PAYO - Payoneer Q4 Earnings: Robust Growth

Summary

- Payoneer Global Inc. is down over 30% since its SPAC merger.

- The fintech company operates in a huge market and is benefiting from strong tailwinds.

- Payoneer Global Inc. fourth-quarter earnings and guidance were extremely strong despite facing a tough macro backdrop.

- A forward EV/EBITDA of <15x looks very reasonable considering its growth and prospects.

- I rate Payoneer Global Inc. as a buy.

Investment Thesis

Payoneer Global Inc. (PAYO) went public back in 2021 through a SPAC merger with Olympus Acquisition Corp. However, it has been performing poorly, with PAYO shares down over 30% from its IPO price, as the market pulled back significantly last year due to inflation worries and rising rates.

I believe this offers a buying opportunity for long-term investors as Payoneer Global continues to execute. It operates in the huge and growing fintech market that should continue to provide tailwinds. Its latest earnings result is once again superb, with growth and guidance both exceeding expectations. The current valuation also looks pretty compelling considering its prospects and growth. Therefore, I rate Payoneer Global Inc. as a buy.

Why Payoneer?

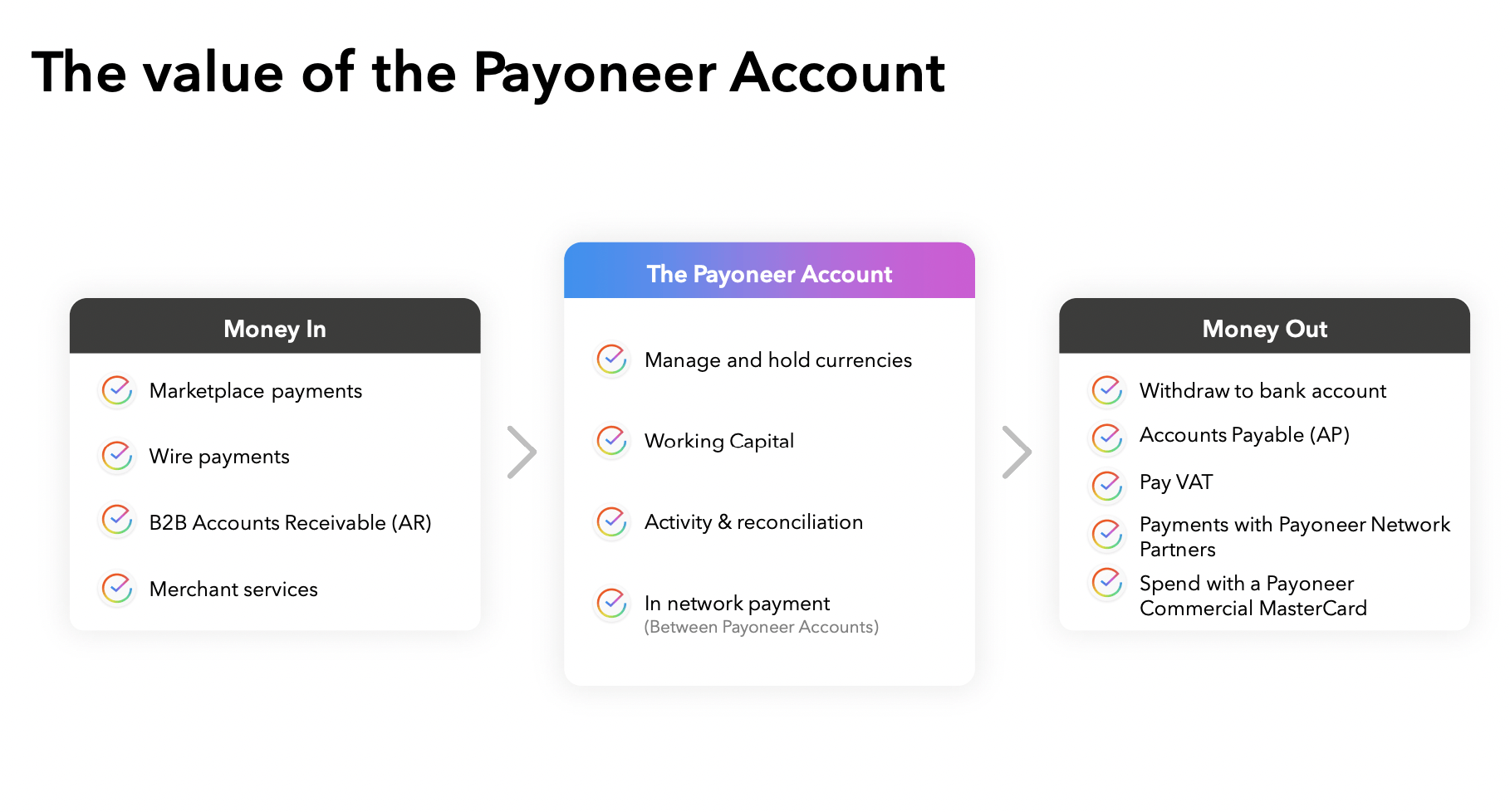

Payoneer Global Inc. is a U.S.-based fintech company founded back in 2004. The company provides users with multi-currency accounts for making payments and receiving funds globally. The account also comes with other features such as managing AR (accounts receivable)/AP (accounts payable), virtual cards, access to capital, and more. It is currently available in over 190 countries and can be used in different popular marketplaces like Shopify ( SHOP ), Airbnb ( ABNB ), and Fiverr ( FVRR ).

The company is very popular among SMBs (small and medium businesses) operating a digital business, as it is much more cost-efficient and convenient compared to wire transfer. A lot of users are shifting from legacy platforms to modern platforms like Payoneer in order to improve their operating efficiency. Companies like PayPal Holdings, Inc. ( PYPL ) are another option, but their transaction fees are usually 1% to 2% higher and it only support 26 currencies, while Payoneer supports 150 currencies.

John Caplan, CEO, on market opportunity

SMBs that transact globally have cross-border operations, expenses and currencies to manage. They need a holistic and cost-effective solution for managing their global financial operations and accessing the capital they need to grow their business, yet they are underserved by the traditional banking and financial system. In fact, approximately 90% of B2B payment volume relies on legacy payment methods. Payoneer provides these SMBs with the tools and services they need to grow their businesses.

The market opportunity for Payoneer is massive. Besides the shift from legacy solutions to modern solutions, it is also benefiting from the increasing popularity of fast-growing industries such as e-commerce, online freelancing, content creation, and more. For instance, the e-commerce market is forecasted to grow from $4.11 trillion in 2023 to $6.35 trillion in 2027, representing a strong CAGR (compounded annual growth rate) of 11.5%, according to Statista . The rapid expansion in these markets continues to increase the need for money movement solutions, which should generate solid tailwinds for the company.

{kind=link}

Q4 Earnings

Payoneer Global Inc. announced its fourth-quarter earnings this week and it reported a strong beat and raise, with guidance blowing past expectations.

Revenue for the quarter was $183.6 million, up 31.8% YoY (year over year) from $139.2 million. This beat consensus by $12.7 million. Volume increased 5% from $16.2 billion to $16.9 billion while the take rate grew 23 basis points from 86 basis points to 109 basis points. The growth is driven by the recovery in the travel sector and strong traction in AR/AP volume, which was up 10% YoY. Customer funds held by Payoneer were $5.8 billion, up $1.4 billion from the prior year. The company was able to leverage higher interest rates and generate $36 million of interest income from customers' balances.

Costs grew much slower than revenue. Transaction costs were $30.4 million, up only 8.2% YoY compared to $28.1 million. This resulted in gross profit increasing 37.9% YoY from $111.1 million to $153.2 million. The gross profit margin also expanded 460 basis points from 79.8% to 84.4%.

Operating expenses for the quarter grew 40% YoY to $162 million. Most of the increase is attributed to S&M (sales and marketing) spending which grew 54% from $33.9 million to $52.2 million, as the company continues to scale its AR/AP segment. The management team mentioned it will not continue to spend in 2023, which is reassuring. Net loss improved by 46.6% from $(18.9) million to $(10.1) million. Net loss per share was $(0.03) compared to $(0.06). The balance sheet was very healthy, with $543 million in cash and only $24.8 million in debt.

The company also initiated guidance for FY23, and it was extremely upbeat. It expects revenue to be $800 million-$810 million, significantly above the street consensus of $738 million. The midpoint represents a growth rate of 28% YoY. The adjusted EBITDA is expected to be $120 million-$130 million, representing a whopping growth of 157% at the midpoint. The bottom line guide is very impressive, as it indicates the adjusted EBITDA margin doubling from FY22.

Investors Takeaway

Overall, this quarter's result was surprisingly strong, especially for the guidance. Most companies are guiding flat or down due to macro uncertainties but Payoneer Global Inc. actually raised it meaningfully, which signals the company's strong momentum and confidence in its growth opportunities. The massive addressable market and the increasing popularity of digital businesses should continue to provide tailwinds moving forward.

Despite the recent rally, Payoneer Global Inc.'s valuation still looks very reasonable in my opinion. Using the midpoint of its guidance, it is currently trading at an fwd EV/EBITDA and fwd EV/sales of just 14.7x and 2.3x, which is pretty cheap considering its growth rates of 30%+ and gross margins of 80%+. The company's bottom line should also start to scale quickly as it cuts back on spending and investment. I believe there are still solid upsides, and Payoneer Global Inc. should continue to perform well from here onwards.

For further details see:

Payoneer Q4 Earnings: Robust Growth