PPL:CC - Pembina Pipeline: A Solid Core Holding For Any Income Portfolio

2023-06-19 09:46:10 ET

Summary

- Pembina Pipeline is one of the largest midstream companies in North America, boasting infrastructure stretching across much of Western Canada.

- The company enjoys remarkably stable cash flows regardless of energy prices.

- The company boasts some strong growth prospects going forward, largely due to the growing demand for natural gas liquids.

- The company has a very strong balance sheet with low leverage.

- The company has an attractive 6.24% dividend yield that appears to be sustainable going forward.

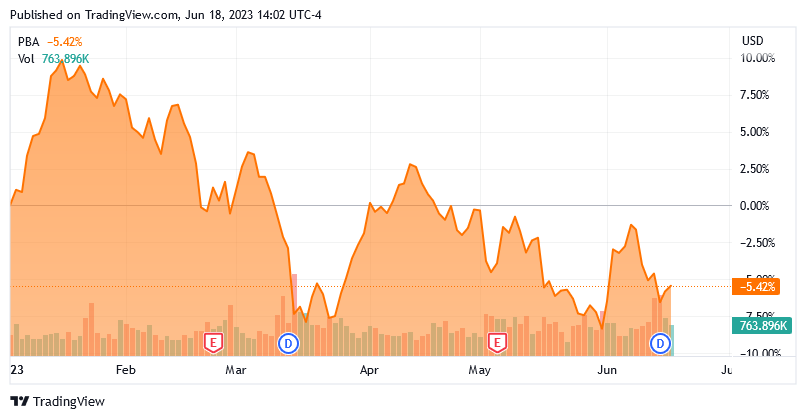

Pembina Pipeline Corporation ( PBA ) is a giant Canadian midstream company that primarily transports crude oil and natural gas throughout the province of Alberta but has some operations elsewhere. The company has long been a favorite of income investors, as its 6.24% yield is hard to beat. Unfortunately, the company has not been performing very well in the market recently as it is down 5.42% year-to-date:

{kind=link}

This is almost certainly at least partly due to energy prices, as the shares of Pembina Pipeline have shared a historic correlation to energy prices. However, energy prices actually have very little impact on Pembina Pipeline's financial performance. Indeed, the company typically enjoys remarkably stable cash flows over time. This has allowed it to achieve one of the best dividend track records in the market, as the company has increased its dividend annually since 1998. It is much more than just a stable dividend payer, as it also boasts strong forward growth prospects. Overall, this company still offers a lot for any income-focused investor and it is deserving of a position in a portfolio today.

About Pembina Pipeline Corporation

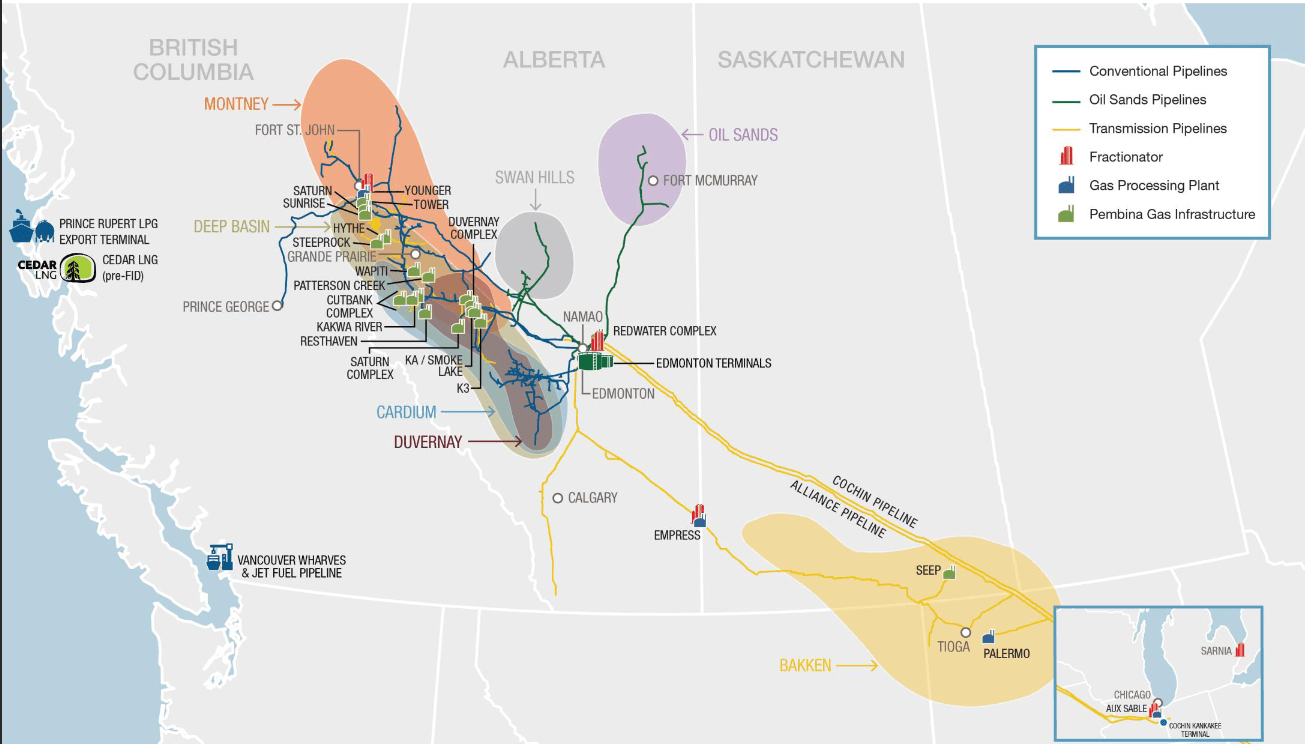

As stated in the introduction, Pembina Pipeline is one of the largest midstream companies in Canada. The company owns a network of hydrocarbon transportation pipelines and natural gas processing plants stretching across much of the provinces of Alberta and British Columbia, as well as into the United States:

{kind=link}

In total, Pembina Pipeline is capable of transporting approximately 2.8 million barrels of oil equivalents per day. The company also owns processing plants capable of handling 5.4 billion cubic feet of natural gas per day, storage facilities with a total capacity of 32 million barrels of liquid hydrocarbons, and a fractionation capacity for 354,000 barrels of natural gas liquids per day. This all makes Pembina Pipeline one of the biggest midstream providers on the North American continent. The market appears to agree with this assessment, as Pembina Pipeline has a market capitalization of $17.18 billion at the current stock price.

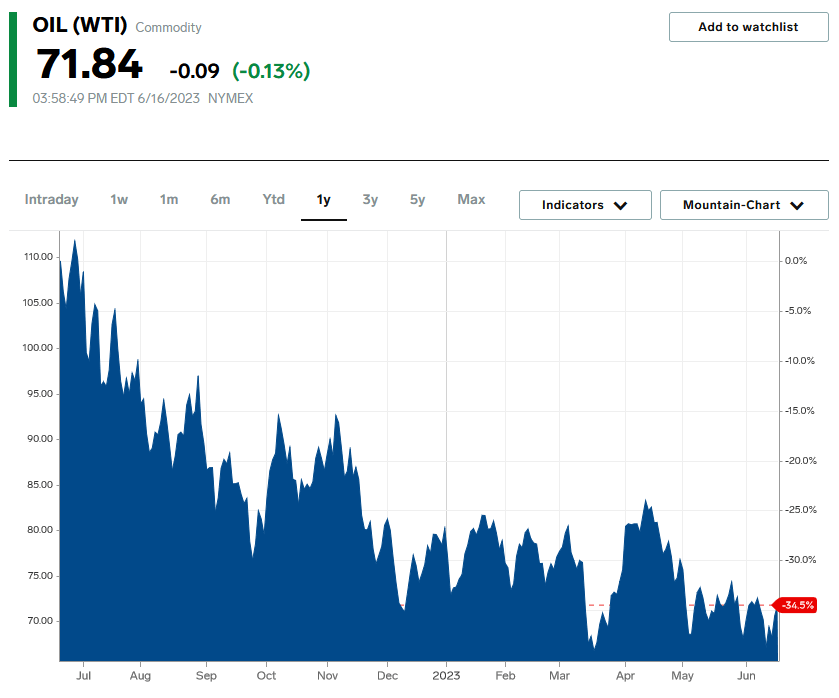

As everyone reading this is no doubt well aware, crude oil prices have not delivered a particularly strong performance so far this year. Over the past twelve months, West Texas Intermediate crude oil is down 34.5%:

{kind=link}

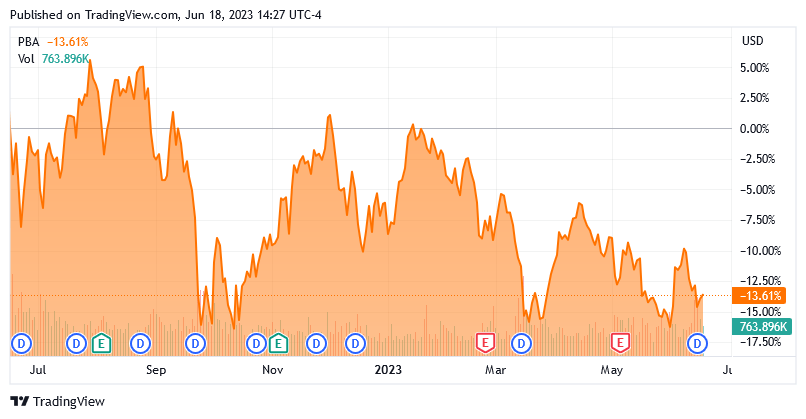

This is generally blamed on near-term recession fears, as such an event would cause the demand for crude oil to decline during the second half of the year. However, as I pointed out in a recent article , the United States government has been drawing down the Strategic Petroleum Reserve in an attempt to keep the market oversupplied with crude oil. The Russian sanctions have also had no impact on global crude oil supply as both China and India have been ignoring them and purchasing oil from Russia at below-market prices, which they then resell internationally. Thus, there are far more factors at play here than just the expectation of a recession. As mentioned in the introduction, Pembina Pipeline has certainly not been unaffected by this energy price decline as the stock is down 5.42% year-to-date and 13.61% over the past twelve months:

{kind=link}

However, Pembina Pipeline's cash flows are not particularly affected by energy price fluctuations due to the business model that the company employs. In short, Pembina Pipeline enters into long-term contracts (the current average remaining contract life is fourteen years) with its customers under which Pembina Pipeline provides transportation, processing, or storage for the customer's hydrocarbon products. In exchange, the customer compensates Pembina Pipeline based on the volume of resources that are being handled, not on their values. This obviously insulates the company against changes in resource prices, especially when combined with the fact that these contracts usually include minimum volume commitments that specify a certain quantity of resources that must be sent through Pembina Pipeline's infrastructure or paid for anyway. These contracts are responsible for 80% to 90% of the company's estimated 2023 EBITDA:

Pembina Pipeline

Thus, it should be pretty easy to see how this contract-based business model will result in remarkably stable cash flows for Pembina Pipeline regardless of resource prices. This stability is immediately apparent in Pembina Pipeline's operating cash flows, which have consistently increased every year over the past decade:

{kind=link}

(all figures in millions of Canadian dollars)

As anyone that has watched the industry for an extended period of time can attest, crude oil prices were all over the place during this period. There were low energy prices during 2015 and 2020 and very high prices during 2022 but this had no apparent impact on Pembina Pipeline's cash flows. This is exactly the kind of thing that we like to see with an income-focused investment as it provides a great deal of support for the company's dividend. After all, it is easier for a company to budget a large dividend payment if it knows with some degree of certainty how much it will make during the next period. This is similar to how a salaried person can carry a larger mortgage relative to income than someone that works on commission.

Growth Opportunities

Naturally, as investors, we are unlikely to be satisfied with mere stability. After all, we like to see every company in our portfolios grow and prosper with the passage of time. As we just saw, Pembina Pipeline has historically grown its operating cash flow on an annual basis, and it is fortunately likely to continue to deliver on this historical track record.

Pembina Pipeline currently has two growth projects under construction:

- Phase VIII of the Peace Pipeline Expansion project.

- Redwater Fractionation IV project.

The first of these is Phase VIII of the Peace Pipeline Expansion project. This project is one that Pembina Pipeline has been working on over much of the past decade, and as the name implies it has already brought several other phases to completion and into operation. It has not necessarily been bringing each phase online in order, as Phase IX started operation back in January but Phase VIII has yet to be completed. Phase VIII is described on the company's webpage thusly:

The Phase VIII Peace Pipeline Expansion will enable segregated pipeline service for ethane-plus and propane-plus NGL mix from Gordondale, Alberta, which is centrally located within the Montney trend into the Edmonton area for market delivery. The project includes new 10-inch and 16-inch pipelines, totaling approximately 150 kilometres, in the Gordondale to La Glace corridor of Alberta, as new mid-point pump station and terminal upgrades located throughout the Peace Pipeline system.

The purpose of this new pipeline is to increase the system's ability to handle the rising volume of natural gas liquids being produced in the Western Canadian Sedimentary Basin. As I have noted in a few previous articles, the global demand for natural gas liquids has been rising over the past several years and this capacity upgrade will allow Pembina Pipeline to transport more natural gas liquids to meet this demand. This phase of the project is expected to be completed and start operation in the second half of 2024, so we should begin to see the impact on the company's financial performance around that time.

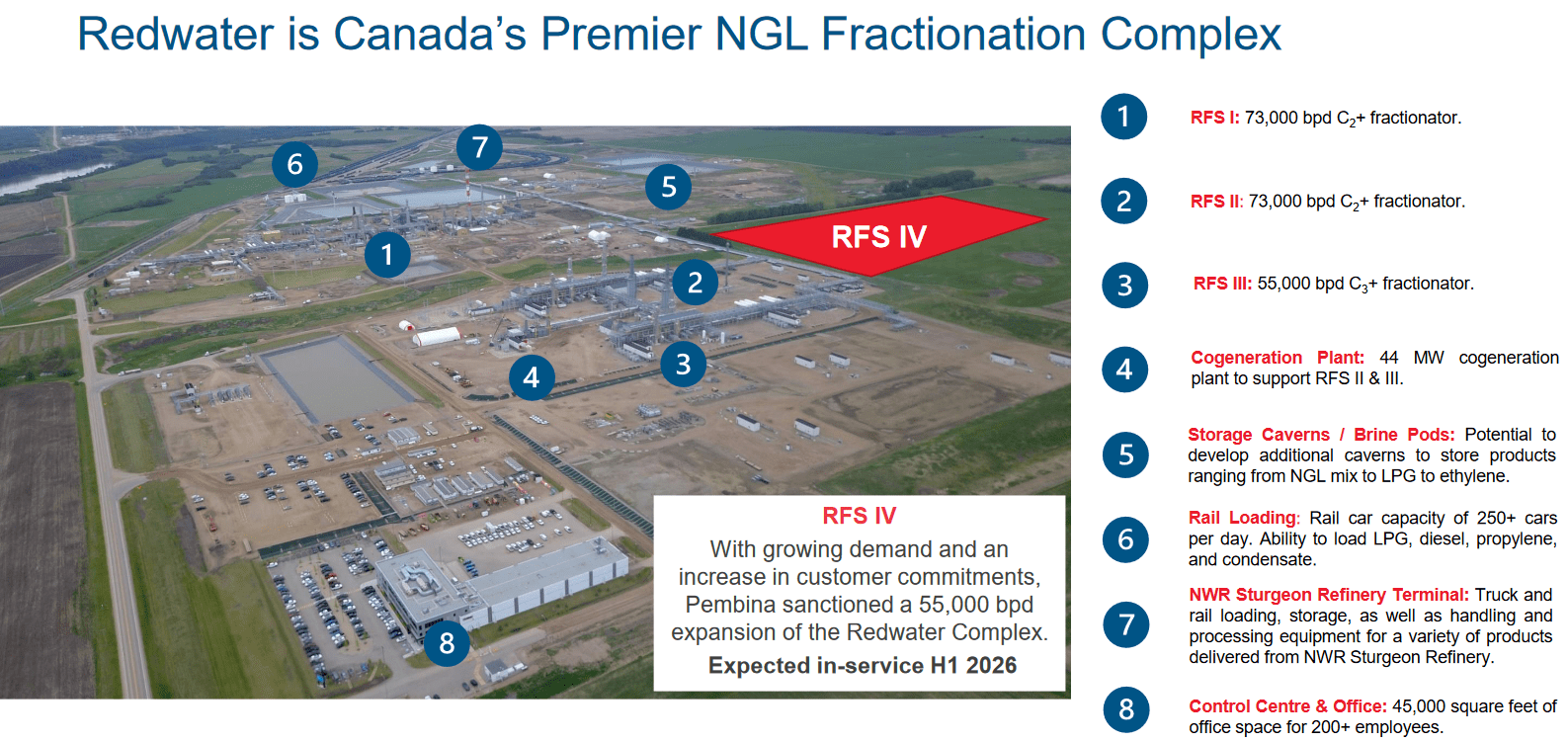

The rising demand for natural gas liquids is also driving Pembina Pipeline's second current growth project, the Redwater Fractionation IV project. The Redwater Complex is one of the largest natural gas liquids fractionation plants in North America:

{kind=link}

The facility broadly converts natural gas liquids into their component parts such as propane, butane, and ethane that can then be sold on the market. The project in question involves the addition of a new 55,000-barrel-per-day total capacity propane production train. This project will thus increase the quantity of natural gas liquids that can be processed at this facility when it is complete. The company expects to bring this new production train online during the first half of 2026. Thus, we will have to wait a bit until the project begins to have an impact on Pembina Pipeline's results, but it also provides the company with a nice medium-term growth pipeline.

The nice thing about both of these projects is that Pembina Pipeline has already secured contracts from its customers for the use of the new capacity. This is nice because it ensures that Pembina Pipeline is not paying an enormous amount of money for new infrastructure that nobody wants to use. It also allows Pembina Pipeline to know in advance how profitable each of these projects will be before it starts to work on them. As such, the company knows in advance that it will earn a sufficient return to justify the investment. The company has not stated exactly what return it expects to realize, but it is common for midstream companies to pay for themselves after four to six years, so that is a reasonable estimate for these projects.

Financial Considerations

It is always important to look at the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and using the proceeds to repay the existing debt. As debt carries an interest rate that is based on the market rate at the time of issuance, a company's interest expenses might increase following the rollover in certain market conditions. As of the time of writing, interest rates are at the highest levels that we have seen since 2007 so this is a very real concern today. In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company's cash flows to decline could push the company into financial distress if it has too much debt. While midstream companies like Pembina Pipeline typically have remarkably stable cash flows, this is still a risk that we should not ignore.

One metric that we can use to judge a midstream company's ability to carry its debt is the leverage ratio, which is also known as the debt-to-adjusted EBITDA ratio. This ratio essentially tells us how many years it would take for the company to completely pay off all of its debt if it were to devote all of its pre-tax cash flow to that task. As of March 31, 2023, Pembina Pipeline had a leverage ratio of 3.6x based on its trailing twelve-month adjusted EBITDA. This is a reasonable ratio that is well below that of fellow Canadian midstream giant Enbridge ( ENB ). Wall Street analysts typically like to see a midstream company's leverage ratio below 5.0x to be satisfied. However, I am more conservative and like to see this ratio below 4.0x in order to add a margin of safety to the position. As we can clearly see, Pembina Pipeline satisfies even this stricter requirement. As such, we probably do not need to worry very much about the company's debt level today.

Dividend Analysis

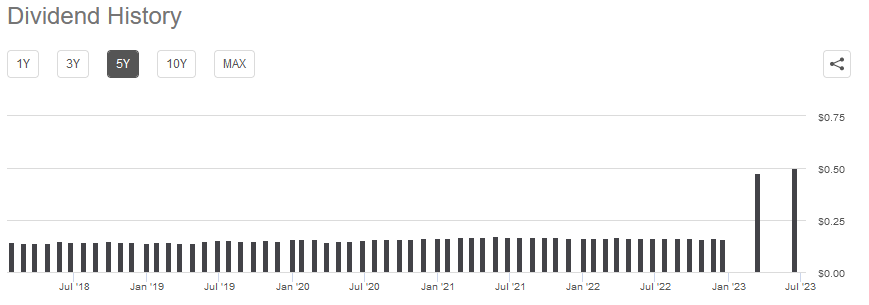

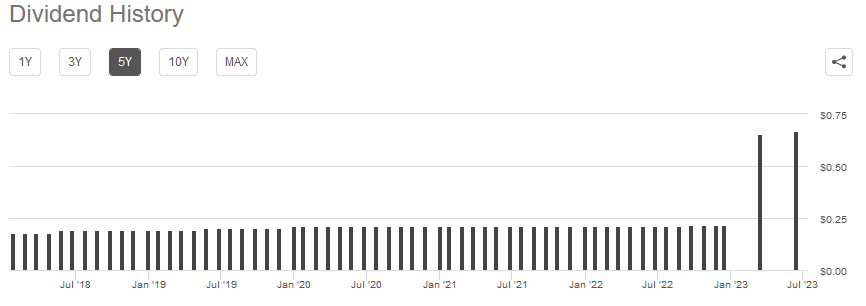

One of the biggest reasons why shareholders purchase shares of Pembina Pipeline is that the company has historically had a very high dividend yield. As noted in the introduction, Pembina Pipeline currently yields 6.24%, which is well above the yield of most other companies in the market. The company also has a long history of growing its dividend over time, at least when measured in Canadian dollars. The U.S. shares have had a somewhat more variable dividend, as we can see here:

{kind=link}

The reason for this is that the American-traded shares pay a dividend in U.S. dollars. Pembina Pipeline actually declares and pays its dividend in Canadian dollars though, so the dividend paid to the American shares depends on the exchange rate on the payment date and exchange rates do vary over time. As we can see though, the trend has still been for dividend growth over time even for the American shares. This growth over time is even more obvious when looking at the Canadian-traded shares ( PPL:CA ):

{kind=link}

The fact that Pembina Pipeline has historically grown its dividend over time is something that is very nice to see during inflationary periods, such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can buy with the dividend that the company pays out. This effect can make it feel as though we are getting poorer and poorer with the passage of time. This is an especially big problem for investors that are dependent on their portfolios to produce the money that they need to survive, such as retirees. The fact that the company increases the amount that it pays us over time helps to offset this effect and maintains the purchasing power of the dividend.

As is always the case, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut, since that would reduce our incomes and almost certainly cause the stock price to decline.

The usual way that we judge a company's ability to pay its dividend is by looking at its free cash flow. The free cash flow is the amount of money that was produced by the firm's ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is the money that can be used to reward the shareholders through debt reductions, stock buybacks, or dividends. In the twelve-month period that ended on March 31, 2023, Pembina Pipeline had a levered free cash flow of CAD$1.115 billion and paid out CAD$1.660 billion in dividends. At first glance, this could be quite concerning as the company failed to cover its dividend out of free cash flow.

However, Pembina Pipeline can be thought of as a utility as it shares many of the same characteristics. In particular, the company has enormous upfront infrastructure costs but its assets produce relatively steady cash flow over time once they are operational. As I have noted in various previous articles, utilities typically finance their capital expenditures through the issuance of equity and debt while paying their dividends out of operating cash flow. In the trailing twelve-month period, Pembina Pipeline had an operating cash flow of CAD$2.732 billion. That was easily enough to cover the CAD$1.660 billion that was paid out in dividends with a great deal of money left over that can be used for other purposes. This is nice to see from our perspective and indicates that Pembina Pipeline can probably sustain its dividend at the current level going forward.

Conclusion

In conclusion, Pembina Pipeline continues to look like one of the best midstream companies in the space. The company boasts an attractive 6.24% yield that should prove sustainable going forward along with some growth prospects that should allow it to continue its long track record of dividend growth. The company also possesses one of the strongest balance sheets in the industry, which should put it in a better position to weather the current high-interest rate environment than some of its peers. Overall, Pembina Pipeline looks like it could make a solid core holding for any investor.

For further details see:

Pembina Pipeline: A Solid Core Holding For Any Income Portfolio