PCH - PotlatchDeltic: 3 Reasons To Get A Little More Optimistic On This REIT

2023-09-25 10:00:00 ET

Summary

- PCH stock has performed poorly, delivering a worse return than the Vanguard Real Estate ETF.

- Q2-2023 results show a decline in adjusted EBITDA, with operating income down by more than 90% without insurance claims.

- We tell you why there are some reasons to be optimistic and suggest an options trade for those bullish on the stock.

We were not too optimistic on the prospects for PotlatchDeltic Corporation ( PCH ) on our last coverage. We looked at the funds from operations ((FFO)) multiples and concluded that this was just too broken from a cash flow perspective to remotely consider buying.

The NAV estimate might provide comfort, but as we examine longer-term charts, we note that PCH has many times traded as low as 40% below consensus NAV estimates. That would bring us to around $36 in this case. PCH gets a 7 on our potential pain scale rating.

Author's Pain Scale Rating From Previous Article

{kind=link}

Source: PotlatchDeltic: Cash Flow Dries Up As Lumber Prices Tank

The stock has obliged our view and delivered a really strong negative return. This return was far worse than if you had simply bought and held the Vanguard Real Estate ETF ( VNQ ) during this timeframe.

We look at the recent results and macro data to update our view.

Q2-2023

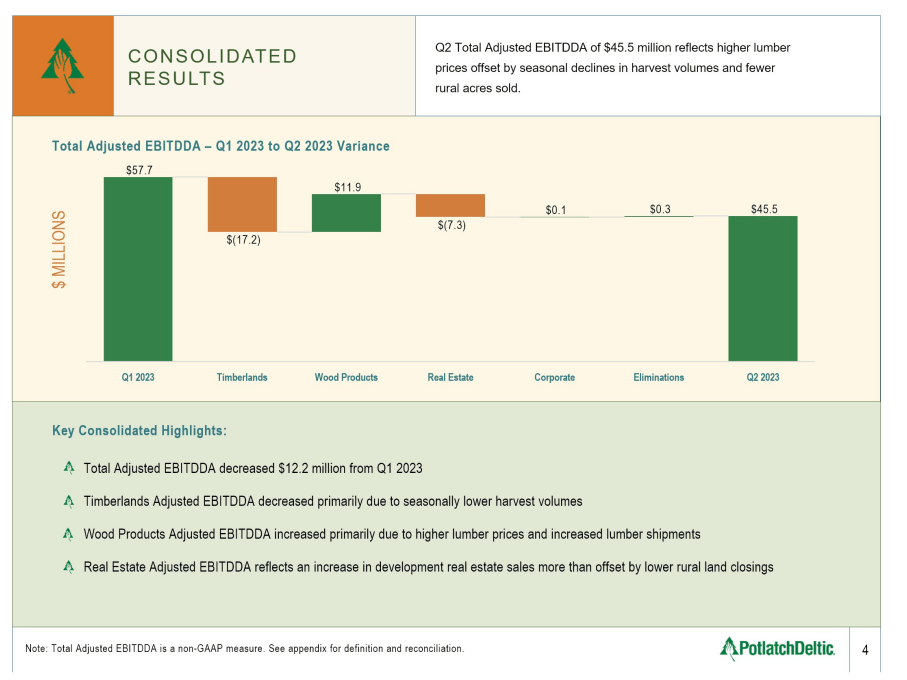

PCH saw a decline in adjusted EBITDA in Q2-2023, relative to Q1-2023. Timberlands and real estate segments were both detractors, while wood products improved sequentially.

{kind=link}

From a big-picture perspective, PCH is now in a different Universe relative to 2022. You can see below that Q1-2022 and Q2-2022 produced a combined $370 million in operating income.

{kind=link}

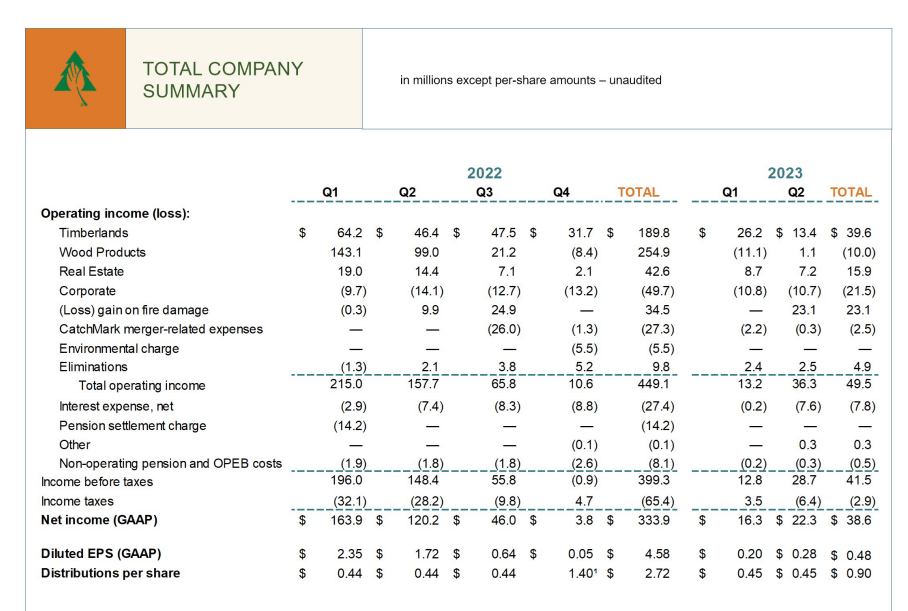

The first two quarters of this year were at less than $50 million. Even that level of operating income was helped by the "gain on fire damage" category of $23 million.

We received $23 million of insurance recoveries in the second quarter for property damage and business interruption related to the Ola sawmill fire. Since our claim was filed in 2021, we have received $73 million of insurance recoveries and expect to finalize our claim before the end of the year.

Source: Q2-2023 Transcript

In other words, outside of this insurance claim from 2021, operating income would have been down by more than 90%.

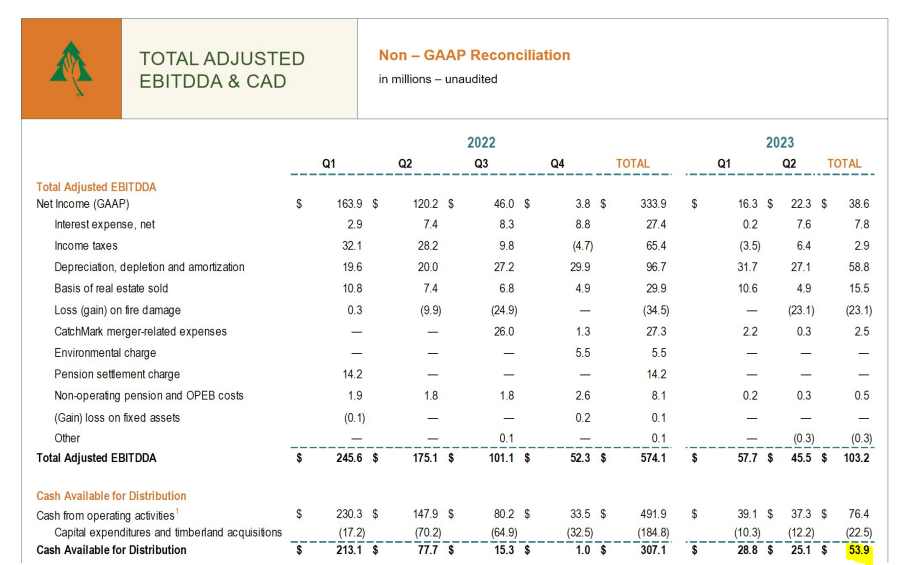

Cash available for distribution, or CAD, was at $53.9 million for the first half of the year.

{kind=link}

With almost 80 million shares/units outstanding we would require about $72 million just to cover the distribution.

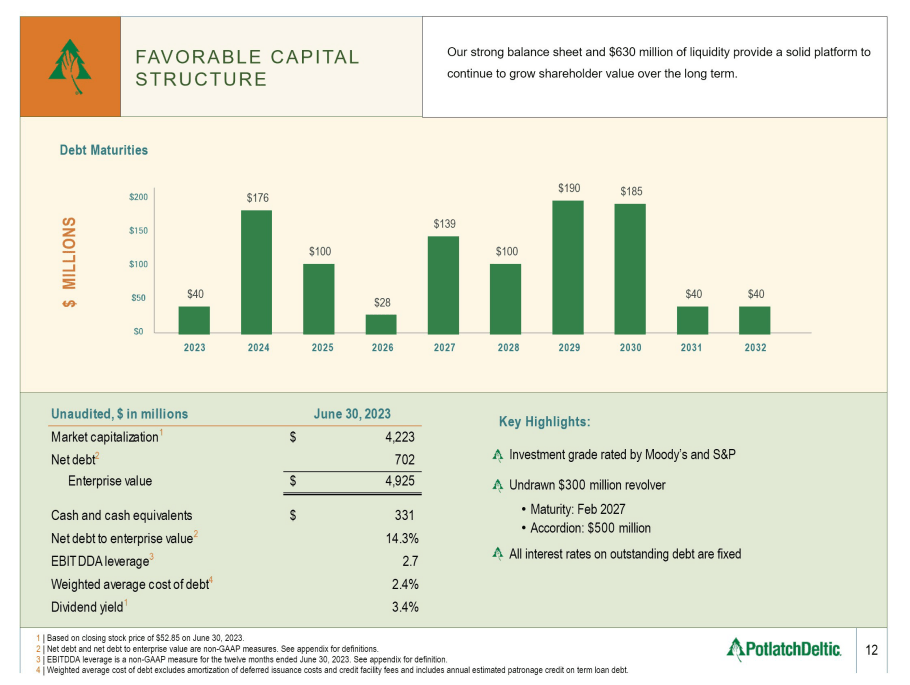

So we are running short, but fortunately, PCH had deleveraged during the boom times. Current debt metrics still look very good for a real estate firm, with net debt to EBITDA at 2.7X. All debt is fixed rate as well, so PCH has not rolled the dice on ZIRP (zero interest rate policy) making a comeback. It also has a large cash hoard, and distribution over and above its cash flow won't be biting the firm any time soon.

{kind=link}

The counterpoint here from the bear cave is that the EBITDA leverage is based on the trailing 12-month metrics. In other words, it is counting quarters that were quite good and will be rolling off soon. If you annualized Q2-2023 EBITDA, leverage jumps to almost 4.0X, from 2.7X.

Outlook

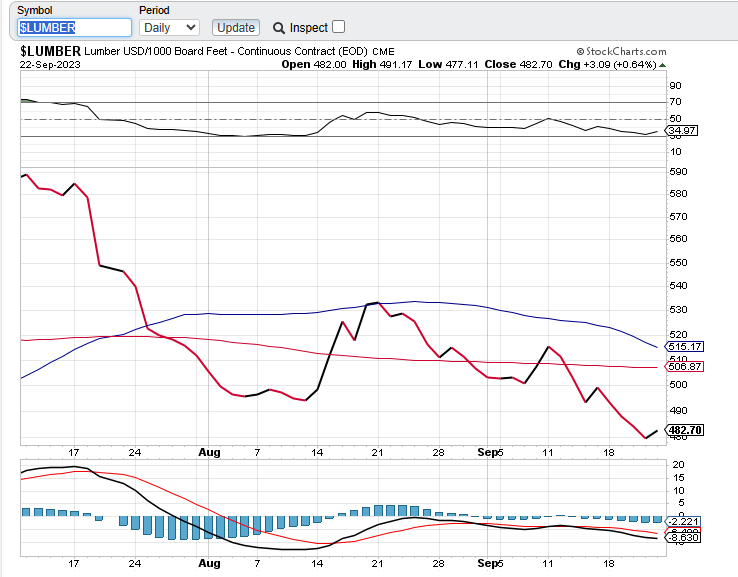

While PCH has fallen and indeed become cheaper, Lumber futures have also declined, a lot since then. In fact, Lumber continuous contract number has fallen more than PCH stock price since that article was released.

{kind=link}

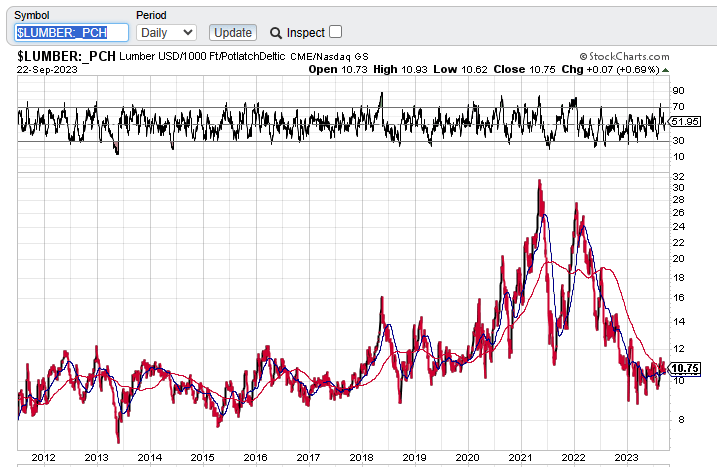

When you plot a ratio of Lumber futures to PCH stock price, you can see that it is near the bottom of its recent range 5-year range and close to the middle of 2011-2019 time frame range.

{kind=link}

So relative to Lumber, it is hard to argue that PCH is cheap. On the earnings front, you have to assume a very strong bounce in commodity prices and then go out to 2025 to get to a 22X multiple.

{kind=link}

So none of these metrics scream cheap and on most numbers the stock looks incredibly expensive for a 5.5% risk-free rate environment. Multifamily housing starts were something that had held together the construction boom even as interest rates rose. Those starts are now faltering.

Calculated Risk

It is hard to envision Lumber making a big recovery under those circumstances. But there are three big reasons here to be a little more optimistic than what we were the last time around.

1) The first of these is that the commercial traders who tend to be the "smart money" have built up a decent long position on Lumber.

CFTC Reports

This is not a sufficient condition for a reversal but increases the odds of a bounce in Lumber prices.

2) We are entering the seasonally favorable period for Lumber and that adds weight to point 1.

Equity Clock

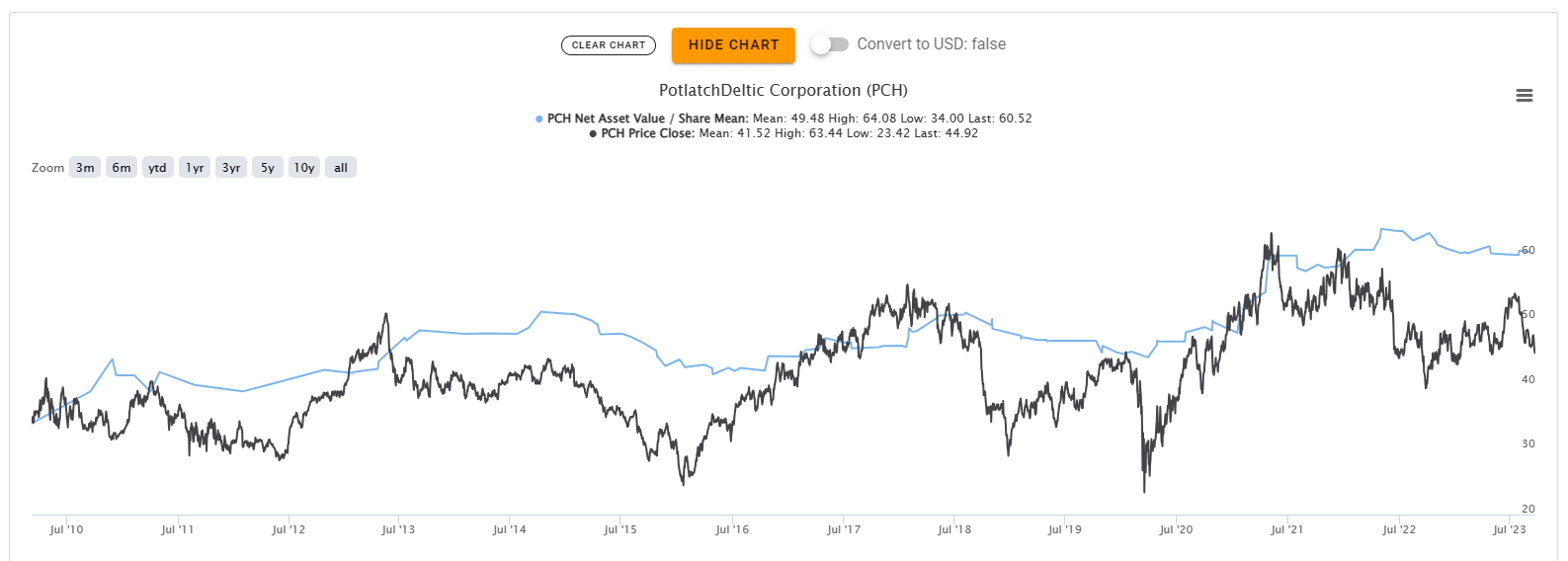

3) PCH is now trading at a solid discount to consensus NAV.

{kind=link}

This improves the odds of you making a positive return from here, although we will note that PCH has traded far cheaper relative to NAV, even in the ZIRP era.

Verdict

PCH now enters our watch list for a potential entry point. The stock was unbelievably expensive the last time around but has become more reasonably priced. While the cash flow remains weak, we see the underlying timberlands as valuable inflation proxies that should appreciate in a chronic inflation environment. As such we are giving PCH an upgrade on our "pain scale" to 5 (from 7 earlier).

{kind=link}

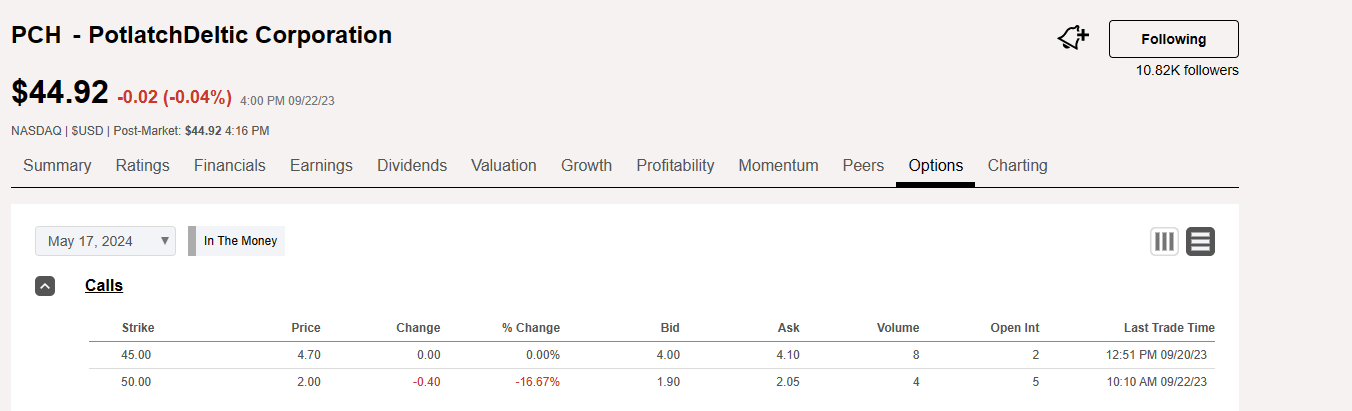

We are not bullish yet and would suggest that investors who are bullish use covered calls to generate superior risk-adjusted returns. The May 2024 covered calls at the $45 strike would be one choice to consider.

{kind=link}

These would provide an 18.65% annualized return if PCH closes above $45 at expiration and create an adjusted entry point of $40.92 if it does not.

Author's App

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

PotlatchDeltic: 3 Reasons To Get A Little More Optimistic On This REIT