PARAP - Paramount Global: Upside Potential On Turnaround To Earnings Growth

2023-07-10 09:51:10 ET

Summary

- PARA has continued to struggle after announcing poor Q1 results that also came with the announcement of a dividend cut.

- The dividend cut should help their balance sheet, and it wasn't too surprising since they were running negative FCF anyway.

- Management expects to be FCF-positive next year, and their DTC business continues to grow sales rapidly with strong subscriber growth for Paramount+.

- I also share an update on writing puts with a trade that recently expired worthless, locking in the options premium.

Written by Nick Ackerman. A version of this article was included in our Cash Builder Opportunity weekly options expiration update originally posted on July 7th, 2023.

Paramount Global ( PARA ) continues to struggle. I'm remaining long the position even with the skinnier dividend announced with the rather ugly Q1 earnings announced. The future should be brighter, at least if management can deliver on their expectations. However, this is clearly not the type of investment that will be right for everyone.

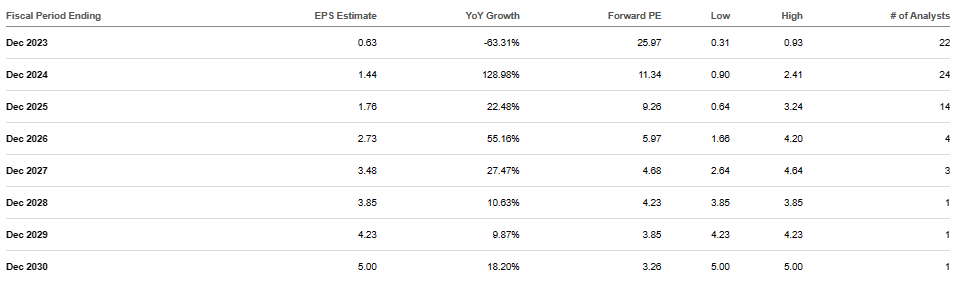

One of the main problems is the outlook for PARA continues to look pretty shaky and get gloomier as analysts have revised earnings expectations lower once again since our previous update. Analysts expect EPS to come in at $0.63 for fiscal 2023.

PARA EPS Estimates (Seeking Alpha)

{kind=link}

That's down from the $0.83 in earnings previously. It helps illustrate why the dividend needed to be cut in the first place, as they continue to sink billions into content for their streaming platform.

The 2024 year is expected to be the year they begin to turn things around. At least in terms of profitability and providing FCF. However, even that went to a gloomier outlook, with EPS anticipated to come in at $1.44 - a decline from the $1.67 estimates from earlier this year.

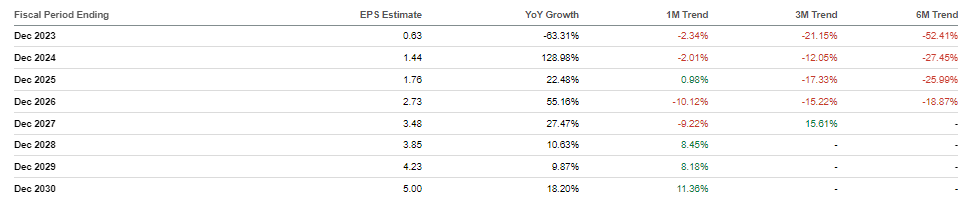

These weren't minor downward revisions either, but material cuts to estimates, and this has been going on for several years now hence, why the stock has been on a long struggle.

PARA Earnings Revisions (Seeking Alpha)

{kind=link}

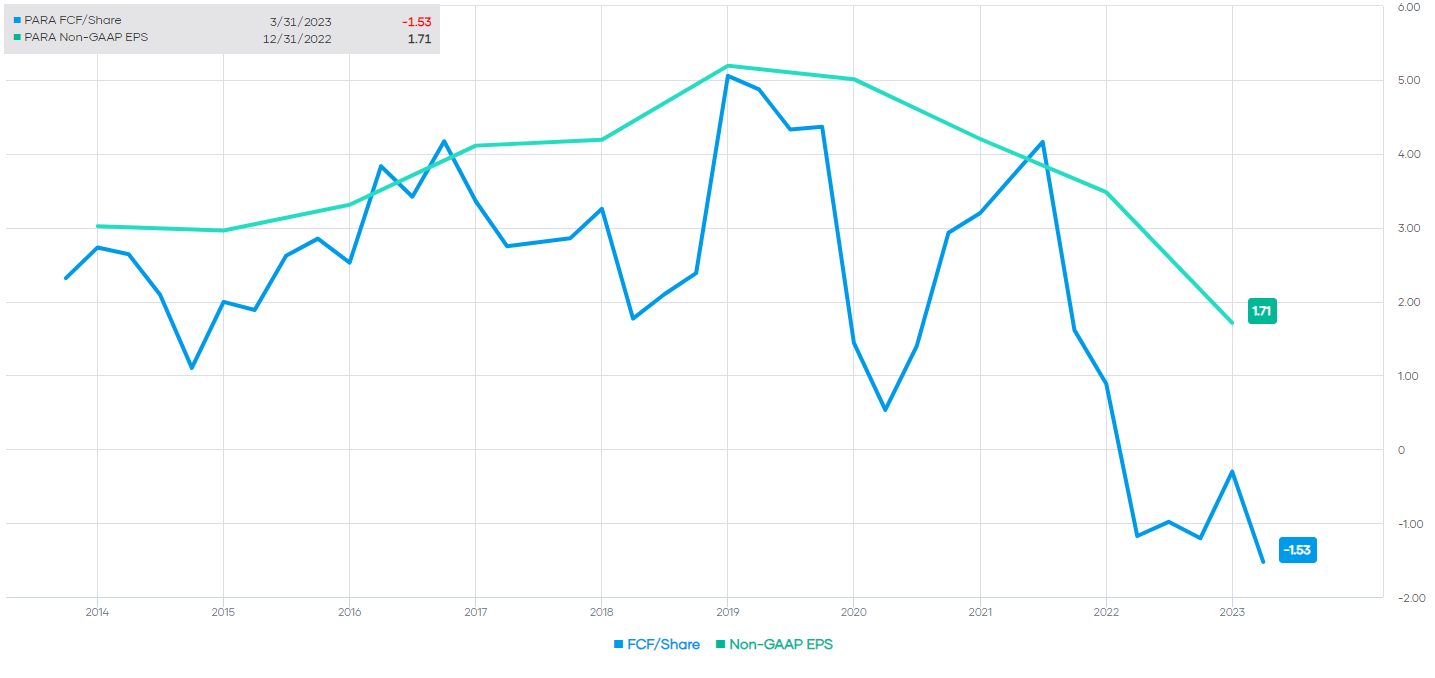

This all further reflected the need for the dividend to be cut as the company has gone free cash flow negative in the last couple of years.

PARA Earnings and FCF Per-Share (Portfolio Insight)

{kind=link}

Again, as they look to spend an intense amount of cash on their streaming business.

That said, their CEO has continued to believe, even in the latest earnings call, that they will be free cash flow positive by 2024.

With the robust content engine at the core, all-in service are delivering long-term value to our shareholders. We are also navigating a challenging and uncertain macroeconomic environment. And you see the impact of that in our financials, as the combination of peak streaming investment intersects with cyclical ad softness. All of this makes us even more focused on making the necessary decisions to return the company to earnings growth and positive free cash flow in 2024.

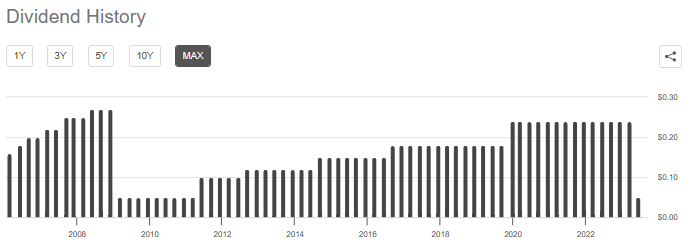

I believe that is what gave them the confidence to have any dividend at all, and they potentially wanted to keep income investors or funds that can only invest in dividend payers on board. With a dividend yield of 1.23% these days, it certainly isn't going to be included in any "high yield" type portfolios, but it is better than nothing. If earnings expectations and FCF is hit next year as expected, that could open them up to potentially raising their dividend. A dividend cut and then subsequent raises aren't out of the question for this company. That's what happened after the GFC.

PARA Dividend History (Seeking Alpha)

{kind=link}

However, before getting too optimistic, it should be considered that the environment is quite different. Streaming is much more competitive and less profitable than legacy television-basically, with too many players vying for limited eyeballs. People easily switch up and cancel streaming services as their programs come and go. Not to mention that a recession is expected as the Fed continues to increase interest rates. A weaker economy could leave consumers weaker.

That being said, I've thought that streaming services would be a cheap enough form of entertainment that might not be as impacted. Nonetheless, only time the next recession will give us a better idea as it'll really be the next recession that tells us how streaming services are impacted. The Covid pandemic recession doesn't count because it was short-lived, and with people stuck at home and given cash, consumers had plenty to spend with nowhere to go.

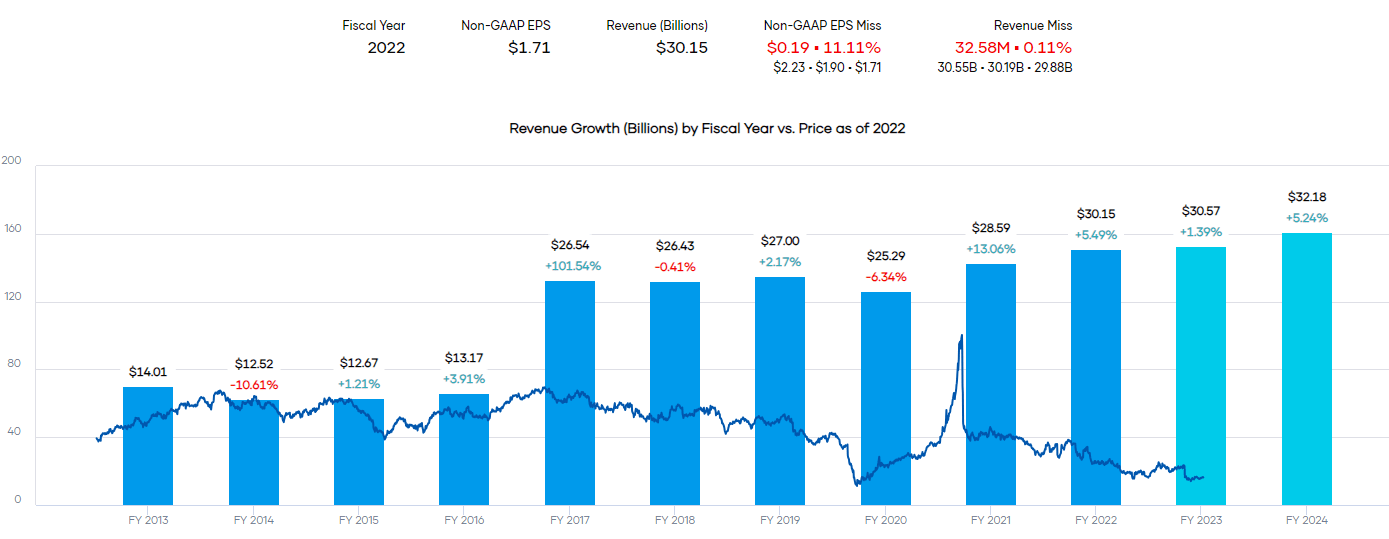

We can also see that revenue has been trending upward despite profitability coming down.

PARA Revenue and Forward Estimates (Portfolio Insight)

{kind=link}

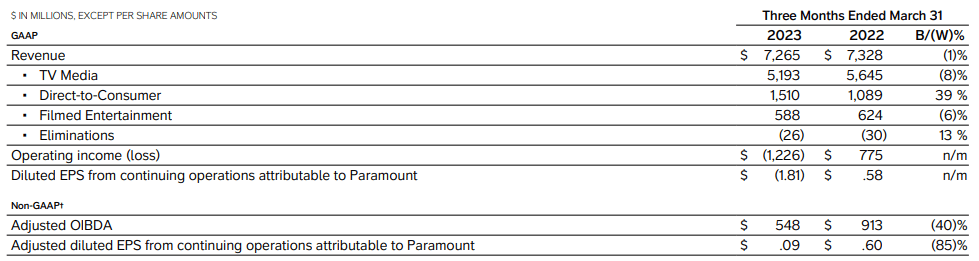

Their traditional TV Media segment continues to decline. It's the largest part of their business, so it has a big impact. However, what they lose on the TV Media side they are offsetting some through revenue growth in the Direct-to-Consumer segment.

PARA Q1 Results (Paramount Global Investor Presentation)

{kind=link}

Year-over-year, they grew the revenue of Paramount+ by 65% with strong subscriber growth. Their DTC also included Pluto TV and Showtime, which was now merged with Paramount+. Noggin and BET are also included in the DTC. Overall revenue increased 39% year-over-year for that segment. With TV Media being such a large part of their business, though, it still meant a year-over-year 1% decline in revenue overall for the company in the first quarter.

It's just the unfortunate fact that due to massive spending, the DTC side of the business is unprofitable.

PARA DTC Segment Earnings (Paramount Global Investor Presentation)

Analysts Outlook

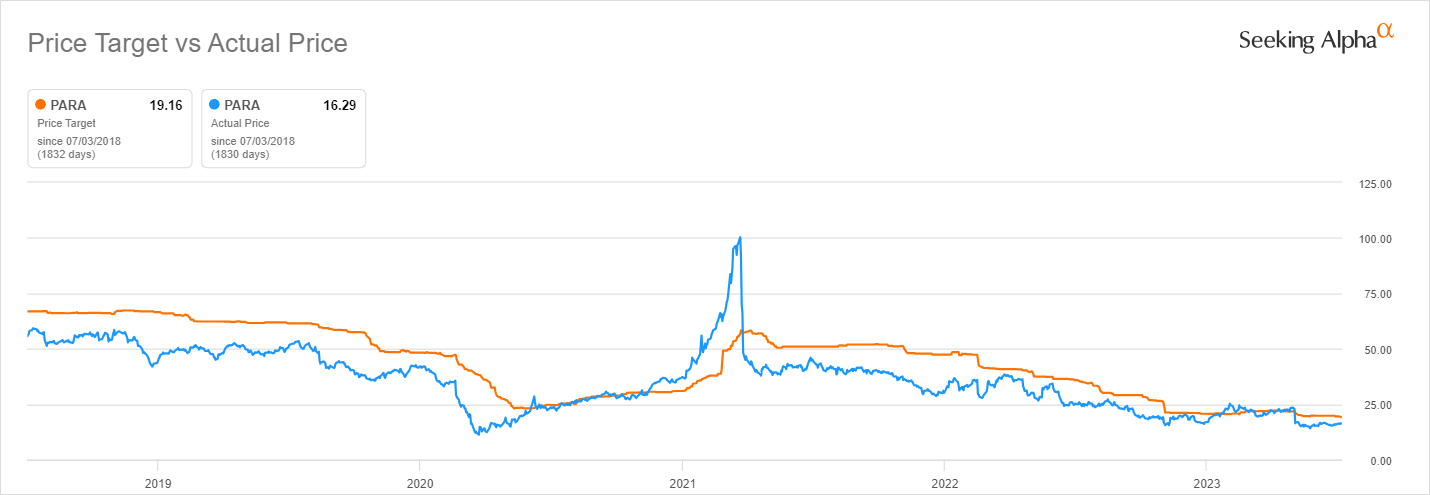

Analysts have an average price target of $19.16 for PARA. Naturally, as the expectations for earnings have come down for this company, so too has its price target. With the latest dive, it would appear that they were slow to cut their price target, but there have been some downward moves.

PARA Analyst Price Target (Seeking Alpha)

{kind=link}

Overall, rate the stock a "Hold." Analysts seem to be just as conflicted on what to expect for PARA as the retail crowd, as there are fierce defenders of this stock and those that are highly opposed to even suggesting PARA is a worthwhile speculative play.

PARA Analysts Rating Breakdown (Seeking Alpha)

Recently, Wolfe downgraded PARA from "Peer Perform" to "Underperform. They have a price target of $14.

Divestitures And The Acquisition Rumors That Never End

They also noted that they are continuing to divest non-core assets in their last earnings call too.

And to that end, we continue to hone our cost structure, align resources with growth areas, and divest non-core assets, because at the fundamental level, our strategy is working, and our momentum is strong. We are producing popular content, adding subscribers, increasing engagement, growing streaming revenue, and progressing towards key business objectives.

That's been an area where they've continued to try to shed business and a place where news for PARA keeps showing up. BET and Simon & Schuster are the primary targets. The company is also looking to sell a majority stake in Noggin, which would keep them a partial owner. Simon & Schuster is something they've tried to sell in the past, but it ultimately didn't lead to a deal. As a publishing business, it doesn't fit with their video approach.

However, the latest news was that the BET sale could be "in trouble as the likely leading bidder is balking at the sale price."

For quite a while now, the biggest bet on PARA was that it would be a great acquisition target. That seems to be the angle that never dies either, as a Wells Fargo analyst reiterated the potential for such a deal last month. This came after a report that Netflix ( NFLX ) "may have looked at buying" PARA at some point. They expect the company to break up and sell off in pieces.

However, Shari Redstone has kept the company hostage as the controlling shareholder. A sale can't be made without her approval, as she controls around 80% of the voting stock. Unless Warren Buffett can nudge something along, the acquisition path appears to continue to be blocked for now.

How I've Been Using Options With PARA

After they reported those ugly earnings with the dividend cut, the shares sunk rapidly. I took advantage of that move by selling some $14 puts with a June 9th, 2023 expiration. I took in $0.31 in premium (making up for the dividend cut and then some), and then that's where our June 5th, 2023 trade comes in. At that time, we closed those original puts for $0.04 and collected another $0.35 for a net premium of $0.31.

Returning to the original May 4th, 2023 trade, there was only a brief period where the price nearly broke the $14 strike price. However, after that, it recovered significantly before ending up flirting around the $16 share price level.

We could have let that previous trade expire instead of closing and "rolling." The trade didn't need to be rolled, but essentially I was "reloading" a very similar position but not taking the risk that during that week, shares would crash, and I could potentially be stuck with more than I intended. So I was being cautious by closing out the previous position before writing more puts.

Either way, in this string of trades, we've collected $0.62 in total premium as this series ends. One of the ideas behind writing more puts was to increase the position's size potentially and do so at a much lower price than our original assignment, therefore decreasing our breakeven by averaging down. With no assignment but premium still rolling in, we are still squeezing some extra cash out of PARA, nonetheless, and you could think of it as a bit of an indirect way of reducing your breakeven.

I was originally assigned puts at $21 a share last year, with the breakeven at $20.42 due to collecting a $0.58 premium in that original trade. No doubt, not one of the better positions to be in, but maybe some solace can come from the fact that Warren Buffett is still sitting in this name, too. It's unclear why Warren Buffett's Berkshire ( BRK.A )( BRK.B ) owns a large stake in PARA, as he isn't quite sure either with a "we'll see what happens" response. He has mentioned that streaming isn't a good business.

We actually started playing the PARA options writing almost exactly a year ago. Looking back at all the trades, our first trade with this name was on June 28th, 2022. We've netted $2.26 in premium over 10 trades, including this last trade. This includes writing puts to potentially average down, and it also includes writing covered calls when the opportunities present themselves.

The only assignment that I've taken was with the September 30th, 2022, expiration. During that time, it means there was another $0.53 in dividends collected during this time too. So still underwater on this one despite these premiums and dividends, but it's a good example of how writing options can mitigate losses.

Conclusion

The idea of investing in PARA would be that they can return to being cash flow positive and participating in a streaming platform that can become profitable and continue to grow. Streaming that would be profitable enough with enough sales to offset the declines in their legacy TV business eventually. Cutting their dividend did free up more cash for them to strengthen their balance sheet as they continue to invest heavily into their streaming platform.

The side speculation can be an acquisition eventually, but that doesn't seem too likely, given the control of PARA.

Q2 earnings will be coming up and are expected in early August. That will give us some more color on what has been happening in the latest quarter with PARA. We'll see if streaming has kept up its strength in revenue and subscriber growth. It should also give us some further idea if management expects they can still be cash flow positive by next year. Every quarter that ticks by, we should be able to gain more clarity.

For further details see:

Paramount Global: Upside Potential On Turnaround To Earnings Growth