CHWY - Petco: Heavily Discounted Despite Favorable Long-Term Trends

2023-10-03 13:48:26 ET

Summary

- Petco shares have fallen 56% year-to-date and are down 78% from its IPO price.

- The decline in high-margin non-consumable revenue has led to a decline in EBITDA.

- Petco is well-positioned in the long term due to long-term growth in pet spending and its position as a leader in the pet industry.

Petco ( WOOF ) shares have fallen 56% year-to-date and are now down 78% from its $18/share IPO price in early 2021. Petco was a beneficiary of the pandemic-induced pet super adoption cycle of 2020-21, which saw a surge in pet ownership and a corresponding increase in high-margin non-consumable sales. As new pet ownership has normalized, the commensurate decline in high-margin non-consumable revenue has led to a decline in EBITDA. The impact to equity holders has been magnified by relatively high financial leverage (3.3x Net Debt to EBITDA).

While the near term is fraught with uncertainty, I believe that Petco is well-positioned in the long term given:

- Long-term secular growth in pet spending

- Petco's position as a leader in the pet industry

- Continued growth in higher-margin services including grooming, veterinary care, training, and vaccination

Following the selloff in Petco shares, the stock trades at an undemanding valuation, with shares valued at less than 6x EBITDA and just 8x my estimate of normalized FCF per share. While the company carries more debt than I would like, I believe leverage is manageable. Looking out 2-3 years, I see the potential for a 50%+ increase in the stock.

Current Results

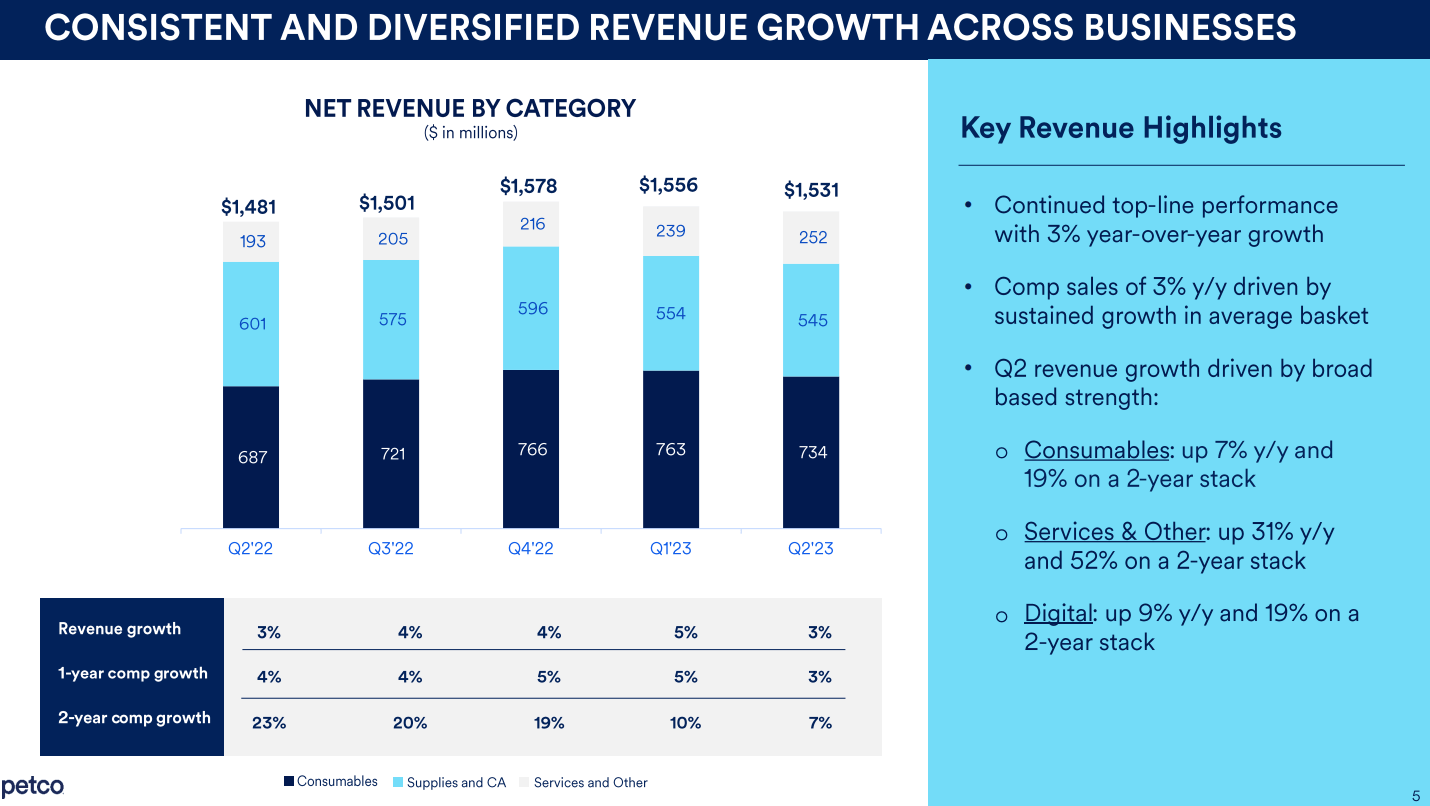

Petco shares plunged in late August when it released 2Q23 results as the company slashed its 2023 EBITDA guidance to a midpoint of $470 million, down 11.5% from its prior guidance. The main culprit was continued weakness in higher margin, non-consumable revenue (down 9% year-over-year in 2Q23 as shown below) linked to the pet adoption cycle. Non-consumable revenue includes items like crates, leashes, and toys which are closely linked to new pet ownership. New pet ownership has normalized following the pandemic-induced pet super adoption cycle of 2020-21, which led to a surge in products tied to new pets.

Petco Quarterly Revenue Composition (Investor Presentation)

{kind=link}

Despite the decline in non-consumable revenue, Petco saw continued growth in its services (grooming, veterinary, training, vaccination) business. Petco continues to focus on adding more veterinary services to its in-store offering.

I see services growth as being a sensible strategy for Petco and a key point of sustainable differentiation versus online-only competitors like Chewy ( CHWY ) and Amazon ( AMZN ). In addition to increasing traffic to its stores, pet services offer higher margins than products and should be a driver of an increase in profitability going forward.

Favorable Long-Term Demand

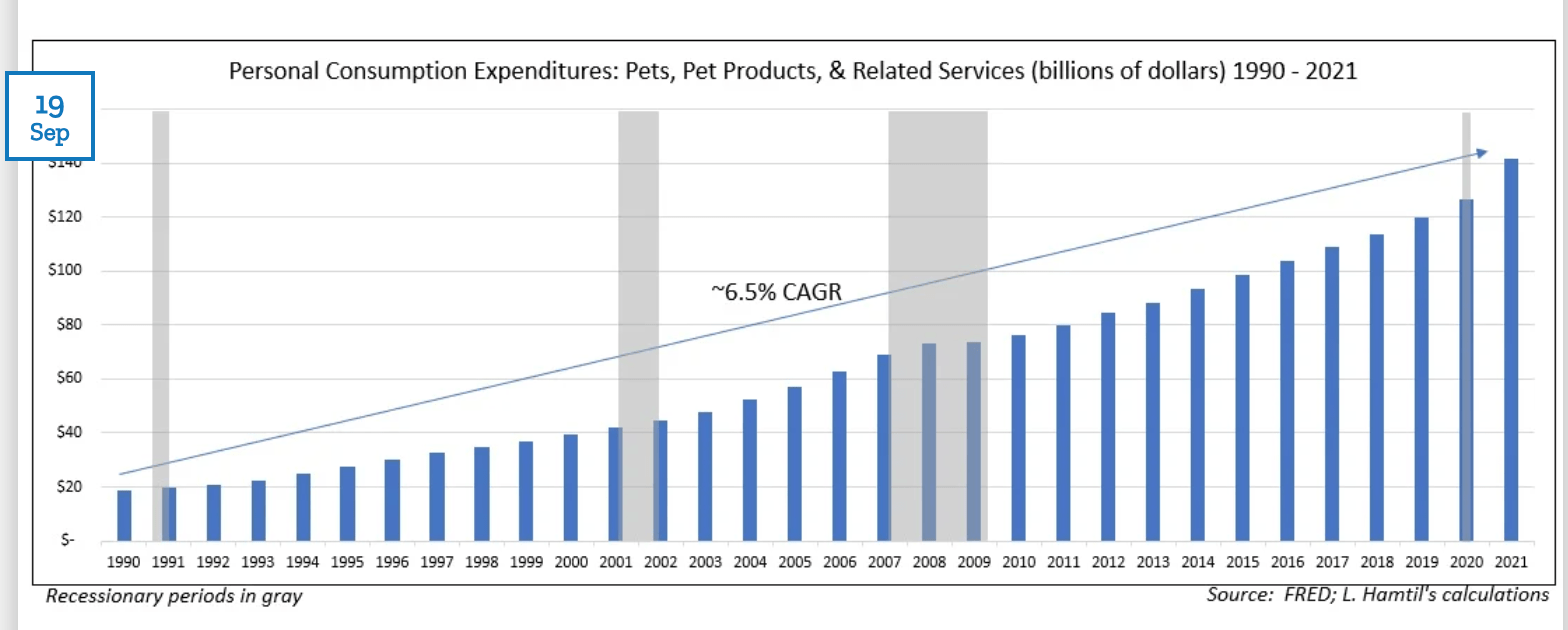

US Pet Spending since 1990 (Fortune Financial Advisors)

{kind=link}

As shown above, spending on pet products and services has increased at over 6% per year for the past 30 years, well in excess of GDP. Pet spending has been driven by:

- Favorable demographic trends as people get married/have children later in life, which frees up disposable income to spoil pets.

- Humanization of pets - people who adopt pets increasingly see themselves as 'pet parents' versus 'pet owners' which has led to higher quality pet care and premiumization of pet products and services (natural foods, pet hotels).

I believe that these demographics and behavioral trends are structural and expect spending on pet products and services to continue to increase faster than overall GDP for the foreseeable future.

Valuation

At the current price of $4 per share, Petco has an equity market capitalization of just under $1.1 billion and a total capitalization of ~$2.5 billion (including debt). This works out to an EV/EBITDA multiple of just 5.5x (using the low end of management's 2023 EBITDA guidance) and is a significant discount to the 9.5x EV/EBITDA that CVC Partners and Canada Pension Plan paid to acquire the business in early 2016. Similarly, competitor Petco was acquired for $8.7 billion in 2015 which works out to ~9x EV/EBITDA.

While higher interest rates have compressed valuations that private equity is willing and able to pay, I see today's valuation of 5.5x EBITDA as being unduly punitive. Given the favorable long-term trends in the US pet industry and the depressed valuation of Petco shares, I would not be surprised to see another bid for Petco.

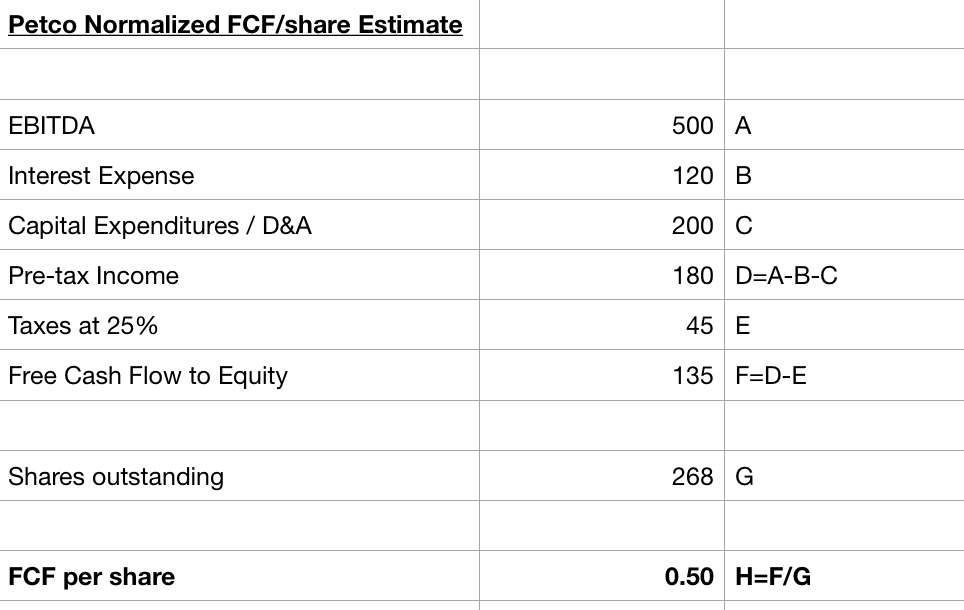

To look at the valuation another way, below I estimate normalized free cash flow per share for Petco:

Petco Normalized FCF/share Estimate (Company Filings; Author Estimates)

{kind=link}

My normalized EBITDA estimate is just 9% above the low-end of management's current 2023 guidance (and 5% below prior guidance and in line with actual trailing twelve months EBITDA). I expect growth in EBITDA given:

- Underlying growth in pet spending

- Continued increase in higher-margin services revenue as Petco continues to expand its service offering to more stores

- Potential benefits from the recently announced $150 million cost-cutting initiative, which is focused on supply chain efficiencies as well as a workforce reduction

Assuming modest debt pay down and a commensurate decline in interest expense and deducting capital expenditures and taxes, this results in $0.50 per share in free cash flow. At the current price of $4 per share, Petco trades at just 8x my normalized FCF estimate. Given favorable long-term trends in pet spending, a strong position in the industry, and an increased contribution from defensible, higher-margin pet services, I think a multiple of 12-15x is appropriate. This suggests a fair value between $6-$7.50, implying 50-90% upside.

Conclusion

Recent operational and share price performance has been disappointing. However, given favorable long-term trends, an increasing contribution from higher-margin pet services, and an attractive valuation, I believe patience will ultimately be rewarded, and have purchased shares in Petco.

For further details see:

Petco: Heavily Discounted Despite Favorable Long-Term Trends