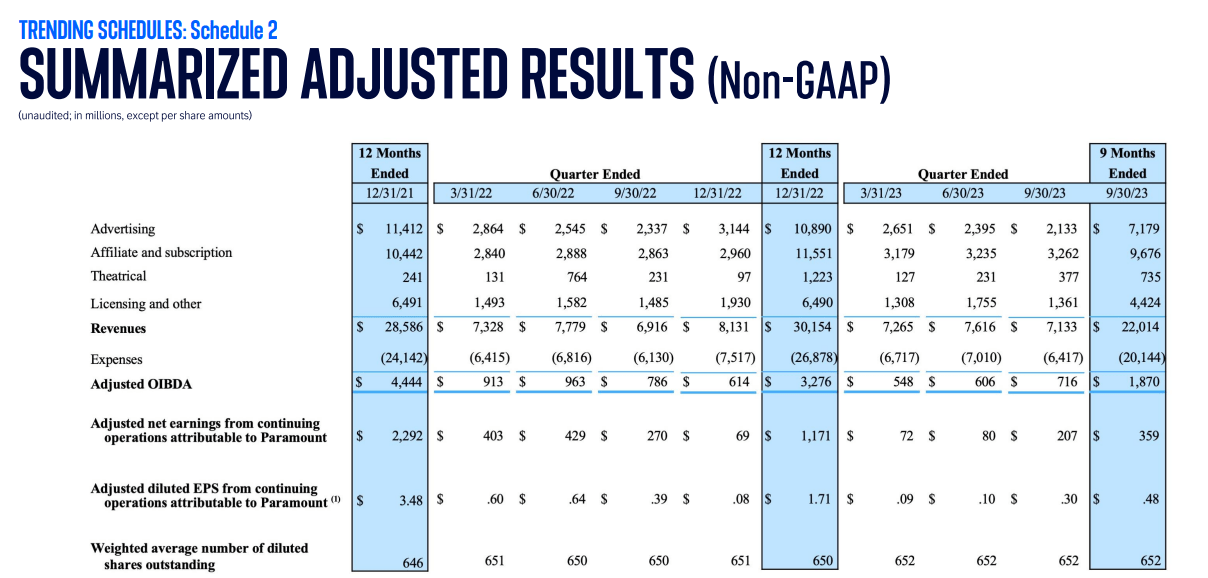

Despite those revenue gains and the beat on the top and bottom lines, the earnings capacity remains anemic. 30 cents a share of adjusted earnings only looks good if you forget where you came from. You can see the drop below from 2021 where the company generated $3.48 of earnings and compare that to the 48 cents generated in the first nine months of this year.

{kind=link}

PARA Q3-2023 Presentation

Advertising revenues were particularly soft as the quarter over quarter and year over year numbers showed the challenges facing the non-Direct To Consumer model. Still the market reacted with some euphoria on the results, suggesting the worst may be priced in.

Outlook

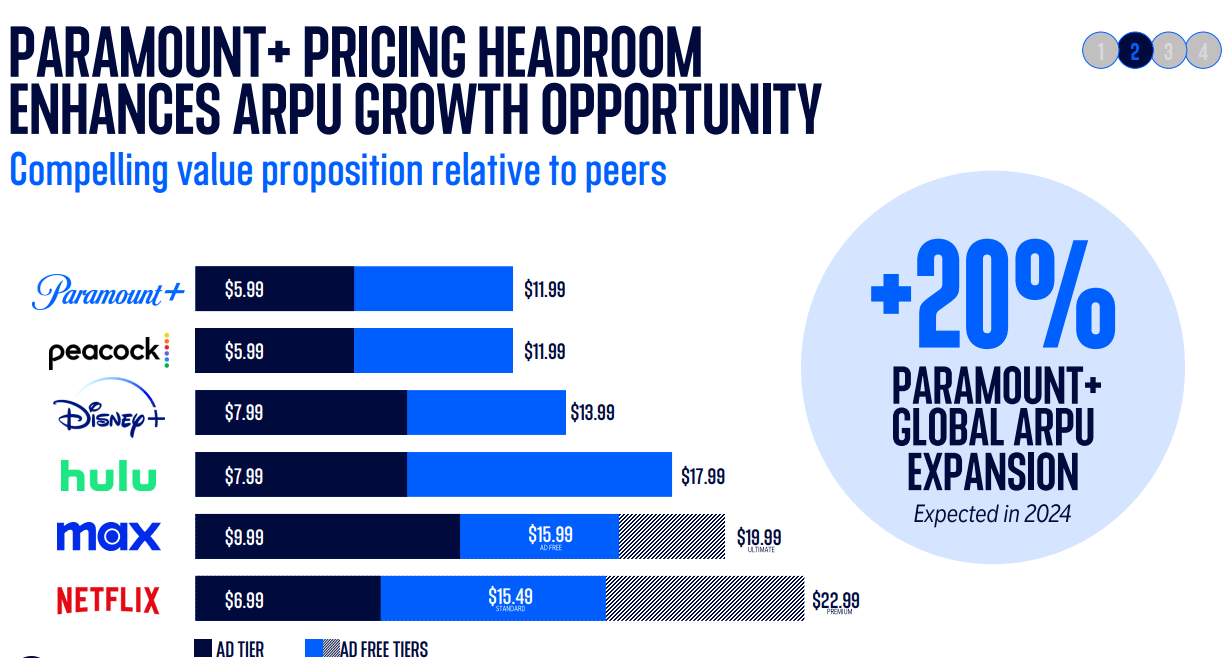

Peak losses. That was the key theme that drove the PARA rally. Management now expects that the direct to consumer model is past the point of maximum pain and the losses should reduce from here. Of course, PARA is profitable now, so that would underpin an improving overall earnings outlook as growth continues. Streaming is likely to be extremely competitive, but PARA has a lot of room to combat the pressures. Its pricing remains low compared to the big boys. The $5.99 ad supported tier looks like an easy addition for any household.

PARA Q3-2023 Presentation

Disney+ ( DIS ) and Netflix Inc. ( NFLX ) are way ahead on their pricing and PARA could increase revenues substantially by just small price hikes.

{kind=link}

PARA Q3-2023 Presentation

Any media firm thinking really long term has to see the value proposition here for PARA. It is cheap and worth acquiring.

Selling At A Fair Price

One of the biggest issues in investing is price anchoring. People are attached to their cost basis or what number they thought they should sell out at. This is what makes logical choices harder. The top-tier management of PARA is no-doubt still having fond memories of the time the market felt it was worth over $60 billion in equity value.

They did not sell then. Would fighting for a 50% premium in a sale today, on top of this rally, which would give them a $17 billion figure, be worth it? It is hard to be objective about these things and you can put this alongside sunk-cost fallacy. But there are signs that management is seriously considering this. Their tone on their losses and focus on reduction of leverage shows that they are not at all sanguine on their prospects if the economy hits a bump down the line.

Moving on to free cash flow. Free cash flow in Q3 was $377 million, and we expect strong free cash flow in Q4 as the strike continues to limit the production of content. Some of the programming changes we've made in response to the strike will be sustained, resulting in lower steady-state production spend and improved cash flow across the two year period of 2023 and 2024, which will also benefit leverage.

We also closed on the sale of Simon & Schuster earlier this week, which generated approximately $1.3 billion in after-tax proceeds. These proceeds will improve year end net leverage by approximately one-half turn.

Today, we announced a $1 billion tender offer for some of our upcoming debt maturities. Not only will this reduce gross debt, but it will extend our maturity profile thereby enhancing financial flexibility. Additionally, next year, the full year benefit of the dividend reduction, together with our expectation for growth in total company earnings will improve leverage even further.

Source: PARA Q3-2023 Conference Call Transcript

We still think fair value is close to $30-$35 today and the noise in the stock price does not change that. We need very modest enterprise value to revenue multiples here to make our case. PARA would trade well under 1.5X even if the buyout was at $30.00 and you compare that to where NFLX is currently perched.

The counterpoint is that it will be difficult to perhaps get there, as even the counterparty is going to have a price anchoring of sorts. No one wants to be the person who paid a 100% plus premium for a stock, especially if things don't ultimately work out. But we did actually see one recent buyout, albeit in a different sector, at a massive premium.

{kind=link}

Seeking Alpha

So maybe there is hope for the long suffering bulls.

Paramount Global 5.75% SR A MDR CON PRE 01/04/2024 ( PARAP )

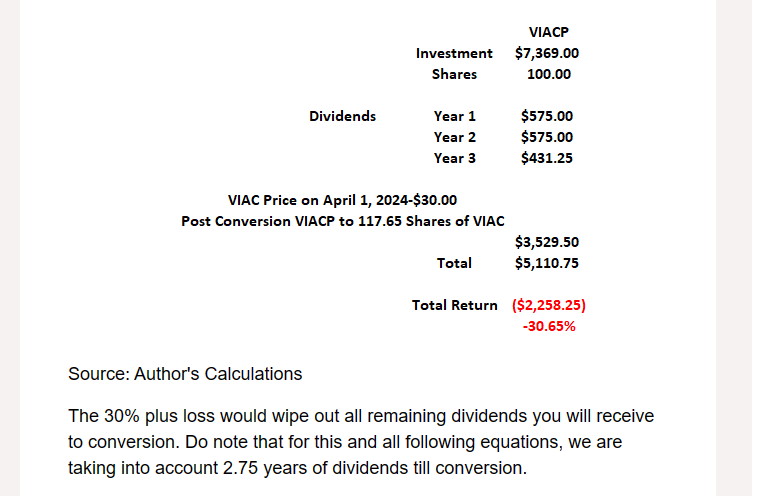

The report would not be complete without touching on the mandatory convertible shares. We had repeatedly warned about the huge premium built into these as dividend chasers ignored the mandatory convertible nature. For example, in 2021 we warned that the piper would be paid for yield chasing and even if PARA (then known as VIAC) would land at $30.00 (coincidentally where we think this saga could end) you would nurse huge losses on PARAP.

{kind=link}

ViacomCBS Preferred: Return Free Risk

PARAP shares have now converged on that reality and delivered really poor returns from that point. How do they fare from here? Well, if there is no deal and the prices remain flat until conversion, they are not too badly priced at $22.64.

{kind=link}

Author's Calculations

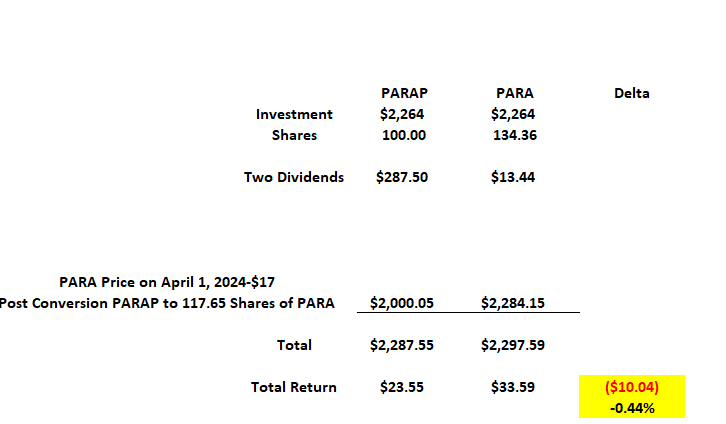

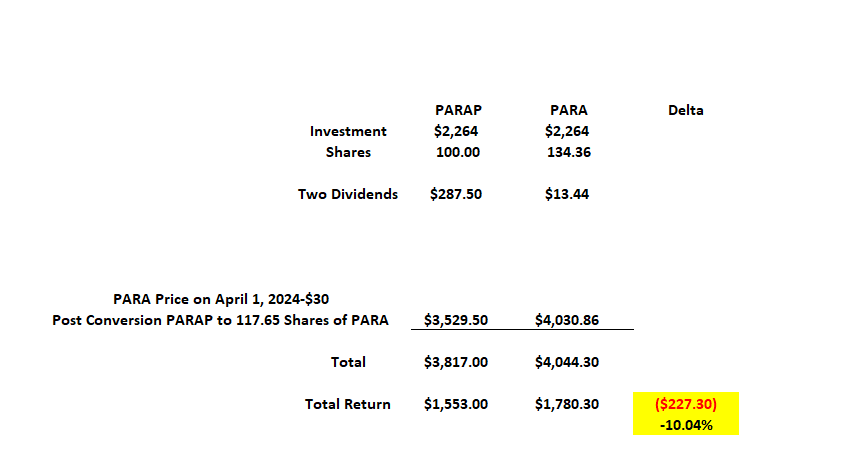

But what if there is a deal? Interestingly enough, PARAP shares remain an awful choice in that case.

{kind=link}

Author's Calculations

Why such a divergence? Well PARAP is getting its return profile till April, 1, 2024, via big dividends. Those don't move up higher if there is a buyout. So PARAP only makes sense to hold till then if you don't expect a bid for PARA. If you expect one, trade out and buy PARA.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Paramount Global: The Mission Impossible Of Selling At Fair Value