PFE - Pardes Biosciences Seeking Strategic Alternatives

2023-05-17 19:43:06 ET

Summary

- Pardes Biosciences Seeking Strategic Alternatives.

- Pardes’ Pipeline is depleted.

- All-Star management team in place.

- Significant cash available.

Pardes Biosciences Seeking Strategic Alternatives Could See Consolidation

Pardes Biosciences ( PRDS ), which said in its recent release of topline clinical trial results that it failed to meet its primary endpoint, is faced with a questionable pipeline, in my opinion, and has a need to find a path forward.

There are some obvious and not so obvious options that will be discussed. Their leading candidate, Pomotrelvir, was tested in standard risk adults that contracted mild-to-moderate COVID-19. The primary endpoint was the proportion of the treated group that was PRC negative in comparison to the untreated group. The company’s top line results showed a 70% undetectable level in the active arm versus a 63% undetectable level in the placebo group. These results show no meaningful statistical improvement over placebo, so they suspended development of the drug and are now looking to “explore a range of strategic alternatives.” The company has a significant amount of cash,~ $172.4 million, with nominal debt at the end of Q1, and a broken pipeline. How will they utilize their cash? Alternatives include, going private, an acquisition, or in-licensing of a new product. Is this the key to their future? The company’s market cap is discounted at $120 million, because it trades for about 23% discount to its cash value. In-licensing of another promising antiviral candidate might make the most sense. Given the evolving competitive landscape and management’s ability to apply lessons learned from failed trials, applying those lessons to a new trial in COVID where they have significant experience may be the best approach to success.

Pardes’ Pipeline Lost Appeal

At its peak in January 2022 PRDS had a market cap of $929 million and it has gone down every successive quarter until it settled at a low of $90 million market cap. The company was developing a novel 3CL protease inhibitor that was similar in function to Pfizer’s 3CL protease inhibitor called Paxlovid. There are a number of 3CL inhibitors and competitors; Pfizer ( PFE ) is the largest, then Shionogi ( OTCPK:SGIOF ), Cocrystal ( COCP ) with its P1 study, and Todos Medical ( OTCPK:TOMDF ) with its P2 hospitalized patient drug and dietary supplement, which users take for acute COVID and Long COVID. There are also some earlier stage 3CL protease inhibitors that are promising from companies like Exscientia ( EXAI ) who is in joint development with Scripps. From a mechanistic point of view, Todos has a 3CL and a CCR5 inhibitor packed into one molecule which may give them an advantage if the viral mutations expand to the protease.

3CLpro Target Becoming Problematic

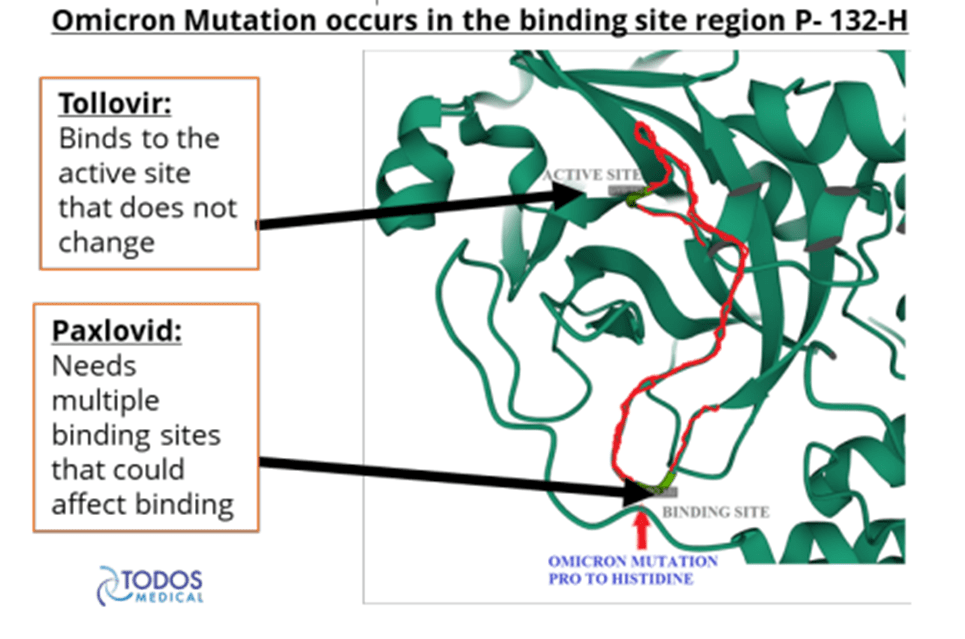

There are hints that Paxlovid is losing efficacy possibly due to mutations forming on the 3CL protease which affect the binding site for Paxlovid. One study developed a map of the hot spots likely to lead to Paxlovid resistance . Todos Medical is suggesting that their drug Tollovir, along with the nutraceutical, Tollovid, may not be susceptible to these mutations. But for most 3CL protease inhibitors, the future doesn’t look as rosy because of the mutations.

{kind=link}

Todos Medical Presentation Slide 20

A more recent study showed evidence that Paxlovid and Japan’s new 3CL inhibitor, Xocova, are indeed losing their effectiveness . Now there are other 3CL protease inhibitor companies, like Sorrento (SRNEQ), which has a drug called Ovydso. This is a Cathepsin L Inhibitor like the Nirmatrelvir component in Paxlovid. While there is a strong argument for the continued development of more 3CL protease inhibitors, the useful one needs to be effective against mutations. Pomotrelvir was supposed to target the conserved region of the 3CL protease, but it simply didn't work well enough. Enanta ( ENTA ) has a promising fast tracked 3CL protease inhibitor that expects a phase 2 readout in May 2023. They call themselves the best in class due to their high micromolar binding and bioavailability, but this needs to be proven in the clinic.

Pardes suspended further development of the drug in light of a failed trial, but it still might be considering the asset valuable for a sale or business development. Early on, Pomoterlevir was widely touted a potential pandemic ender. To most investors the trial appeared to fail abysmally, but experienced biotech analysts might have a different view. It is my opinion that enrolling vaccinated patients without risk factors 5 days after the start of symptoms seems to be a mistake because those with a healthier or younger immune system or prior immune activation from vaccination/exposure may clear the virus faster . Additionally, some laI believe that they must get the drug to people earlier in the disease state, because many healthy and/or vaccinated patients may start improving within a few days. This, in theory, limits the time window to detect a meaningful difference in viral load, though the magnitude of effect or likelihood of making a meaningful difference in measured efficacy in the study is difficult to ascertain. Regardless, Pardes didn’t follow Pfizer's lead which was to treat patients with at least one underlying medical condition. They treated standard risk patients which may have created too high of a hurdle for the treatment.

Next Steps

Pardes has a few options to choose from to create shareholder value. First and most simply, they could dissolve the company and issue a special dividend for their cash value at the end of the quarter of $2.54/share discussed later in the financial analysis. This would give shareholders roughly a 23% premium above the current share price, but it would be a big disappointment considering the IPO price was $10 in 2021.

The largest fund ownership is with Foresite Capital Management, who owns 27.24% of the company and made a non-binding offer on April 20, 2023 to the board of directors of Pardes to take the company private. They also made it very clear that they were not in favor of “an alternative change of control transaction,” and would vote against any other plan. The letter had all sorts of language to the effect that they would not move forward unless the Special Committee approved it. This is an offer with a lot of contingencies that do no more than act as a big bid from a motivated institution underlying the stock that limits an investor's downside. It is unlikely to amount to anything because there is no takeover price referenced for investors to arbitrage against. Furthermore, the announcement has little to no impact on the stock as it has only moved $.08 or 3.2% higher.

Another option would be for them to redo their trial with at-risk patients and cut down their time-to-treat to about 3 days, instead of 5 days, after infection or symptoms. But perhaps the most lucrative move to reward shareholders would be to in-license another asset.

Pardes has experience and lessons-learned in COVID, as well as, a mission and vision to stop the pandemic and cultivate change in a post-pandemic world. Although companies sometimes reverse merger and completely change as a company, it makes sense for Pardes to use its cash to approach the COVID market, which has ample need for better solutions.

Their 3CLpro target was a good target; however, it might be in the company’s best interest not to focus on a biological target that now has two approved drugs from big pharma, Pfizer and Shionogi. To differentiate themselves it would be better to go after a critical target with a promising drug.

However, when it comes to COVID assets to buy, there are many companies with failed drugs, including Atea Pharmaceuticals ( AVIR ). It is in a similar situation as Pardes, but with a more robust pipeline that is diversified beyond COVID, where they failed. Pardes must not acquire an early-stage asset if they want to regain a strong valuation and put the ~$172 million in cash to use in a timely manner. While the options grow thin when considering this, there is one very successful P2/3 ready asset called ProLectin-M that has shown significant promise in clinical trials. The drug achieved an 88% responders rate by day 3 against 0% in the control. Their peer-reviewed article was released in the past month. This asset is owned by Bioxytran, Inc. ( OTCQB:BIXT ) which has gone on record indicating that they are looking for joint ventures with companies with weak or failed pipelines and healthy balance sheets.

All Star Management Team

Pardes has a who's who management team. It is highly likely that they could absorb another asset, sell the company, or even do a licensing deal.

The CEO, Tim Wiggins, is a successful biotech entrepreneur. Before agreeing to head Pardes he was had a huge win when he sold Demira Inc., with its atopic dermatitis drug, to Eli Lilly ( LLY ) in 2020 for $1.1 billion. The irony is that he started his biotech career at Eli Lilly. After Eli Lilly he served as CEO and Chairman of the Board of Directors of Peplin Inc. until the acquisition by LEO Pharma A/S in 2009. He also has served as CEO and Chairman of the Board of Directors of Connetics Corporation and in various other executive positions at CytoTherapeutics Inc. and Ares-Serono S.A.

The Chief Development Officer, Brian Kearney, is antiviral drug development veteran with 2 decades at Gilead Sciences ( GILD ). One of his accomplishments is the HCV treatment SOVALDI ® . His contributions were key in the approval of 15 new drugs. The Chief Commercial Officer, Sean Brusky, was head of healthcare delivery for Genentech (Roche Group) and was in business development at Vertex Pharmaceuticals ( VRTX ). Rounding out this incredible team is Ann Kwong who has been a strategic contributor in development of multiple antiviral compounds at Vertex in their HCV program and influenza program. She has numerous accomplishments in virology.

With the depth of knowledge they have, this team could seemingly overcome any obstacles thrown at them, including a failed clinical trial.

Financial Analysis

The company has issued 1.72 million shares out of 250 million shares authorized. The company was initially capitalized with $275 million in PIPE investments. As of the annual report, the company has $200 million in cash and short-term investments. In the course of a year the company burned $75 million only to find that they needed to abandon development of their COVID therapeutic. Their current cash and short-term investments totaled $172.4 million at the end of the first quarter indicating they burn a little over $25 million quarterly.

While not explicitly stated in the last press release, this highly capable management has likely suspended hiring and initiated layoffs to right size the company while they figure out their next moves. At the end of Q1 they had $7.7 million in accrued expenses which is likely the result of restructuring costs in the form of salaries, severance, and other expenses. Since R&D represented approximately 70% of the costs, it's reasonable to think the company cut their quarterly burn to about $7.5 million quarterly and has ample cash to properly evaluate any strategic alternatives. The end of Q2 cash estimate is $157.2 million which factors in an elimination of accrued expenses and the estimated $7.5 million quarterly burn. This works out to $2.54 in cash.

Investment Summary

While there are a number of strategic alternatives, one promising path seems obvious. Pardes has an All-Star management team with a mission statement displayed on their homepage; stop the pandemic and cultivate a post-pandemic world. This team isn’t likely to let the hiccup of a failed trial defer their overall mission. Investors should expect them to stay true to their mission with another COVID asset with more potential than the last. While the list of viable therapeutics is short, those that remain are unique, differentiated therapeutics of high quality. Their current market cap is under $120 million and is trading approximately $37 million below estimated Q2 cash. The downside risk of loss of market cap is low if management takes swift and decisive action to stem the outflow of cash and rebuild the company with a new asset.

A healthy biotech company needs three key things: 1) great technology, something that is unique and valuable, 2) a great management team that can take the treatment through the FDA maze to completion, and 3) capital. Pardes really only needs a promising technology at this point. If they can get their hands on a good asset, the stock should respond accordingly and should at least give the company a neutral or positive enterprise value. This is a speculative investment with a relatively small downside risk due to the cash position.

For further details see:

Pardes Biosciences Seeking Strategic Alternatives