PAYO - Payoneer: Loving Higher Rates

Summary

- Payoneer reported another strong quarter and is now guiding to 2022 revenues of $585 million easily topping original SPAC targets.

- The company is seeing a $20+ million boost to revenue in the 2H of the year.

- The stock trades at just 3x EV/S targets for 2023.

Payoneer Global ( PAYO ) is a prime example of a company where higher interest rates provide a solid tailwind for the business. The global payments company continues to fly past estimates, even in Ukraine where business sits at 75% of pre-war forecasts. My investment thesis remains ultra Bullish on the stock, as management continues to deliver blowout results while the stock languishes.

Interest Rate Tailwind

While a lot of SPACs have run into hiccups since closing their deals, Payoneer continues to power through all of their problems. Oddly though, the stock trades far below the deal price at $10 due to some Ukraine induced weakness perceived as a corporate related problem.

While the market was distracted on numbers cut due to Ukraine, Payoneer just guided to 2022 revenue actually topping the levels forecast for the year prior to the war. The company has seen a strong shift in the business towards new products with a higher take rate while the lower take rate e-commerce business has slowed with tough comps.

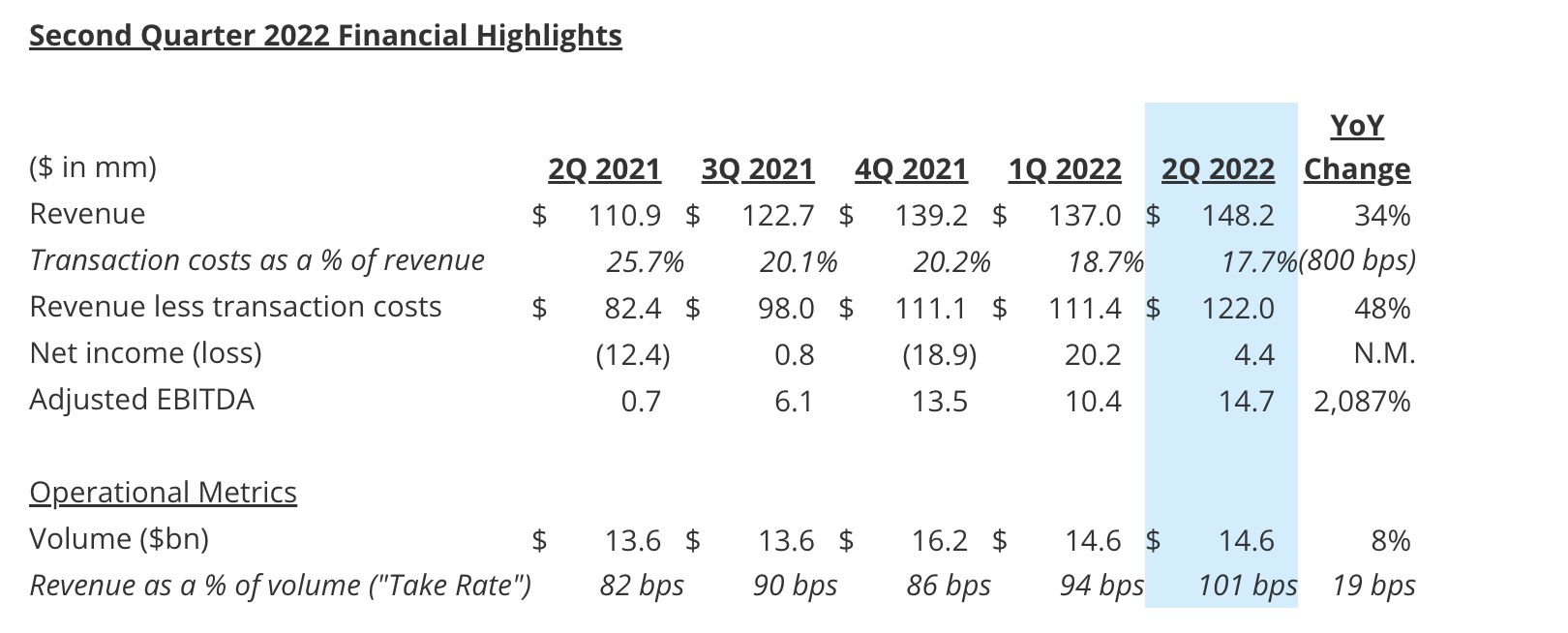

The primary benefit is that Payoneer has seen what amounts to net revenues surging 48% on just an 8% boost in payment volumes. Revenues are up due to a 19 bps point boost in the take rate to 101 bps while transaction costs as a percentage of revenues dipped 800 bps to just 17.7%. The positive outcome was net revenue jumping to $122.0 million from $92.4 million last year.

{kind=link}

While the company continues driving volume growth despite the e-commerce headwinds, the flip side is a business seeing a boost from higher interest rates. Payoneer now has $5.1 billion in customer funds with half the assets earning interest with no costs.

The global payments company saw Q2'22 interest income reach $3.5 million, up from just $0.7 million last Q2. On the earnings call , CFO Michael Levin forecast the company earning over $20 million in interest income in the 2H of the year:

Not all of our balances are in U.S. dollars. So a portion of balances are being used operationally. Others are – the balances are non-USD. So that’s why not all of it is interest earning. We do focus on trying to optimize. We do think that it will be meaningful in the second half and continue to climb with a very strong exit rate. And I think from a – where we think things you do to sort of math on current balances, you’re probably coming out to low to mid-20s in the second half in terms of [indiscernible].

After the strong Q2 and combined with quarterly interest income jumping to $10+ million, the updated Payoneer guidance appears low. The company guided to revenue between $580 to $590 million.

Payoneer generated $285 million in the 1H of the year with guidance suggesting revenues of $150 million per quarter in the 2H. The global payments firm would generate limited revenue growth while still getting a solid profit boost from the higher financial income.

Still Cheap

The stock has rallied off the $3 lows, but Payoneer still trades far below the prior levels. The company has a market cap of ~$2.8 billion based on ~429 million diluted shares outstanding with an additional 65 million warrants and earn-out shares exercisable when the stock exceeds $11.50 (a large gain from current $6.50 levels).

Analysts now forecast the global payments firm generating $712 million in revenue next year. The stock trades at just 4x 2023 revenue targets plus the EV is even cheaper with a cash balance of $492 million.

Payoneer has bounced off the lows, but the company has produced the results warranting the SPAC trading above the $10 deal level. The company originally guided to 2022 revenues of just $540 million, and despite the impacts in Ukraine, Payoneer is now guiding up at least $40 million for the year. Analysts are now forecasting additional revenue growth of $120 million in 2023 for 20% growth.

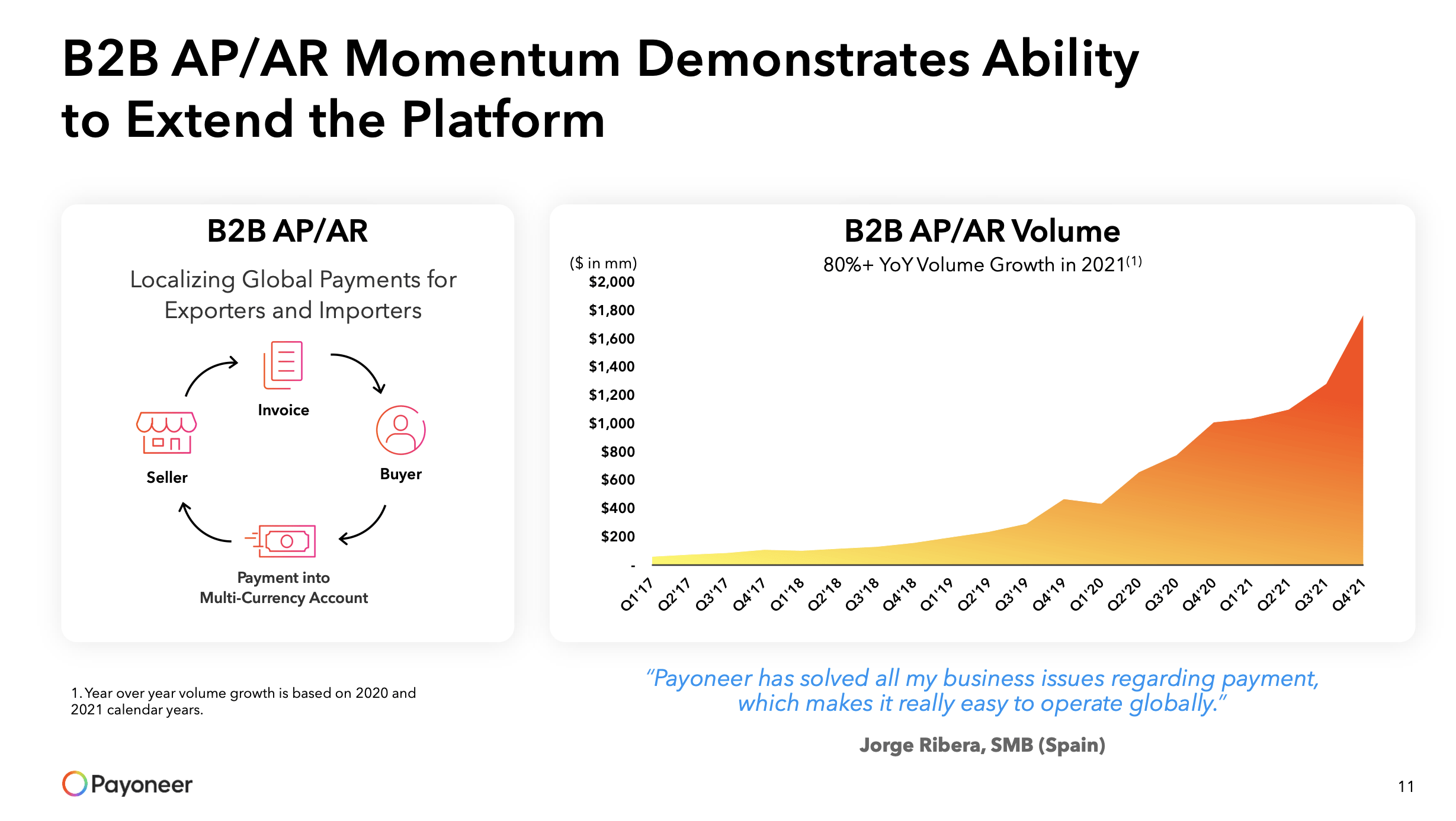

The stock shouldn't be trading at a discount here after generating such strong results. Payoneer continues to buildout a powerful platform with new products launched such as the virtual Payoneer Commercial Mastercard and now Payoneer Checkout. The B2B AP/AR product wasn't even a material volume producer entering 2019 and the payment volume has grown close to 10 fold during the 3-year period.

{kind=link}

As the company signs up new customers for this product, Payoneer attracts additional customers that interact with the Payoneer platform in a strong flywheel effect.

Takeaway

The key investor takeaway is that Payoneer is crazy cheap as the former SPAC deal continues to surpass all prior financial targets. The stock shouldn't trade with a forward EV/S multiple of 3x while higher interest rates are driving revenues higher, providing a bonus tailwind.

For further details see:

Payoneer: Loving Higher Rates