XOM - Phillips 66 Benefiting From Historically High Distillate Yields

2023-10-19 14:33:36 ET

Summary

- Phillips 66's Refining Segment continues to be the dominant factor for earnings upside given PSX's high distillate yield and strong diesel margins.

- The company's acquisition of DCP Midstream's LP units will contribute to strong growth in the Midstream Segment's EBITDA over the coming year.

- Despite my continuing concerns about the Chemicals Segment performance, PSX's improved refining market capture could provide upside.

- Considering current FY23 EPS estimates are for $15+/share, the current annual dividend obligation of only $4.20 obviously leaves significant room for significant dividend increases going forward.

While Phillips 66 ( PSX ) has been heavily investing in its Midstream and Chemicals segments in order to diversify the company from the cyclical refining business, in the near term the company's Refining segment continues to be the dominant factor when it comes to earnings upside. From that perspective, PSX has a higher distillate yield, as compared to its peers and will benefit from continuing strong diesel margins. Today, I'll review Phillips 66's operations and discuss what investors can expect from the Q3 report, which is due out before the market opens on Friday, Oct. 27.

Investment Thesis

As most of you know, PSX has been executing on a multi-year plan to diversify away from refining by heavily investing in its chemicals and midstream segments. If you follow me, you know that I have not been impressed by the company's massive investments in new large-scale global chemicals plants because they're competing head on with other companies, like Exxon Mobil ( XOM ), that have been doing the same. As a result, there's arguably over-capacity in the global petchem markets and margins are very poor: See Phillips 66: Q2 To Show Weak Chemicals Margin (Again) . Meantime, PSX already has reached FID on two-more large-scale petchem projects even though the last two expansions have yet to reach decent profitability (sigh ...).

The much better news is that PSX, in June, completed the purchase of all DCP Midstream's LP units that it did not already own. As a result, the upcoming Q3 report will be the first full-quarter that will include all of DCP's LP results. Note that Enbridge ( ENB ) still owns a 13.2% economic interest in DCP via the General Partnership. As I have opined on Seeking Alpha, it's likely just a matter of time before PSX buys out ENB's remaining economic interests in DCP.

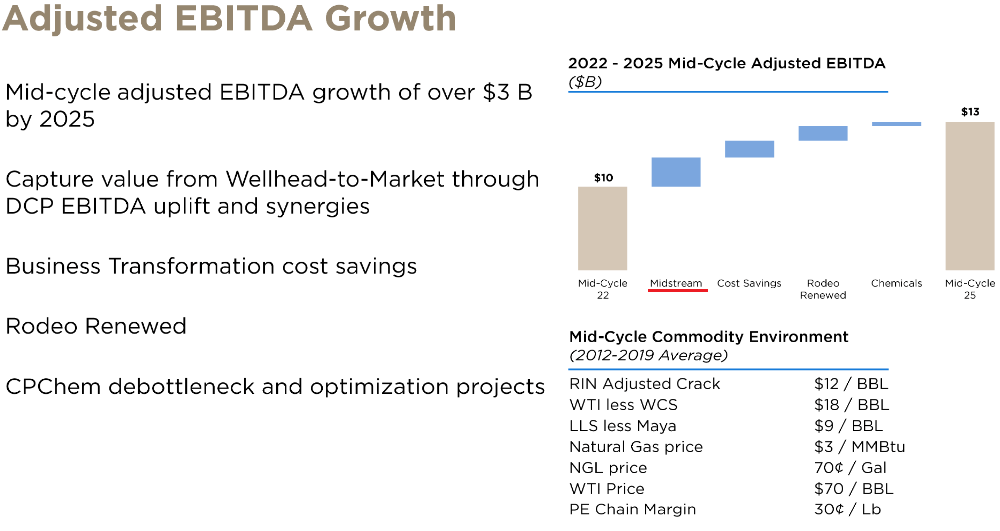

Regardless, and with DCP now firmly under the PSX umbrella, the company expects to deliver strong growth in Midstream EBITDA from its integrated wellhead-to-market strategy. Indeed, the Midstream segment is expected to be the biggest single contributor of the $3 billion in expected mid-cycle EBITDA growth from the period 2022-2025. This is shown in the slide below from PSX's August Investor Update Presentation :

{kind=link}

Phillips 66

Refining

However, and considering the moribund Chemicals Segment, near-term performance will likely continue to be dominated by the performance of the company's Refining Segment, which has been a laggard for years when compared to its primary competitors Valero ( VLO ) and Marathon Petroleum ( MPC ). This under-performance is clearly shown in the relative five-year total returns performance of the three companies:

Yet there is some good news in PSX's Refining Segment. The company has finally started to make some significant headway in improving its Refining Segment's market capture and expects to achieve an incremental increase of $400 million annually via refining margin expansion.

Meantime, PSX - which is the largest importer of Canadian Oil Sands WCS crude - is benefiting from its higher distillate yield as diesel margins remain strong as we head into the winter heating season (see graphic below). This is good news for PSX shareholders because, as you know, distillate demand is seasonal with increased consumption during the winter months.

EIA

As you can see from the diagram above, while below blow-out 2022 pricing, the 2023 distillate crack spread (green dots) has remained significantly above average and jumped higher toward the end of Q3, with the average August crack spread coming in at $1.10/gallon. That was $0.30 higher than the RBOB gasoline crack spread in August ($0.80/gallon). As a result, PSX continues to optimize its refineries for diesel. Indeed, on the Q2 conference call , Brian Mandell - head of PSX's Marketing & Commercial Operations - reported that PSX's exports were up nearly 50,000 bpd yoy during the quarter:

We exported over 200,000 barrels this quarter, which was up. In large part, our Sweeny refinery was making some higher sulfur diesel that we exported to Latin America. Like others have said, we have been exporting more distillate to Europe as trade flows from Russia change and Russia is importing more barrels, particularly into Brazil, 120,000 barrels to 140,000 barrels, and where U.S. exporting more barrels to Europe.

Meantime, the recent increase in Brent/WTI oil prices should mean higher margins for PSX's NGLs fractionation capacity as well as better pricing for PSX's LPG exports.

As a result, and according to Yahoo Finance , consensus earnings estimates for Q3 have risen sharply from $3.82/share 90-days ago to the current estimate of $4.76:

Yahoo Finance

For the year, the consensus estimate is for $15.71/share of earnings, which I believe may be on the low side given projections of only $2.97/share in Q4, which I believe is overly pessimistic given current market conditions and the recent increase in WTI. Also, the EPS estimates for next year appear to be on the low side as well given PSX's strategy to reduce costs while increasing efficiencies and refining margin expansion. However, PSX has been talking about increasing refining margin capture for many years, and it could be that the market is simply in "show me" mode.

Regardless, and given PSX's current stock price of $115.91 at pixel time, the $15.71/share EPS estimates equates to a P/E=7.4x and a forward P/E=8.5x. The current $4.20 annual dividend equates to a yield of 3.6%. This valuation level appears reasonable given PSX's past performance, the relatively poor performance expectations of the Chemicals Segment, and the macro geopolitical and economic environment.

However, I believe that significant upside potential exists if PSX management can show real and sustaining improvement in the Refining Segment's market capture. I also think it possible that PSX could benefit from accelerating its integration of DCP integration and realizable cost synergies.

The Dividend

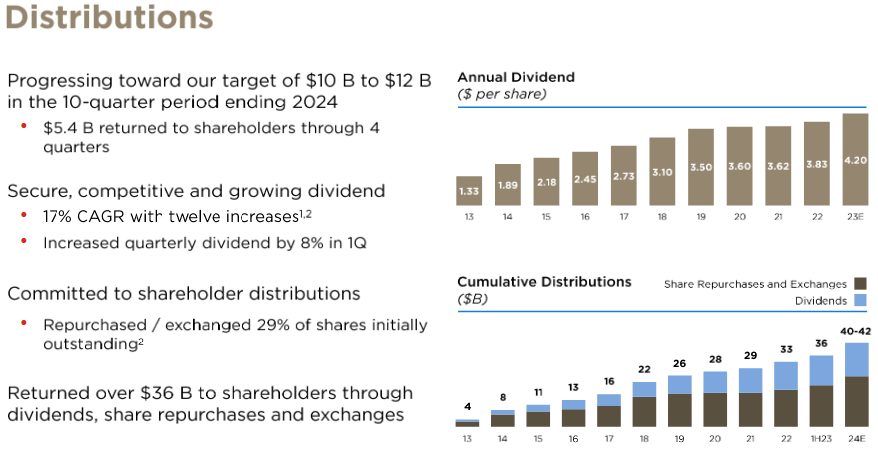

As seen in the graphic below of PSX's quarterly dividend growth, prior to the global pandemic, PSX was one of the best dividend growth stocks in the entire S&P 500:

Given the current dividend obligation is only $4.20 in comparison to expectations of over $15/share of earnings this year, shareholders can expect a big boost in the dividend. Remember, part of relatively new CEO Mark Lashier's strategy was a commitment to return $10-$12 billion to shareholders - via dividends and share buybacks - during the 10 quarters ending in 2024. So far, the company is ahead of schedule in that it has delivered $5.4 billion to shareholders over the first four quarters of the plan:

{kind=link}

Phillips 66

Risks

At the end of Q2, PSX had $3 billion in cash, $19 billion in long-term debt, and a net debt-to-capital ratio of 35%. That relatively high ratio is primarily a result of the DCP acquisition. However, the company is on record to reduce that leverage metric by the end of the year. Still, there should be plenty of free cash flow to reward shareholders with a hefty dividend increase.

Summary and Conclusion

Given PSX earnings outlook, continued strong distillate margins, multiple cost and operational efficiency initiatives, and its relatively low P/E ratio, I'm tempted to upgrade PSX from Hold to Buy. However, I have been frequently disappointed by the performance of PSX's Refining Segment in the past, and have decided to curb my enthusiasm and reaffirm my Hold rating. However, I do believe that upside risks are greater than downside risks and, regardless of the second half earnings reports, I expect a strong boost in the dividend sooner rather than later.

I'll end with a long-term total returns comparison of PSX vs. the broad S&P500 as represented by the Vanguard S&500 ETF ( VOO ) since the spin-off of PSX from its mother ship ConocoPhillips ( COP ) back in 2012:

As can be seen in the graphic, PSX was a significantly outperforming stock prior to the pandemic. But, just like Exxon Mobil , the company was caught with its pants down during the pandemic (mostly due to massive cap-ex over-spending on global petchem projects...) and had to leverage the balance sheet to meet its dividend obligation. I expect PSX will, once again, begin to outperform the S&P 500 going forward. Indeed, it's already starting to do so (see far right hand side of the chart above).

For further details see:

Phillips 66 Benefiting From Historically High Distillate Yields