XLU - Potentially The Greatest Swap Idea In CEF History: Sell GUT Buy PGP

2023-04-04 11:48:38 ET

Summary

- What could go wrong with a fund near an all-time high 105% market price premium combined with a near all-time low NAV?

- Shareholders of the Gabelli Utility Trust may think they own a safe utility stock fund offering a very attractive 8.4% current market yield, but that couldn't be further from the truth.

- Only one other CEF in recent history has breached the 100% market premium level and that was the PIMCO Global StocksPLUS & Income fund.

- Today however, after four distribution cuts since 2016, PGP's premium has collapsed from a high of 110% in July of 2016 to only 1.2% today.

- What happened? Well, read on and find out why I turned my bearish opinion around and made PGP my Top Specialty Pick for 2023. And just as importantly, is there a lesson to be learned for GUT shareholders? Well, let's just say this might be the greatest swap idea in CEF history.

What is the biggest mistake income investors make when choosing a CEF? They only look at the fund's market price, market yield and market price performance.

I've called many, many CEF distribution cuts and distribution raises over the years, and you know what? None of them had anything to do with a CEF's market price or market yield.

That's because it's the "behind-the-scenes" statistics that investors should be paying the most attention to and no statistic is more important to a CEF than its NAV yield. That one statistic would keep most CEF shareholders out of trouble, and yet, I would estimate that 95% of CEF shareholders have no idea of what their fund's NAV yield is.

I'll go one step further and say that most CEF shareholders have no idea of what their fund's NAV and NAV performance is either, and yet, these easily calculated statistics will give you everything you need to know about whether your fund is overvalued or not and whether it will be able to maintain its distribution.

Take the Gabelli Utility fund ( GUT ), $7.16 current market price . Do you think any shareholder would be concerned that GUT has an 8.4% current market yield? Probably not. They may think that's very generous for a utility fund, but they probably just figure that's the added yield that the fund generates with leverage.

But what if I told those same shareholders that's not the case at all and that the real yield that GUT has to pay is its 17.2% NAV yield. Do you think shareholders would feel as confident anymore, particularly when they realize they're not even receiving half the yield of what the fund is actually paying?

How does that make any sense whatsoever and how does GUT mosey on along at over a 100% market price premium like everything is A-OK even while its NAV is near an all-time low?

Y-charts

Now don't get me wrong, GUT may be the best managed utility focused fund in history, but that still doesn't take away from the fact that GUT's NAV yield is still way too high. How else can we see this other than looking at GUT's 17.2% NAV yield?

Just go to GUT's Annual Report as of 12/31/2022 and see that for the year, GUT's Net Investment Income - NII - was $5,255,626 (page 11) and yet GUT paid out ($42,192,023) in distributions to shareholders last year.

And that distribution total will just keep going up after last year's Rights Offering and the fund will probably need another one this year. Clearly, 2022 was difficult for all funds but did you know that the SPDR Utility Select ETF ( XLU ), utilities actually gained +1.4% in 2022?

So if utility stocks were up slightly last year, why would it be necessary to go to the well again with a Rights Offering ? Could it be because GUT will have a hard time covering its NAV yield no matter what market environment we are in? And is there any limit to how many times shareholders will be willing to pay a 35% premium over NAV just to help shore up GUT's NAV?

Heck, the Cornerstone funds ( CLM ) and ( CRF ), which also have extraordinarily high NAV yields of over 21% , use Rights Offerings priced over NAV too to help shore up the fund's NAV. Only shareholders are asked to pay a 12% premium over NAV, not 35% .

But even with NAV total return performances that blow away GUT's and even with a shareholder friendly reinvestment option that no other fund family offers, the Cornerstone funds have only been able to get back up to about 15% market price premiums over NAV, nowhere close to their 60% premiums they once commanded.

And yet, GUT continues to mosey along at a 105% market price premium.

When Good Funds Keep Putting Off The Inevitable

In early 2016, I wrote this article, Equity CEFs: PIMCO's Sinking Ship , which was my latest warning to shareholders of the PIMCO Global StocksPLUS&Income fund ( PGP ), $7.37 current market price , when the fund was at $17.91 and an 87.1% market price premium, that PGP was on an unsustainable path due to its extremely high 23% NAV yield.

Understand, this had nothing to do with the fund's income and appreciation strategy and I even said in the article ,

You can't beat PIMCO's fixed income research and capabilities and PGP is really just a heavily leveraged exploitation of those capabilities. Combine that with PGP's long E-mini futures positions on the S&P 500 and PGP can have incredible upside as well as downside potential both in its market price and NAV.

No, PGP's seeds of destruction back in the summer of 2016 had to do with its NAV yield. And combined with a bond and equity market at near all-time highs at the time, if PGP couldn't cover its NAV yield back then, then how could it reasonably be expected to cover it's NAV yield going forward.

And if you can't cover your NAV yield then the end result is NAV erosion, which only accelerates with a lower and lower NAV. And this was PGP's problem at the time.

What Is The PIMCO Global StocksPLUS & Income Fund?

This might be a good time to briefly explain what PGP is. Despite its name, PGP is not really global and not really stock oriented. In fact, PGP is really like most of the popular PIMCO multi-sector fixed income CEFs, but with an added twist.

Most of PIMCO's fixed-income CEFs are heavily leveraged in corporate bonds, both high-yield and investment grade, mortgage-backed securities, both agency and non-agency, bank loans and to a lesser degree, other US and sovereign debt instruments.

So in that sense, PGP is not that much different than say, the PIMCO Corporate and Income Opportunity fund ( PTY ), $12.58 current market price or say, the PIMCO Dynamic Income fund ( PDI ), $18.09 current market price , two very large and very popular PIMCO funds.

Here is PGP's homepage:

PIMCO Global StocksPLUS & Income Fund

Now all of the PIMCO fixed-income CEFs, including PGP, may have different fixed-income sector weightings, leverage amounts and sources as well as average maturities, but the real difference that separates PGP from the other PIMCO fixed-income CEFs is that PGP is the only PIMCO CEF that takes a portion of its portfolio income and goes out and buys S&P 500 E-mini derivatives on a regular basis.

And from a notional value standpoint, these E-mini futures can represent huge equity positions (which is where the StocksPLUS comes in), meaning PGP can capture enhanced S&P 500 upside as well as bond market upside when both markets are rallying.

As we know, both equity and bond markets have been in bear markets over the past year and this has hurt all of the PIMCO CEFs, not just at NAV and MKT prices, but in particular, their premium valuations which for many of the PIMCO fixed-income CEFs, reached as high as 50% .

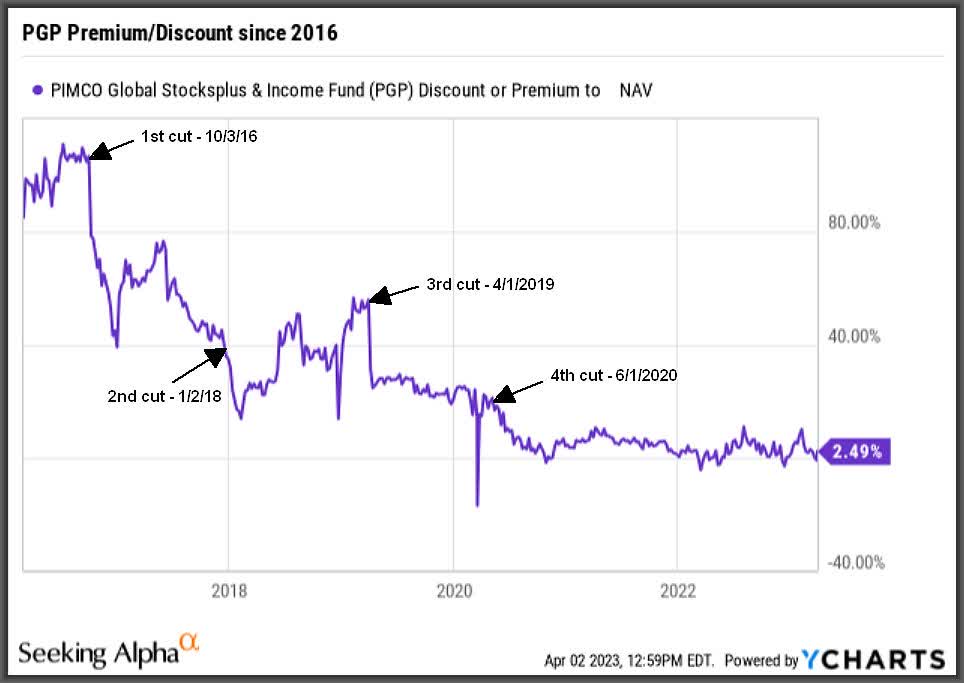

But none of the PIMCO fixed-income CEFs came close to PGP's 110% market price premium high-water mark, though PGP started losing valuation when the fund first declared a distribution cut on Oct. 3, 2016. And the very next day, I wrote this article, Equity CEFS: The Sum Of All Insanities - Part II

PIMCO would go on to cut PGP's distribution another three times and I have marked the approximate dates on PGP's Premium/Discount chart below, starting in 2016:

{kind=link}

The real question however, is why did PGP attain such a high premium in the first place? Part of it was PGP's high-octane bond and E-mini equity strategy that worked for as long as the bond markets and equity markets were being fueled by the Federal Reserve's rate cuts and liquidity stimulus.

But once the Fed started looking to reverse course and start raising rates, first beginning in 2017-2018 and then combined with negative equity markets in 2015 and 2020, it became harder and harder for PGP to cover its high distribution.

The good news was that once 2022 rolled around and the Fed really started raising rates aggressively, resulting in a bear market in both stocks and bonds, PGP had already made all of its distribution cuts despite having a -27.0% NAV performance last year.

Keep in mind that PIMCO had kept PGP's distribution at its 2005 inception $0.1834/share per month for over a decade through up and down markets, including the 2008 financial crisis, and as a result, PGP developed an almost cult-like status that it could do no wrong.

But once again, it all came down to the NAV yield. PIMCO kept PGP's original $2.201/share annual distribution for far too long but in the eyes of shareholders, everything was A-OK, even as PGP's market price reached over $20 per share while its NAV eroded, resulting in the first CEF to breach the 100% market premium in 2016.

And yet, all you had to do was track PGP's NAV over this time period to know that PGP was on an unsustainable path, no matter what the market environment was. Though it took a while, and even after several articles I wrote beginning in 2015, it wouldn't be until October of 2016 before PIMCO finally cut PGP's monthly distribution from $0.1834/share to $0.1467/share per month.

But when it came time to finally cut, the first is usually not the last when you're starting from such a high NAV yield, and after a series of cuts, with the last on 6/1/2020 during the COVID-19 pandemic, PIMCO finally got PGP's distribution down to the much more manageable $0.069/share per month ( $0.828/share annualized) we see today.

So starting with the first distribution cut in October of 2016, PGP has dropped precipitously at market price and has now settled in at only a slight 1.2% premium today.

Y Charts

Clearly, this was a horrible time to be a PGP shareholder, but if you followed my advice and avoided PGP and instead swapped into the other funds I mentioned in my articles over the years, you would have been a heck of a lot better off.

I'm not going to throw out performance numbers but just realize that in the Equity CEFs: PIMCO's Sinking Ship article I wrote in early 2016 before any distribution cuts had even begun for PGP, I said:

Though I can't say when, and frankly, it should have happened a long time ago, PIMCO will need to cut PGP's distribution by up to 50% and when that happens, PGP shareholders are looking at a major haircut.

And that's exactly what has happened and then some.

But you know what? That was then and this is now, and even during the most accelerated rate rise in history last year, much worse than the 2017-2018 period, and even during a raging bear market in equities too, PIMCO did NOT have to cut PGP's distribution again.

That's what happens when you finally get your NAV yield down to a sustainable level and that is why I made PGP my Top Specialty Pick for 2023.

Why PGP Is Attractive Once Again

Though I'm sure to get the proverbial "but look at PGP's graph!" from readers, you must understand that the problems with PGP in the past were 1). Too high of a NAV yield and 2). The bond and equity markets that were not conducive to optimize PGP's income and appreciation strategy.

So let's address number 1). After four distribution cuts, PGP's NAV yield is now down to 11.4% , which is significantly more attainable than the 20%+ NAV yield PGP had before it started cutting its distribution.

Though a 11.4% NAV yield is still relatively high compared to most CEFs, you also have to take into account that PGP has a very aggressive income and appreciation strategy, so if PGP's strategy is hitting on all cylinders, that NAV yield is not a problem.

Which leads into number 2). The equity markets, after an -18.1% drop in the S&P 500 ( SPY ) last year, finally look like they are turning the corner and so far this year, PGP's NAV is up 8.4% after three months, one of the best of all CEFs I follow. Annualized, that would mean a 33.6% NAV total return performance, which is probably unrealistic but anything over its current 11.4% NAV yield would mean that PGP's NAV was growing instead of eroding.

But what will probably have the most beneficial impact on PGP, and indeed all of the PIMCO fixed-income CEFs, is that if we are near the end of the Fed's rate hike cycle and we can start to see bond and equity prices move up, while rates gradually move back down, then we are back in a market environment that dovetails nicely with PGP's strategy.

Though 2). is still an unknown, at the very least, PGP is in much better shape to weather any disappointments should the equity and bond markets not continue in their recovery. And that was shown last year when PGP's NAV was down -27.0% but saw no more cuts.

Here are PGP's current statistics compared to the same date in 2016:

| MKT Price |

| NAV Price |

| Premium |

| Annual Distribution |

| MKT Yield |

| NAV Yield |

| PGP on 3/31/2023 |

| $7.41 |

| $7.23 |

| 2.5% |

| $0.828/share |

| 11.2% |

| 11.4% |

| PGP on 3/31/2016 |

| $19.00 |

| $10.00 |

| 90.0% |

| $2.201/share |

| 11.1% |

| 22.0% |

Looking at the table above, does anybody else find it amazing that a current buyer of PGP could get a higher 11.2% market yield today, even after four distribution cuts, than seven years ago?

Yes, good things come to those who wait. At least for those who wait for NAV yields to come down.

The Greatest Swap In CEF History?

I'm sure it's not lost on readers that the Gabelli Utility fund, $7.15 current market price , is now the second CEF in modern times (there may have been others since CEFs have been around for a long time) to attain a 100%+ market price premium.

Though this article is more about the opportunity in PGP, which is a much different fund than GUT, let's not overlook the risks that ANY fund trading at a premium possesses, let alone a 100% market price premium.

Just remember, your financial interest in a CEF is not given by the market price if anything goes wrong with the fund or the markets. The market price is simply what another investor is willing to pay for your fund and for most funds (ETFs and mutual funds), that market price also represents the current value of the fund.

But for CEFs, your financial interest is represented by the NAV (assuming all holdings could be liquidated at near current market prices). Now that can mean opportunity, like in the fall of 2008, when quite a number of CEFs traded down to -30% discounts or more for short periods. In that situation, you would love to see your CEF liquidated or merged as that would then unlock the NAV value.

But for CEFs that trade at a premium, it works just the opposite way. So when you see PGP trading at a slight 1.2% premium now over its $7.28 NAV, there's a level of safety there no matter what happens. On the other hand, GUT trading at a 104.6% premium over its $3.50 NAV adds a level of risk that goes beyond just a deteriorating NAV.

GUT shareholders may not have to worry about a distribution cut until the next three-month declaration in mid-May and we may even see another Rights Offering before then, but make no mistake, time is not on GUT's side.

Now won't a bull market in equities and bonds also help GUT? Well, sure, but keep in mind, PGP hit its 100%+ premium valuation when the S&P 500 ( SPY ) was at an all-time high of $218 during the summer of 2016 and SPY is now at $411 . So don't think an 88% rise in SPY over the last 7-years could overcome PGP's high premium and high NAV yield.

GUT may not have as aggressive a portfolio as PGP and may not have a 20%+ NAV yield (just yet), but when I look at the similarities between these two funds overlapped seven years, the trajectories look eerily similar. History may not repeat itself, but it often rhymes, and I believe it's only a matter of time before GAMCO is forced to cut GUT's distribution too.

And when that happens, the greatest CEF swap in history will be complete.

For further details see:

Potentially The Greatest Swap Idea In CEF History: Sell GUT, Buy PGP