WMB - PDT: Keep An Eye On This Recession-Resistant CEF

Summary

- The high inflation rate is straining the finances of many American households, especially younger ones.

- John Hancock Premium Dividend Fund invests in a blended portfolio of securities that should be reasonably recession-resistant.

- The PDT fund's blended portfolio should be reasonably stable over time but unfortunately, the Fed's policy over the past decade has made stocks and bonds correlate together.

- The closed-end fund failed to cover its distribution in 2022, but it did manage to cover it over the trailing two-year period.

- The price is reasonable, although the current discount is quite small.

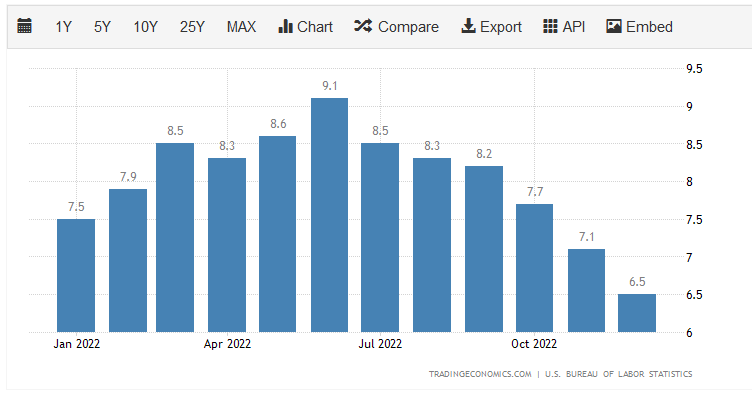

One of the biggest problems that Americans have been suffering is the incredibly high rate of inflation throughout the economy. Although the rate of inflation has been coming down over the past few months, there is still no month in which the consumer price index did not increase by at least 6.5% compared to the prior year:

{kind=link}

This forty-year high has made it very difficult for those that are looking for a safe source of income as bank savings accounts and even certificates of deposit are paying negative rates in spite of the Federal Reserve’s aggressive rate hikes. More importantly, the rising cost of living has made it very difficult for people to make ends meet. In fact, a recent Prudential Pulse survey reveals that about 77% of Millennials have either entered the gig economy or are planning to do so as a means to supplement their incomes and obtain the money that they need to pay their bills. The problem is particularly pronounced among those of limited income as much of the inflation has been centered on food and energy, which are necessities.

Fortunately, as investors, we can put our money to work for us, reducing the need to take on second jobs to boost our incomes. One of the best ways to do this is to purchase shares of a closed-end fund ("CEF") that specializes in the generation of income. This is a somewhat underfollowed asset class, but some of these funds can boast yields that are higher than pretty much anything else in the market. This is because these funds enjoy the benefit of professional management teams that are able to employ certain strategies that boost their yields beyond that of any of the underlying assets.

In this article, we will discuss the John Hancock Premium Dividend Fund ( PDT ), which is one fund that falls into this category. As of the time of writing, the fund has an 8.97% yield, which far exceeds the S&P 500 Index ( SPY ) as well as pretty much any other index fund. I have discussed this fund before, and admittedly the overall thesis has not changed. This is basically a fund that you purchase as a way to get extra income. However, a few months have passed since that last article was written, so a few things as changed. Most importantly, the fund has released an updated financial report. As such, this article will focus specifically on these changes and provide an updated analysis of the fund’s finances.

About The Fund

According to the fund’s webpage , the John Hancock Premium Dividend Fund has the stated objective of providing its investors with a high level of current income. The fund is also aiming to grow its capital at a modest rate. This differentiates it somewhat from funds that aim to maximize their capital gains as well as funds that simply want to preserve their principal and generate as high a yield as possible. As such, this fund can likely act as a way to reduce the risk inherent in an aggressive growth portfolio. The fund’s strategy itself reflects this as it invests in both common equities and fixed-income securities:

CEF Connect

As we can see, the fund employs a relatively balanced mix of fixed-income and common equities. This is reasonable given its objective. After all, common stock is the usual investment vehicle for people seeing growth while preferred stock, and especially bonds usually have higher yields but fewer capital gains potential. Fixed-income securities are also usually somewhat more stable than stocks because they have no inherent link to the performance of the issuing company. After all, a company does not increase the payments that it makes to its creditors when its profits increase and it does not reduce the payments that it makes to its creditors when profits go down.

Historically, fixed-income securities tend to go down when the Federal Reserve is raising interest rates but stocks actually go up since the Federal Reserve only raises rates when it is trying to cool off an overheating economy. The reverse is also historically true as interest rate cuts cause bond prices to rise but should cause stock prices to fall as that is a sign of a weak economy. Unfortunately, that was not the case in 2022, as the economy has become addicted to free money after the Federal Reserve’s rather irresponsible policies over the past decade. Thus, these two asset classes are now correlated, which makes this fund’s portfolio not as safe as it once would have been. Nevertheless, the fund should still be less volatile than all-stock portfolios over time.

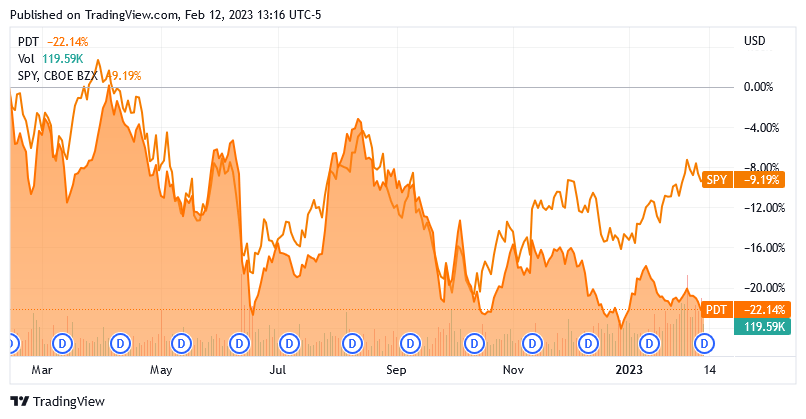

This has not really been the case over the past year though. As we can see here, the fund moved somewhat similarly to the S&P 500 Index ( SPY ) over most of the past year but it did not rebound this year as the market did:

{kind=link}

This unfortunately shows that fixed-income securities and common stocks are now correlated with each other. This also shows that the John Hancock Premium Dividend Fund may be thought of as a fixed-income fund despite the fact that more than half of the portfolio is in common stocks.

The S&P 500 Index (SP500) is not the best index to compare this fund to, however. This is partly because of the fund’s almost even split between common stocks and fixed income. In addition, the John Hancock Premium Dividend Fund states that it invests at least 80% of its assets into assets that pay a dividend. That is very different from the broader market index that includes a substantial number of non-dividend-paying companies. The closed-end fund has, in fact, beaten its benchmark blended index in several historical periods, including over the course of 2022:

{kind=link}

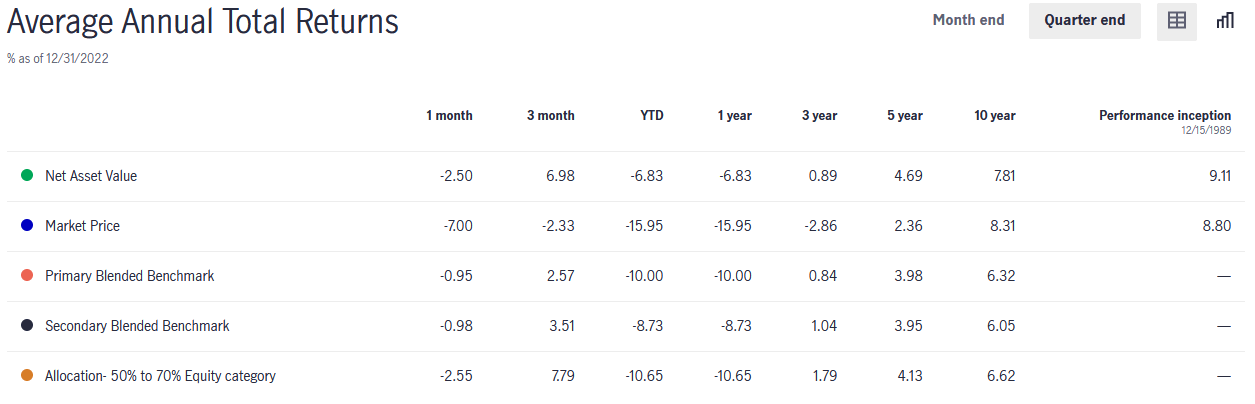

The most important performance measure for the fund is net asset value, not market price. That is because the net asset value is how the portfolio itself actually performed. As we can clearly see, the portfolio performed much better than the fund’s market price did over most of the past year. This is an unfortunate characteristic of closed-end funds. They can sometimes perform very differently than the portfolio itself. However, this performance difference can sometimes represent an opportunity for savvy investors, as we will see later in this article.

As stated earlier, the John Hancock Premium Dividend Fund states that it invests at least 80% of its assets into dividend-paying stocks. A look at the fund’s largest positions reveals that it is certainly focusing on these assets:

{kind=link}

The largest positions in the fund are mostly the same as when we last reviewed it, although there is one notable change. This is that NextEra Energy’s ( NEE ) preferred stock was removed and replaced with Dominion Energy's ( D ) common stock. This is a reasonable change as it basically represents a swap from a utility preferred share to a utility common share. It might have reduced the fund’s income slightly though as the NextEra Energy preferred stock was theoretically yielding 6.219% compared to the 4.48% yield of Dominion Energy. As both of these positions were a fairly small percentage of the fund’s total holdings though, it is unlikely to make a huge difference.

The fact that so few of the fund’s positions have changed over the past three months will likely lead one to believe that the fund has a remarkably low turnover rate. This is certainly true as the John Hancock Premium Dividend Fund’s 16.00% annual turnover is one of the lowest that I have ever seen among equity funds. It is not the lowest for a fixed-income fund but it is nowhere close to the highest in the sector, either. The reason that this is important is that it costs money to trade stocks or other assets. These expenses are billed directly to the shareholders of the fund, which creates a drag on the portfolio and makes management’s job more difficult. This is because the fund’s management needs to produce a sufficient return to cover these expenses and still have enough left over to deliver a return that is reasonably in line with what the shareholders expect. There are very few management teams that manage to accomplish this task on a consistent basis, which is one of the reasons for the popularity of index funds. This fund is not really too bad here and, as we have already seen, it generally performs pretty well against two blended indices.

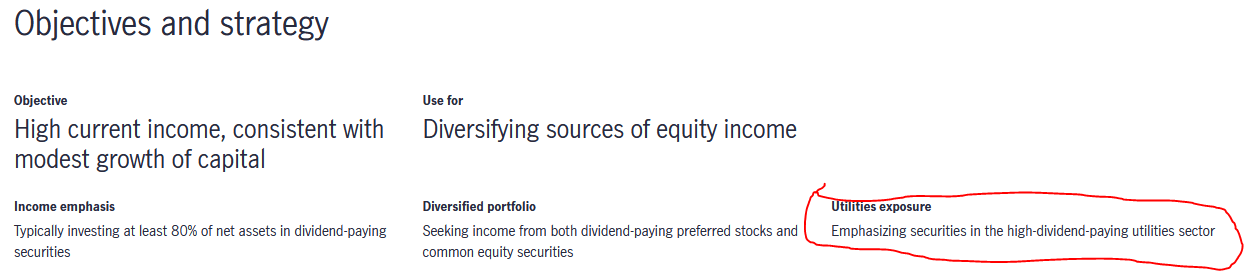

One thing that an eagle-eyed reader will likely notice by looking at the largest positions listed above is that many of the fund’s assets are utility stocks. This is no accident as the fund states that it “emphasizes securities in the high-yielding securities sector.”

{kind=link}

There are some advantages to these securities for dividend investors. Perhaps the most significant of these is that utility companies typically enjoy remarkably stable cash flows regardless of the conditions in the broader economy. I have stated this in numerous previous articles. It is caused by the fact that these companies provide a service that most people consider to be a necessity in the modern world. As such, they usually prioritize paying their utility bills ahead of discretionary expenses during times when money gets tight. As was mentioned in the introduction, a large number of people throughout the United States have been forced to take on second jobs or perform odd tasks just to make ends meet today so saying that money is getting tight is an apt description of the situation faced by many households today. In such an environment, it can be a good idea to hold companies that are unlikely to be hurt much by such a situation.

Despite that perceived emphasis, only 45.51% of the portfolio is invested in the utility sector. However, we also see some high-yielding midstream companies like The Williams Companies ( WMB ) among the fund’s holdings. These companies are not utilities but they also enjoy the same general cash flow stability. This is due to their business model that is underpinned by long-term contracts with their customers. These contracts essentially guarantee a certain baseline cash flow to the company. That is great for income investors because cash flow is ultimately what funds a company’s dividends. Thus, stable cash flows provide a great deal of support and sustainability to a dividend and by extension to the fund’s income that ultimately flows through to the investors.

Leverage

In the introduction to this article, I stated that closed-end funds have the ability to utilize certain strategies that boost their yields beyond that of the underlying assets. One of the strategies that is utilized by the John Hancock Premium Dividend Fund is leverage. Basically, the fund borrows money and uses that borrowed money to purchase income-producing common equities and fixed-income securities. As long as the purchased assets generate a higher return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the overall yield of the portfolio. As the fund is able to borrow at institutional rates, which are significantly lower than retail rates, this is not a particularly difficult task to accomplish.

However, the use of debt is a double-edged sword because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage as that would expose us to too much risk. I do not typically like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. The John Hancock Premium Dividend Fund’s levered assets comprise 36.47% of its assets as of the time of writing so it does exceed this level. As such, there may be some concerns that the fund is exposing its investors to an excessive amount of risk through its leverage strategy. This is something that we want to keep an eye on, particularly if the market weakens again since the fund may decline more than might be expected given its conservative portfolio.

Distribution Analysis

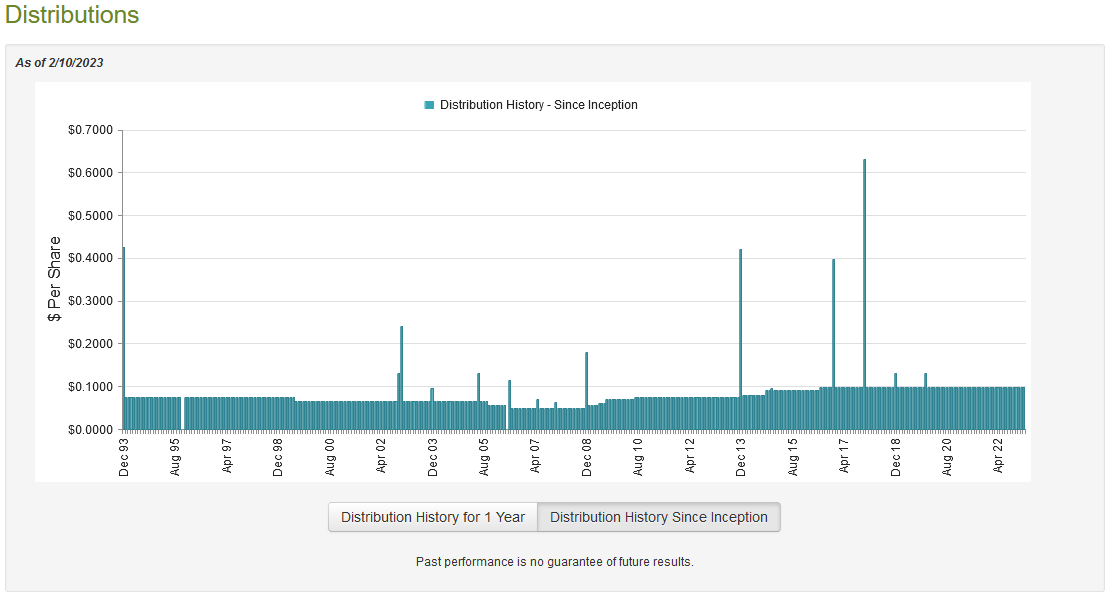

As stated earlier in this article, the primary objective of the John Hancock Premium Dividend Fund is to provide its investors with a high level of current income. It invests in a blended portfolio of dividend-paying assets to accomplish this goal and then applies leverage to boost the effective yield. As such, we might assume that the fund has a fairly high yield at the current price. This is certainly the case as it pays out a monthly distribution of $0.0975 per share ($1.17 per share annually), which gives it an 8.97% yield at the current price. The fund has been fairly consistent about its payout over the years since the financial crisis as it has slowly raised its distribution since 2008 with no cuts:

{kind=link}

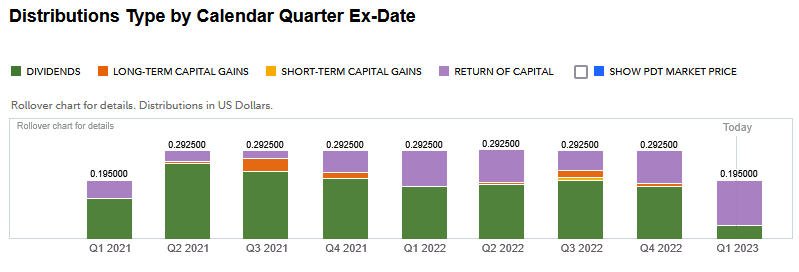

This will probably appeal to those investors that are looking for a stable and secure source of monthly income that they can use to pay their bills or finance other expenses. This fits pretty well with our overall thesis as presented in the introduction as well. Unfortunately, the fund has been issuing a great many return of capital distributions over the past several months, which might be concerning:

{kind=link}

The reason why this may be concerning is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be considered a return of capital. Chief among these is the distribution of unrealized capital gains, which is something that this fund might obviously be doing. As such, we should investigate exactly how it is financing these distributions in order to determine how sustainable they are likely to be.

Fortunately, we do have a very recent document that we can consult for that purpose. The fund’s most recent financial report corresponds to the full-year period that ended on October 31, 2022. Although this fund will not include any information about the fund’s performance over the past three months, it is still far newer than the report that we had available the last time that we discussed this fund. In addition, the market trouble in 2022 started in March when the Federal Reserve started hiking interest rates so this should give us a good idea of how well the fund performed during the aftermath of that event. During the full-year period, the fund received a total of $37,814,629 in dividends and $14,401,781 in interest from the assets in its portfolio. After we subtract out the foreign withholding taxes that the fund paid, it had a total investment income of $52,000,265 over the year. It paid its expenses out of this amount, which left it with $35,285,384 available for the shareholders. That was unfortunately not enough to cover the $57,179,674 that the fund paid out in distributions during the period. At first glance, this is likely to be concerning as the fund clearly failed to cover its distribution out of net investment income.

However, there are other ways that the fund can finance its distribution. For example, it can earn capital gains and pay those out to investors. That is a common strategy used by many closed-end funds. The fund had limited success at that task during the period as it did achieve net realized gains of $20,077,718 during the period. This was more than offset by $109,947,904 net unrealized losses. Overall, the fund’s assets under management declined by $107,298,715 after accounting for all inflows and outflows. This is concerning as the fund clearly failed to cover its distributions. In fact, even the net realized capital gains plus the net investment income is not enough to cover the distributions that were paid out, although the fund did get pretty close. With that said, the fund did have slightly more on October 31, 2022, than it had on November 1, 2020. Thus, it did manage to earn enough over the two-year period to cover all of its distributions over the period. The big test will come over the next year as a weak market could spell trouble for the fund’s ability to sustain the distribution. We will want to watch this.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the John Hancock Premium Dividend Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because this scenario implies that we are acquiring the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of February 9, 2023 (the most recent date for which data is currently available), the John Hancock Premium Dividend Fund had a net asset value of $13.21 per share but the shares currently trade for $13.05 each. This gives the shares a 1.21% discount to the net asset value at the current price. This is not quite as good as the 2.36% discount that the shares have had on average over the past month so it might make sense to watch the shares patiently for a better entry point to present itself. With that said, though, generally speaking, any discount represents an acceptable price to purchase a fund.

Conclusion

In conclusion, the John Hancock Premium Dividend Fund has a decent strategy in the current environment. As many households are increasingly squeezed for money, the fund’s focus on utilities and other companies that should prove to be resistant to declines in consumer spending should prove to be a solid strategy. Unfortunately, the fund may struggle to maintain its distribution if 2023 does not prove to be a strong bull market. John Hancock Premium Dividend Fund’s price is decent, though, and it has delivered reasonably good performance relative to its benchmarks. It might be worth keeping an eye on this one.

For further details see:

PDT: Keep An Eye On This Recession-Resistant CEF