TSLA - Polestar: Guidance Cut Again And Major Capital Raise Needed

2023-11-09 02:10:04 ET

Summary

- Polestar Q3 revenues of $613 million badly missed street estimates and the quarterly operating loss surged over the prior year period.

- The company reduced its delivery guidance for 2023 to approximately 60,000 vehicles, less than half of the original forecast.

- PSNY's financial situation remains concerning, with negative working capital, high debt, and the need for an additional $1.3 billion in external funding.

When it comes to the electric vehicle space, one of the most disappointing names in recent years has been Polestar Automotive Holding ( PSNY ). The company came to market with a grand growth plan and business model that looked to be one that would deliver for investors. Unfortunately, the name has consistently failed to deliver, with the latest set of results suggesting the stock could still have a lot more downside ahead.

For the third quarter , Polestar delivered revenues of $613 million. While this number was up 41% over the prior year period, it badly missed street estimates for about $727 million, or 67% growth. This is despite management slashing guidance for the year twice already, resulting in dramatically reduced analyst revenue estimates. In the United States, the company has been heavily promotional throughout this year for the Polestar 2, with better and better offers coming as 2023 has progressed.

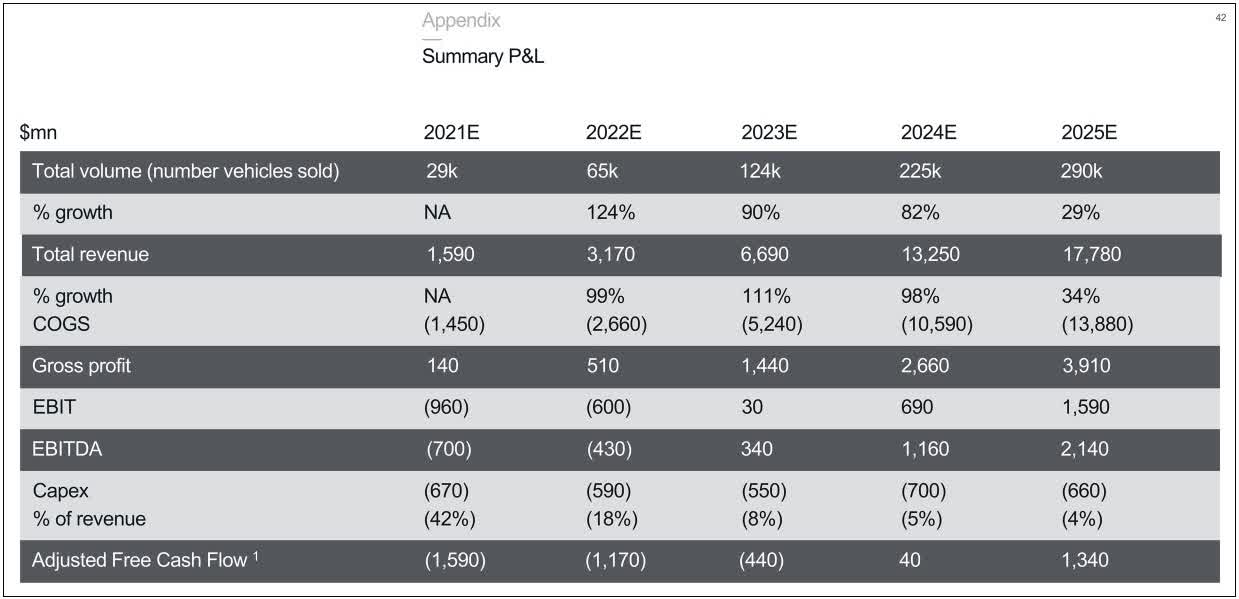

While Polestar is showing decent growth in vehicles delivered and total revenue, the numbers coming in are well short of what investors had been hoping for previously. Management reduced guidance on Wednesday again, now calling for deliveries this year of approximately 60,000 vehicles, down from the previous range of 60,000 to 70,000. This new guidance is less than half of what the company originally was looking for this year as the graphic below shows, although part of the shortfall is due to a new model release being delayed until 2024.

Polestar Original Guidance (Company SPAC Presentation)

{kind=link}

With such low volumes currently, Polestar is having a tough time getting those large gross profits it was hoping for. In the latest quarter, the gross margin figure was just 3.6%, down half a percentage point over the prior year period despite the revenue surge. Operating expenses also rose significantly, leading the company's operating loss to balloon by 33% to more than $261 million. The number here might have been even worse if not for a small gain recorded on the sale of the Chengdu manufacturing plant.

As I discussed in my most recent article , the biggest problem I have with the company is its overall financial situation. As the chart below shows, working capital continues to go further negative, finishing Q3 at a deficit of more than $2 billion. Polestar finished Q3 with about $950 million in total cash, but it has roughly $3 billion in debt, and that's not good in a rising interest rate scenario. Worse yet, the company's inventory balance rose again to a new high over $1 billion, which could result in more discounts and write-downs in the future.

Polestar Working Capital (Company Earnings Reports)

I've been talking for several quarters now about another major capital raise being needed here, and we did get news on that front Wednesday. The company has unveiled a new business plan , one that targets being cash flow break-even by 2025, with deliveries of 155,000-165,000 vehicles. Given the numbers I showed above, the new forecast is well below original expectations for almost 300,000 deliveries in 2025 and positive cash flow in 2024. The new plan came with the following quote from Thomas Ingenlath, Polestar's CEO:

Achieving cash flow break-even already in 2025 will show the strength of our asset-light business model. Margin over volume is our way forward, supported by a gorgeous line-up of four exclusive performance cars."

To me, this statement is out of touch and very misleading. There is no strength in the business model when you have to cut sales guidance by nearly half just to get to positive cash flow a year later than originally planned. Additionally, while the company got some additional financial backing recently from major supporters Geely Holding and Volvo Cars, it was revealed that Polestar still needs an additional $1.3 billion of external funding to get to this potential break-even point. That's more than a third of the stock's market cap as of Wednesday's close.

When you look at valuation, Polestar trades at a discount to other EV players in the space, going for less than 0.5 times expected 2025 revenues, although more revenue estimate cuts are likely coming. Industry leader Tesla ( TSLA ) goes for 4.8 times expected 2025 revenue, as it clearly has the best profitability and cash flow situation currently. Polestar trades more like some of the startups, being a little less than the average of names like NIO ( NIO ) going for 0.8 times and Fisker ( FSR ) at less than 0.3 times.

However, Polestar still trades for more than double what established automakers like General Motors ( GM ) and Ford ( F ) go for on a 2025 price to sales basis, so I can't really say shares are undervalued at this point. The average analyst price target was over $4 going into Wednesday's report, which would represent significant upside, but you have to figure that this number will be coming down moving forward. Also, it was just over a year ago that the street saw this name worth more than $11.

My personal rating on this stock remains a sell after this report. Management continues to take down guidance almost quarterly, so I need to see much better execution here. Second, that $1.3 billion needed to get through the next 12-18 months or so is a huge overhang that needs to be addressed, and that could push shares much lower. I would consider moving to a hold if the company can get its balance sheet in order, as well as if the stock moved more towards a price to sales valuation that's closer to Fisker since that is the name that 2025 delivery volumes will most likely compare to.

In the end, Polestar announced another very disappointing set of results on Wednesday, which could lead shares to a new all-time low. The company badly missed street revenue estimates for Q3, while also reporting a much larger operating loss than the year-ago period. Management again cut 2023 delivery guidance, now to a point that's less than half of the original forecast from a couple of years ago. The company unveiled a new business plan aimed at getting to cash flow break-even in 2025, but that's a year later than originally hoped and will come with much lower vehicle volumes. With a terrible balance sheet getting worse by the quarter, another billion dollars plus of external funding is needed in the next year or so. Until this name can show some measure of actual progress and get its financial house in order, I just cannot recommend owning the name.

For further details see:

Polestar: Guidance Cut Again And Major Capital Raise Needed