PAYO - Payoneer: Time To Exit SPAC Penalty Box

Summary

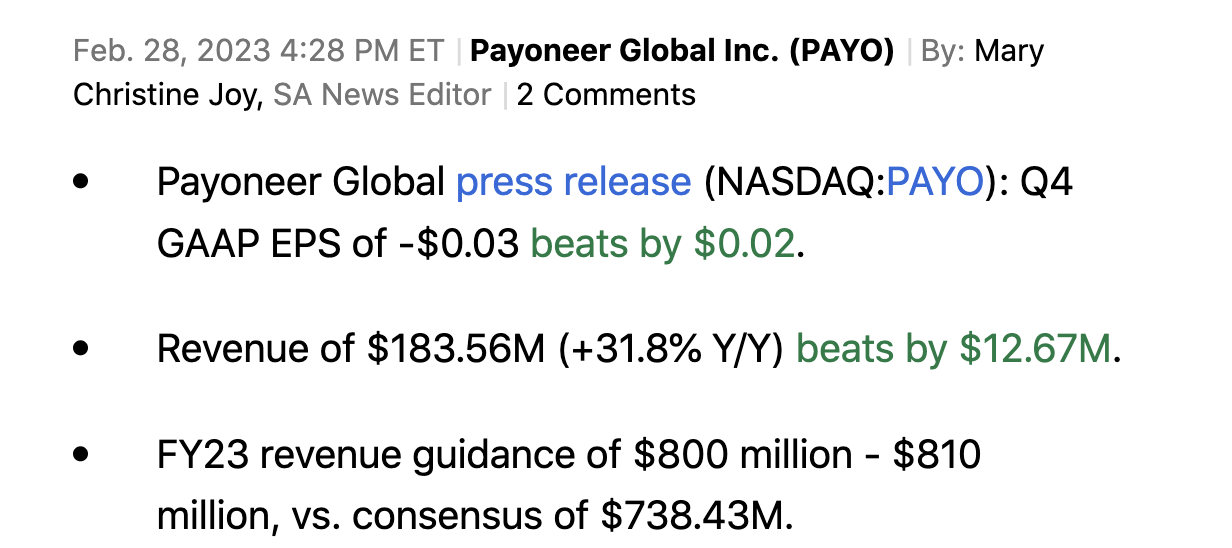

- Payoneer Global Inc. reported Q4 2022 metrics that beat analyst targets.

- The global payments firm guided to 2023 revenues far above analyst targets.

- Payoneer Global stock only trades at 3x forward EV/S targets despite consistent 30% growth rates.

A lot of former SPACs are starting to exit the penalty box due to strong fundamentals. Payoneer Global Inc. ( PAYO ) is primed for the next company to rally back to the $10 SPAC price after spending a year in purgatory despite rather solid results. My investment thesis remains ultra Bullish on the global payments firm executing on strong growth not reflected in the current stock price.

Source: Finviz

Solid Execution

Quarter after quarter, Payoneer reports consistently strong revenue growth. The company continues to garner additional payment volumes, but most importantly Payoneer has transitioned to additional products with higher take rates.

For Q4 , the fintech boosted revenues by nearly 32% to reach quarterly revenues of $183.6 million . The GAAP earnings aren't very useful to a small cap, but Payoneer did produce a solid adjusted EBITDA in the quarter of $11 million.

{kind=link}

Even better, the company guided to a massive 2023 revenue beat. Payoneer forecast revenues to beat consensus estimates by ~10% and the company even topped the bullish forecast from Jefferies with a $788 million revenue target.

The global payments company has constantly beaten analyst targets the last year after the war in Ukraine initially disrupted the business. Now, Payoneer is seeing a boost from higher income from customer deposits providing a substantial upside from when global interest rates were 0%.

Management guided to $180 million in such revenues for 2023. In the last quarter alone, customer deposits soared $800 million to $5.8 billion. At the end of 2021, the customer balances were $4.4 billion, providing 32% growth while interest rates soared.

Payoneer had originally brought up the upside from customer funds back in early 2022. The company had forecast an annualized rate of ~$40 million and ended up generating $36 million of interest income in Q4'22 alone, up from just $1 million in the quarter to end 2021. While rates aren't likely to rise much from these levels, the company should continue growing customer funds and optimizing the income earned.

Still Priced Like A Failed SPAC

While SPACs initially started off as hot items, any company going public via this method were priced at discounted valuations in 2022 and into 2023. The recent success of Hims & Hers Health ( HIMS ) and Luminar Technologies ( LAZR ) have highlighted how former SPACs can eventually exit the penalty box and trade back towards $10.

Payoneer should see this scenario unfold in 2023 following the massive Q4 beat and guide up for 2023. The stock has a listed market cap of ~$2.7 billion at a pre-market trading price of $6.50 and an enterprise value below $2.2 billion due to a cash balance of $543 million.

The global payments firm has up to an additional 117.8 million shares outstanding via options, RSUs, warrants and earn-out shares. For a diluted share count, the 62.6 million options, RSUs and private warrants are all mostly exercisable at prices far below the current stock price and should be included in share counts. The 25.2 million public warrants aren't exercisable until $11.50 per share and shouldn't impact the EV due to the company collecting the cash on those exercises. Payoneer has an additional 30.0 million earn-out shares not issued until the stock traded above $15 and $17 over a 30 trading day period. These shares shouldn't be included in the diluted share count unless Payoneer reaches those price level.

The stock is crazy cheap here with an EV of ~$2.2 billion and a 2023 revenue target of $805 million. Very few companies guiding to 30% sales growth trade at an EV/S multiple below 3x.

Even better, Payoneer is now targeting 2023 adjusted EBITDA of $125 million, making the company highly profitable going forward. The stock trades up at ~18x 2023 EBITDA targets, but the financial metric is set to grow 160% in the year, far above the multiple.

Takeaway

The key investor takeaway is that Payoneer Global Inc. continues to fire away at building a global payments company with strong network benefits in attracting new customers. Payoneer Global stock is cheap primarily due to going public via a SPAC in 2021, and the stock should exit the penalty box this year.

For further details see:

Payoneer: Time To Exit SPAC Penalty Box