AEVA - Post-Merger Ouster: The Aftermath Remains To Be Seen

2023-03-27 23:30:42 ET

Summary

- Ouster remains my bet on Lidar, based on technology.

- The lack of the yearly forecast is understandable but weakens the story.

- Expect messy costs for at least two quarters.

- The merger's aftermath will remain unknown for some time and represents a risk in its own right.

Introduction

In this review, I follow up on Ouster's ( OUST ) results, assessing pre-merger Ouster with some indicators of post-merger outcomes. Evaluating the company's full-year potential based on just 40 days of operating as a merged entity is challenging. The merger's aftermath is unknown as the company moves through consolidation and reorganization. However, Ouster remains my bet on Lidar because of its technology, digital Lidar, now entering B sample in consumer automotive applications, and its leadership in non-ADAS applications.

Although Ouster may require selling equity, the amount needed is considerably less than that of other companies. This is mainly due to the company's existing cash runway, which enables it to focus on achieving realistic profitability. Furthermore, Ouster's strategy offers some risk aversion over its future, as it has 850 clients in 50 countries, differentiating it from companies that rely solely on one vertical or a single customer.

Results

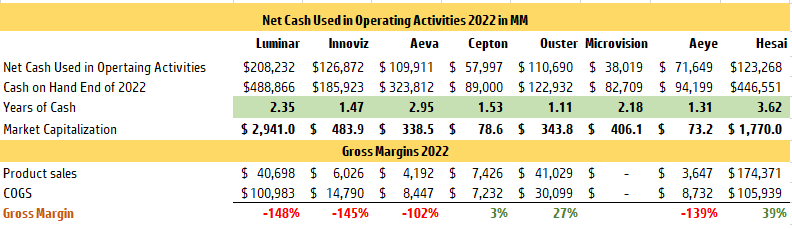

I want to start with Ouster's first-quarter revenue estimate of $15 to $17M. That is more than Innoviz ( INVZ ) will do in the year, and almost as much as Cepton ( CPTN ) plans to do. More than Aeva ( AEVA ) sets as a yearly target. Analysts charted by Yahoo Finance still see $103M for 2023.

On February 10 th , the company signed an amendment to a loan with Hercules, and the document features a trailing 12 months revenue table with a goal of $78M in 2023. Low, but still, a Luminar's ( LAZR ) territory of revenue expectations for the year.

The $40 to $55M range for 2022 revenue was barely breached by $1M when the company achieved $41M. That wasn't very reassuring. Q4 revenue was under $11M, missing expectations. The margins were 17% for the quarter but 27% for the year. Sensors shipped was a new record for a quarter with 2,950 units and the year with 8,650.

I put some of those numbers to show the evolution of Ouster in 2022 in comparison to 2021. The company achieved 22% revenue growth, a 34% increase in shipments and a drop of the ASP per sensor by 9%. The gross margin looked similar to 2021 but was down by 2%, as COGS did not drop fast enough, coming down only by 8%.

The news release announcing smart infrastructure revealed that agreements had doubled to 213, with a demand for 3,500 sensors in 2022. However, shipments to this vertical decreased by 20% during the year. The expected revenue from this demand must be part of 2023 projections and factored into $70M of bookings made in 2022—a term which replaced the previously used strategic customer agreements.

Despite losses in the robotaxi, bus, and truck under the automotive vertical, the industrial and robotics verticals grew significantly last year.

Ouster Shipments by Vertical (Ouster Inc. Author)

The merger between the company and Velodyne was completed on February 10th. Ouster gained intellectual property of many patents, the ability to collect licence fees from other manufacturers and cash. Still, the company now faces pressure on its gross margins supporting sensors sales, most recently sold at a deep loss by Velodyne.

The solution is to continue moving a selective suite of sensors into the Fabrinet plant in Thailand throughout the year, a process initiated by Velodyne to make loss turn into a positive margin.

But the battle for margins hit closer to home, as during Q4, Ouster experienced a drop in gross margins to 17%, primarily due to the startup cost of a new sensor line and the shipment of a large volume of sensors at a low ASP, which I assume was for Amazon. I anticipate that the REV6 inventory worth $20M in Q3 may be discounted until it is sold out, adding to pressure on the margin in Q1 and Q2.

Furthermore, the merger will result in an accounting laundry list to consolidate two companies. As a result, the costs in Q1 will be the highest for the year. I also anticipate that Q2 may not be in the best shape as the reductions will continue adding one-time costs. Only in Q3 do I believe we will see the desired operating cash cost.

The lack of forecast

It is unclear whether the absence of a forecast is the first casualty of the new regime, but there are several reasons why Ouster may have chosen not to offer yearly revenue guidance. One possibility is that the company recognized significant uncertainty in its business. That reason seems to be embraced by the Wall Street analysts as at least three decided to drop share price recommendations following the conference call.

Another reason could be that the new CFO, Mark Weinswig, wanted to avoid any negative impact if revenue guidance was missed, as a missed guidance in 2022 created a mess in the stock price and led to a loss of trust in the then CFO.

Lastly, the merger process and introduction of the new products, REV7, and a new market entry with Gemini and Blue City software packages could confound the outcome enough to hold off on long-term expectations.

As someone who has criticized AEye ( LIDR ) for not offering guidance and praised Luminar for doing so, I am disappointed to see Ouster without full-year guidance. The company's differentiation of being the consistent revenue leader and steadfast operator in a non-ADAS environment is hard to defend with only quarterly updates. That puts Ouster at a disadvantage even though Ouster is compared to competitors who excel in PowerPoint presentation skills.

On the other hand, Ouster never received a premium valuation for having revenue in the first place and the ability to offer reasoning behind its guidance. The absence of an ADAS order book celebrated across the spectrum of analysts covering the space had always put Ouster on the periphery of interest and deprived it of recognition. The fact that the analysts on the call did not pick up on CEO Angus Pacala's excitement over the B sample coming to the OEMs' hands and did not ask any questions confirms their exclusionary behavior.

The cash management

I still consider current cash insufficient to carry the company to profit. At $315M, cash seemed like a good starting point. A $75M reduction of the running rate within nine months of the merger via synergies also sounds desirable. The company already achieved a $50M reduction in the first quarter, at the one-time cash cost of $12 to $14M, out of the $30M total severance based on eliminating 200 jobs.

But what is the running rate which gets reduced? As per CFO:

"The synergy estimate is baselined against the stand-alone cost structures of the two companies as of the third quarter of 2022."

Velodyne had used $26.3M of net cash in operations during Q3. Ouster had $27.8M. I understand the quarterly running rate of combined entities would be $54.2M without synergies and, for a year, $217M.

Carving out $75M leaves $142M and quarterly spent of $35.5M with the synergies. Since Ouster took $50M out in Q1, I calculate $41.7M as the run rate for Q2.

I put all those figures into the table, adding prospectus numbers and already mentioned the trailing 12 months' data from the loan agreement. I see $180.9M for cash costs for 2022. My figures are about $14M more, perhaps because of the severance. As a checkpoint, I saw Andres Sheppard, from Cantor Fitzgerald, opine that the annual cash burn is only $107M. I wish he were right because that is less than cash burned by Ouster in 2022, discounting the addition of 60 more staff members.

In my cost analysis, I decided to use $97M rather than $78M as revenue in 2023 and calculate the spending for the year. Why? $78M is my guesstimate of revenue in 2022 for the two companies combined. I hope to see growth. I also assume that the inclusion of expectation in covenant as a level of revenue should be on the conservative side of things, meaning achieved with ease. Once more, I like to remind the reader those figures are all cash. The operating expenses within the income statement will differ because of stock compensation. What I am tabulating will be found in the cash flow statement, the part about operations.

The ending cash for 2023 is about $145M. Revenue of $78M will leave a bit less, around $140M. No kidding, $194M for cash spent is a huge number. I am unsure about the merger costs figure, but those come from the prospectus. Did the company pay some in Q4, perhaps? In the absence of the Velodyne balance sheet, it is a guess. When Q3 ended, two companies had $353M of cash. At the end of Q4, Ouster declared $315M for both companies, but Ouster added $20M cash from the draw on debt. That would indicate a $58M cash burn in Q4, with $27M done by Ouster. I feel that my cash burn is more realistic than Sheppard's.

{kind=link}

Net Cash Used in Operations (Financial Statements - Author)

Then I took a look into 2024. I used the forecast again from the prospectus, where the cash cost dropped to $132M. I put a small equity offering for $11M to prop a cash account supporting the Hercules loan. The revenue of $147M is from the prospectus, but the mentioned T12M table has it at $150M. Everything else in the table combines the prospectus and the T12M, which ends in the first half of 2026, having $250M for it. I took the liberty to take it to even $500M and go for $700M in 2027.

Ouster will need around $73M equity sale; if they fancy paying the loan, another $50M. There is a good chance that the costs I am showing can be reduced, and the revenue given is increased. The mass production for the OEM partner is still expected in 2025 and certainly in 2026, so the numbers could be better. Not sure whether they can be better between now and 2025.

Ouster Cash Runway (Ouster's SEC published documents, Author)

Amazon warrant

One venue to get cash is an Amazon ( AMZN ) warrant worth $5.07 per share at some 32.6M shares. Inherited from Velodyne via merger, it automatically vested upon merger to a total of 18.5M shares available to purchase by Amazon. 32.6M shares at $5.07 is $165M. 18.5M shares would provide $93M cash. If Amazon elects to exercise it all, it will enable Ouster to reach the profit year in 2026 at a dilution of 8.4%.

I want to quote the fragment from 10-K describing the unvested warrant and the relationship with Amazon:

"Warrant vested as a result of the Velodyne Merger, and the remainder will vest over time based on payments by Amazon or its affiliates to us in connection with Amazon's purchase of goods and services from us."

Ouster offered a meek confirmation of the business relationship with Amazon. We have all seen Proteus robots equipped at one point with a Velodyne sensor but replaced by OS. I will take that in the absence of a news release.

In my other articles, I speculated a $185M equity sale for Luminar and as much as $262M for Innoviz. The exact equity sale requirement is actual for Cepton and AEye. During the banking crisis and high-interest rates, how will those companies sell equity while competing for dollars with the strength of their business objectives and order books? Can one think that vested warrants represent comfort? Maybe, and I hope so, but for now, it is just an option for Amazon.

Technology roadmap

Digital Lidar is the future of the Ouster product line despite the support for Velodyne sensors adopted as VLP-16, VLP-32 and VLS-128. There will be margin pressures here as the company continues transitioning those products into Thailand. In the end, while they will be manufactured based on agreements made by Velodyne, the hope is that OS models will replace pucks sooner rather than later.

The most significant impact from the CC is the early B sample, which is coming to OEMs second part of the year. Some of the descriptions given by the CEO during the conference call are worth quoting here because they are exhilarating:

"We released our first A samples in 2022, which demonstrated that our solid-state digital flash architecture could achieve the stringent performance requirements of the automotive industry at a competitive cost. In the second half of the year, we plan to release final form factor early B samples of our DF sensors. This is a critical milestone on our automotive roadmap and in our commercial engagements with automakers, including our strategic OEM partner. For the first time, we will be placing DF sensors in OEM hands to represent the final size, shape and performance of the DF product line. I can't wait to demonstrate the performance, cost and flexibility advantage of the DF product line."

And this one:

And I would actually point to what Ouster is doing in automotive and bringing now, looking to 2023 with the DF sensor line finally coming with early B samples into the automotive market as an indication of the presence Ouster is going to have in this market that historically some of our competitors thought was safe. And just to highlight some of the benefits that we are bringing to the market there. The DF sensor is really targeted at ultra-cost competitive, high performance modular sensors to go into the consumer vehicles that you and I drive. And there is immense amount of technology that has gone into building the world's highest performing solid-state digital lidar sensors in this DF product line and doing it at a cost point that is fundamentally shifting the entire kind of landscape of automotive Lidar.

What I like about B sample info is that Ouster did not lose its place on a train to 2025/2026 production. Innoviz and Aeva also aim for their production to start in those years. Luminar is not coming with a new sensor until the 2030 production date, and the current one's form factor can be loved by its creators only. Anything with the same spec but smaller will replace it. I expect the digital Lidar sensor to be the end game, but it has to compete on specs, so hopefully, when the spec is published, the end game will be apparent.

The table below helps to illustrate the current state of automotive deals made by non-Chinese, US-publicly traded companies. 2023 will shape the industry for the next few years, but everyone on that list will need cash raise to reach imagined or actual profitability, while some will only extend their stay as long as possible.

Automotive Deals US-listed Companies (Companies' data - Author)

Conclusion

I believe there is a need for equity sales ranging from $73M to $123M, including the payout of the Hercules loan. Additionally, the option available to Amazon to exercise the vested warrant could provide $93M. The merger has resulted in cost reductions through synergies, but the company will continue to work in the next two quarters, and the results may not be as attractive to the markets based on the spending. I expect the cash burn in 2023 to be between $180M to $195M, a significant amount in the current business environment.

By the end of 2023, I expect Ouster to have $140M to $145M in cash, placing the company in cash holdings after Luminar ($300M) and Aeva ($200M). I am hoping for Ouster to keep up in revenue with Luminar in 2024 but be a much leaner business with a lot less cash burn, at $132M vs $265M. I see little revenue coming to Aeva in 2024.

Ouster is at risk of delisting due to its sub $1 condition, and a reverse split may be necessary. At this point, I doubt this matters to anyone anymore. A long-term investor can see the necessity to continue and perhaps the potential for equity sale beyond the penny level as more accessible. If Amazon exercised the warrant, it is evident that the share price would follow, but nobody publicly knows the deal here.

While the reverse split ratio would apply to warrants equally, it isn't easy to envision Amazon paying $50 per share, opening a door for readjustment and negotiations. Despite the risks, I consider Ouster a buy, as explained in my opening, as it has a believable path to reach profit and product quality for success. However, in the short term, there are concerns regarding gross margin pressure from Velodyne pucks and the potential reduction of ASP due to scaled-up sales to Amazon. These sales could help vest the rest of the warrants, but their long-term worth depends, in the end, on Amazon's purchasing the stock.

For further details see:

Post-Merger Ouster: The Aftermath Remains To Be Seen