PAYO - Payoneer Global: Attractive Growth Story

2023-08-10 17:04:52 ET

Summary

- Payoneer Global Inc. has reported strong revenue growth, but its stock struggles to rally.

- Payoneer is active in high-growth emerging markets and recently acquired Spott for AI analytics.

- The company's conservative guidance may be holding back Payoneer Global stock, with the current valuation at only 10x EV/EBITDA targets.

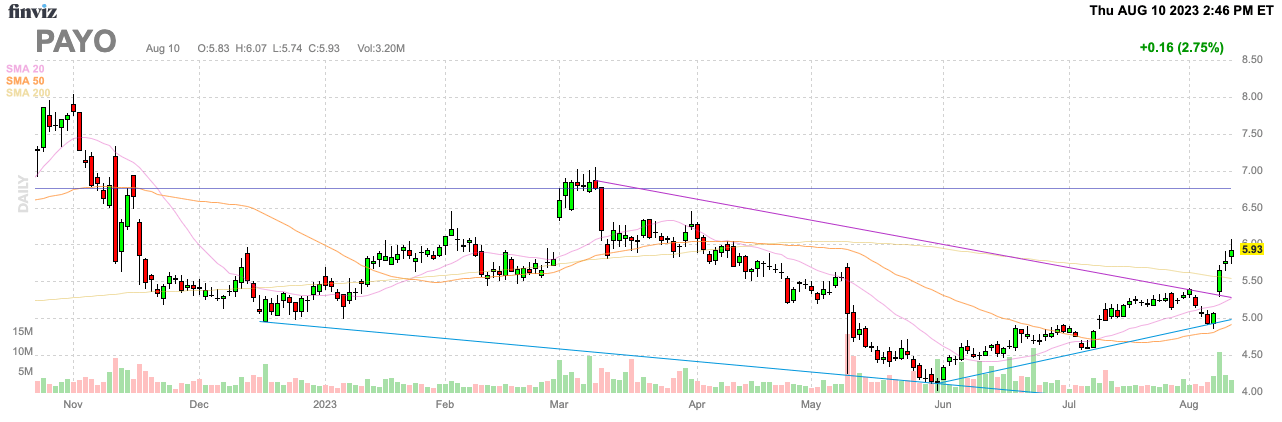

Payoneer Global Inc. ( PAYO ) reported another blowout quarter, yet the stock had a hard time rallying just back above $5.50 on the news. The global payments company now has a history of reporting 40% revenue growth without the stock budging much. My investment thesis remains ultra Bullish on the stock, which is trading at a disconnect with the growth rate on opportunities in global payments.

{kind=link}

Playing Global Growth

Payoneer offers a great way to play global growth and the intersection of cross-border payments. The company is very active in areas like China, Southeast Asia, and Latin America, where the higher growth emerging markets need access to a global payments platform.

Source: Payoneer Q2'23 presentation

{kind=link}

Payoneer just announced a deal to acquire Spott to provide AI analytics to make faster business decision-making to better serve SMB (small and medium-sized business) customers around the globe. The company reported growth driven by areas like India and UAE, where programming and services sector customers are signing up and the payments platform needs help sorting out attractive customers for the platform.

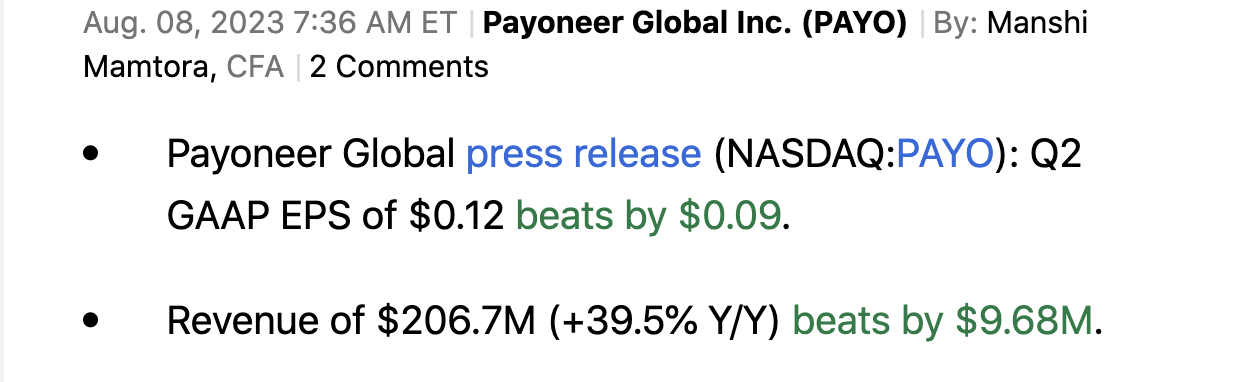

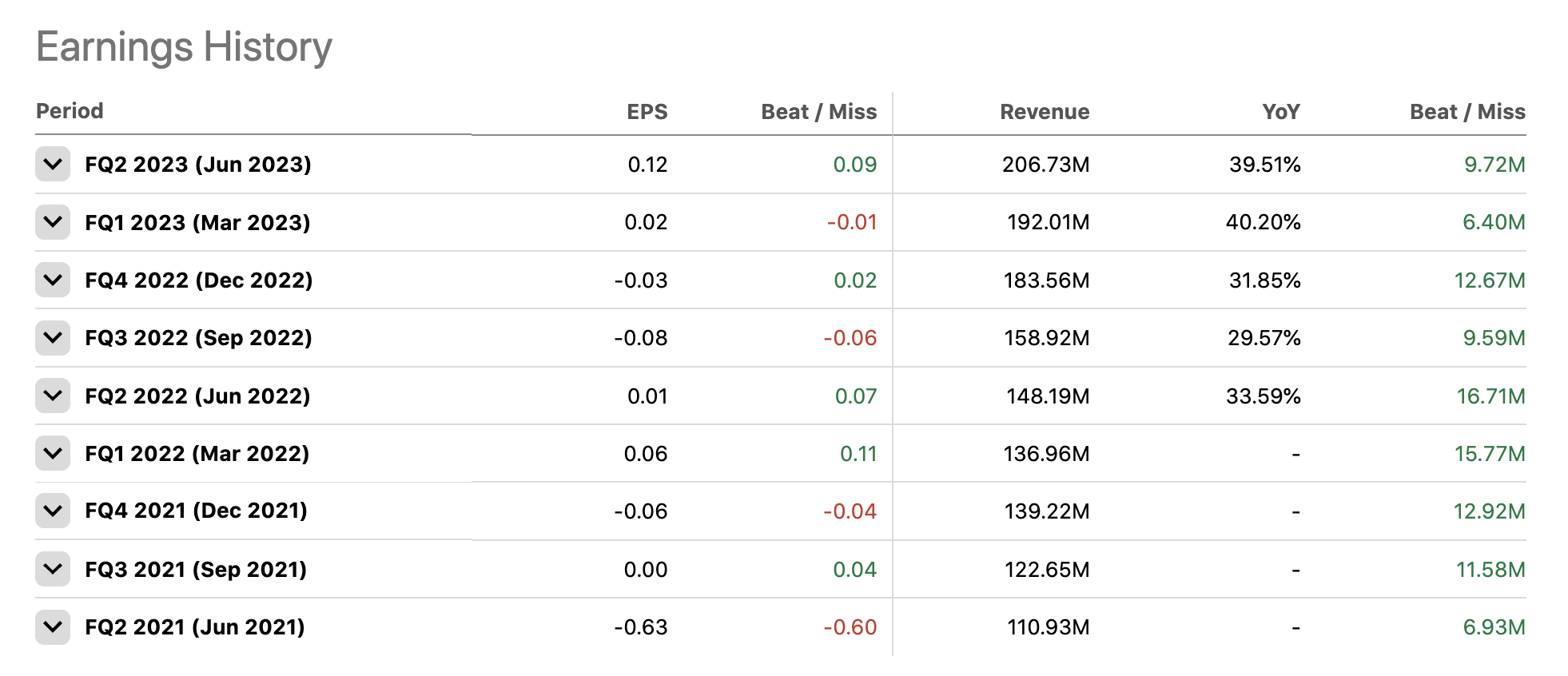

The company reported Q2'23 results that again smashed consensus estimates as follows:

{kind=link}

A prime reason for growth is that take rates continue to soar. Payoneer doesn't need to grow payment volumes, with the take rate growing by nearly 30% YoY to 131 basis points.

The virtual commercial card has been a home run product for the company. The product has a 2.5% take rate, double corporate average, and Payoneer only has 4% customer penetration rates generating $979 million in LTM payment volumes to produce 100% growth.

All while new products and features are driving growth, Payoneer continues to benefit from larger customer balances generating higher interest income. The customers balances grew 1% sequentially to $5.5 billion, leading to $55 million in interest income for Q2.

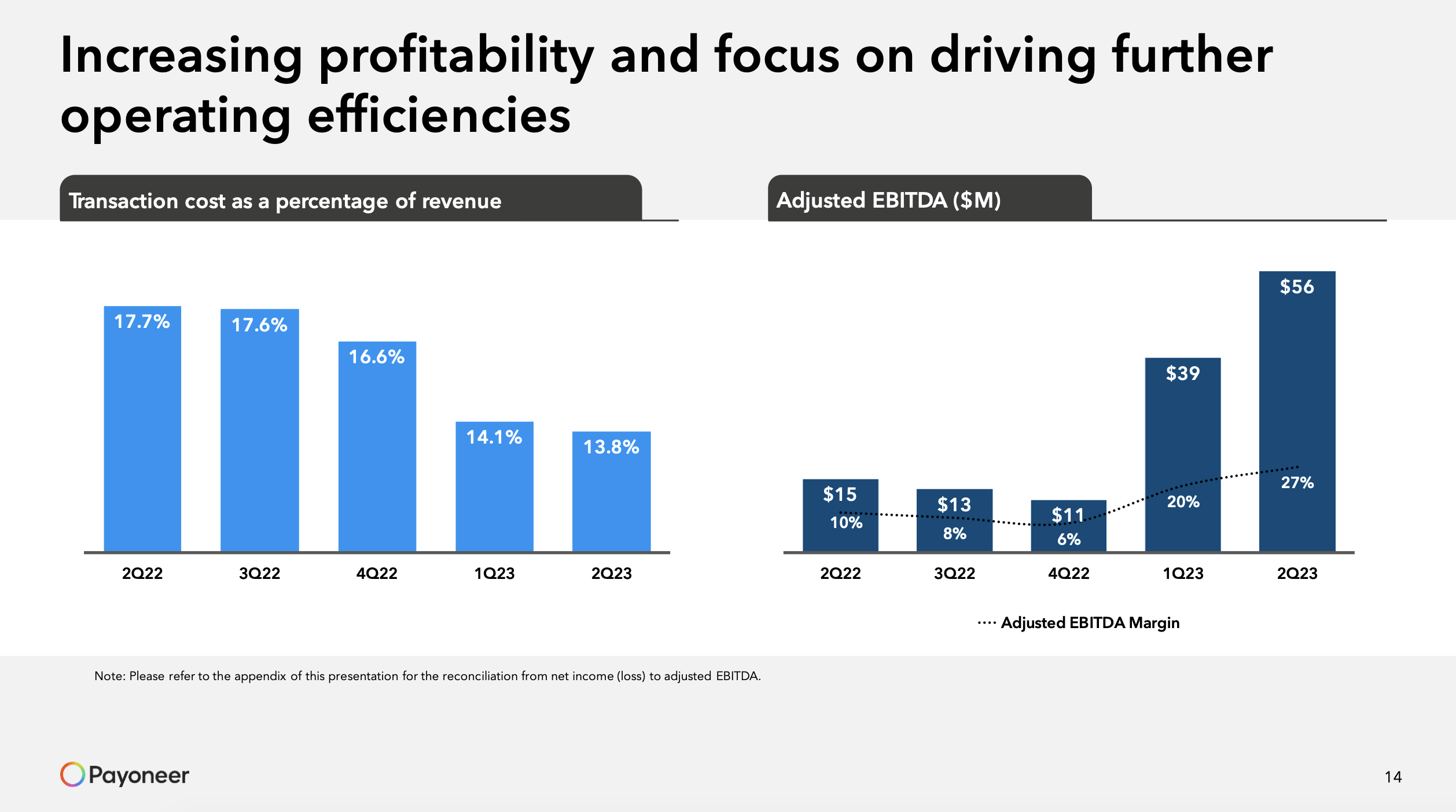

The net results are that Payoneer has quickly zoomed into large adjusted EBITDA profits. The company had already exceeded the long-term goals for 20%+ margins with a 27% quarter in Q2.

Source: Payoneer Q2'23 presentation

{kind=link}

Conservative Guidance

Payoneer has now reported 2 straight quarters with 40% revenue growth, yet the stock doesn't trade any higher. A big part of the issue is that the company constantly provides very conservative guidance.

As highlighted above, Payoneer beat Q2 revenue targets by nearly $10 million. The company has beaten numbers by somewhere around $10 million quarterly going all the way back to Q3 '21 and extending through the war in Ukraine, where numbers were cut too aggressively.

{kind=link}

The management team guided to the following financial targets for 2023:

- Revenue $820 to $830 million, up from $810 to $820 million

- Transaction costs at ~15.5%

- Adjusted EBITDA $160 to $170 million, up $20 million from $140 to $150 million.

The main issue holding back the stock is guidance only implies 10% growth in the 2H absent the interest income boost. Payoneer earned interest income of $15 million last Q3 and $36 million in Q4'22.

As an example, the consensus estimates are for Q4'23 revenue estimates of $222 million. The forecast is for sales to rise ~$38 million and up to $19 million of the boost will come from flat interest income with last quarter. The end result is just roughly $19 million in higher payments related revenue in Q4 for 10% growth.

Also, Payoneer has already generated $95 million worth of adjusted EBITDA during the 1H of the year. The high end of guidance only amounts to $75 million of EBITDA for the 2H.

The numbers don't really add up, other than to suggest Payoneer has under promised again. Remember, the company just boosted adjusted EBITDA guidance for the year by $20 million after reporting Q2 numbers and the original guidance for the year was $120 to $130 million now suggesting a $40 million adjusted EBITDA beat for the year.

Takeaway

The key investor's takeaway is that Payoneer Global Inc. continues to provide conservative guidance. The global payments company should continue adding customer funds to drive interest income even higher.

The stock only trades at ~10x EV/EBITDA targets. The company has $590 million in cash, contributing to the cheap valuation and why investors should load up on these low values.

For further details see:

Payoneer Global: Attractive Growth Story