PAYO - Payoneer Global: Strong FY 2023 Outlook And Long-Term Trends

2023-04-03 11:50:10 ET

Summary

- PAYO 4Q results and 2023 guidance show a positive outlook for the company with significant growth anticipated despite the sluggish state of online retail.

- I believe PAYO has a large long-term growth potential in B2B payments made across international borders.

- PAYO's emphasis on scaling high-take rate products coupled with its strategic shift in focus to larger, more profitable customers, is expected to drive profits and boost profitability.

Description

I believe Payoneer Global ( PAYO ) 4Q results and 2023 guidance is positive for the share price from a sentiment and capital flow perspective as PAYO guided significantly ahead of the street on the bottom line. Moreover, despite the sluggish state of online retail, healthy growth for FY23 is still anticipated. From a business perspective, I believe PAYO is set to enjoy significant tailwinds to the top and bottom line as a result of higher interest rates and the monetization of customer funds. The recent increase in rates has given PAYO the freedom to invest in the company, while forcing many other businesses to scale back their plans and prioritize profitability. I think this would help PAYO stand out from the competition in the long run. To put this growth in context, consider that PAYO's organic customer acquisition is up over 25% this year with almost no additional investment in customer acquisition. PAYO has also conducted a strategic review of its customer base, which has led to the elimination of low-quality customer relationships in its B2B business and a rededication to serving customers with higher unit-economic value. Last but not least, PAYO has invested heavily in its compliance and customer onboarding platform to facilitate more profitable growth; this is, in my opinion, the single most important factor, as profitable growth is incredibly highly valued in today's environment. Given the strong secular uptrend and the revised revenue outlook, I now view the stock as attractive, changing my rating to buy on the belief that there is a 21% upside potential.

TAM is still very attractive

The way I see it, the long-term game plan for PAYO is to take advantage of the vast expansion potential in B2B payments made across international borders. PAYO's global footprint means that it has the potential to serve more than 300 million small and medium-sized businesses that are in need of PAYO's cross-border payments and other financial services. Specifically, I believe there are large long-term growth opportunities in areas like Latin American payments, B2B AP/AR, commercial card, and working capital. As such, I am expecting to see management continue innovating and launching new products to further penetrate and expand its geographical footprint in these areas. With all these in play, I believe that PAYO can maintain an annualized rate of organic growth of more than 20% over the medium to long-term.

Expect high-take rate product to drive profits

Aside from achieving profitable growth, I expect newer product offerings such as B2B AP/AR and commercial card which are more complex but have attractive unit economics, will see high adoption rates. These products have already experienced rapid growth, with B2B AP/AR increasing by 40% in the fourth quarter of 2022, and I believe they still have significant potential for growth. I expect management to continue to focus on expanding these solutions while also exploring opportunities to expand the product suite through organic development and mergers and acquisitions. Ultimately, I believe this will expand the total addressable market, generate more revenue growth, and improve profitability in the long run.

Strategy update

I think what is reassuring and helpful for the stock sentiment is that there is a strategic shift in focus to larger, more profitable customers. I believe this delivers a clear message to the market that PAYO is gunning for profits with healthy growth. I expect this combination to be well received by the market given PAYO now lies in the sweet spot of value investors and growth investors, as such capital inflow to the stock should further support share price and valuation. In addition to its emphasis on profitable growth, PAYO is making reinvestments in its platform with the intention of enhancing its customer onboarding infrastructure. In order to more profitably serve lower-volume customers, the platform enhancements will center on enhancing the artificial intelligence and predictive tools associated with onboarding. Faster and safer onboarding, streamlined operations, and a solid foundation for future profitable growth are all things I see as possible benefits. Since 25% of customers account for more than 50% of revenue and EBITDA, it's encouraging to see management shift its go-to-market strategy to concentrate on higher-margin regions like Latin America, EMEA, and APAC in an effort to attract new customers with profiles similar to its highest-value cohorts.

Guidance

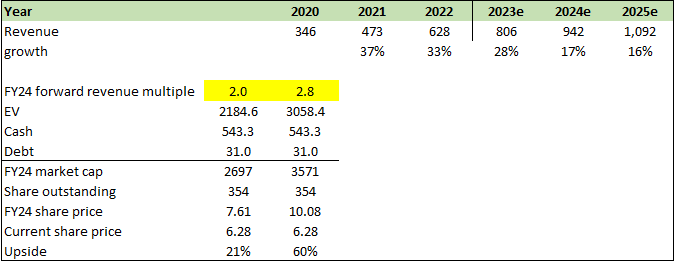

Management provided FY23 revenue guidance, projecting revenues between $800 million and $810 million. Interest income is projected to account for 22 percent of this total, or $180 million, indicating that core revenues will be around $625 million at the midpoint, up 9 percent. Also, management guided an adjusted EBITDA of $120 million to $130 million for 2023.

Valuation

With the revised growth outlook, I believe the upside to PAYO stock today is much more appealing than I previously thought. Importantly, this expansion is expected to be accompanied by higher profit margins, which I believe will drive valuations higher (not included in my base case as I want to be conservative). PAYO has historically traded at an all-time high of 2.8x forward revenue. If it reverts to that average, the upside potential increases to 60%.

{kind=link}

Summary

In conclusion, PYO 4Q results and 2023 guidance show a positive outlook for the company from a business, sentiment and capital flow perspective. The company is set to benefit from higher interest rates and the monetization of customer funds, which will allow for significant tailwinds to the top and bottom line. Furthermore, PAYO strategic shift towards larger, more profitable customers and its focus on expanding its product offerings, particularly in areas like B2B payments and working capital, present significant growth opportunities for the company. With the projected revenue growth and higher profit margins, I shift my rating to a buy.

For further details see:

Payoneer Global: Strong FY 2023 Outlook And Long-Term Trends