WMB - PDT: This CEF Looks Great In The Current Climate But It Is Overpriced

2023-04-27 17:06:17 ET

Summary

- The high rate of inflation today has made investors and many investors desperate for income.

- John Hancock Premium Dividend Fund invests in a blended portfolio of common stock and fixed-income assets in order to provide its shareholders with an incredibly high level of income.

- The PDT closed-end fund's portfolio is heavily biased toward utilities, which could be a good thing as the economy continues to weaken.

- The 9.35% yield appears to be sustainable going forward.

- The fund is trading at a larger-than-normal premium to the net asset value, so it looks overpriced.

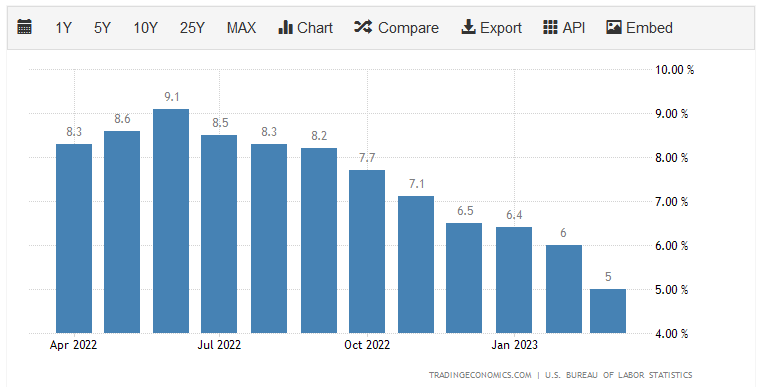

There can be little doubt that one of the biggest problems facing the average American household today is the rapidly rising cost of living in the United States. This is perhaps best evidenced by the consumer price index, which has posted at least a 6% year-over-year increase in eleven of the past twelve months:

{kind=link}

While this situation appears to be improving, the narrative may be somewhat faulty. This is because the improvements in recent months have been entirely driven by falling energy prices. The core consumer price index, which excludes volatile food and energy prices, has not really fallen at all. In fact, it started to tick up last month. This high inflation has caused real wage growth to be down for 24 straight months and has caused many American families to have to spend down their savings or borrow money just to pay their bills and feed themselves. That is the reason why we have seen so many people take on second jobs or enter the gig economy over the past year. In short, people need more income than one job can provide just to stay afloat in today’s economic environment.

As investors, we are certainly not immune to this. After all, we have bills to pay and need to eat too. However, we do not necessarily have to resort to taking on second jobs just to make ends meet. After all, we have the ability to put our money to work for us to earn an income. One of the best ways to do this is by purchasing shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are unfortunately not very well followed in the financial media and many financial advisors are unfamiliar with them. As such, it can be difficult to find information on these entities. That is a shame because closed-end funds offer a number of advantages over open-ended mutual funds and exchange-traded funds. One of the biggest of these advantages is that closed-end funds have the ability to employ certain strategies that can boost their yields well beyond that of any of the assets in the fund’s portfolio. As a result, many of these funds have among the highest yields that are available in the market.

In this article, we will discuss the John Hancock Premium Dividend Fund ( PDT ), which is a closed-end fund that focuses on income. It certainly performs this role admirably as the fund’s 9.35% yield is certainly sufficient to boost the income of any portfolio. I have discussed this fund before, but a few months have passed since that time so obviously a few things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s financial condition and valuation. Let us investigate and see if the John Hancock Premium Dividend Fund could be a worthy addition to a portfolio today.

About The Fund

According to the fund’s webpage , the John Hancock Premium Dividend Fund has the objective of providing its investors with a high level of current income. This is not exactly the objective that we would expect as dividend funds typically invest in common stock. This one is rather unique though as it is currently split between common stock and preferred equity:

CEF Connect

This is in line with the fund’s description of its strategy on the webpage:

{kind=link}

As we can see, the fund states that it invests in common and preferred stocks. As both of these security types pay dividends, the name of the fund makes sense. This is definitely different from many other dividend-focused income funds though as most of them only invest in dividend-paying common stock. It is not necessarily a bad thing though since preferred stocks are generally considered to be somewhat safer than common stock. This is because a preferred stock has no inherent link with the financial performance of the underlying company. Preferred stock is something of a hybrid between common equity and debt, but it has somewhat more in common with debt securities. This is because the dividend paid by the common stock is fixed at the time of issuance of does not change with the performance of the issuing company. This is a marked departure from common stock, which typically pays a dividend that is at least somewhat based on the performance of the issuing company.

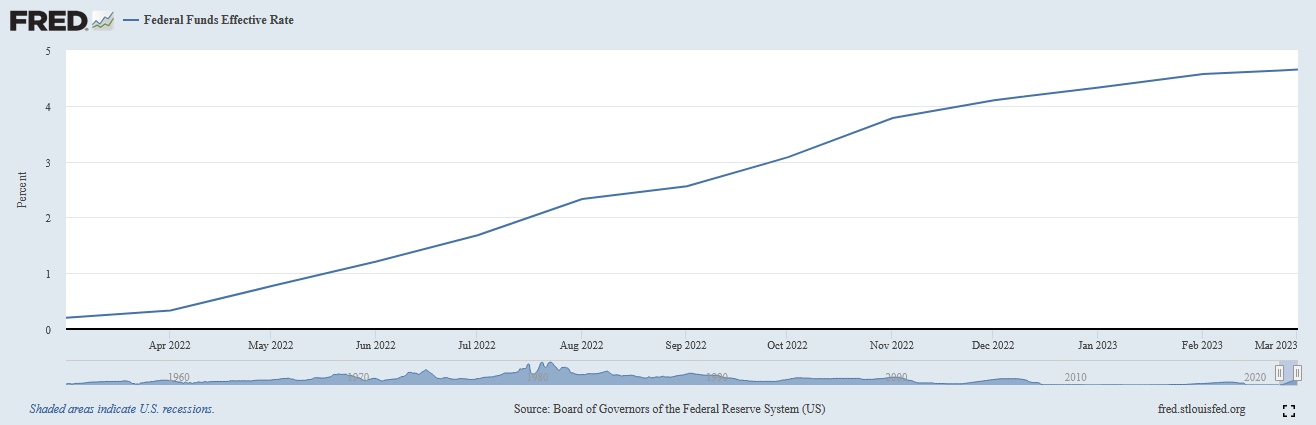

For this reason, preferred stock does not trade based on the company’s financial performance as common stock does. Rather, preferred stock trades are based on interest rates, much like a bond. It is an inverse correlation, so when interest rates go up, preferred stock prices decline. The reverse is also true. As everyone reading this is certainly well aware, the Federal Reserve has been aggressively raising interest rates over the past year as part of its attempt to combat the incredibly high inflation in the American economy. We can see this in the fact that the effective federal funds rate went from 0.20% in March 2022 to 4.65% today:

{kind=link}

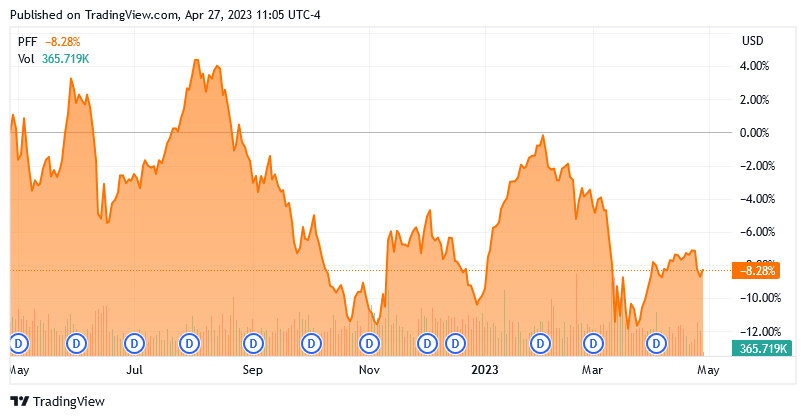

That has naturally caused preferred stock prices to plunge, with the ICE Exchange-Listed Preferred & Hybrid Securities Index ( PFF ) falling 8.28% over the past year:

{kind=link}

The index likely would have fallen further, were it not for the fact that many preferred stock issues have floating rates. I discussed how floating-rate securities generally hold their value in a rising rate environment in a recent article . Nevertheless, we can see that preferred stock has generally declined in price over the past year and since preferred stock accounts for a bit less than half of the fund’s portfolio, we can expect that this will have an impact on the fund’s portfolio.

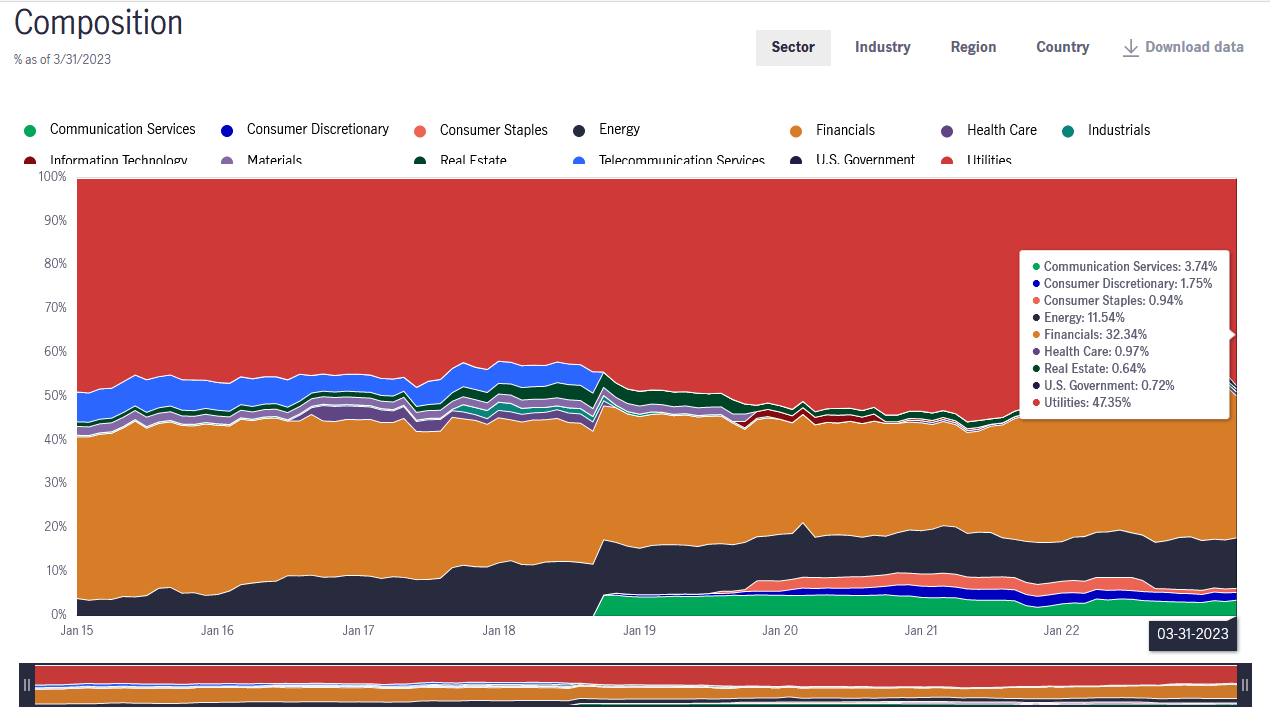

As we discussed in the previous article on the fund, the John Hancock Premium Dividend Fund places a special emphasis on investing in utility companies. This is still the case as utility securities account for 47.35% of the portfolio:

{kind=link}

That is an increase from the 45.51% of the PDT portfolio that was invested in the sector the last time that we reviewed the fund. This is not particularly surprising either considering that the economy has deteriorated over the past few months. In particular, we saw the banking sector begin to experience problems with a few high-profile collapses in both the United States and Europe, which has sparked a certain degree of fear among investors. The utility sector is generally considered to be a safe haven due to its remarkably stable cash flows and balance sheets. As I have pointed out in various previous articles, utility companies provide a product that people generally consider to be a necessity for our modern way of life. As such, they typically prioritize paying their utility bills ahead of anything else during times when money gets tight. As was mentioned in the introduction, the rising cost of living has already made money extremely tight for most people and it will get even more so if the economy heads into a recession. Thus, it makes a great deal of sense to be increasing the allocation of utility companies in a portfolio as these companies should perform much better than either financials or anything dependent on discretionary spending in today’s environment.

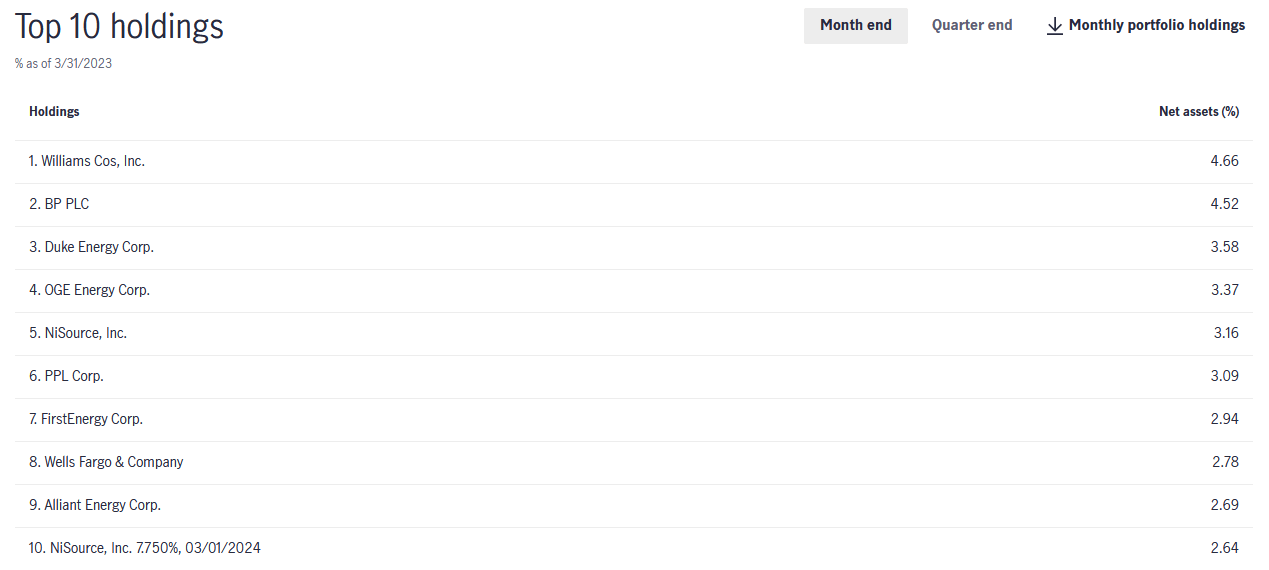

As my regular readers are no doubt well aware, I have devoted a considerable amount of time and effort to discussing utility companies and other high-yielding stocks on this site over the past few years. As such, the largest positions in the portfolio are likely to be familiar to most readers. Here they are:

{kind=link}

I have discussed all of these companies except for PPL Corp. ( PPL ) and Wells Fargo & Company ( WFC ) at some point in the past. As such, all should be at least somewhat familiar. We do clearly see that not all of these companies are utilities, though. In particular, BP ( BP ) is an integrated energy supermajor and Wells Fargo is one of the largest banks in the United States. They are both high-yielding stocks though, with BP’s 4.02% current yield long making it a mainstay in the portfolios of many income-focused investors. The Williams Companies ( WMB ) is also not a utility, strictly speaking, as it is a natural gas-focused midstream company. However, midstream companies share a great many things in common with utilities and are often found in utility funds.

Most importantly, these companies have a great deal of protection against economic conditions and enjoy very stable cash flows over time. These stable cash flows support high yields, with The Williams Companies currently boasting a 6.08% yield. Thus, we can see that except for two companies, all of the fund’s largest positions are either utilities or similar.

There have been two major changes to the fund’s largest positions list since the last time that we looked at it. These changes are that one of Citizens Financial’s ( CFG ) preferred offerings were removed and replaced with Alliant Energy ( LNT ) and Dominion Energy ( D ) was replaced with the NiSource ( NI ) preferred stock shown above. This fits with our earlier discussion about the fund increasing its exposure to utilities in the risk-off trade. The fact that relatively few assets have changed in the past few months could be a sign that the fund has a relatively low turnover. This is reinforced by the fact that the fund had a 16.00% annual turnover in 2022. The reason that this is important is that it costs money to trade stocks or other assets, which is charged directly to the fund’s shareholders. This creates a drag on the portfolio’s performance and makes the job of the fund managers more difficult. After all, the fund’s management needs to earn sufficient returns to cover these expenses and still have enough money left over to provide the shareholders with a satisfactory return. This is a task that very few fund managers manage to achieve on a consistent basis. This is the reason why most actively managed funds fail to match their benchmark indices.

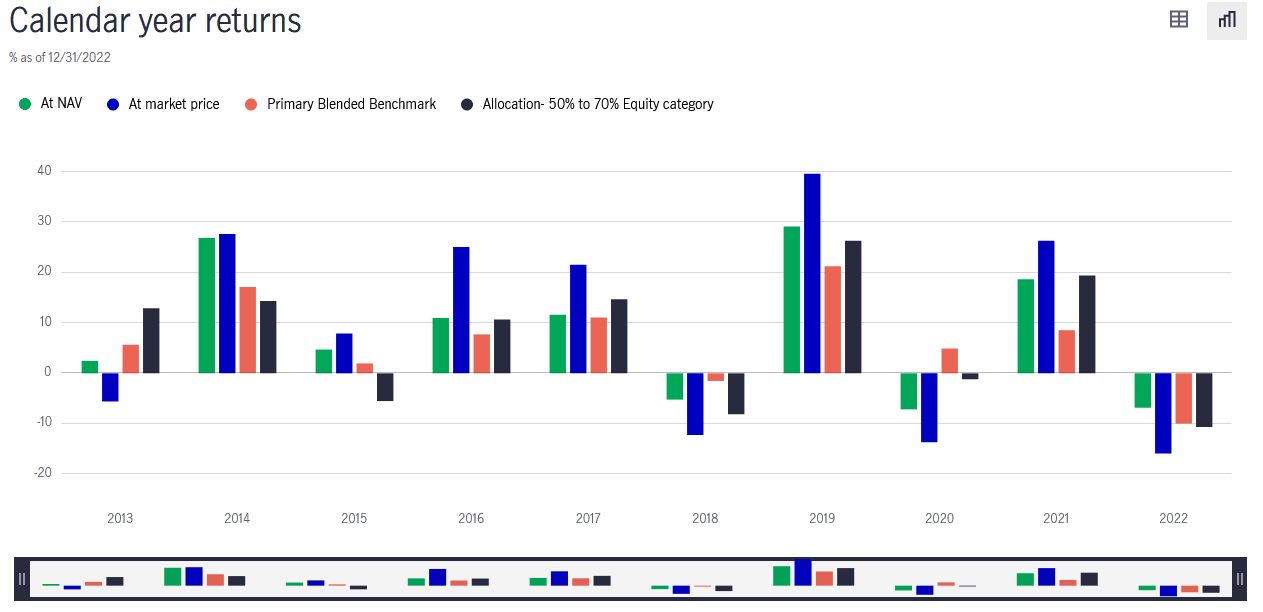

This one has not done too badly over the past year though, as its portfolio delivered a total return of –6.83%, which beat the S&P 500 Index (SP500). It also beat the –10% total return of the fund’s own blended benchmark. The fund’s long-term performance is somewhat spottier as it beats its benchmark during some years and lags it in others:

{kind=link}

Naturally, past performance is no guarantee of future results. However, we can see that the fund’s management generally seems to deliver a reasonable performance relative to a blended benchmark index.

Leverage

In the introduction to this article, I stated that closed-end funds like the John Hancock Premium Dividend Fund have the ability to employ certain strategies that boost the effective yield of their portfolios well beyond that of any of the underlying assets. One of these strategies is the use of leverage. Basically, the fund is borrowing money and then using that borrowed money to purchase common and preferred stocks. As long as the purchased assets deliver a higher return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund has the ability to borrow money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage as that would expose us to an excessive amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. Unfortunately, the John Hancock Premium Dividend Fund currently exceeds this level. As of the time of writing, the fund’s levered assets comprise 38.87% of its assets. This fund is investing in reasonably safe assets, particularly the half of its portfolio that is invested in fixed-income securities, so it can probably carry a higher level of leverage than a pure common equity fund. However, this is still a bit more leverage-related risk than we really want.

Distribution Analysis

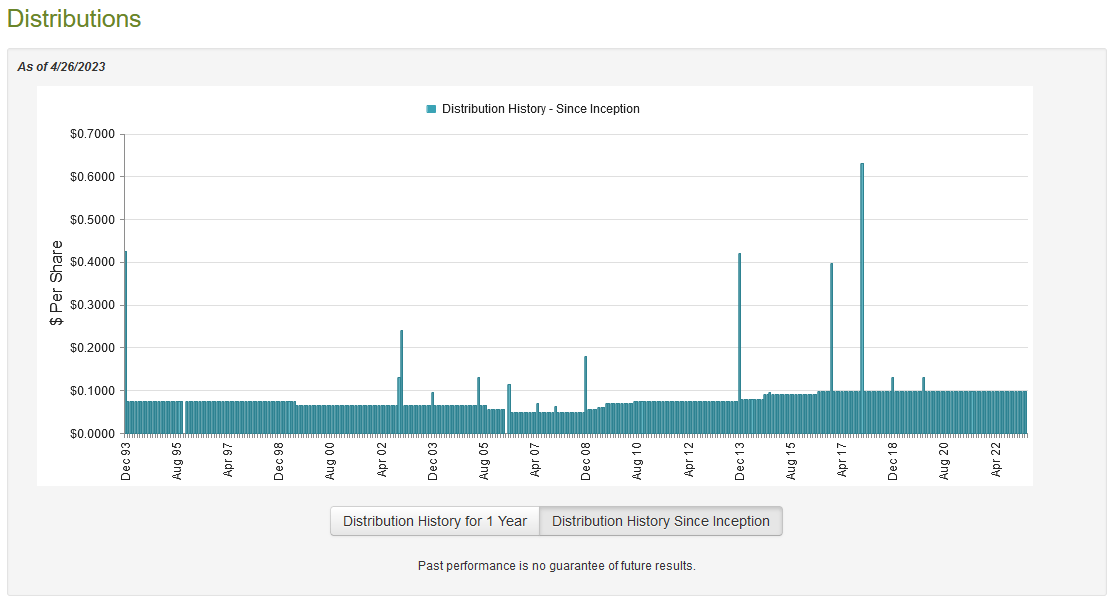

Earlier in this article, I mentioned that the primary objective of the John Hancock Premium Dividend Fund is to provide its investors with a high level of current income. In order to accomplish this, it invests in preferred stock as well as common stock of companies that pay fairly high yields. The fund then applies a layer of leverage to boost the effective yield of its portfolio. As such, we might assume that the fund itself sports a very high yield. That is certainly the case as the John Hancock Premium Dividend Fund pays a monthly dividend of $0.0975 per share ($1.17 per share annually), which gives it a 9.35% yield at the current price. The fund has been remarkably consistent about this distribution as it has steadily raised it since the 2009 recession:

{kind=link}

This is a better track record than that of just about any other closed-end fund, and it will undoubtedly appeal to any investor that is seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. However, it is somewhat difficult to believe that this fund was able to deliver such a consistent performance when most of its peers could not. This is particularly true in 2022, which was a year in which almost everything fell significantly in price. As such, we should have a look at the fund’s finances in order to determine how sustainable its distribution is likely to be.

Unfortunately, we do not have a particularly recent document to consult for that purpose. The fund’s most recent financial report corresponds to the full-year period that ended on October 31, 2022. As such, it will not include any information about the fund’s performance over the past several months. However, it will still give us a good idea of how well the fund weathered the volatile market during the first half of 2022. That was the period during which the Federal Reserve switched from its “free money” policy to the current monetary tightening regime, so it was more volatile than the past few months have been. During the full-year period, the John Hancock Premium Dividend Fund received $37,814,629 in dividends and $14,401,781 in interest from the assets in its portfolio.

When we net out the money that the fund paid in foreign withholding taxes, it had a total income of $52,000,265 during the period. The fund paid its expenses out of this amount, which left it with $35,285,384 available for the shareholders. This was, unfortunately, not nearly enough to cover the $57,179,674 that the fund paid out in distributions during the period. At first glance, this is likely to be concerning as the fund’s net investment income was insufficient to cover the distributions.

However, the PDT fund does have other methods through which it can obtain the money that is needed to cover the distribution. For example, it will frequently pay out its capital gains to investors. It was not as successful at getting capital gains as we would like, though. The fund managed to earn net realized gains of $20,077,718 during the period, but these were more than offset by $109,947,904 net unrealized losses. Overall, the fund’s assets declined by $107,298,715 during the period after accounting for all inflows and outflows. This is concerning, although the fund’s net investment income plus its net realized gains were very close to enough to cover the distribution. These two items combined were $55,363,102, which leaves the fund a little less than $2 million short of being able to afford the distribution.

As of October 31, 2022, the fund did have more money than it did on October 31, 2020, so the fund did manage to earn enough money during the trailing two-year period to cover the distribution.

| October 31, 2022 |

| October 31, 2020 |

| Fund Assets At Market Close |

| $49,091,976 |

| $48,689,976 |

Overall, the distribution is probably safe as long as the fund manages to have a strong enough performance going forward to cover it. We should watch the fund’s finances on a semi-annual basis to ensure that this is the case.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a sure-fire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the John Hancock Premium Dividend Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of the fund’s assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund’s assets for less than they are actually worth. This is, unfortunately, not the case with this fund today. As of April 26, 2023 (the most recent date for which data is available as of the time of writing), the John Hancock Premium Dividend Fund had a net asset value of $11.97 per share but the shares trade for $12.59 each. This gives the shares a 5.18% premium to the net asset value at the current price. This is significantly higher than the 2.65% premium that the shares have had on average over the past month, and it is not a good idea to buy the shares of any fund at a premium regardless. Thus, it appears that the best approach here is to sit and watch for a better entry price.

Conclusion

In conclusion, the John Hancock Premium Dividend Fund appears like a decent investment today. The fund’s blended portfolio and emphasis on utilities should position it pretty well to weather through any economic difficulty that may hit in the near term. This is especially important today due to the fact that numerous economic indicators are pointing to a recession hitting sometime in the second half of the year. The fund also has a solid performance track record and a stable distribution that appears to be sustainable. The only real problem here is that the John Hancock Premium Dividend Fund appears to be overpriced today. John Hancock Premium Dividend Fund is definitely worth watching, though.

For further details see:

PDT: This CEF Looks Great In The Current Climate, But It Is Overpriced