CA - Praetorian Capital Fund Q1 2023 Investor Letter

2023-06-29 07:15:00 ET

Summary

- Praetorian Capital is a hedge fund managed by Harris “Kuppy” Kupperman dedicated to seeking non-correlated, asymmetric returns in a benchmarked world.

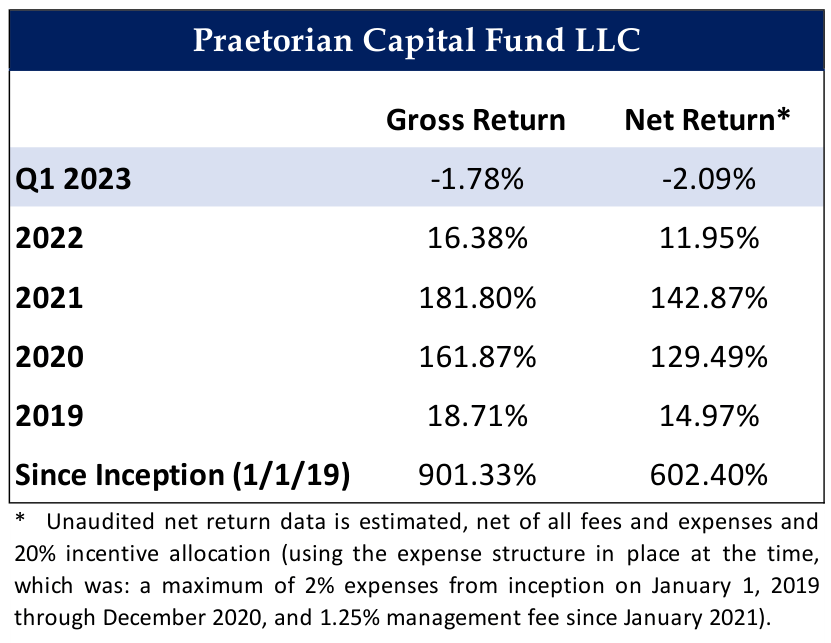

- Praetorian Capital Fund LLC depreciated by -2.09% in the first quarter of 2023.

- I believe that the imminent arrival of an energy crisis, precipitated by dramatic increases in the price of oil, will supersede whatever impact rates may have on the economy.

- I believe that 2023 will be a year that tests many investors as tail events become commonplace and formerly reliable bastions of stability are forever shattered.

To the Investors of Praetorian Capital Fund,

During the first quarter of 2023, Praetorian Capital Fund LLC (the “Fund”) depreciated by -2.09%, net of fees. Given the Fund’s concentrated portfolio structure and focus on asymmetric opportunities, I anticipate that the Fund will be rather volatile from quarter to quarter. During the first quarter, many of our core portfolio positions treaded water, while the Event-Driven book produced a small negative return.

{kind=link}

While the core portfolio was rather uneventful, I want to remind you that the Event-Driven book will occasionally experience losses. Fortunately, the losses this quarter were all smallish and in-line with my expectation for maximum potential loss on any one situation. Unfortunately, these losses were repetitive with very few gains to offset them. This will happen from time to time and is perfectly within my range of expectations. Remember, in the Event-Driven book, we’re playing probabilities and just like a well-managed insurance company, occasionally we get hit by a hurricane or two. The important fact is that this quarter’s loss was negligible in relation to the many quarters before it that returned multiples of this number.

I would like to note that in my experience, periods of low or negative returns in the Event-Driven book, are often followed by a bonanza of opportunities and dramatically heightened profitability in the Event-Driven book. For instance, following a rather miserable showing for the Event-Driven book in 2019, the strategy had astounding results in 2020 and 2021 before returns faded a bit in 2022 as volatility diminished. I remain hopeful that before too long, we’ll experience another “golden era” of Event-Driven profitability, just like the prior one.

Market Views

Many market pundits are currently fixated on interest rates and their expectation that the fastest rate cycle in recent memory will succeed in creating a recession. While I’m receptive to such a view, I don’t think that rates will be the kill-shot. Rather, I believe that the imminent arrival of an energy crisis, precipitated by dramatic increases in the price of oil, will supersede whatever impact rates may have on the economy.

Taking a step back, I’ve been speaking about oil for a while now. At first, the recovery from negative prices in 2020, made me look astute as a prognosticator. However, since peaking out following the Russian invasion of Ukraine, oil prices have drifted lower, losing almost half of their peak price. As a result, it would be disingenuous for me to tell you how oil is about to rapidly increase in price, if I didn’t first explain why oil prices took a breather, especially over the past 9 months.

In the end, it all comes down to math. Unfortunately, given the nature of oil, precise data is impossible to come by. Instead, I’m forced to use some back-of-the-envelope internal estimates that are likely to be directionally correct, if empirically incorrect. With that in mind, I believe that oil investors have now suffered through the following since the late summer of 2022:

- China locking down over COVID for approximately 200 days with a demand loss of 2.5 million barrels per day (bbl/d) or 500 million barrels (bbl) throughout Asia

- Global Strategic Petroleum Reserve releases in excess of 300 million bbl

- Russia dumping approximately 150 million bbl of crude and refined products before sanctions took hold

- A warm winter in Europe and North America which reduced heating oil and propane demand by approximately 100 million bbl

In total, we’re looking at a swing of approximately 1.05 billion barrels over a period of roughly 200 days, or 5.25 million bbl/d. With that in mind, the surprise shouldn’t be that oil prices declined under the weight of this massive swing. Rather, the surprise should be that global commercial inventories barely increased. Where did those barrels go? They got consumed. What’s more, they got consumed during a period where increasing interest rates incentivized many consumers to run down their existing inventory, inventory that is not tracked by the various acronym agencies tasked with tracking inventory, adding a further headwind to global imbalances.

Now, we find ourselves at a moment in time when the first three of the headwinds noted above are reversing, and no one can predict the weather. Meanwhile, global demand grows every year. If global commercial inventories could barely increase with these extreme factors in play, what happens now that they’ve reversed? What happens if there’s an accident on the supply side for a change?

In my year-end letter to you, I estimated that the year-end 2023 deficit would be between 4 and 6.5 million bbl/d. I remain convinced that this is a great baseline to use (adjusted for a smaller decline in Russian production offset by an increase in global consumption as the “Work from Home” trends reverse) and recent OPEC moves to reduce production by 1.15 million bbl/d will only accentuate the deficits.

Now, think about how ludicrous it sounds to say that we’ll draw inventory at 5.15 and 7.65 million bbl/d to account for the recent OPEC cuts? Of course, we will not draw at anything approaching that rate, but that’s only because oil prices will have to rise to a level that destroys roughly that much demand, balancing the market. Hence why I’m not worried about interest rates. Instead, I’m trying to envision the magnitude of the energy crisis necessary to destroy somewhere between 5% and 7% of global demand. For a point of reference, the GFC, which was the largest economic crisis since the Great Depression, destroyed less than 2% of global energy demand. Could a crisis, a few times worse be necessary and imminent?

Of course, in a highly dynamic market like oil, there are often countervailing forces at play—some positive and some negative for balances. Who could have predicted that a warm winter would save Europe from having to burn copious quantities of oil for power generation? Or that Libya would enter a rare period of relative political stability? These were both impossible to predict, yet positive for overall balances. Where were the inevitable and offsetting negative events?

In summary, it’s odd for a period of time to witness so many events that swing balances in one direction, without other offsetting adjustments in the other direction. I think the past 200 or so days were an unusual outlier, that is unlikely to repeat, and without the events noted above, the energy crisis would have already arrived. At the same time, I’m finely attuned to the fact that many of these events are out of my control, and I have positioned the portfolio so that if the thesis again gets postponed or adjusted in magnitude, we should not suffer too gravely. Ideally, we can profit handsomely, even if the events play out differently than I anticipate.

The fact that some prominent and successful energy investors use similar math, means that I am by no means an outlier in my thinking about oil balances. What makes me an outlier, is that I’m gravely attuned to what this means for other risk assets—while most market participants, having never contemplated an energy crisis, seem blissfully unaware of what is coming their way.

While all of this is happening on the energy front, we’re simultaneously witnessing an inflationary crisis, a slow-burning banking crisis, a pending commercial real estate crisis, multiple geopolitical crises, and likely a fiscal crisis intertwined with a monetary crisis. All of these will be accentuated by the coming energy crisis, especially as the Fed is increasingly powerless to react, as its tools are pressed to the limit for fear of breaking something else.

I believe that 2023 will be a year that tests many investors as tail events become commonplace and formerly reliable bastions of stability are forever shattered. I believe that many of the economic systems that we have taken for granted for most of our lives are about to be upended. Longer-term, I believe that this is healthy as the whole system desperately needs a reset. However, as this unfolds it will be downright terrifying.

To summarize, I’m unusually bearish on things and anticipate a period of chaos. However, unlike many doomsday prophets in the markets, I want to be clear that I will keep an open mind about the trajectory of things. For instance, I can very easily envision a world where the stock market crashes higher. I can imagine a world with a banking crisis along with raging inflation (who says banking crises are deflationary?). I can see a world where the Fed loses control of interest rates, and the fiscal side simply loses the narrative. Alliances can suddenly shift, and trade-flows become upended. Meanwhile, small regional conflicts can suddenly engulf the Great Powers. I believe that all kinds of demons that have festered are about to explode into the open, upon people who are unusually unprepared.

Anticipating chaos, I’ve kept our exposure at reduced levels for over a year. I had wanted to unleash our capital reserves and max out our positions on a market bottom, and I genuinely thought that I’d be deploying capital into GDP sensitive companies, as the Fed began to cut rates. Instead, I’m increasingly of the view that macro events may trump fundamentals. Instead, I am considering precious metals, which may be entering a new bull market, possibly even THE bull market that comes when the edifices around us collapse and the authorities lose control.

The Freedom to Lose Money

I’m sure that I’m going to regret this sub-header, but I’m going with it out of my belief in transparency.

You see, in the volatile world that we’re about to enter, wild swings in our P&L are going to be inevitable. Knowing the financial landscape, I also know that these swings will wreak havoc on other investors, especially given their copious use of leverage and desire to achieve a reduced quantum of volatility for their clients, by constantly adding and reducing exposure. These investors will inevitably exit at extremes and accentuate moves, in both directions. Short term, this volatility will be terrifying, but also an amazing source of opportunity for us. This is because I simply do not care about our short-term P&L. As far as I’m concerned, I have the freedom to lose money, sometimes surprisingly large sums of money as various assets swing around wildly. Otherwise, I’d be like every other investor, forced to de-risk and de-gross at extremes. In fact, I’d say that my willingness and ability to just ignore the volatility, is one of the Fund’s greatest competitive advantages.

As we enter an increasingly volatile world, it’s worth reminding you that my expectation is that roughly every 18 to 24 months, we’ll experience a 35% pullback in our returns. Of course, depending on the timing of the extremes of the move, you may only see some small portion of such a move, as much of it may be truncated intra-month. However, there will come times when the extremes are vividly portrayed on your statements. I want to stress again that this is a feature and not a flaw in my style.

There will also be times when temporary losses become permanent and realized. This should be self evident to all investors. While we could try and hide from this fact or even try and mitigate it, my approach is to accept it as part of the price we pay to target outperformance. Accepting this as simply part of the game, is tantamount to gaining an edge amongst those who think they can side-step such losses and volatility. Perpetually acting fearful seems foolish.

I believe the only way that you can reduce volatility, is to reduce the upside and that seems silly to me. The Fund is focused on outperformance over rolling three-year intervals. Anything shorter is simply noise to me.

Position Review (top 5 position weightings at quarter end from largest to smallest)

Uranium Basket (entities holding physical uranium)

It may take some time still, but I believe that society will eventually settle on nuclear power as a compromise solution for baseload power generation. This will come at a time when there is a deficit of uranium production, compared with growing demand. As aboveground stocks are consumed, uranium prices should appreciate towards the marginal cost of production. Additionally, there is currently an entity named Sprott Physical Uranium Trust ( SRUUF ) that is aggressively issuing shares through an At-The-Market offering, or ATM, in order to purchase uranium (we are long this entity). I believe that these uranium purchases will accelerate the price realization function by sequestering much of the available above-ground stockpile at a time when utilities have run down their inventories and need substantial purchases to re-stock. The combination of these factors ought to lead to a dramatic increase in the price of uranium as it will take multiple years for sufficient incremental supply to come online—even if the restart decision were made today.

Ironically, I believe uranium will be a prime beneficiary of sanctions on Russia as Russia is one of the world’s largest enrichers of uranium. I believe that as the West is forced to enrich more of the uranium that ultimately goes into reactors, underfeeding of tails will flip to an overfeeding of tails. In my opinion, the net effect could be anywhere between a 10% and 30% swing in the global supply and demand balance of uranium—which may dramatically accelerate the timing of my thesis while increasing the ultimate magnitude of the upward swing in uranium prices.

Oil Futures, Futures, ETFs, ETF Options and Call Spreads on Futures

I believe that years of reduced capital expenditures, along with ESG restricting capital access, combined with Western governments that are openly hostile to fossil fuels, have created an environment for dramatically higher oil prices. While we could purchase oil producers, and we are long shares of Journey Energy ( JRNGF ), I feel it is far more conservative to simply own the physical commodity itself.

I believe that this leveraged play on oil gives us the most upside to oil and ultimately inflation, while exposing us to reduced risk when compared to producers.

Energy Services Basket (Positions Not Currently Disclosed)

In 2020 when oil traded below zero, drilling activity ground to a halt and many energy service providers declared bankruptcy. Many of these businesses had teetered on the verge of bankruptcy for years due to reduced demand and over-leveraged balance sheets. The bankruptcies led to consolidation and reduced future industry capacity, removing future competition in the recovery.

With oil prices now recovering, I believe that demand for drilling and other services will increase from subdued levels. While producers have been slow to increase spending on exploration despite recoveries in energy prices, I believe that this only extends the timing on the thesis. In the end, the only way to reduce future energy prices is to see a dramatic increase in global oilfield services spending. Any postponement of this spending only leads to higher prices and more wealth transfer from the global economy to the oil producers, which will likely end up resulting in an increase in spending on exploration and production.

We purchased many of these positions at fractions of the equipment’s replacement cost, despite restored balance sheets and positive operating cash flow. As spending in the sector recovers, I believe that the potential for cash flow will become more apparent and this equipment will trade up to valuations closer to replacement cost.

St. Joe ( JOE )

JOE owns approximately 175,000 acres in the Florida Panhandle. It has been widely known that JOE traded for a tiny fraction of its liquidation value for years, but without a catalyst, it was always perceived to be “dead money.”

Over the past few years, the population of the Panhandle has hit what I believe to be a critical mass where it now has a center of gravity that is attracting people who want to live in one of the prettiest places in the country, with zero state income taxes and few of the problems of large cities.

The oddity of the current disdain for so-called “value investments” is that many of them are growing quite fast. I believe that JOE will grow revenue at 30% to 50% each year for the foreseeable future, with earnings growing at a much faster clip. Meanwhile, I believe the shares trade at a single-digit multiple on Adjusted Funds from Operations [AFFO] looking out to 2024, while substantial asset value is tossed in for free.

Besides the valuation, growth, and high Return on Invested Capital [ROIC] of the business, why else do I like JOE? For starters, land tends to appreciate rapidly during periods of high inflation—particularly an inflationary period where interest rates are likely to remain suppressed by the Federal Reserve. More importantly, I believe we are about to witness a massive population migration as people with means choose to flee big cities for somewhere peaceful.

I suspect that every convulsion of urban chaos and/or tax-the-rich scheming will launch JOE shares higher, and it will ultimately be seen as the way to “play” the stream of very wealthy refugees fleeing for somewhere better.

Legacy to Digital Transformation Securities Basket (Various Positions)

Most global print newspapers have seen their readership decline for decades as subscribers seek out alternative digital sources of information. In response to this, newspapers have tried to build up their digital presence. Historically, this digital revenue stream was always rather negligible as it was coming from a small base, especially when compared to steep declines from the print side.

Over the past few years, digital revenue growth has accelerated to the point where I expect that the newspaper companies in our basket are within a few years of their digital revenue overtaking their print revenue—assuming recent trends hold. Digital revenue represents a higher margin and higher return on capital business when compared to the capital and manpower intensity of printing and distributing physical newspapers. My belief is that, as these digital businesses come to dominate the revenue stream, newspaper company valuations will re-rate—particularly as many of them trade as if they are dying businesses, when in reality the digital side of their businesses is growing quite rapidly.

While many well-known global newspapers have successfully made this digital transition and seen earnings growth for a number of years, many smaller papers have continued to see earnings decline. I believe that these smaller papers are now on the cusp of an inflection to earnings growth as digital growth overtakes print declines. Should this happen, I anticipate it will dramatically change the narratives for these companies, along with their valuations, much like what occurred at more well-known papers. The Fund owns a global basket of these smaller newspaper companies.

Returning to the markets, during the first quarter of 2023, the Fund experienced a slightly negative return. After an extended period of reduced exposure, I’m anxious to increase exposure and target higher returns on our capital. However, I intend to remain patient when finding the right moment to max things out. I feel as though it will be obvious when the time arrives. Until then, the focus is on staying patient and trying to avoid unforced errors.

That dry powder will come in handy, as I anticipate that the coming energy crisis, wrapped in a banking crisis, engulfed in a fiscal and monetary crisis will create epic opportunities, surrounded by risk and massive volatility. I thrive in an environment like this. Following six consecutive quarters of rather mundane results, I’m excited for some volatility.

Bring it on! I’m ready!!

Sincerely,

Harris Kupperman

Appendix

Disclaimer

This document is being provided to you on a confidential basis. Accordingly, this document may not be reproduced in whole or part, and may not be delivered to any person without the consent of Praetorian PR LLC (“PPR”).

Nothing set forth herein shall constitute an offer to sell any securities or constitute a solicitation of an offer to purchase any securities. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents for Praetorian Capital Fund LLC (the “Master Fund”) or Praetorian Capital Offshore Ltd. (collectively, the “Funds” or each a “Fund”), managed by PPR, which include, among others, a confidential offering memorandum, operating agreement and subscription agreement, as applicable. Such formal offering documents contain additional information not set forth herein, including information regarding certain risks of investing in a Fund, which are material to any decision to invest in a Fund.

No information in this document is warranted by PPR or its affiliates or subsidiaries as to completeness or accuracy, express or implied, and is subject to change without notice. No party has an obligation to update any of the statements, including forward-looking statements, in this document. This document should be considered current only as of the date of publication without regard to the date on which you may receive or access the information.

This document may contain opinions, estimates, and forward-looking statements, including observations about markets, industries, and regulatory trends as of the original date of this document which constitute opinions of PPR. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Actual results could differ materially from those in the forward-looking statements due to implementation lag, other timing factors, portfolio management decision-making, economic or market conditions or other unanticipated factors, including those beyond PPR’s control. Statements made herein that are not attributed to a third-party source reflect the views and opinions of PPR. Opinions, estimates, and forward-looking statements in this document constitute PPR’s judgment. PPR maintains the right to delete or modify information without prior notice. Investors are cautioned not to place undue reliance on such statements.

Certain information contained herein has been obtained from third-party sources. Although PPR believes the information from such sources to be reliable, PPR makes no representation as to its accuracy or completeness.

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Targeted returns reflect subjective determinations by PPR based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Unaudited net return data for the Fund is estimated, net of all fees and expenses (using the expense structure in place at the time, which was: a maximum of 2% expenses from inception on January 1, 2019 through December 31, 2020, and 1.25% management fee since January 1, 2021). The net return presented is also net of Incentive allocation of 20% which is subject to the high-water-mark provision, is accrued monthly, and crystallized yearly.

The past performance of a Fund, PCM, PPR, its principals, members, or employees is not indicative of future returns. The performance reflected herein and the performance for any given investor may differ due to various factors including, without limitation, the timing of subscriptions and withdrawals, applicable management fees and incentive allocations, and the investor’s ability to participate in new issues.

There is no guarantee that PPR will be successful in achieving the Funds’ investment objectives. An investment in a Fund contains risks, including the risk of complete loss.

The investments discussed herein are not meant to be indicative or reflective of the portfolio of the Master Fund.

Rather, such examples are meant to exemplify PPR’s analysis for the Master Fund and the execution of the Master Fund’s investment strategy. While these examples may reflect successful trading, not all trades are successful and profitable. As such, the examples contained herein should not be viewed as representative of all trades made by PPR.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Praetorian Capital Fund Q1 2023 Investor Letter