PDCE - PDC Energy: 2023 FCF Estimated At $900 Million

2023-04-25 22:17:59 ET

Summary

- PDC Energy looks capable of generating approximately $900 million in free cash flow during 2023 at current strip.

- This is more than the $825 million it estimated in late February, as current strip is a bit more favorable than the $75 oil and $3 gas that it assumed.

- This free cash flow would allow PDC to reduce its share count to around 83 million by the end of 2023 along with 0.4x leverage.

- Inventory situation looks fine in the near term, but it may run out of Delaware Basin inventory by 2028.

- It is also mainly developing its better-quality DJ Basin inventory in the near term as well.

PDC Energy ( PDCE ) is now expected to generate just over $900 million in free cash flow during 2023. This is based on current strip of approximately $77 WTI oil and $2.70 Henry Hub gas. This should allow PDC to pay off most of its credit facility debt as well as reduce its share count to around 83 million by the end of 2023.

PDC's projected free cash flow is a bit lower than my expectations from early February due to slight cost increases plus slightly weaker commodity prices. However, PDC's 2023 production guidance is also a bit stronger than I previously expected.

I now believe PDCE stock is worth approximately $80 to $85 per share in a long-term $75 WTI oil and $3.75 Henry Hub gas environment.

2023 Outlook

PDC expects approximately 260,000 BOEPD in average production during 2023, including 84,000 barrels per day in oil production. This is around 2% higher total production and 1% higher oil production compared to what I had modeled for PDC before.

At the current 2023 strip of roughly $77 WTI and $2.70 Henry Hub natural gas, PDC is projected to generate $3.271 billion in revenues including the effect of hedges. PDC's 2023 hedges have an estimated value of negative $80 million at this time.

| Barrels/Mcf |

| $ Per Barrel/Mcf (Realized) |

| $ Million |

| Oil (Barrels) |

| 30,660,000 |

| $74.70 |

| $2,290 |

| NGLs (Barrels) |

| 26,980,800 |

| $22.50 |

| $607 |

| Natural Gas [MCF] |

| 223,555,200 |

| $2.03 |

| $454 |

| Hedge Value |

| -$80 |

| Total Revenue |

| $3,271 |

PDC expects its capital expenditure budget to be around $1.425 billion. This leads to a projection that it can generate $901 million in free cash flow in 2023 at current strip. This includes the impact of a small amount of cash income taxes.

PDC is devoting 80% of its capex budget towards the Wattenberg Field where it intends to run a three rig program. The other 20% is going towards the Delaware Basin where it intends to run a one rig program.

| $ Million |

| Lease Operating Expense |

| $305 |

| Transportation, Gathering and Processing |

| $142 |

| Production Taxes |

| $251 |

| G&A |

| $162 |

| Cash Interest |

| $70 |

| Capital Expenditures |

| $1,425 |

| Cash Taxes |

| $15 |

| Total Expenses |

| $2,370 |

PDC previously estimated that it could generate $825 million in free cash flow in 2023. This was at slightly lower overall commodity prices of $75 WTI oil, $3 Henry Hub natural gas and $20 NGLs though.

Potential Uses Of Cash

PDC increased its quarterly cash dividend to $0.40 per share . This could result in approximately $138 million in base dividends being paid out during 2023. PDC intends to return at least 60% of its post base dividend free cash flow to shareholders via share repurchases and potentially a year-end special dividend.

Thus PDC could put $458 million (at 60% of post base dividend FCF) towards share repurchases (and special dividends) during 2023, leaving $305 million for debt reduction.

The share repurchases could reduce PDC's share count to approximately 83 million by the end of 2023. It is authorized to spend $2 billion repurchasing shares and had used close to $800 million of that capacity by the end of 2022.

PDC ended 2022 with $370 million in credit facility debt (along with $6 million in cash on hand). It also has $200 million in 6.125% unsecured notes due September 2024 and $750 million in 5.75% unsecured notes due May 2026 outstanding.

The projected debt reduction would pay off most of its credit facility by the end of 2023 and leave it with approximately $1.01 billion in net debt by the end of the year and leverage of 0.4x. It also appears to be in good shape to deal with its September 2024 notes.

Inventory Situation

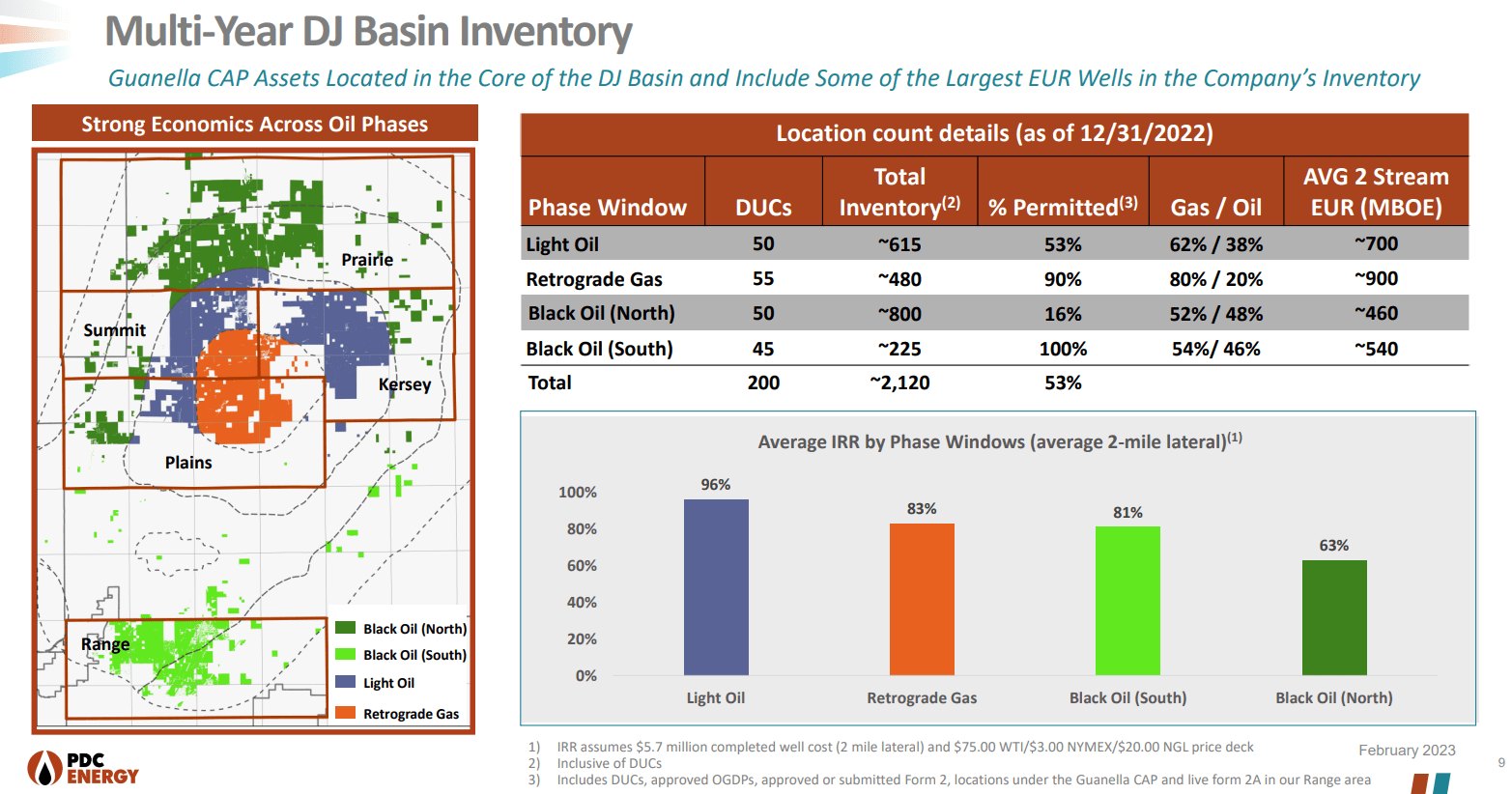

PDC appears to be in a good situation with regards to its permits. It has approved DJ Basin inventory (including approved Comprehensive Area Plans) to last into 2028 at its 2023 development pace of 200 to 225 wells.

{kind=link}

The expected returns on its near-term development inventory are strong at $75 WTI oil and $3 Henry Hub gas, as it has received permits for a higher proportion of its better inventory. One thing to note is that its unpermitted inventory is typically weaker. PDC's Black Oil (North) locations have the lowest estimated IRRs and that area accounts for 67% of its unpermitted inventory compared to 12% of its permitted inventory.

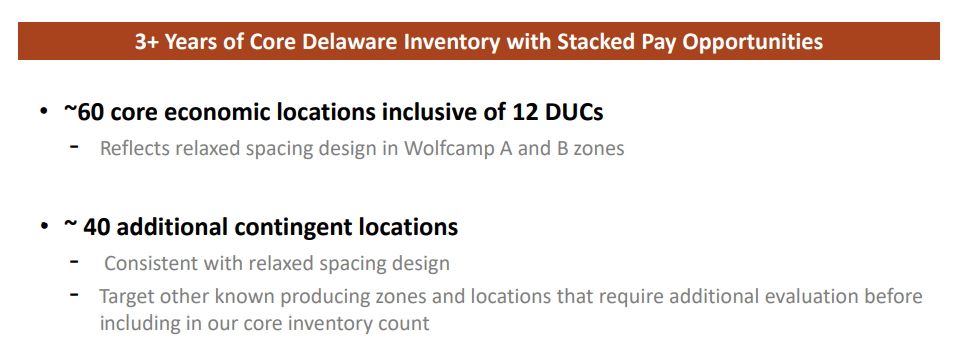

PDC may also be running low on its core Delaware Basin inventory, with around 3 years of core inventory at its 2023 development pace of 15 to 25 wells. It may have another two additional years of Delaware Basin inventory pending evaluation.

{kind=link}

So without further acquisitions, PDC may end up having used up its Delaware Basin inventory by 2028 while also needing to develop its weaker DJ Basin inventory around that time. This is a challenge many producers are facing in terms of using up their best inventory though.

Notes On Valuation

I've modified my long-term commodity price estimates to $75 WTI oil and $3.75 Henry Hub natural gas. At those commodity prices and 83 million outstanding shares at the end of 2023, I estimate PDC's value at approximately $80 to $85. This also assumes that PDC can generate approximately $900 million in free cash flow in 2023.

At $75 oil and $3.75 gas, PDC Energy should also be able to maintain production levels and generate around $13 per share in unhedged free cash flow, before the impact of cash income taxes.

Conclusion

PDC Energy looks capable of generating around $900 million in free cash flow at current strip prices. This would allow it to reduce its leverage to around 0.4x by the end of 2023 while also repurchasing shares to bring its share count down to around 83 million.

PDC's ability to generate a substantial amount ($13 per share) of free cash flow at my long-term commodity prices (including $75 oil) helps support an estimated value of $80 to $85 per share. PDC's inventory situation looks good until around 2028, but after that point it may run out of Delaware Basin inventory, while its remaining DJ Basin inventory would skew towards lower quality locations.

For further details see:

PDC Energy: 2023 FCF Estimated At $900 Million