COM - Precision Drilling: Put A Driller In Your Stocking

2023-12-22 17:36:27 ET

Summary

- Precision Drilling Corporation is being undervalued in the OFS market despite projected growth in their Canadian client base for 2024.

- Analysts rate PDS as a buy with price targets ranging from $83 to $107, implying potential for a 2-bagger from current prices.

- PDS is the leading drilling contractor in Canada and expects a strong start to 2024 with customer demand exceeding previous levels.

- We rate PDS as a Strong Buy.

Introduction

I don't often stop the presses, pull the fire alarm, break into regular programming, pull the emergency stop on the train… and demand the attention of the members of my Investing Group. I did the other day when I saw the decline in Precision Drilling Corporation ( PDS ). This stock has been irrationally dragged down along with the rest of the OFS market. Why do I say irrationally? Well, when their client base in Canada is projecting growth for 2024, off an average free cash yield of nearly 15% at $70 WTI, the sell-down in PDS makes no sense.

{kind=link}

Most Canadian operators are still comfortably in the black at $70 WTI, thanks to low debt, share count reduction, and of course the narrowing WCS discount. That is PDS' core market and suggests that the current sell-off represents an asymmetric investing opportunity.

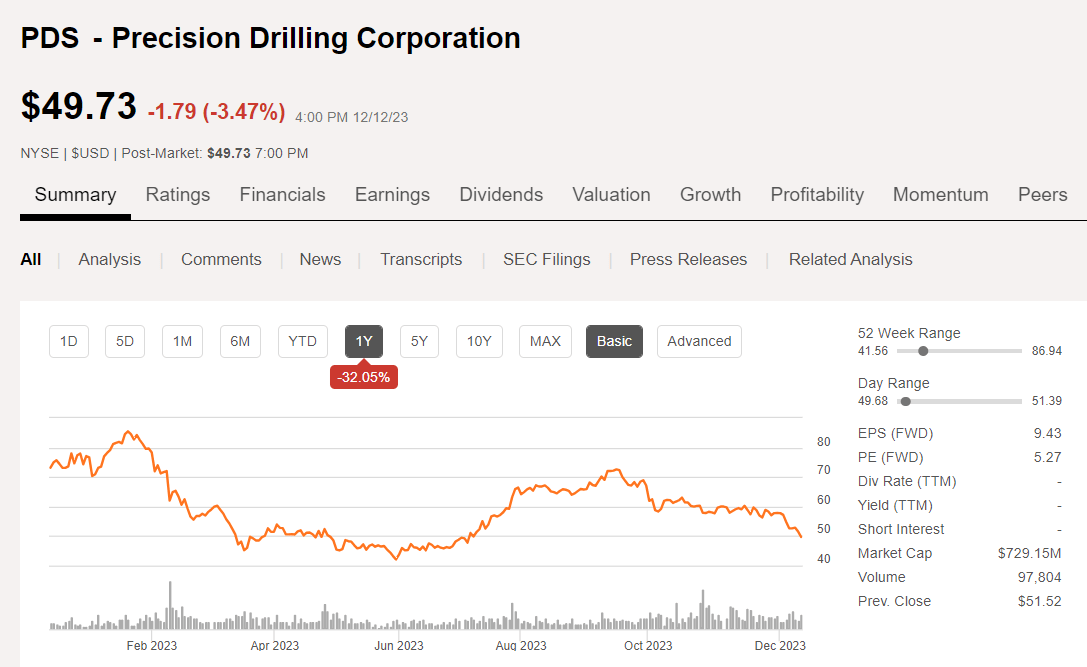

Analysts are bullish on the company, with 11 out of 11 rating it as a buy. Price targets range from a low of $83 to a high of $107. The median is $96, implying the seagulls are pretty optimistic as a cohort. PDS had been trading in a bearish Descending Channel Pattern and was well below its 200-day SMA, when I made this initial call.

It was also nearing mid-year resistance at $45, when WTI prices were also in the upper $60s, when investors came to their senses and started bidding up shares of the company. We think there is more to come, and wanted to share this take with the larger Seeking Alpha community. With the median price forecast of $96 per share, we are looking at the possibility of a 2-bagger from current prices, with most of this coming over the next few months.

Let's talk about the negative sentiment in the oil market

The narrative is that shale production has been "surging" and the OPEC+ cuts are proving ineffective in supporting oil prices (CL1:COM). At some point the Saudis, who have taken the brunt of cuts from their side of the supply equation, may become frustrated and take a page out of their 2015 playbook and flood the market. Hence, the big trading firms who control the paper market for WTI and Brent have programmed their algos to sell relentlessly, driving down prices. A sort of self-fulfilling prophecy. And, one that bears little relevance to the physical market for crude, as Eric Nuttall notes.

Eric Nuttall of Nine Point Partners posted the graph below on his X feed highlighting the outcome of this bearishness, and noting that-

Sentiment has reached its lowest point in history as measured by the net speculative length. Traders are now more bearish than they were during the Covid lockdowns that resulted in the biggest demand shock in history. The paper market is now on twelve hours long of oil demand. Commodities bottom when sentiment bottoms.

Eric Nuttall chart on paper oil market (Eric Nuttall)

Let's deal with surging production now. Using the EIA-914 as our base case, we can report that we can see through September U.S. production has risen by 1.1 mm BOPD. That's a significant increase to be sure, but there is a backstory.

If you follow the crude market and upstream E&P operators, you are aware of the intense M&A activity this year. Well over a $200 bn in transactions have been announced, and included in that data is the fact that the acquired companies have been leading the charge higher in output . Particularly on the private side, as this graph from Ted Cross VP of Novi Labs discusses.

Chart on source of shale production increase (Ted Cross Novi Labs)

To tie a bow on the surging production notion, the increase this year has been driven by private operators looking to juice output to make them more attractive in M&A scenarios. The Gulf of Mexico also saw a several hundred thousand BOPD rise this year. What is significant is that this scenario is very unlikely to be replicated in 2024.

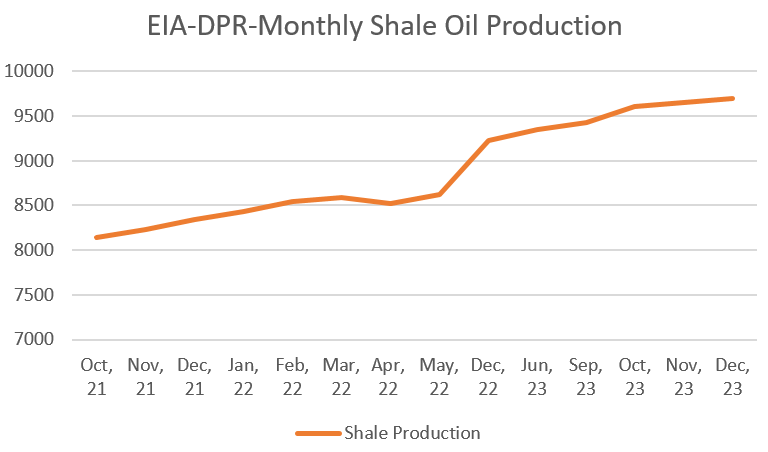

This also is driven by the fact that the decline in new drilling is getting very close to outpacing the amazing productivity gains. We see this in the flattening of the EIA DPR curve , which has gone from modest monthly increases being modeled, to small declines over the past few months. There is no "surge" in shale production.

{kind=link}

Then, let's look ahead to the supply-demand picture for 2024. There are any number of sources to which I could refer-OPEC, IEA, but the EIA STEO is one we all recognize. It shows a tight balance between consumption and production well into the next year. Updates to this report are likely to show the impact of the Fed pause and expectations for a pivot. ( I am not going to debate the "will they or won't they," as pertains to the highly anticipated FED pivot. What is becoming clear is that the soft landing is here, and the U.S. is not expected to slide into a deep recession next year. ) What this suggests is that the current curve could be conservative on the demand side, and push prices higher.

EIA STEO supply/demand chart (EIA)

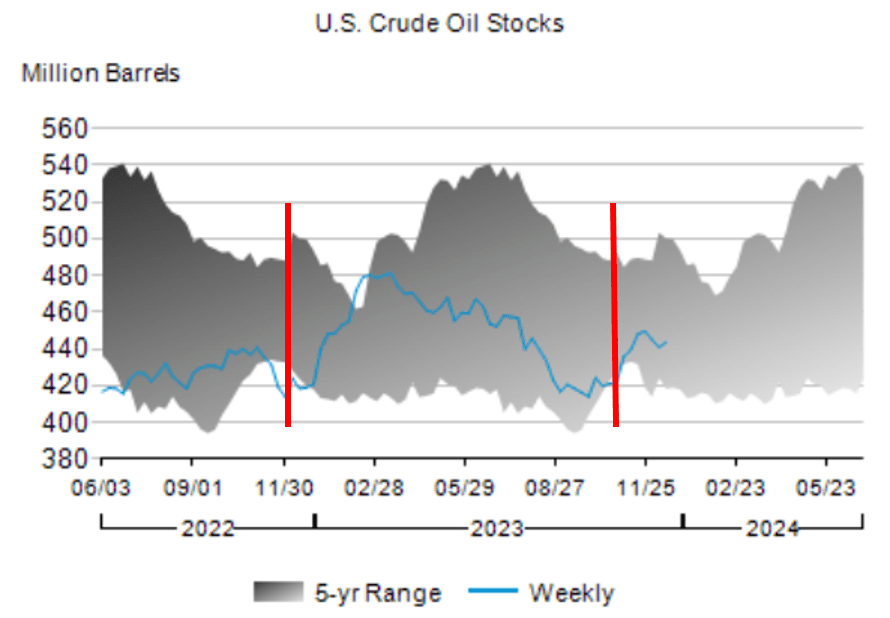

Finally, there is the inventory rise ongoing currently. This is seasonal and related to refinery turnarounds more than anything else as the EIA WPSR graph points out.

{kind=link}

Hopefully, you can now see the negative sentiment is overblown and as we turn the page on 2023, we should see stronger prices for WTI and Brent.

The thesis for Precision

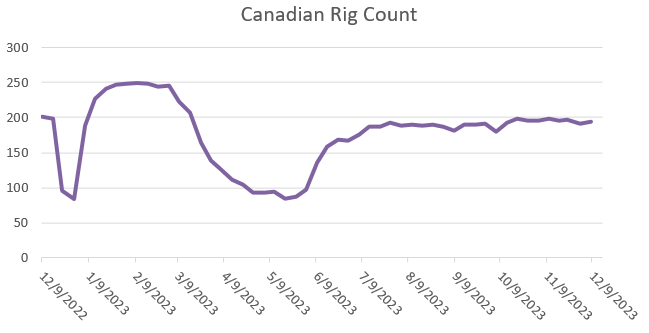

PDS is the leading drilling contractor in Canada with about 35% of the total market. It also has a respectable share in the U.S. with 44 rigs operating as of the report date. Rig activity in the Great White North is off a bit YoY, a fact attributable to crude and gas prices and impacting the totals. What's noteworthy is that after the Christmas pause, where about half the rigs just shut down, the busiest time of the year lies ahead in Q-1, 2024.

{kind=link}

PDS has also just completed the acquisition of CWC Energy Services, diversifying their offerings and adding to their rig count. Kevin Neveu, CEO was quoted as saying -

This acquisition supports our High Performance, High Value strategy as it allows us to expand our service offering in both Canada and the U.S. with high-quality rigs and field personnel. With the expected synergies and by further leveraging our scale, we believe the transaction will be accretive to earnings and provide significant cash flow to drive shareholder returns and support our debt reduction strategy. I am excited to welcome the CWC employees to the Precision team

If the graph I put together above using Baker Hughes data is remotely accurate, we are getting ready to see a surge in Canadian drilling, and that's bullish for PDS.

Kevin Neveu, CEO comments on expectations for the coming winter season-

Customer planning for winter suggests a strong and fast start to 2024, with customer demand exceeding 23 levels, and we look forward to the addition of the CWC drilling rigs improves and we expect that Precision's combined activity this winter could be up 10% to 15% from last year.

That's it essentially. The busiest time of the year is just ahead, and the company has been beaten down with rest of the OFS category. Here are links to my previous articles on this company if you would like more granular information on PDS.

A Catalyst for PDS

In addition to the strength forecast for 2024 in Canada, the company's international division appears to be primed for growth during the year. CEO Kevin Neveu comments in this regard in the Q-3 call-

Internationally, drilling activity for Precision in the quarter averaged six rigs. International average day rates were US$51,570, an increase of 3% from the prior year due to rig mix. We recently activated our fourth rig in Kuwait and expect the fifth rig will be activated in the next few weeks. We expect earnings in our international business to increase approximately 50% from 2023 to 2024.

As I have noted in past articles the MEA will be the source of substance capex expenditure - hundreds of billions of dollars, as these countries look to recharge their production over the next decade.

Q3 2023 and guidance for Q4

The company missed expectations on the top and bottom lines for Q3, with weakness in U.S. drilling noted in the call. CAD revenues of ~$426 mm were higher than those in Q2, and adjusted EBITDA of CAD $115 million was driven by drilling activity, improved pricing and strict cost control. It included a share-based compensation charge of 31 million. Without this charge, adjusted EBITDA would have been CAD $146 million, which compares to normalized EBITDA of CAD $126 million in Q3 2022, an increase of 16%

During the quarter, PDS reduced debt by CAD $26 million and has now reduced debt by CAD $126 million year-to-date. Despite incurring cash costs related to the CWC acquisition, PDS still expects to meet their annual debt reduction target of CAD $150 million pointing to robust cash flow expectations in the fourth quarter.

As of September 30, their long-term debt position , net of cash, was approximately CAD $915 million, and the total liquidity position was CAD $621 million, excluding letters of credit. Net debt to trailing 12-month EBITDA ratio was approximately 1.7X. Net debt to adjusted EBITDA ratio is expected to be below 1.5 times by year-end with net debt of approximately CAD $900 million and the run rate interest expense of approximately CAD $65 million.

The full-year 2023 capital plan has increased from CAD $195 million to CAD $215 million, largely a result of signing term contracts with upgrade capital paid back inside the term of the contract. For several of these contracts, the company received cash upfront from the customer.

Guidance

In the U.S., drilling activity for Precision averaged 41 rigs in Q3, a decrease in 10 rigs from Q2. Daily operating margins in Q3, excluding the impact of turnkey and IBC were US$11,941, a decrease of US$1,563 from Q2. For Q4, margins of are expected, excluding the impact of turnkey and IBC to be in line with Q3 margins in the US$11,500 to US$12,000 range.

In Canada, drilling activity for Precision averaged 57 rigs, a slight decrease in two rigs from Q3 2022. Daily operating margins in the quarter were CAD $13,913, an increase of CAD $1,830 from Q2 2023. For Q4, our daily operating margins are expected to average over CAD $15,000, an increase of CAD $1,000 from Q3 levels due to ancillary winter equipment and improving pricing.

Source .

Your takeaway

Analysts are expecting Precision Drilling Corporation EPS of $2.10 for Q4, an 18% bump higher from Q3. Q1, 2024 is when they really are expected to rip the cover off the ball with EPS of $3.29, an additional 37% bump from Q4, 2023.

Precision Drilling Corporation stock is trading at less than 4X forward EV/EBITDA, which is very competitive. Its 15-20% free cash yield is also compelling at current prices. But, that's not what stirs the imagination. What does is the $4.12 EPS for Q1, 2023. If you take that and add the 15% growth the company is projecting for the next quarter, you can get to $4.50-4.60 per share pretty easily. (Oil prices might moderate those expectations a bit as the analysts note, so let's not carried away).

That should certainly deliver a stock price in the upper range of analyst estimates. I am slapping a strong buy on Precision Drilling Corporation, and have entered the stock at prices slightly lower than today.

I think PDS rates a strong buy and investors with a reasonable risk tolerance should put the company on their naughty or nice list.

For further details see:

Precision Drilling: Put A Driller In Your Stocking