META - Patience Is The Name Of This (Market) Game

2023-09-24 03:32:10 ET

Summary

- Market weakness continues due to concerns about the Federal Reserve and interest rates.

- Energy sector is showing signs of strength, with oil prices rising and potential for above-market returns.

- Market weakness during earnings "quiet periods" may present buying opportunities, as strong business fundamentals persist.

Brian Dress, CFA -- Director of Research, Investment Advisor

Is anyone else tired of talking about the Federal Reserve?

After reading back last month’s newsletter, it seems like we will be singing a familiar tune for you again this week. Market participants continue to be concerned about the Fed and interest rates; it seems to the exclusion of almost anything else happening in the market. Of course, in this month’s newsletter, we will address the happenings at the latest Federal Reserve meeting. But as we have tried to do over the past couple years, we want to make sure we keep our focus on what really matters, the underlying businesses that comprise the stock market – a market of stocks.

As we referenced in last month’s Amidst Rising Rates, Don't Forget About Growth! , the negative relationship between interest rates and stock prices remains extremely strong. As we have seen the 10-year US Treasury rate continue to rise, now near to 4.50%, stocks have persistently been weak for the first three weeks of September. Since the start of September, the S&P 500 has lost roughly 4% in value, with the tech-heavy NASDAQ down nearly 6% (tech stocks respond more dramatically than the overall market to higher rates). This comes as the ten-year rate rose from 4.09% to 4.44% today.

We speak with investors daily and we know that this can be a frustrating phenomenon. After a strong first half of the year, sentiment feels really negative again among investors. Believe me, we can understand the exhaustion with all the Fed watching, we lament it regularly here in the office!

One sector of the market does appear to be finding its footing yet again – energy. Investors piled into energy stocks during the market turmoil of 2022, only to rotate out in the first half of 2023, toward growth-oriented securities. Energy is strong again, with oil prices now back above $90 per barrel. In today’s letter, we will discuss our thoughts on energy and one particular sub-sector therein where we think there is still opportunity for growth.

Can you remember the last time we received an earnings report? It’s been quite some time since we’ve heard directly from CEOs and CFOs about the health of their individual companies. We think it is no coincidence that stocks have drifted lower since the last earnings season. Here we explore that phenomenon and ultimately urge patience for investors. In the short-term, macroeconomic factors like interest rates seem to be directing markets. We expect fundamentals eventually to win out. In this section, we will mention a couple of healthcare stocks that have already been through the wringer and have started to come out the other side, a bit under the radar.

Finally, we will discuss some potential catalysts to reverse the negative feelings now plaguing the market. With this in mind, we consider a key characteristic of a successful long-term investor – patience. In an investment journey spanning many decades, having the patience to hang in during short and temporary periods of volatility is essential to long-term success. We hope today’s article helps you to exercise patience in a frustrating time!

With that all being said, let’s get into it!

The Federal Reserve – Not Again?!?

The most widely-followed event in the markets this past week was the September Federal Reserve Board meeting, concluding on Wednesday. Chairman Jerome Powell announced that the Fed is leaving rates steady, keeping the overnight funds rate at 5.25-5.5%. However, Powell indicated that a hike in the November meeting remained a strong possibility. But what really seemed to spook investors was the outlook for interest rates in the future.

Chairman Powell reiterated that he does see steady progress toward the goal of bringing inflation in line with historical averages, but that there still remains work to be done. Powell also noted that economic growth is in excess of what he had previously expected. A relatively strong economy complicates the Fed’s efforts to control prices. In our view, the Fed will continue to talk tough until the very last moment before they let up on the tightening cycle. The last thing they want is for market participants to begin to place bets that rates will drop before their intended work to bring down inflation is completed – that would defeat the whole purpose of the tightening!

In the Fed’s “dot plot”, Federal Reserve Governors anonymously give their projection for future rates. Previously, the dot plot implied a Fed Funds rate in 2025 of 3.4%. There was a major shift in the plot in this week’s meeting, as implied probabilities now project a Fed Funds rate of 3.9%. Essentially, we are seeing the Fed telegraph a policy of “higher for longer”, which dashed the hopes of investors that interest rates might be lowered significantly in 2024.

While it is true that some industries will struggle in a high interest rate environment – housing and cyclical businesses come to mind –history tells us that strong stock performance is possible in a relatively high interest rate environment. We think today has strong similarities to the mid-1990s: at that time, the Federal Funds rate vacillated between 5-6%, but the Internet Revolution 1.0 led to very strong stock market returns from 1995 to 1999.

Given the primacy of Artificial Intelligence ((AI)) and the very real business uses for the emerging technology, we think drawing an analogy between today and the mid-1990s makes sense. While past results are no indication of future returns, we can envision a scenario in which stocks deliver above-average returns in the coming years, despite high interest rates. Short-term thinkers will disagree with me vehemently and that’s just fine. In this case, we ourselves exercise patience and suggest other investors adopt a similar attitude!

Energy – Reemerging with Little Fanfare

The last decade in the energy business has been a journey! Oil prices spiked in the early 2010s, ultimately plateauing and falling sharply in 2014. As oil prices collapsed in the mid-2010s, we saw a significant number of oil and gas companies filing bankruptcy, having horribly overextended themselves to drill for oil in an environment of high prices.

In the early days of the Covid pandemic, oil prices fell so sharply that they actually traded to a negative price for two days in early 2020. Interestingly, we saw far fewer bankruptcies in this period, as those left after the past bust cycle were the stronger operators. But beyond that, the industry had learned its lesson – the plan going forward would be to maintain discipline in capital expenditures, not only to preserve solvency, but also to constrain supply. Whether implicit or explicit, we are seeing cartel-like behavior here, not just from the traditional OPEC producers, but also from Western-based oil companies.

That all feels like ancient history now. In 2022, the Russian invasion of Ukraine sent oil prices soaring to levels unseen since 2014 (roughly $125/barrel). With Russian oil/gas embargoed, world supply now has an underlying constraint, putting upward pressure on prices. But interestingly, oil prices erased much of that progress, closing 2022 in the low $70s. Investors largely abandoned the most popular theme of 2022, energy, seeking higher returns from tech and other growth sectors.

TradingView

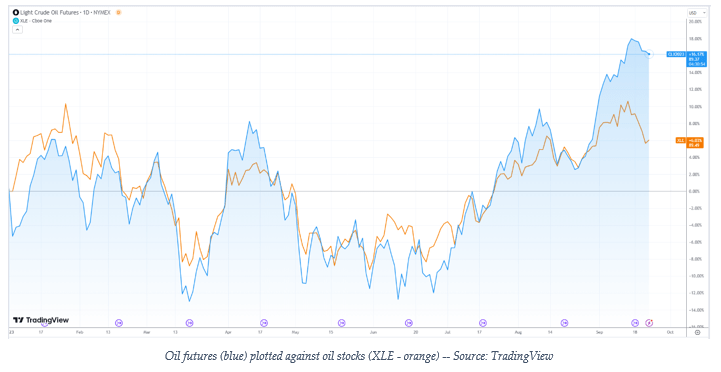

A bit under the radar, we have seen oil prices creep back up roughly 25% over the past 9 months, recently eclipsing the $90/barrel mark. However, in the year-to-date chart of oil prices plotted against oil stocks, with the Energy Select Sector SPDR Fund ( XLE ) as a proxy, we see a significant lag. We think this suggests that there is still a good opportunity to add exposure to this area with a strong possibility of above-market returns over the next year.

{kind=link}

For those investors looking for a more specific investment idea here, we think it is worth considering companies that operate in the oil services space, the types of which comprise the VanEck Oil Services ETF ( OIH ). Since COVID, oil companies, particularly in the US, have been tapping already drilled wells that had not yet been converted into oil/gas for sale. The supply of the so-called Drilled, but Uncompleted ((DUC)) wells is beginning to dwindle. Therefore, we think that major oil companies are likely to increase their spending on drilling in the coming years. This means a potential boon for companies in oil services. Two that we like particularly are Schlumberger ( SLB ) and Transocean ( RIG ) .

Now It’s a Phenomenon – Weakness Between Earnings

What was once a curiosity is now a phenomenon. We noticed in late 2022 that stocks, as a collective, seemed to perform quite well during the earnings seasons and tended to drift lower in earnings “quiet periods”, when investor focus shifted from generally solid business fundamentals to worries about macroeconomics, specifically interest rates.

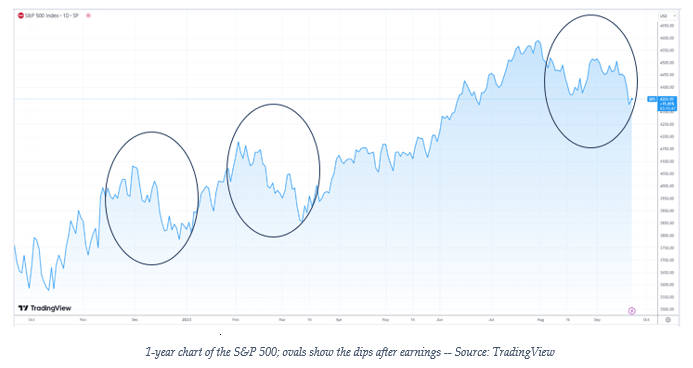

We now have what I consider to be ample evidence that this is happening. Earnings season tends to come in the 3 rd through 6 th week after quarter close, so largely we are speaking of the time periods of mid-January to mid-February, mid-April to mid-May, mid-July to mid-August, and mid-October to mid-November. I think the best way to tell this story is to tell is visually looking at the 1-year chart of the S&P 500:

{kind=link}

As we look at the 1-year chart, this pattern has played out in three of the last four quarters (represented by the ovals). We theorize that during the barrage of earnings releases, investors are seeing overall strong results on the microeconomic level and responding to the good news they hear from earnings reports by purchasing shares. While, at the same time, investors seem to be shifting their gaze to macroeconomic challenges in the absence of fundamental news.

What is our takeaway from this phenomenon? We maintain optimism in what we are seeing at the corporate level. There are dozens of companies in various industries driving profits and sales higher, whether it be in tech, healthcare, industrials, or financials. We think there is pessimism directly related to interest rate jitters, a story we have been telling for a very long time now, actual business results do seem to be strong.

Finally, there is one additional phenomenon I wanted to address: strong responses to earnings disappointments. Three stocks come to mind when I think of this: Amgen ( AMGN ), Cigna ( CI ), and Alteryx ( AYX ) , though there are many others who have exhibited this pattern.

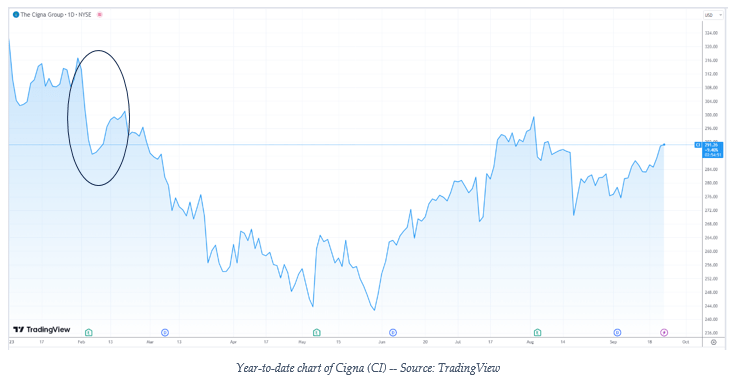

Cigna has been one of our favorite healthcare insurance stocks over the past few years. In February, Cigna delivered what we thought was a fairly strong earnings release, but the market absolutely punished the stock:

{kind=link}

As you can see, the stock has rebounded smartly since. Often times, counterintuitive stock price moves after earnings can constitute excellent opportunities to purchase stocks we have been following closely but struggle to add because stock prices seem “expensive”. We think this is something to watch when earnings season begins again in a month from now.

What is the Possible Catalyst?

In periods of negative sentiment, it can feel to an investor like nothing can change the dynamic. Understandably, the interest rate concern has hung over investors’ heads like a sword of Damocles, with no end in sight. Rates may continue to cause concern for investors over the next year, but we think there are a number of events on the horizon that could shake up the dynamic and put the bulls back in charge of this market.

The first, and most obvious, for us is the coming earnings season. Market leaders like Meta Platforms ( META ), Alphabet ( GOOG , GOOGL ), Nvidia ( NVDA ) ,among others, have delivered strong results for a few quarters running. Markets have rallied strongly after these releases throughout 2023. Since there is considerable business momentum at some of the largest stocks that have led the market this year, we expect the trend to continue in 3 rd quarter earnings, beginning next month.

The next catalyst is the so-called “ Santa Claus rally ”. For whatever reason, November and December have typically been some of the strongest months for stock market performance over a long historical time frame. Interestingly, August and September tend to be some of the worst months for stock market performance. If history serves as any guide, things could pick up in the 4 th quarter.

A combination of strong fundamentals of some prominent individual businesses, coupled with where we stand on the calendar, give us some hope that the current spate of pessimism could end soon. Remember, if you are in the wealth accumulation phase, temporary periods of stock market weakness are in your favor. Stocks trading at lower prices means you can purchase more shares of a stock at a lower price for the same money than you would have been able to do at the higher price. For long-term investors that are regularly investing money, this period of weakness should be viewed as an opportunity!

Stock Trader's Almanac - 2018

Takeaways

This is the second straight month of market weakness, fueled mostly by the Fed and investor worries around interest rates. We have seen progress in slowing inflation over the past few months, so we continue to think that macroeconomic fears are only temporary.

We have seen one sector starting to creep higher in the current environment – energy. Since the movement of energy stocks has lagged the price of the commodity, we still think there is opportunity here for investors, particularly in the oil service segment of the industry.

We now think we have identified a pattern in the market that investors can potentially take advantage of – market weakness in the quiet periods between earnings seasons. We will watch to see if this continues next quarter, but with business momentum in a variety of sectors, it certainly might.

It may be difficult as an investor in these periods of pessimism, but we continue to counsel patience. There are a few catalysts on the horizon, including the next set of earnings and a favorable positioning in the calendar. If history repeats, we may be poised for a strong 4 th quarter in markets. For long-term investors, lower prices represent an opportunity to purchase shares at a discount, which is ultimately advantageous.

DISCLAIMER: This report contains views and opinions which, by their very nature, are subject to uncertainty and involve inherent risks. Predictions or forecasts, described or implied, may prove to be wrong and are subject to change without notice. All expressions of opinion included herein are subject to change without notice. Predictions or forecasts described or implied are forward-looking statements based on certain assumptions which may prove to be wrong and/or other events which were not taken into account may occur. Any predictions, forecasts, outlooks, opinions, or assumptions should not be construed to be indicative of the actual events which will occur. Investing involves risk, including the possible loss of principal. The opinions and data in this report have been obtained from sources believed to be reliable; neither Left Brain nor its affiliates warrant the accuracy or completeness of such and accept no liability for any direct or consequential losses arising from its use. In addition, please note that Left Brain, including its principals, employees, agents, affiliates, and advisory clients, may have positions in one or more of the securities discussed in this communication. Please note that Left Brain, including its principals, employees, agents, affiliates, and advisory clients may take positions or effect transactions contrary to the views expressed in this communication based upon individual or firm circumstances. Any decision to effect transactions in the securities discussed within this communication should be balanced against the potential conflict of interest that Left Brain, its principals, employees, agents, affiliates, and advisory clients has by virtue of its investment in one or more of these securities.

Past performance is not indicative of future performance. The price of securities can and will fluctuate, and any individual security may become worthless. A high or favorable rating, rating outlook, gauge, or similar opinion is not indicative of future performance, and no user should rely on any such rating, rating outlook, gauge, or similar opinion to predict performance or potential for return. Future performance may not equal projected or forecasted performance or potential for return. All ratings and related analysis, as well as data, statistics, analysis, and opinions contained herein are solely statements of opinion and are not statements of fact or recommendations to purchase, hold, or sell any security or make any other investment decisions.

This report may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will materialize. Reliance upon information herein is at the sole discretion of the reader.

THE REPORT IS PROVIDED ON AN "AS IS" AND "AS AVAILABLE" BASIS WITHOUT REPRESENTATION OR WARRANTY OF ANY KIND. Left brain Wealth Management DISCLAIMS ALL EXPRESS AND IMPLIED WARRANTIES WITH RESPECT TO THE REPORT, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

The Report is current only as of the date set forth herein. Left Brain Wealth Management has no obligation to update the Report, or any material or content set forth herein.

For further details see:

Patience Is The Name Of This (Market) Game