CSGKF - Position Your Portfolio For Falling Inflation And Continued Uncertainty

2023-04-14 04:26:59 ET

Summary

- Recent distress in the banking sector has created an additional layer of uncertainty across financial markets.

- While the future trajectory of monetary policy remains uncertain, inflation and many of its main components are moving lower.

- Given distortions in the market and the likelihood of volatility, investors might be well-served by employing a barbell approach within equity allocations.

- Adding duration within fixed income allocations eliminates reinvestment risk while also creating upside potential in the event interest rates decline in the foreseeable future.

The events and associated headlines in recent weeks have created a heightened level of uncertainty for financial markets. The failures at Silicon Valley Bank ( SVB ) and other regional banks here in the U.S., the takeover of Credit Suisse ( CS ) by UBS ( UBS ) in Europe, and the uncertain future path of monetary policy have created fear of a potential broader financial crisis. The debate has just begun on whether, and to what extent, FDIC insurance should be expanded, and the full impact of these recent bank failures is likely not completely understood yet. Fortunately, at least for the time being, it looks like the issue has been contained.

Higher interest rates combined with an increasing pace of corporate layoffs is a negative for real estate, both commercial and residential. It has become more difficult for families to afford homes as borrowing costs have climbed significantly higher while home prices remain sticky at elevated levels. Commercial real estate financed with variable rate mortgages may become vulnerable as interest payments increase while layoffs continue, reducing the overall demand for office space. One possible silver lining could be that more layoffs may serve as motivation for many to return to the office rather than continue working remotely. If you fear that you might lose your job, showing up at the office might help your chances of remaining employed. Just a thought.

Impact of Banking and Real Estate on the Economy

The importance of banking and real estate to the broader economy should not be underestimated. Banking provides the credit individuals and companies need to purchase assets and to grow. A slowdown in lending would be detrimental to all areas of the real estate market while also reducing the overall profitability of the banks. While SVB didn't take outrageous risks by investing in toxic assets, it did do a poor job of matching assets and liabilities, which is ultimately what led to its downfall. Let's hope that other banks, both regional and money center, have been more dialed in on risk management. SVB's issues have highlighted that at any given time there are known risks and unknown risks, and it is important to position investment portfolios to withstand a wide range of scenarios.

If the shake-up in banking cannot be contained, then ripples starting from the banking sector will quickly wreak havoc in real estate followed by the broader economy. In that scenario, it would be reasonable to expect a meaningful increase in the pace of layoffs. It is disappointing to write these words as it was less than two months ago that I believed that a "soft landing" was not just possible, but probable. While I'm not saying that's completely off the table, it is looking increasingly less likely. Shifts in markets and sentiment occur incredibly fast, a factor that shouldn't be underestimated. However, I continue to believe that the faster markets move, including measures of sentiment and momentum, that patient investors will continue to be rewarded in the long run.

While layoffs in the tech sector have drawn the greatest attention, it is likely too early to determine what the secondary effects will be. In many cases, the layoffs have been trivial in size compared to the hiring that was done over the last three years. Other than trimming headcount at the margin, many of the mega cap tech companies remain solid, with slow but positive revenue growth, relatively stable margins, and sizable cash holdings. Microsoft ( MSFT ), for example, is currently sitting on about $100 billion of cash and short-term investments, an amount that would be expected to insulate the company from any meaningful slowdown.

Monetary Policy

The Federal Reserve has put itself in a difficult position. By raising rates faster than any other time in its history, it has caused the yield curve to invert, insolvency (on a mark-to-market basis) at some banks, and effectively frozen the residential real estate market as mortgage rates have spiked much faster than the time needed for prices to adjust.

While the official measure of inflation has decreased well below its peak at about 5% in March, it is far from the target level of 2.0-2.5%. That said, most key inflation components have been falling (not just increasing at a slower rate) in recent months.

Inflation Components

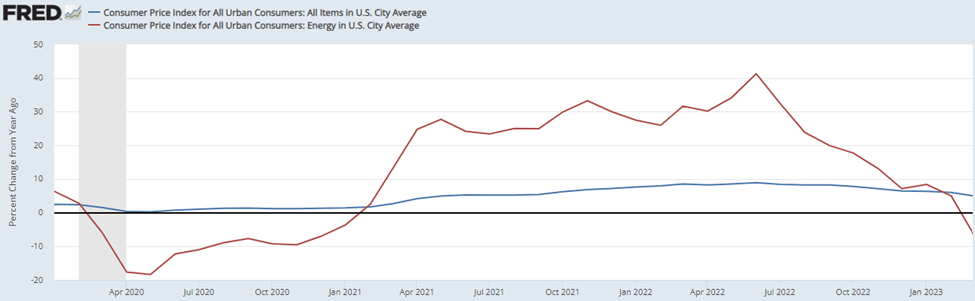

Energy prices have been falling since last June, driven by the decline in WTI crude prices from a 2022 high of over $120/barrel to the current level of about $75-$80 per barrel. Energy costs had been a significant driver of inflation, pulling the overall level higher since the beginning of 2021. The continued decline in energy prices since late 2022 has brought those costs back down to a point where they are no longer pulling inflation higher. In fact, according to the Bureau of Labor Statistics, energy costs decreased by 3.5% in March and fuel oil fell 4.0% during the month.

CPI versus Energy Costs (FRED)

{kind=link}

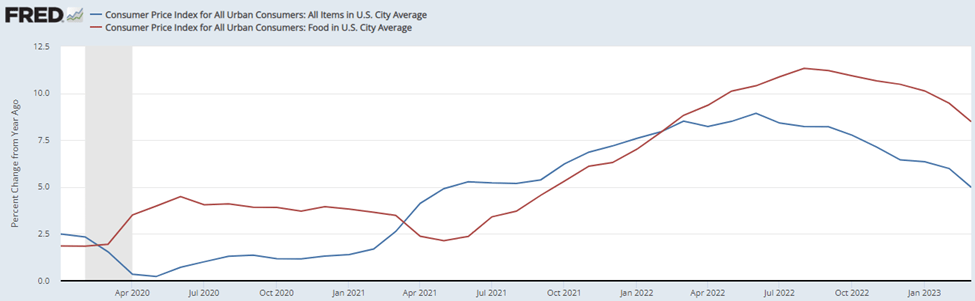

Food prices started increasing at an accelerating rate in mid-2021. While food prices, incorporating both at home meals and dining out, continue to be a positive contributor to inflation, that trend is slowing and in the process of reversing. Looking at the chart below, we see that while food price increases remain above inflation, they are declining at what appears to be an accelerating rate, meaning it is reasonable to expect food to no longer drive inflation higher in coming months. Looking at the stats from the Bureau of Labor Statistics, food prices were unchanged in March, with food at home decreasing 0.3% and food away from home increasing 0.6%. Clearly the food at home component has a larger weight than food away from home.

{kind=link}

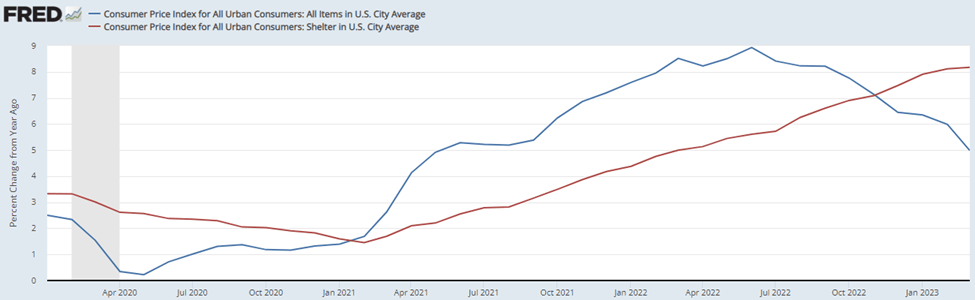

Unfortunately, shelter costs continue to rise and in recent months have been rising faster than the inflation rate. The chart below incorporates both mortgage and rentals costs and has been rising steadily since the beginning of 2021. While it is reasonable to expect shelter costs to be sticky at current levels, it is difficult to make a case that they will continue to rise at the same rate as the last two years. While mortgage costs have risen, it is reasonable to expect interest rates to level off soon, if they haven't already, and for the same to happen with house prices and rent. According to the Bureau of Labor Statistics, shelter costs rose 0.6% in March and are higher by 8.2% in the last twelve months.

CPI versus Shelter Costs (FRED)

{kind=link}

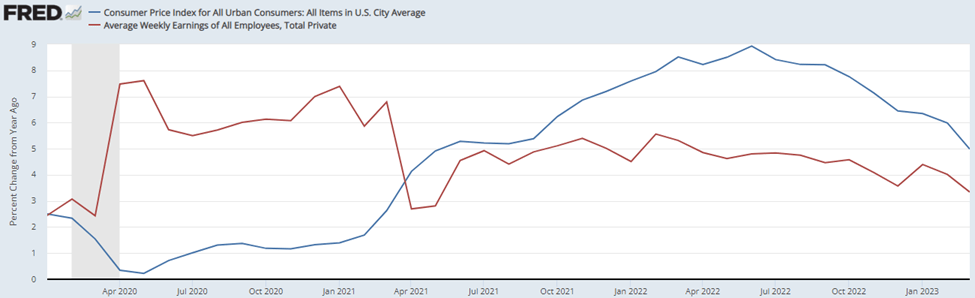

Furthermore, the idea that this has been wage-driven inflation is incorrect. Wages have been rising at a rate BELOW that of inflation for about the last two years. This means that wage growth cannot possibly be the culprit for sticky inflation at this point.

CPI versus Earnings Growth (FRED)

{kind=link}

Positioning Portfolios

In this period of uncertainty and disjointed markets, it can be difficult to find a clear approach to portfolio management. I remain focused on maintaining a highly diversified strategic allocation for the long-term but see opportunities at the margins for some improvements both within equities and fixed income.

Equities: A Barbell Approach

For equity allocations, a barbell approach might make sense in this environment. With uncertainty comes a wide range of strong opinions that ultimately lead to increased volatility. A barbell approach in that situation would be expected to provide some downside protection while also allowing for upside appreciation.

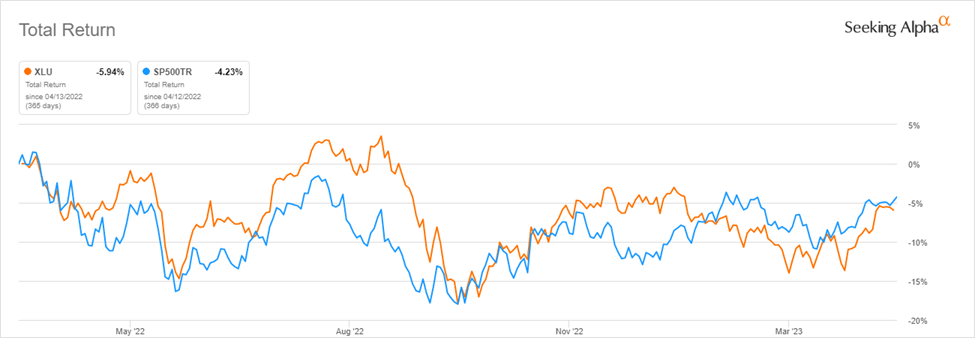

For the safe side of the barbell, I suggest adding to utilities. While the sector is lower by nearly 6% on a total return basis over the last year, it has performed similarly to the S&P 500. As the Federal Reserve slows, stops, and at some point, reverses, its tightening, utilities will become more attractive. While they are low beta relative to the broader market and expected to be resilient during any economic slowdown, a pause in raising or decrease in interest rates will make these companies more attractive from a discounted cash flow perspective.

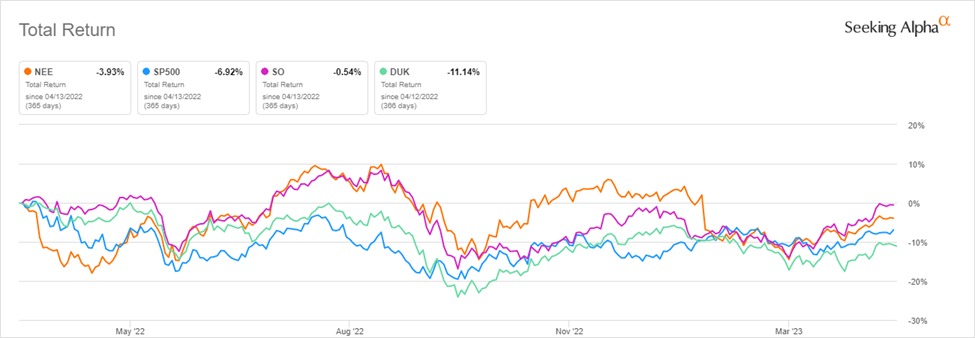

As with most of my suggestions, I suggest acquiring, or adding to, diversified exposure to the space through a low-cost ETF. I use the Utilities Select Sector SPDR ETF ( XLU ) that has an expense ratio of 0.10%, a current yield over 3% and holds a portfolio of about 30 names. It is important to be aware that the top three names in the fund, NextEra Energy ( NEE ), Southern Co. ( SO ), and Duke Energy ( DUK ) represent over 30% of total portfolio value.

1-Year Total Return: XLU versus S&P 500 (Seeking Alpha) 1-Year Total Return: NextEra, Southern Co, and Duke Energy (Seeking Alpha)

{kind=link}

{kind=link}

On the riskier end of the barbell, I am looking at large cap tech. As mentioned above, mega cap companies like Microsoft and others are holding enormous amounts of cash and equivalents on their balance sheets, assets that would insulate these businesses in the event of a broader turndown. The layoffs in the space have not been a cause for concern in my opinion as they have been trivial relative to the hiring of the last three years and relative to their total headcount.

While many of these names have already rebounded during the first quarter, I continue to believe that they offer more upside over the long run while maintaining the ability to be resilient during any possible downturn. In an environment in which interest rates are stabilizing and eventually decreasing, it is reasonable to expect revenue and profit to rebound within the tech sector. Furthermore, as a premium is placed on future growth and earnings, and lower discount rate driven by falling interest rates would be expected to result in higher valuations.

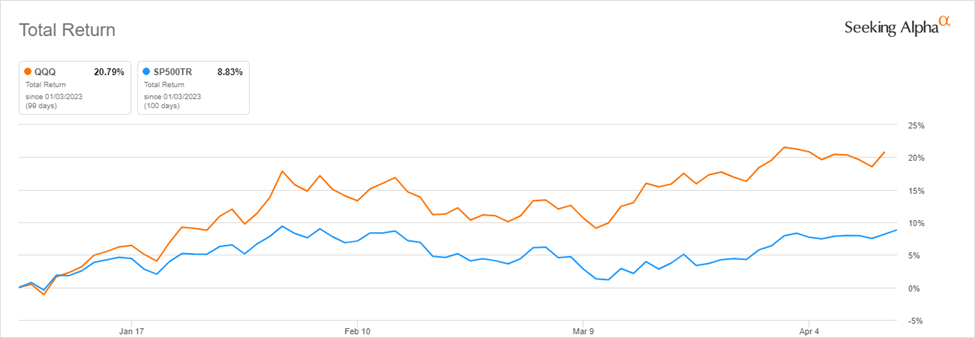

With my typical focus on simplicity, I think it is reasonable to make a broad bet by adding the Invesco QQQ Trust ETF ( QQQ ). It removes idiosyncratic risks that result from holding individual stocks. The fund also provides market weight exposure to the most important names in the tech sector as well as communication service and consumer discretionary. The top three positions, Microsoft, Apple ( AAPL ), and Amazon ( AMZN ) represent over 30% of the fund's value with the remaining 97 names representing the other 70%.

YTD Total Return: QQQ versus S&P 500 (Seeking Alpha)

{kind=link}

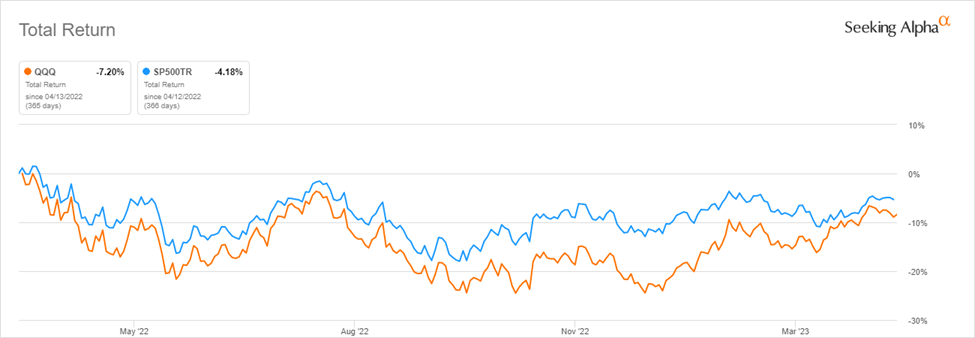

While many names in the fund are off to a fast start year-to-date, the trailing 1-year performance remains below that of the S&P 500.

1-Year Total Return: QQQ versus S&P 500 (Seeking Alpha)

{kind=link}

Bonds: Adding Duration

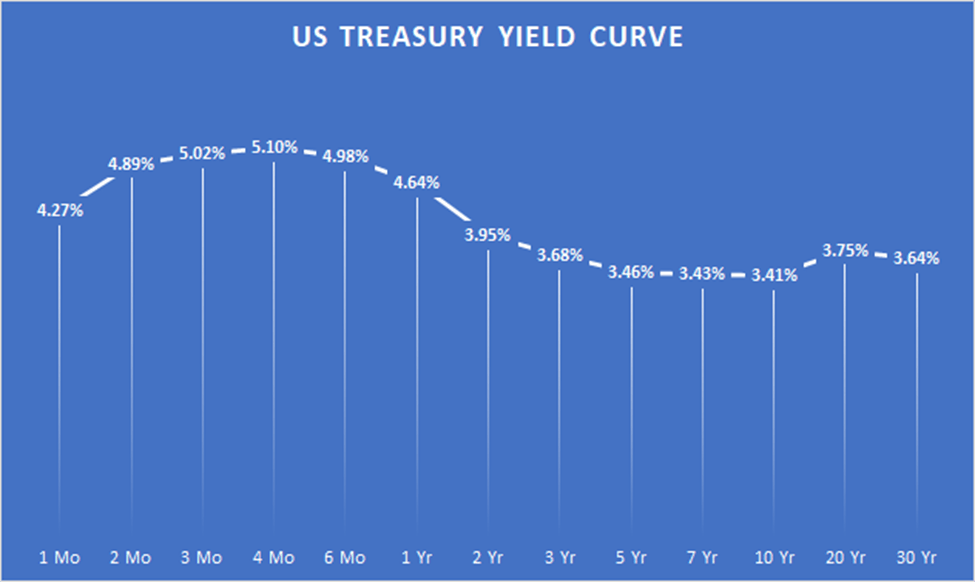

Despite an inverted yield curve, it might make sense to add duration to bond allocations. While investors can earn more on an annualized basis on T-Bills versus long bonds, those yields come with reinvestment risk as well as providing little upside if/when interest rates stop increasing or decline. Buying further out on the curve generates a lower yield, but it eliminates the reinvestment risk, and the longer duration exposure provides the possibility for upside in the event rates fall.

US Treasury Yield Curve (US Treasury Department Data, Author)

{kind=link}

To gain exposure to long-term Treasuries, I use the iShares 20+ Year treasury Bond ETF ( TLT ). The fund is down nearly 10% on a total return basis over the last year, a significant decline for the fund in a 1-year period. For the full year 2022, the fund declined by 27.7% on a total return basis.

1-Year Total Return: TLT (Seeking Alpha)

{kind=link}

However, those returns have been driven by the aggressive tightening by the Fed during that period, a situation that is unlikely to repeat itself moving forward. Because I believe that it is reasonable to expect monetary tightening to slow, and possibly reverse, adding duration at this time makes sense. Given the level of interest rates, inflation trends, and other economic data, I see asymmetry between the relatively small downside risk versus the potential upside.

Final Thoughts

Like most times throughout history, investment and trading decisions are driven by the uncertainty in the economy and financial markets. The pandemic and the economic shutdowns are decisively in the rearview mirror at this point, but we continue to work through the consequences, both intended and unintended. The distortions that shutdowns, monetary policy, fiscal policy, and supply chain issues have caused are likely to remain for another couple of years in some form. Long-term, I am bullish. I am optimistic that capitalism will continue to create wealth and push asset prices higher, creating an opportunity for patient investors. However, in the more immediate term, there are simply too many unpredictable variables to be certain. Because of this, I am suggesting that investors tweak their portfolios using a barbell approach to both protect from the downside while keeping the door open for growth. These suggestions should be considered within the broader context of strategic asset allocations as well as personal needs and constraints. Any overweight or underweight positions need to be considered carefully to understand the impact on long-term total returns. Thank you for reading. I look forward to seeing your feedback and comments below.

For further details see:

Position Your Portfolio For Falling Inflation And Continued Uncertainty