PAYO - Payoneer Global: Remain Positive On The Business As Growth And Profitability Should Accelerate

2023-08-21 11:21:35 ET

Summary

- PAYO had a strong 2Q23, surpassing revenue and profit estimates, driven by interest on customer funds and pricing initiatives.

- I expect growth to accelerate in the coming quarters, driven by fast-growing regions and verticals.

- PAYO's improved profitability should lead to a gradual increase in valuation towards peers' levels.

Investment action

I recommended a buy rating for Payoneer Global ( PAYO ) when I wrote about it the last time, as I turned positive about the strong secular uptrend and revised revenue outlook. Based on my current outlook and analysis of PAYO, I recommend a buy rating. I expect growth to accelerate in the coming quarters, ending FY23 in a strong manner. Profitability should accelerate as well, pushing PAYO valuation upwards and closer to peers’ levels as the margin difference closes.

Review

2Q23 was a strong one for PAYO. Boosted by interest on customer funds, PAYO 2Q23 revenue of $206.7 million surpassed consensus estimate of $196 million. Revenue growth helped push Transaction profits up to $178.2 million, above the $166 million predicted by the street. The acceleration in revenue growth excluding float is noteworthy, and the fact that management expects this trend to continue throughout the quarter is indicative of robust demand. PAYO also benefited from a number of pricing initiatives that drove a higher take rate, so I think the growth outlook in the near future is fairly mitigated.

We drove take rate expansion by increasing adoption of commercial card and checkout products, earning higher interest income on customer funds and improving monetization of certain customer segments.

as we drive more accounts receivable into Payoneer account holders accounts and then cross-sell and up-sell the commercial Mastercard, which is under-penetrated from our perspective, we saw 50% growth year-over-year and there's deep and intense focus. 2Q23 call

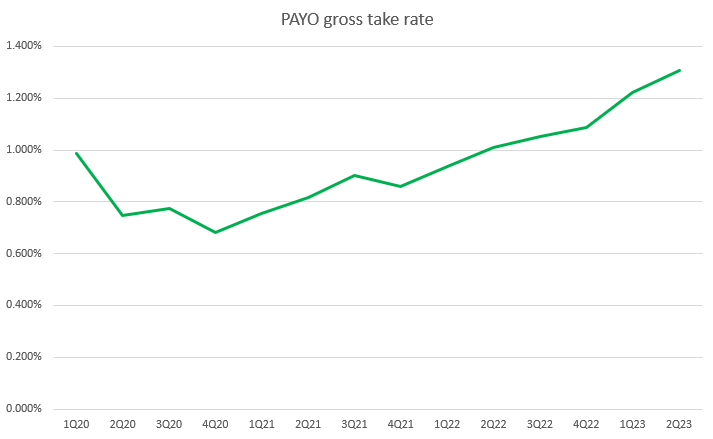

In particular, PAYO's gross take rate increased by 30bps, reaching 1.31% for the first time since 1Q20. This should send a positive signal to the market that management is steadfast in increasing monetization.

{kind=link}

Looking ahead, focusing on volume (which I deem as the one of the key indicator for PAYO growth), I expect growth to accelerate in the coming quarters as fast growing regions/verticals represent a bigger part of the business, along with lapping easy comps. For the latter, I anticipate an acceleration in B2B volume growth in 2H23 as PAYO laps proactive customer terminations. To put things into perspective, adjusting for the effect of proactive customer terminations in 3Q22 reverses the reported 2% decline in B2B volume growth in 2Q23 to a 12% Y/Y increase. Something else to note is that the most significant decline in B2B volume, 17%, occurred in the developed countries whose economies are experiencing a downturn. These include the United States, Europe, and China. In contrast, PAYO is expanding rapidly (29%) in APAC, SAMEA, and LatAm, where it now accounts for 40% of B2B volume. As the major economies recovers, PAYO grow should further accelerate. Elsewhere, in regions with a higher take rate, such as Latin America, Asia Pacific, and the Middle East and Africa, the overall number of active ICPs (a stand-in for more valuable customers) continued to grow at a healthy 13% year over year.

We grew our largest ICPs, or those who do more than $10,000 a month on average in volume, by 18% once again. This segment represents approximately 10% of our overall ICPs and it contributes to over 50% of total Payoneer revenues.

Look, in terms of what we're seeing, which obviously informs our guidance and the assumptions that underpin that, look, overall in our business, what we're assuming and what we're seeing is high single-digit aggregate volume growth, with higher volume growth in some of those regions where we're seeing an accelerated pace of growth. 2Q23 call

The increase in revenue was a major contributor to PAYO's $56mn (vs $36mn cons) in adjusted EBITDA. An important milestone for investors is that PAYO has achieved profitability excluding float. After a successful 2Q23, management increased expectations for FY23. The new revenue forecast for FY23 is $820–$830 million, up from $810–820 million. This represents growth of 31.5% Y/Y at the midpoint. The previous range of $140–150 million for adj EBITDA has also been increased to $160–170 million. I attribute the brighter EBITDA forecast to the positive effects of recent layoffs, reduced hiring, and streamlined operations. I anticipate that the street will raise their projections in light of the strong results and positive revision to guidance.

In summary, I anticipate that the company's revenue growth will pick up speed. This will happen as the company moves beyond the reduction in B2B customer activity, gains advantages from pricing strategies, and experiences a gradual increase in the usage of its higher-take rate services.

Valuation

Author's work

I believe PAYO can grow at the same rate I expected previously, but with FY23 growth adjusted upwards to reflect management guidance. FY23 should end strongly, as I expect growth to reaccelerate due to the reasons above. I modeled PAY to trade at 2x forward revenue in FY24, a slight discount to peers, as I believe the market is putting more emphasis on profitability today than growth (the PAYO margin profile is lower than peers). The positive thing about this is that as PAYO profitability improves, valuation should move towards peers’ levels. As I expect profitability to accelerate from here, I believe valuation will inch up gradually (from 1.7x to 2x, which is where it was trading just 3 months ago) over the course of the next few quarters.

{kind=link}

Risk & Final thoughts

PAYO generates revenue by accepting payments via multiple online marketplaces and e-commerce platforms. If consumers stop making purchases online, it could be bad news for PAYO's bottom line. Even though every expert in the field believes that e-commerce will continue to grow at its present rate, there is no guarantee that this will be the case.

In conclusion, my stance on PAYO remains positive, anticipating an acceleration in growth and profitability. Looking ahead, growth prospects are promising, particularly in fast-growing regions and verticals. The recovery of major economies should drive further acceleration, while management's increased revenue forecast for FY23 ($820–$830 million) reinforces near-term positive expectations. I expect PAYO's valuation to rise gradually towards peers’ level, in line with improving profitability.

For further details see:

Payoneer Global: Remain Positive On The Business As Growth And Profitability Should Accelerate