AHCO - Patterson Companies: A Prospect To Brighten Your Smile

2023-03-09 08:22:47 ET

Summary

- Patterson Companies has had a rather mixed operating history in recent years, with sales climbing, but profits and cash flows posting volatile results.

- That trend has continued into the 2023 fiscal year, though cash flow data is looking up.

- The firm may not be the greatest prospect on the market, but it does seem to offer some upside based on how shares are priced today.

Unfortunately, humans do not have the same evolutionary advantage that some creatures, such as sharks, have been gifted with. For instance, we only possess a single set of permanent teeth. Especially in an era defined by high sugar consumption and significant amounts of processed foods, our teeth health is unbelievably important. One company that plays in this market, as well as in the animal health market, is Patterson Companies ( PDCO ). Over the past few years, management has done well to grow the company's top line. However, recent performance on the top line has been a bit disappointing and historical volatility for the company on the bottom line has been the norm. This creates some risk for investors moving forward. But given how shares are currently priced, it seems as though the market is definitely factoring these issues into the equation. While the company is far from a home run prospect, I do think PDCO stock is affordable enough to warrant a bit of upside from here.

A niche player

According to the management team at Patterson Companies, the company operates as a value-added specialty distributor that serves the US and Canadian dental supply markets. It also serves the animal health supply markets in both of those countries, as well as throughout the UK. To really understand the company though, we should break it up into its two core operations. The first of these is the Dental segment. Through this, the company provides dental products to over 100,000 dental practices, dental laboratories, educational institutions, and community health centers. Specific products that it sells include, but are not limited to, consumables such as infection control, restorative materials, and instruments. 57% of the segment’s revenue came from the consumable category during the 2022 fiscal year. 32% of revenue for the segment came from the sale of technology and dental equipment, various software solutions, and more. That leaves 11% of revenue under the segment coming from value-added services and other offerings. Examples here include software and design services, maintenance and repair activities, and equipment financing. All combined, this operating segment accounted for 38.7% of the company's revenue during its 2022 fiscal year.

Even larger than the dental operations that the company has are its animal health operations. Under the Animal Health segment, which is responsible for roughly 61.3% of sales, the company sells about 100,000 SKUs from roughly 2,000 manufacturers to approximately 50,000 customers in the animal health supply market. Examples of products here include pharmaceuticals, vaccines, diagnostics, prescription and non-prescription diets, nutritionals, equipment, software, and more. Approximately 96% of the offerings under this segment are in the form of consumables. Another 3% comes from equipment and software, while the remaining 1% is attributable to value-added services and other offerings.

{kind=link}

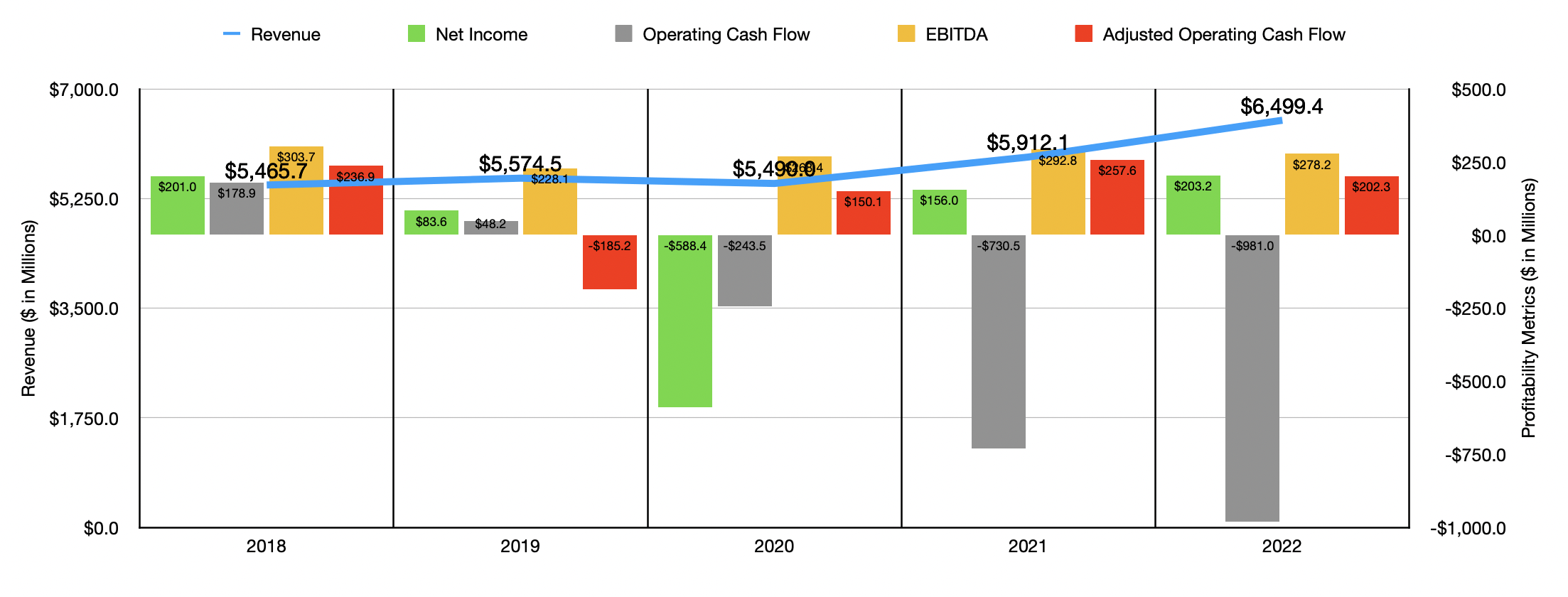

Over the past five years, management has done a pretty good job growing the company's top line. Revenue went from $5.47 billion in 2018 to $6.50 billion in 2022. Though it is worth mentioning that sales growth really didn't tick up until 2021. From 2021 to 2022, the company was aided by a 1.9% contribution associated with the extra operating week that it had compared to one year earlier. The firm also saw a marginal contribution from foreign currency fluctuations. The biggest increase for the firm though came from the Animal Health segment, which reported revenue expansion of 11.9%. 2% of that came from the aforementioned extra week of sales. But most of the sales increase was driven by higher demand across all of the businesses and geographies for the segment. Meanwhile, the Dental segment grew at a more modest but still impressive 8.1%. This was driven by an 8.4% rise associated with consumables and a 9.5% increase driven by equipment and software. Value-added services and other activities saw an expansion of only 3.4%. At the end of the day, management attributed some of the sales increase to the fact that 2021 was negatively impacted by the COVID-19 pandemic.

While the revenue trajectory for the company has been quite positive in recent years, profits have been all over the map. The company has gone from as bad a situation as a $588.4 million net loss to as good a situation as a $203.2 million net profit. Operating cash flow has been far more volatile. In each of the past three completed fiscal years, the company reported significant cash outflows. But as you can see in the initial chart in this article, that picture changes when we adjust for changes in working capital. In this case, the metric would have been $202.3 million in 2022 compared to the negative $981 million actually reported. The greatest stability for the company came from its EBITDA, which remained in a fairly narrow range of between $228.1 million and $303.7 million over the past five years.

{kind=link}

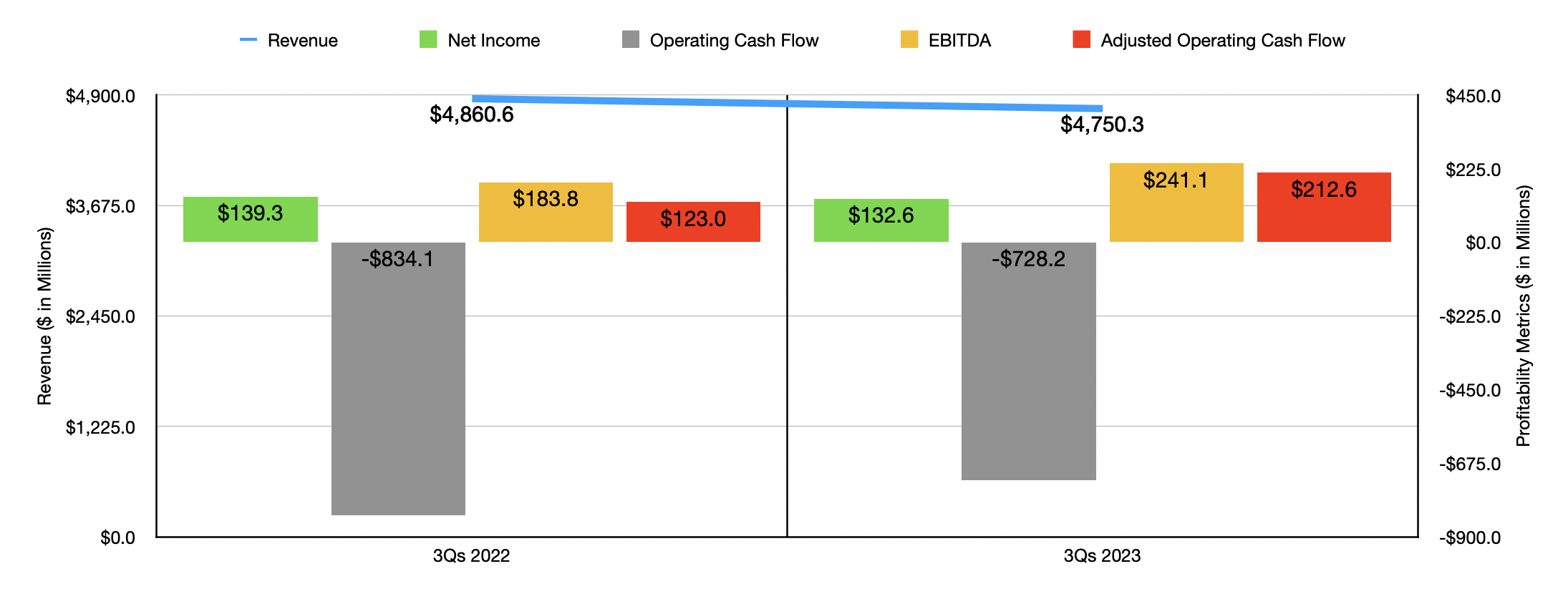

When it comes to the 2023 fiscal year, the results experienced so far have been quite mixed. Revenue, for instance, totaled $4.75 billion in the first nine months of the 2023 fiscal year. That's down from the $4.86 billion reported one year earlier. This decrease, management said, was driven in large part by the absence of an extra week that the company benefited from in the prior year. In addition to that, foreign currency fluctuations impacted sales negatively to the tune of 1.8%. The biggest decrease for the company came from its Dental segment, which saw revenue drop by 3.8%. And the biggest drop there was attributable to a 6.1% decline in consumables thanks to the absence of said extra week and lower sales of personal protective equipment. The drop in sales brought with it a decline in profits. Net income, for instance, shrank from $139.3 million in the first nine months of the 2022 fiscal year to $132.6 million the same time of 2023. Operating cash flow improved, turning from negative $834.1 million to negative $728.2 million. But if we adjust for changes in working capital, it would have improved from a positive $123 million to a positive $212.6 million. And finally, EBITDA for the business popped up from $183.8 million to $241.1 million.

{kind=link}

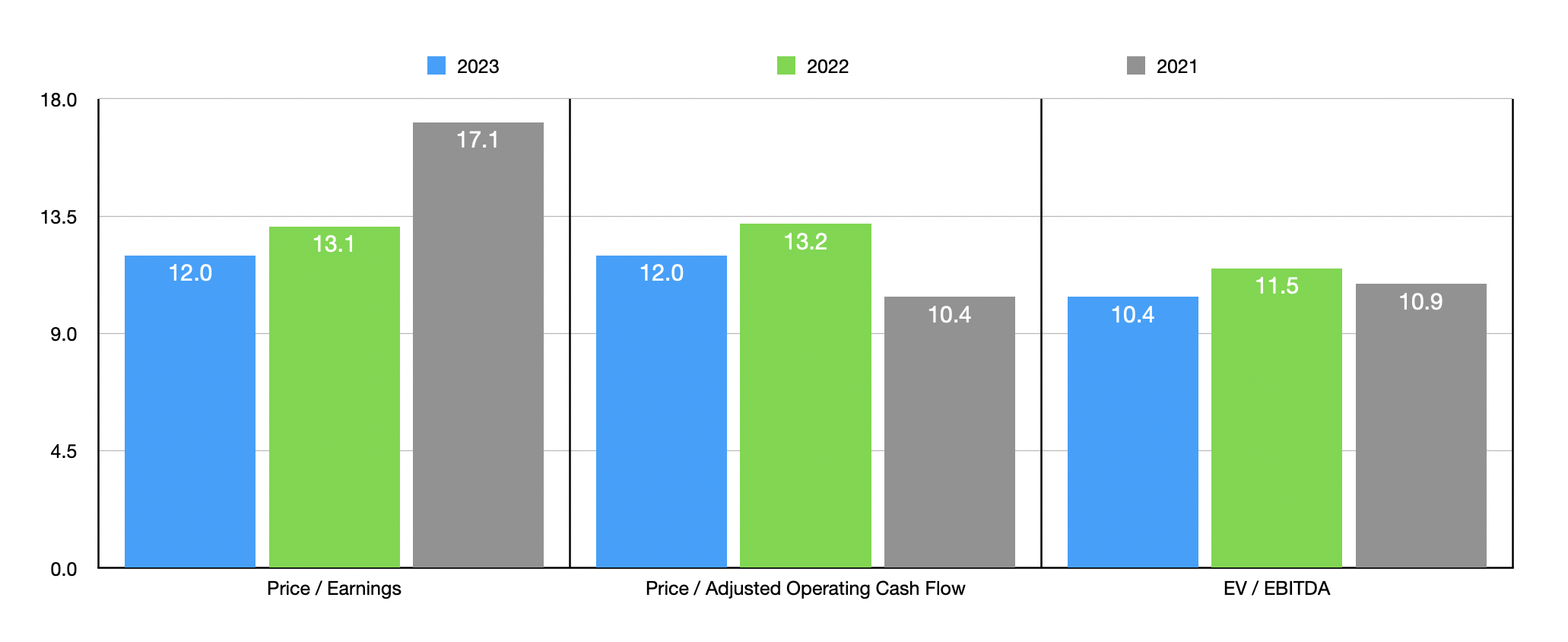

For the 2023 fiscal year in its entirety, management expects earnings per share of between $1.96 and $2.01. On an adjusted basis, profits per share should be between $2.25 and $2.30. At the midpoint, that would translate to net income of $222.9 million. We don't know what to expect when it comes to the other profitability metrics. But if we assume that they will change at the same rate that net income is expected to, we should anticipate adjusted operating cash flow of $221.9 million and EBITDA of $305.2 million. Based on these figures, the company is trading at a forward price-to-earnings multiple of 12. That's also the same reading that we get for the forward price to adjusted operating cash flow multiple. And finally, the EV to EBITDA multiple for the business should be 10.4. For context, I also included evaluation data using results from two prior years in the chart above. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 19.9 to a high of 57.9. Our prospect was the cheapest of the group. Using the price to operating cash flow approach, the range was between 3.4 and 17.8. In this case, four of the five companies were cheaper than our target. And finally, using the EV to EBITDA approach, we end up with a range of between 7.5 and 43.4. Two of the five companies were cheaper than Patterson Companies.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Patterson Companies |

| 12.0 |

| 12.0 |

| 10.4 |

| AdaptHealth ( AHCO ) |

| 57.9 |

| 5.6 |

| 7.5 |

| Owens & Minor ( OMI ) |

| 51.8 |

| 3.4 |

| 9.8 |

| PetIQ ( PETQ ) |

| N/A |

| 6.7 |

| 43.4 |

| Henry Schein ( HSIC ) |

| 19.9 |

| 17.8 |

| 12.3 |

| Cardinal Health ( CAH ) |

| 30.2 |

| 6.2 |

| 33.0 |

Takeaway

From what I can see, Patterson Companies is not exactly a fantastic business. It's not a bad business either. Sales growth has continued in recent years, though profit and cash flow data have been somewhat disappointing. Relative to similar firms, the pricing of the business is all over the map. But on an absolute basis, shares do look reasonably attractive. Given this, I would make the case that the firm warrants a soft ‘buy’ rating at this time.

For further details see:

Patterson Companies: A Prospect To Brighten Your Smile