PARA - Paramount Global: Time To Turn Bullish

2023-12-31 12:00:00 ET

Summary

- Paramount Global's shares have been rising on rumors of a potential sale or merger in recent months.

- The company's Q3 earnings beat estimates, with improved revenues and bottom-line performance, signaling a positive outlook for the future.

- Paramount's streaming business is gaining momentum, with increased DTC revenues and subscribers, and plans for expansion, making it an attractive investment.

Shares of Paramount Global ( PARA ) have been on the rise in recent months on rumors that the company could be sold or merged with one of its competitors. While there’s no clarity about what’s going to happen next, we could assume that the worst for the company is likely behind it. While the rumors a bout the deal could certainly continue to push the shares higher, the expected improvement of Paramount’s own business in the future also makes the company an attractive investment at the current price.

More Upside Ahead?

Paramount reported decent earnings results for Q3 last month, which could indicate that the worst for the company is finally behind it. After underperforming last year and at the beginning of this year, the company’s revenues in Q3 beat the street estimates by $10 million and were up 3% Y/Y to $7.13 billion. At the same time, the improvement of the bottom-line performance and the expectations of a strong cash flow next quarter should help the business retain its momentum.

The rise of DTC revenues by 38% to $1.69 billion and the rise of Paramount+ subscribers by 2.7 million to 63 million in Q3 signal that the streaming business is finally picking up momentum. The company now believes that the DTC losses are expected to be lower in the future, as the OIBDA losses narrowed by more than 30% in Q3, and the streaming business is now on the path to profitability. To continue to grow, the company is looking to launch an ad-supported version of Paramount+ in different markets, release Paramount+ Essential on Amazon channels in the United States, and expand its global footprint by working with local partners to launch Pluto TV across different regions.

All of those growth catalysts could certainly help Paramount retain its momentum and continue to exceed expectations in Q4 and beyond. What’s more, is that the company is also improving its debt situation. Considering that at the end of Q3, Paramount had only $1.8 billion in cash reserves and $15,6 billion in long-term debt, it made sense for the company to use the net proceeds from its sale of Simon & Schuster for $1.62 billion last month to pay down some portion of its debt. On top of that, the $1 billion tender offer that was announced last month should also help Paramount to reduce its debt and extend its maturity profile, which could make its shares a more attractive investment.

In addition to the growth of the core business and an improvement of a debt profile, Paramount could also become a great M&A play for a lot of investors. At the beginning of this month , it was reported that Apple ( AAPL ) is interested in bundling its own streaming service with Paramount+, which could lead to a boost in the number of subscribers for both services in the future in the future. At the same time, there is news that Skydance Media is raising a war chest to acquire Paramount’s assets in the coming months. In addition to that, there are reports that Warner Bros. Discovery ( WBD ) is aiming for a merger with Paramount as CEOs of both companies held a meeting last week to discuss a potential deal. Considering that Paramount’s streaming business has finally gained momentum and advances on the path to profitability, there’s a chance that we could see a bidding war happening in the foreseeable future given all of those reports.

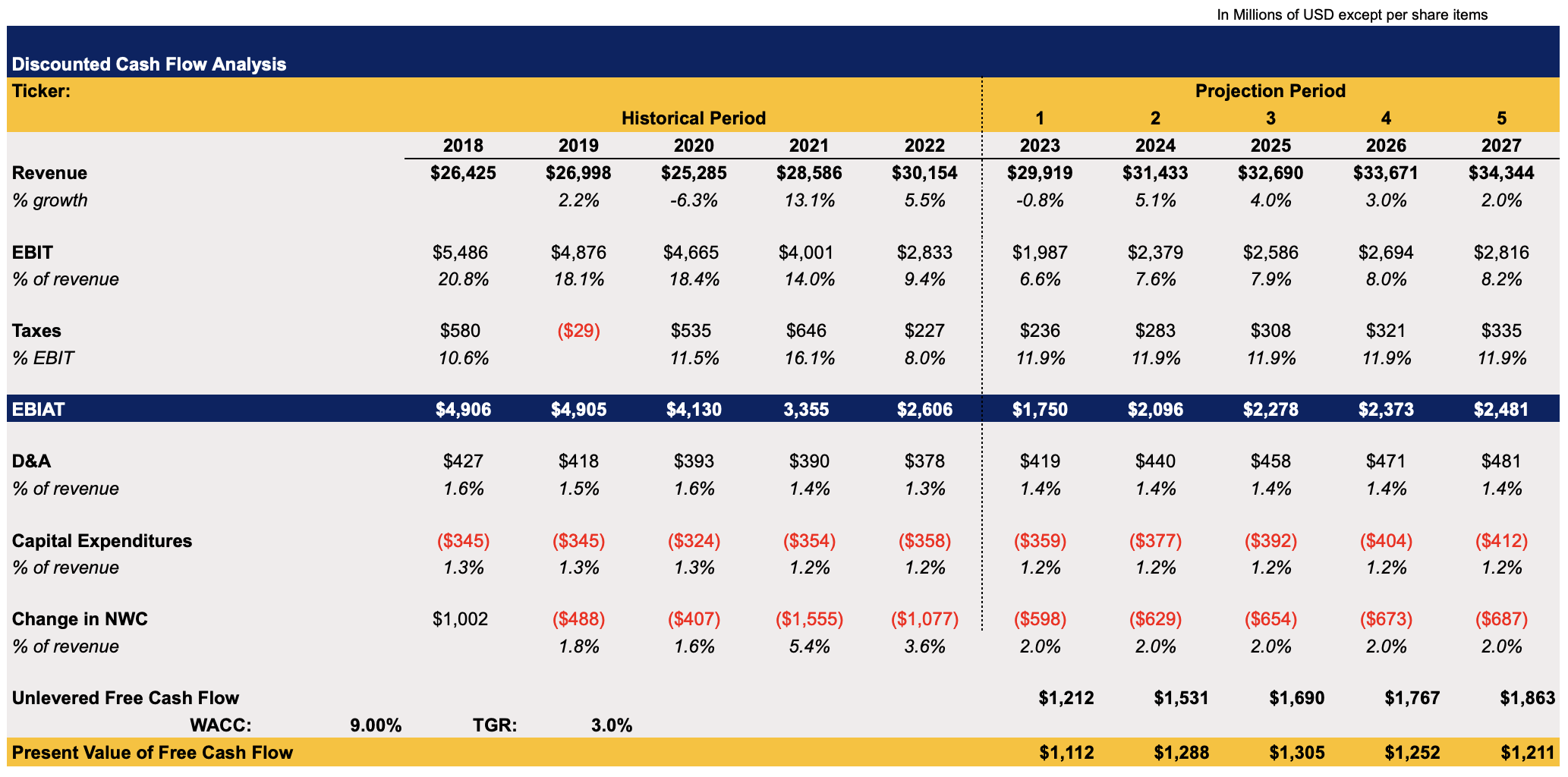

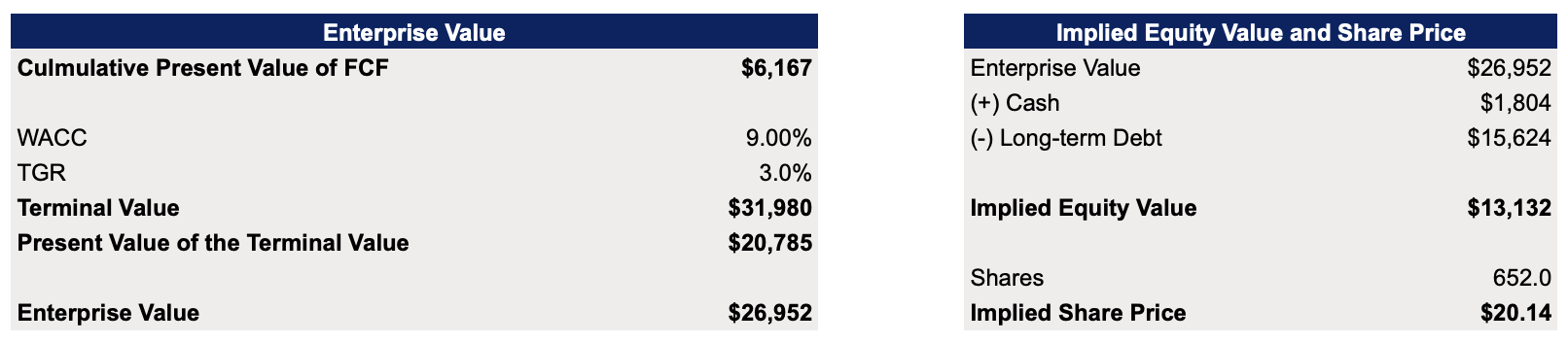

To figure out how big is Paramount’s upside given all of those developments, I’ve decided to create a DCF model that can be seen below. Most of the assumptions in the model are either closely aligned with the street estimates or in-line with the historical performance. The WACC in the model is 9%, while the terminal growth rate is 3%.

Paramount's DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

{kind=link}

The model shows that Paramount’s enterprise value is $26.9 billion, while its fair value is $20.14 per share, which represents an upside of over 30% from the current market price. If any type of deal to sell assets is made, then it’s likely that the company would be valued at over $20 per share. After all, Paramount itself has been trading at over $20 per share earlier this year, so such a premium is not unreasonable given the decent performance of its business in the latest quarter.

Paramount's DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

{kind=link}

Major Risks To Consider

Despite being undervalued and having several growth catalysts going for it, Paramount’s business could still underperform in the following quarters which could lead to the depreciation of its shares. Earlier this year, some reports stated that a quarter of adults from the United States canceled their streaming subscriptions due to the rising inflation. While recently we’ve entered a disinflationary environment and are on track to have a soft landing, it could still take a while to fully tame the inflation.

Given the competitive theatrical and streaming landscape along with the current macroeconomic environment, Paramount is always at the risk of underperforming against others, especially when it’s exposed the most to external factors in comparison to its much larger peers. It’s no surprise that Paramount has the lowest ARPU of $6.11 per month among its competitors due to its smaller size, which leaves little margin for error. That’s why even $60 million in strike-related idle costs is a big deal for a company of its size.

It’s also important to note that there’s no guarantee that any deal will be reached, and some assets will be sold in the foreseeable future. Earlier this year Paramount already rejected a more than $3 billion deal for its Showtime assets to its former executive and a similar situation could happen again. Any news of no deal is more than likely to negatively affect the performance of Paramount’s shares in the short-term as those investors who are betting on the deal happening would unwind their positions and look for other M&A opportunities.

The Bottom Line

While there are certainly major risks to Paramount’s growth story, the company nevertheless has decent catalysts that could help its shares to continue to appreciate in the near-term. If any type of deal is announced, Paramount would be able to quickly realize the shareholder value and create decent returns for its investors. If there’s no deal, then the company would still be able to create additional shareholder value over the longer term thanks to the expected improvement of its business in the future.

For further details see:

Paramount Global: Time To Turn Bullish