KO - PepsiCo: The Dividend King Has Its Price

Summary

- PepsiCo increased its revenue in the second quarter while earnings per share declined, mostly due to the Europe business.

- Not only is the business resilient against a recession, the company also entered the ranks of a dividend king.

- But the stock is still overvalued in my opinion and PepsiCo is not a good investment.

While I was writing this article about PepsiCo, Inc. ( PEP ) I have also been writing an article about General Mills, Inc. ( GIS ) and both companies are operating in a similar industry – at least in parts – and can be seen as competitors. I am a shareholder of General Mills, which worked out quite well so far, but won’t become a shareholder of PepsiCo at these prices.

Since my last article about PepsiCo was published in January 2022 (I rated the stock as a “Hold” back then), the stock outperformed the overall market (represented by the S&P 500 ( SPY )), but the stock did not gain in value and is trading almost for the same price as eight months ago. In my last article I argued that PepsiCo is too expensive to be a good investment and, in this article, I will make a similar argument. We start by looking at the last reported results.

Quarterly Results

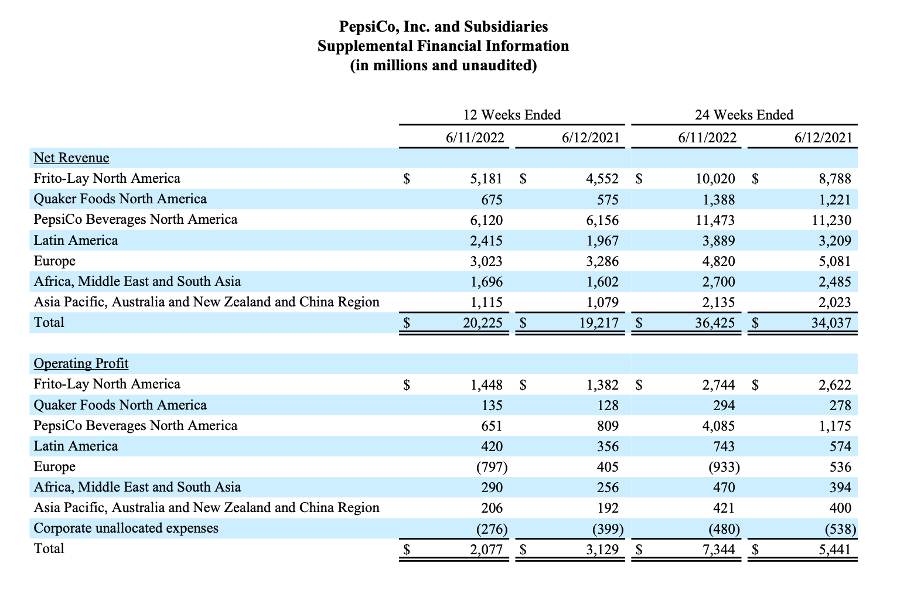

When looking at the second quarter of fiscal 2022, PepsiCo reported mediocre results. While net revenue increased from $19,217 million in Q2/21 to $20,225 million in Q2/22 (an increase of 5.2% year-over-year), operating profit declined from $3,129 million in the same quarter last year to $2,077 million this quarter – a decline of 33.6% year-over-year. And finally, diluted net income per share declined from $1.70 in the same quarter last year to $1.03 this quarter – a decline of 39.4% YoY. And while reported revenue increased only 5.2%, organic revenue growth was 13.0% in the second quarter.

For the full year of fiscal 2022, PepsiCo is now expecting 10% organic revenue growth (compared to a previous guidance of only 8% organic revenue growth). Management is also expecting core earnings per share to be $6.63, which would result in about 6% year-over-year growth.

PepsiCo Q2/22 Earnings Release

{kind=link}

When looking at the different segments, revenue growth especially stemmed from “Frito-Lay North America” as well as “Latin America”. On the other hand, we saw declining revenue from “Europe” and compared to an operating profit of $405 million in the same quarter last year, the segment had to report an operating loss of $797 million this quarter. During the last earnings call , CEO Ramon Laguarta commented on Europe in response to an analyst’s question:

Yes. Good. Listen, Europe, obviously, has been impacted by -- more than other parts of the world by, I would say, the war, so our business has been impacted both in Ukraine and Russia. Ukraine, because obviously, we had to stop a lot of our manufacturing and commercial activities as reflected in our performance in Europe. And also in Russia, given the commitments we made to stop our beverage, some of our beverage, large brands and also stop advertising and promotion of our more essential food brands. So clearly, that's part of the reason why the European business has been impacted.

Recession

One of the reasons PepsiCo could be interesting in these times is the ability to withstand a recession quite well. I don’t want to include an entire business description as we all know PepsiCo is operating in the convenient foods (55% of revenue) and beverages (45% of revenue) market and has several well-known brand names of everyday products.

PepsiCo CAGNY 2022 Presentation

{kind=link}

And customers will continue to purchase many of these products even in times of a recession. In case of Pepsi vs. Coke we could even make the argument that consumers might choose the cheaper Pepsi instead of the more expensive Coke from competitor The Coca-Cola Company ( KO ). While I don’t know if Pepsi would be able to gain market shares during a recession (in the past two decades it mostly lost market shares ), the company is pretty resilient to a recession.

When looking at revenue during the last few decades, we see a few declines. But in my opinion, these declines can’t be associated with a recession and occurred for different reasons. Additionally, we can also look at earnings per share and see declining numbers on several different occasions. Some of these declines might be the result of a recession, but the declines were not extremely steep, and PepsiCo usually managed to return to previous levels within a few quarters.

Long-Term Growth Targets

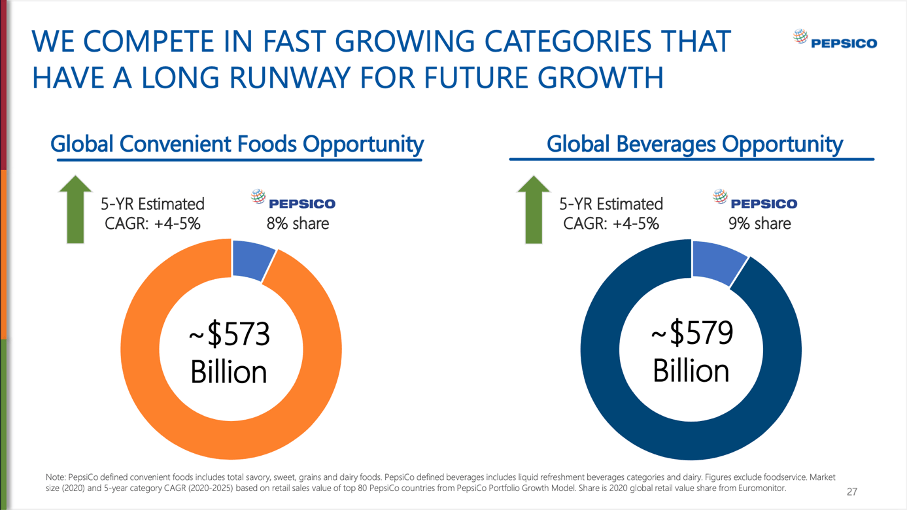

PepsiCo is one of the major players in the global convenient foods and global beverage market and has a market share between 8% and 9% in both markets. As PepsiCo is expecting both markets to grow with a CAGR of 4% to 5% in the next five years, the company should be able to grow its top line just by growing with a similar pace as the overall market (and holding its market share).

PepsiCo CAGNY 2022 Presentation

{kind=link}

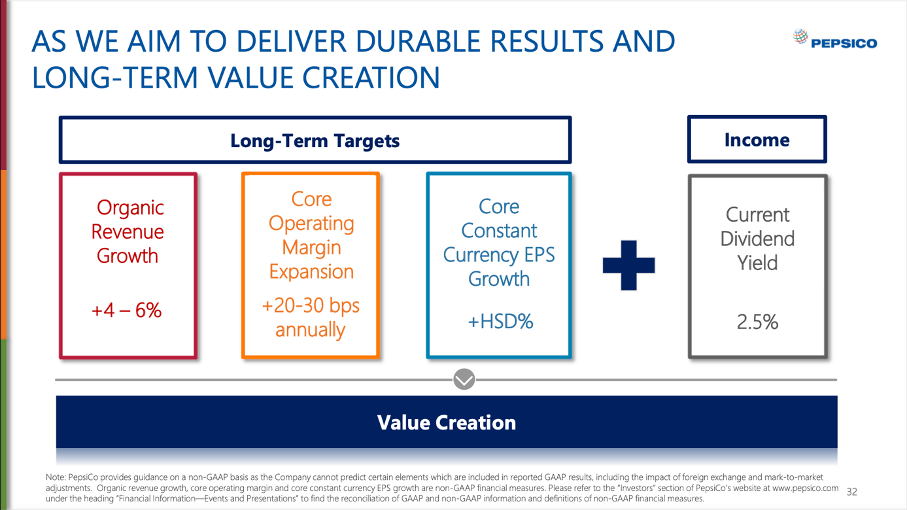

And aside from organic growth, PepsiCo will most likely continue with acquisitions (a recent example would be the acquired 20% stake in AQUA Carpatica ). When considering these growth rates for the overall industry being realistic and PepsiCo also being able to grow a bit by acquisitions, PepsiCo’s long-term targets of revenue growth being between 4% and 6% could be realistic (as the company rather lost market shares in the beverage market in the last two decades, I don’t think gaining market shares will contribute to growth). PepsiCo is also expecting its margins to expand in the coming years and core constant currency earnings per share is expected to grow in the high single digits.

PepsiCo CAGNY 2022 Presentation

{kind=link}

These long-term targets are not unrealistic or impossible to achieve for PepsiCo, but we also should not be surprised if the business is not able to grow with 8% or 9% annually. When looking at the last decade, PepsiCo was certainly not able to grow with a similar pace.

Balance Sheet

The company has more or less a solid balance sheet. On June 11, 2022, the company had $6,032 million in short-term debt obligations as well as $33,247 million in long-term debt obligations. When comparing the total debt to the total equity of $18,674 million this is resulting in a debt-equity ratio of 2.10. While this is a rather high D/E ratio, we can also compare the total debt to the operating income of the last four quarters, which was $12,259 million. When comparing the total debt to the operating income, it would take about 3.2 years to repay the outstanding debt, which is acceptable.

Additionally, the company has $5,405 million in cash and cash equivalents as well as $287 million in short-term investments, which could be used to repay outstanding debt. And when looking at the asset side, we also must mention $18,547 million in goodwill (20% of total assets).

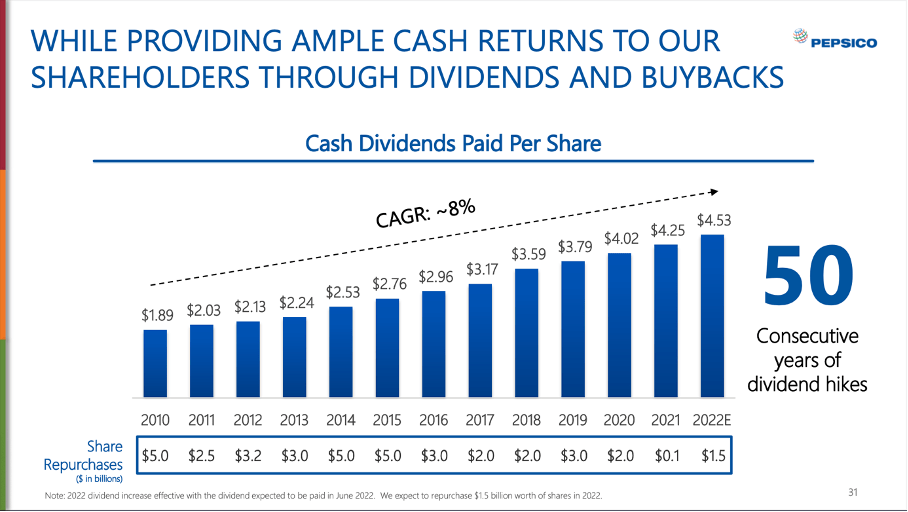

Dividend

It is also worth mentioning that PepsiCo joined the club of dividend kings with 50 consecutive years of dividend hikes. Right now, the company is paying a quarterly dividend of $1.15 resulting in an annual dividend of $4.60 and a dividend yield 2.63%.

PepsiCo CAGNY 2022 Presentation

{kind=link}

And while PepsiCo is paying a solid dividend yield and being a dividend king makes a company certainly interesting for dividend investors, we must acknowledge the rather high payout ratio. I don’t think we are facing the risk of a dividend cut, but dividend increases in the low single digits could be a possibility.

We can start by comparing the current annual dividend of $4.60 to the diluted earnings per share of $6.64 in the last four quarters and we get a payout ratio of 69% which is a rather high payout ratio. Aside from comparing the dividend to earnings per share, we can also compare dividend payments of $5,970 million in the last four quarters to a free cash flow of $6,338 million in the last four quarters. And paying out 94% of its free cash flow as dividends is extremely high. A business can distribute the entire free cash flow to its shareholders, but usually the company is also repurchasing shares or using free cash flow in some other ways.

And for PepsiCo I would expect dividend increases rather in the low single digits unless the company is able to improve earnings per share and/or free cash flow significantly in the next few years.

Intrinsic Value Calculation

In my opinion, Pepsi is too expensive. When looking at the price-earnings ratio, PepsiCo is trading for 26 times earnings and while there are many companies and stocks trading for a much higher valuation multiple, this is not cheap. And especially when looking at the price-free-cash-flow ratio we find not only the highest valuation multiple of the last ten years, but 38 times free cash flow seems to be extremely expensive.

Additionally, we can also calculate an intrinsic value by using a discounted cash flow calculation. As basis for our calculation, we can take the free cash flow of the last four quarters (which was $6,338 million). The next question we must answer is what growth rates are realistic in the years to come. And let’s be optimistic for the coming years and use the long-term targets of PepsiCo and assume the business can grow 9% annually in the next ten years (followed by 6% growth till perpetuity). When using these numbers (and a 10% discount rate as well as 1,389 million outstanding shares), we get an intrinsic value of $141.08 for PepsiCo – making the stock already overvalued.

However, to calculate realistically, we should also take a potential recession into account and although PepsiCo can be seen as rather resilient to a recession, we should assume stagnating free cash flow in fiscal 2023 (with declining free cash flow also being a possibility). And expected growth rates will probably not be higher than 8% or 9% for the next ten years. This results in an intrinsic value of $120 to $130 for PepsiCo. And at least in theory we should account for the net debt of $33,587 million on the balance sheet, which is resulting in about $24 in debt per share. When subtracting that amount from the calculated intrinsic value we get an intrinsic value slightly above $100 for PepsiCo and the stock is certainly trading at a premium.

Competitors

PepsiCo is trading for a premium at this point and doesn't seem like a good investment. This is also becoming obvious when comparing PepsiCo to some of its competitors - including companies like The Coca-Cola Company, Nestle S.A. ( NSRGY ), Mondelez International, Inc. ( MDLZ ) or General Mills, Inc.. When looking at the 10-year earnings per share CAGR, PepsiCo – together with Coca-Cola – reported the lowest growth rates but is simultaneously trading for extremely high valuation multiples. And one does not have to be a genius to realize this is a horrible combination.

| PepsiCo |

| Coca-Cola |

| Nestle |

| Mondelez |

| General Mills |

| Revenue 5-year CAGR |

| 4.82% |

| -1.58% |

| -0.52% |

| 2.07% |

| 3.99% |

| Revenue 10-year CAGR |

| 1.80% |

| -1.84% |

| 0.43% |

| -6.18% |

| 1.32% |

| EPS 5-year CAGR |

| 4.72% |

| 8.59% |

| 17.12% |

| 23.69% |

| 9.80% |

| EPS 10-year CAGR |

| 3.14% |

| 2.00% |

| 7.43% |

| 4.33% |

| 6.52% |

| 5-year ROIC |

| 17.35% |

| 11.70% |

| 13.65% |

| 8.65% |

| 12.24% |

| Operating Margin |

| 15.17% |

| 28.06% |

| 17.04% |

| 15.55% |

| 17.27% |

| P/E ratio |

| 26.28 |

| 28.39 |

| 19.01 |

| 22.72 |

| 17.48 |

| P/FCF ratio |

| 38.28 |

| 26.65 |

| 41.77 |

| 25.91 |

| 17.23 |

On the other hand, PepsiCo has the highest 5-year ROIC of the five companies mentioned above and return on invested capital is certainly an important metric. But this is not enough to make the argument of PepsiCo being a good investment at this point. I already mentioned General Mills and among the companies mentioned in this section, it would probably be the pick I would choose right now. While General Mills will be able to grow with a solid pace, it is also trading for a reasonable valuation multiple.

Conclusion

While I don’t want to make the argument that PepsiCo is not a great business, I would like to make the argument that the stock is not a good investment right now. Paying 26 times earnings or 38 times free cash flow doesn't seem justified for a business that's had trouble growing with a solid pace in the last few years and has yet to prove that it's able to deliver on its long-term targets.

Considering the high risk of a potential recession in the coming quarters, PepsiCo would be a good pick as we can expect the business to withstand a recession quite well. But the high valuation multiple and the stock being rather overvalued is imposing some downside risk for the stock. I would not short PepsiCo at this point as we are still talking about a solid business that will perform solid over the long run and so I would rate the stock once again as a “Hold”. And when someone wants to make investments in the consumer staples industry, we can find better picks in my opinion – like General Mills.

For further details see:

PepsiCo: The Dividend King Has Its Price