PAYO - Payoneer Global: Offers An Opportunity For Long-Term Focused Investors

2023-11-05 08:06:20 ET

Summary

- Payoneer Global offers cross-border multi-currency payment solutions for small businesses, contractors and remote workers with strong revenue growth and potential for profitability.

- The company's gross margins have improved, and it has been generating positive operating cash flow. Net profits to follow soon.

- With the expected growth in global trade, Payoneer has room to expand its customer base and increase market share.

- It's trading for 17 times forward earnings and 19 times operating cash flow which is cheap for a hyper growth company.

Payoneer Global ( PAYO ) is a financial technology company that mostly works with small businesses to run a variety of transactions and online money transfers. The company offers a solid growth story and likely a path to profitability at a relatively low price after investors heavily punished it in last year's bear market.

Along with other products, the company offers a cross-border payment system which allows business owners to collect payments across the world in different currencies globally. The company's customer base includes small businesses that do different types of businesses such as import, export, freelance work, contract work, consulting, digital artists as well as employees of companies who work remotely away from their company's main location which is becoming more common lately. When an employee works in one country but lives in another country, getting them paid can be a complicated manner between currency fluctuations, taxations and different regulations in different countries and Payoneer has expertise and experience in dealing with situations like this.

{kind=link}

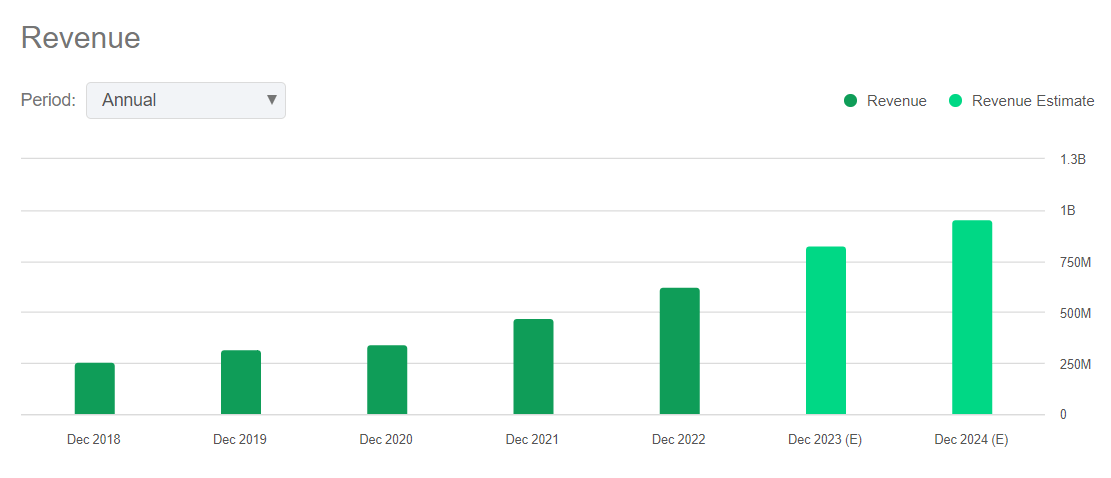

While the company has been around since 2005, it had its IPO just a couple years ago in 2021. In recent years the company's growth has accelerated as its products gained more adoption from people who work and get paid across borders. Between 2018 and 2022, the company's revenues jumped from $250 million to $600 million and it's on track to reach almost $1 billion by the end of next year based on analyst estimates which would represent a four-fold growth from 2018.

{kind=link}

As the company's revenues grew, so did its margins as the company was able to take advantage of economies of scale. Since its IPO, the company's gross margins climbed from 70% to 86% which is nothing short of impressive. I wouldn't bet on these margins to improve further since they are pretty close to 100% as it is but if the company can maintain its margins where they are right now, its path to profitability will be paved.

The company hasn't posted full profits yet but it's getting there. As you can see below, the company's operating cash flow has been improving almost every quarter since its IPO. In the last 12 months, the company was able to generate $115 million of cash flow from its operations which is impressive considering it's still in its growth stage. Many companies report large losses when they are in early stages of their growth and it's rare to see positive margins and growth at the same time since a lot of growth companies have to sacrifice one for the other.

Between now and 2030, global trade is expected to grow from $30 trillion to $40 trillion and this could create a pretty nice opportunity for companies like Payoneer that process international multi-currency payments. With its market cap of only $2 billion, this is still a small company and even if it can take a very tiny bite out of this ever-growing global trade apple, it will result in a meaningful growth for the company. There are more than 80 million businesses that work internationally but don't use a solution that will allow them to process transactions internationally in a reliable manner which creates a lot of room for the company to grow for the foreseeable future. Currently the company's customer base consists of about 2 million customers which means it has a pretty small market share which can still grow for years to come.

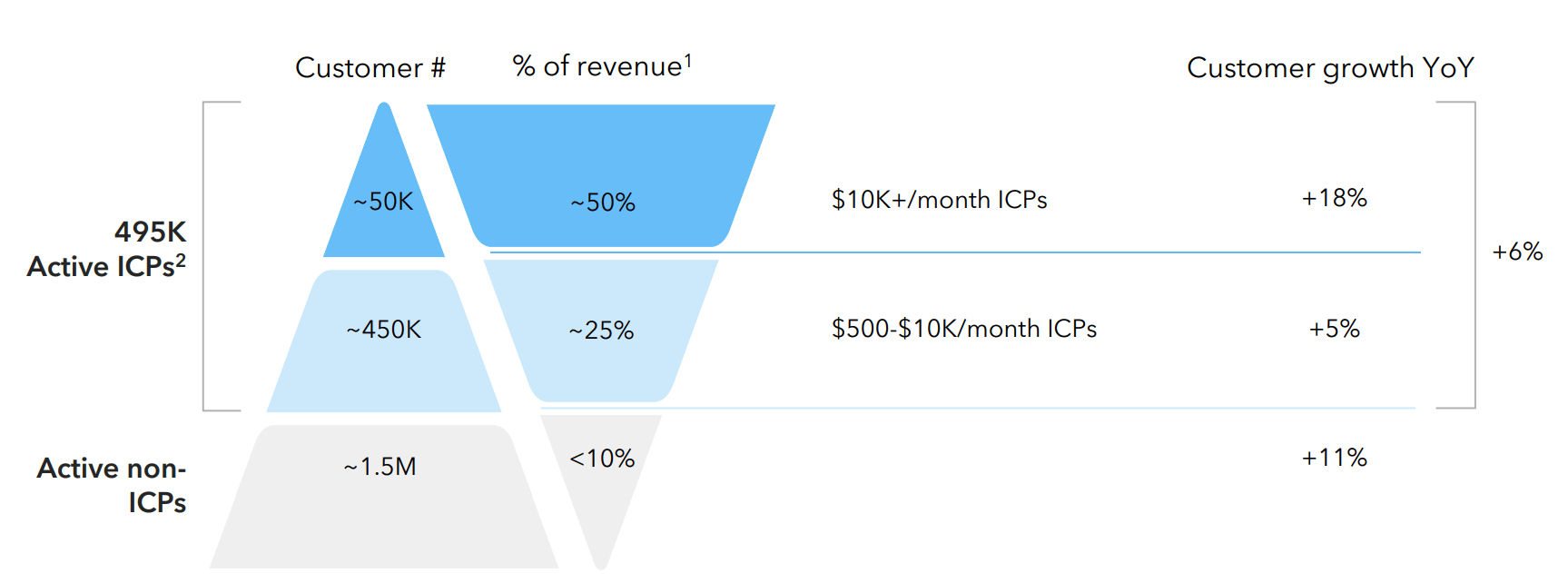

As for the company's existing customers, its most active 50k customers account for 50% of revenues whereas its 1.5 million customers account for less than 10% of its revenues. Since the company is dealing with small businesses, their engagement and volume levels will fluctuate greatly where some customers will generate huge volumes and revenues while others will not. If the company could find a way to get some of its least engaged customers more engaged, it could unlock more growth potential. Many of the company's customers are barely getting started in their cross-border business so it will take them some time to grow this segment of their business and make more use of PAYO's products. In a way PAYO's success also depends on success of its international customers. The more successful those small businesses become in cross-border trades, the more successful PAYO will become so the company has an incentive to make it easier for those small businesses to succeed in cross-border trades.

{kind=link}

In the future there is also a potential for the company to offer more services through usage of AI. For example it can create personalized experiences for customers including AI generated communications businesses can send to their customers, using predictive models to see business trends better to address future customer needs, utilizing predictive power for businesses to predict creditworthiness of their customers and fraud detection. Small businesses can benefit from usage of these services and Payoneer could see further growth opportunities if its suit of AI solutions can get to a level of self-service for its business customers. Since the company has so many customers of different sizes around the world and it handles millions of transactions every month, the company likely already has enough data to build some good predictive models. This is still a work in progress and we will have to wait and see the adoption rates of the company's AI solutions.

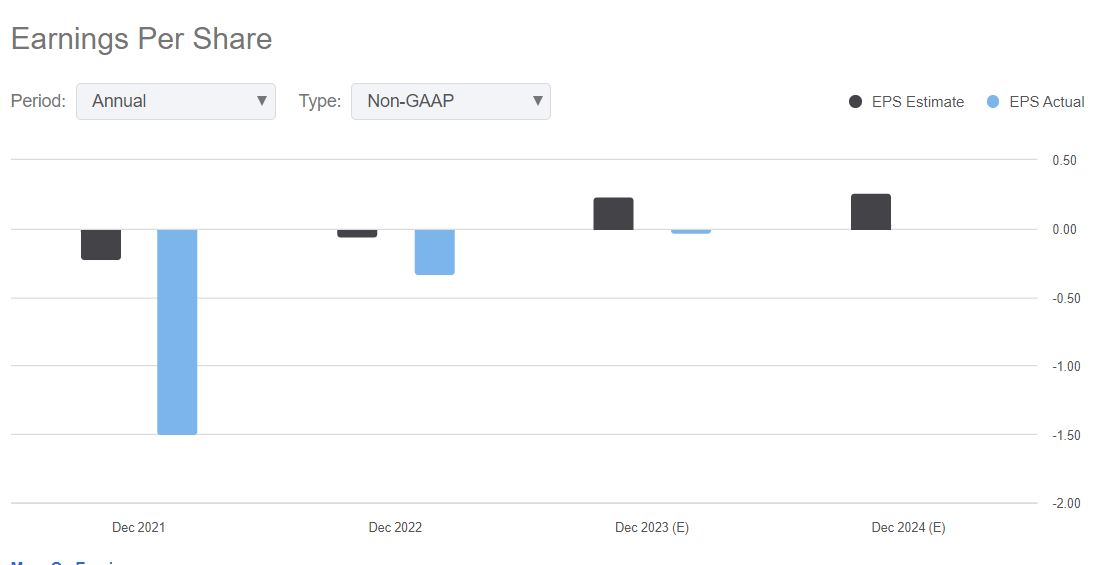

The company now has a path to profitability. After posting a large loss and missing analyst estimates badly in 2021 (it lost $1.50 when analysts were expecting it to lose only $0.22), the company improved its finances in 2022 and posted a much smaller loss of 33 cents, although it still missed analyst estimates. In 2023, the company was expected to post a small profit and it posted a small profit of 12 cents in the last quarter while analysts were expecting it to generate 3 cents. Analysts expect the company to post a small profit for the remainder of the year and a profit of 26 cents per share in 2024. Since the company has a history of missing profit estimates from time to time, it might still miss in 2024 but at least its finances are a lot better than they were a couple years ago and the company has a path to profitability. As I said above, the company already improved its gross margins and achieved positive operating cash flow so it is getting there slowly but surely even if it misses estimates from time to time along the way.

{kind=link}

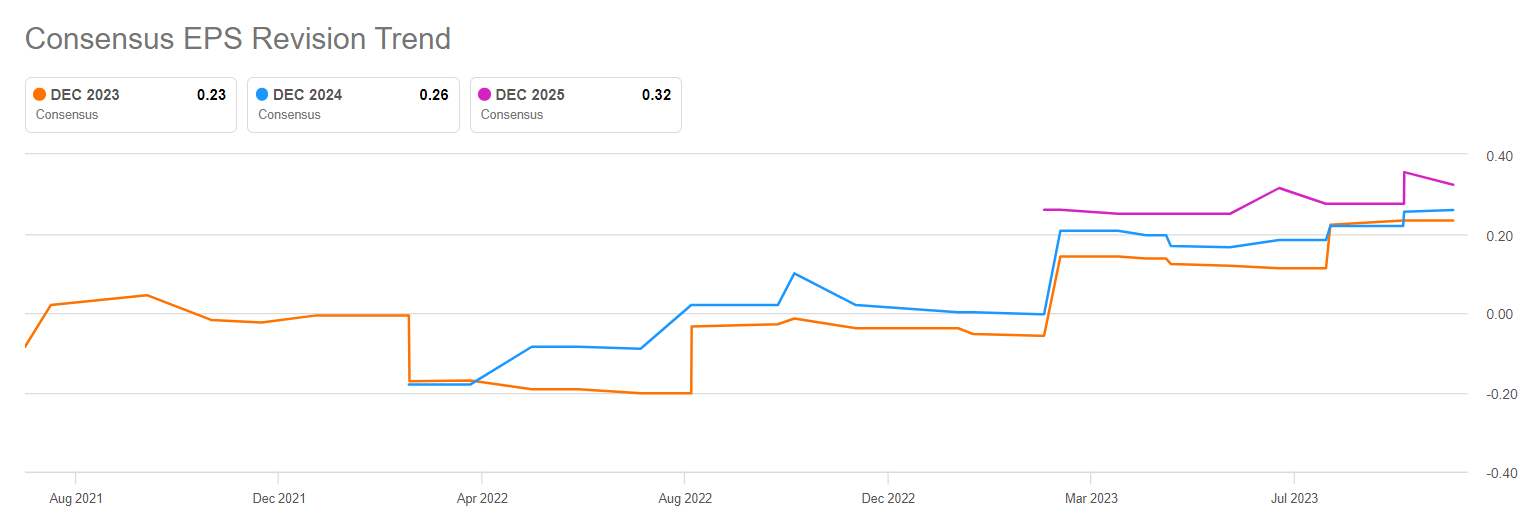

If anything, analysts have been revising their estimates upwards for the company in recent months which means they are more optimistic about the company. Since this is a small cap company, there are only a handful analysts covering the stock but this is still better than nothing. There are also a couple analysts who initiated their estimates for 2025 and they are calling for 32 cents per share in net income. If the company were to achieve that, this would give it a forward P/E of 17 which is pretty cheap for a company that's growing in double digits.

{kind=link}

Investors haven't been very favorable for this company during its entire existence as a publicly traded corporation. Since its IPO a couple years ago, the stock is down by almost half. Part of it could be because investors didn't have much faith in the company and part of it could be because the company's IPO came at a bad timing right before last year's bear market started. This year it looks like we are not in a bear market anymore but it's mostly driven by the performance of mega caps. Many small caps are still in bear territory and this stock seems to be one of those as well.

The stock's bad performance could continue in the short term until the sentiment shifts but this stock likely offers a good opportunity for long term investors regardless of short term headaches. It is a good growth story that also comes with a path to profitability and the company has a lot of growth potential it can unlock if it executes correctly which it has been doing lately. There are many reasons to be hopeful and optimistic about this company's future and it's valuation isn't too bad either with a forward P/E of 17.

For further details see:

Payoneer Global: Offers An Opportunity For Long-Term Focused Investors