NBN - Primer Series: Northeast Bank - Partnering With One Of The Best Bankers In America

2023-06-15 00:32:00 ET

Summary

- Northeast Bank is a small regional bank in Maine, run by one of the best bankers in America in terms of track record.

- The analyst community is asleep at the wheel with the story of value creation over the past decade. However, NBN's recent loan purchases suggest the best is yet to come.

- NBN has identifiable advantages in its core business of buying loans at a discount in the secondary market. NBN's accordion-like balance sheet allows it to deploy capital opportunistically when needed.

- Valuation is undemanding at 1x P/BV for a bank that can deliver mid/high teens ROEs over the cycle. Excellent capital allocation by Rick and his team could make the shares a multibagger opportunity for the next decade.

This is an article part of an ongoing primer series on great and undercovered companies at attractive valuations. These pieces will provide in-depth analysis of business models, financials and valuations. All figures in US dollars, unless otherwise noted.

Introduction

Northeast Bank ( NBN ) is a small regional US bank based in Maine. The bank was founded in 1872 and until 2010 had an unremarkable history with mediocre financials. In 2010, a group of investors led by Rick Wayne acquired the bank and began a successful turnaround that has since created massive value for shareholders. Over the past decade, Rick Wayne has implemented the exact same strategy (buying loans at deep discounts in the secondary market) that he used when he ran Capital Crossing from 1988 to 2007, the year he sold the bank to Lehman Brothers for 3x tangible book value, resulting in a 23% CAGR for his investors.

However, as I will argue, the best is yet to come, as NBN is still a small bank (around $320M. in market cap) with plenty of runway for Rick to continue to allocate capital in an excellent manner. The key points of the thesis can be summarised as follows:

- In terms of track record, Rick Wayne is one of the best bankers in America. Period. He had an extraordinary run at Capital Crossing; the National Lending Division (NBN’s segment that buys secondary loans) is currently firing on all cylinders (having bought more loans in Q4 than at any time in NBN’s history); he seized the opportunity to take massive advantage of the Paycheck Protection Program ((PPP)); and, finally, he also made two (unsuccessful) bids for Silicon Valley Bank and Signature Bank (!). Rick has shown himself to be a shrewd capital allocator and not afraid to make big bets when the opportunity presents itself.

- The stock is fairly obscure, having not been covered here on Seeking Alpha since 2021, and has less than 1,000 followers (at the time of writing). Furthermore, the turmoil in the banking sector has hidden from investors the value creation that has taken place in the bank over the past three quarters.

- Although the underwriting standards and excellent corporate culture are key ingredients of the thesis, the most important (and underappreciated) part of the thesis is that, although NBN is nominally a bank, its business is more akin to a private credit fund. However, NBN’s easier access to capital, its accordion-like balance sheet and its reputation as a bank with sellers make NBN’s legal structure far superior to that of its competitors.

- NBN’s valuation is extremely cheap. At $42 per share, the company has a market cap of $320M., implying a P/BV 3Q’22 of 1.1x. Given that NBN’s return on equity (ROE) has averaged 18% from 2017 to 2022, and that its residual/economic earnings (earnings after taking into account the cost of capital) per share have been growing at a healthy clip, the level of discount is too high to ignore it. What is more, the massive loan acquisitions that have been carried out recently will bring more earnings power in short order, so earnings growth will be massively skewed upwards in the short term. In any case, a 10% discount rate and a (very modest) 2% future growth rate in residual earnings, assuming ROEs in the 14-18% range, would yield target prices of $56 and $64, respectively, implying equity returns of 13% and 16.5% in perpetuity.

NBN’s history and description of the business

Northeast Bank is a small regional US bank based in Maine. The bank was originally founded in 1872 and until 2010 had the unremarkable history of a community bank with mediocre financials.

In 2010, in the wake of the Global Financial Crisis, the bank was in a difficult spot with an uncertain future. A group of investors led by Rick Wayne acquired the bank and began a successful turnaround that has since created massive value creation for NBN shareholders.

Although not as famous as many of his larger banking peers, Rick is a banker with one of the best track records in US banking over the past three decades. He started in 1988 at Atlantic Bank & Trust Company (later renamed as Capital Crossing Bank in 1999), where he developed a strategy focused on buying discounted, performing, small-balance commercial loans, primarily from regulators who had taken over failed competitors. Today, this secondary market still exists as banks regularly dispose of unwanted or non-strategic relationship assets. On the other hand, mergers and acquisitions (a topic that has become important again) typically drive banks to sell assets that would give them more exposure than they want to any segment, geography, or collateral.

In 2007, Rick sold the bank to Lehman Brother (yes, that Lehman) for 3x tangible book value. Although it is difficult to pin down an exact figure, Rick’s tenure resulted in a CAGR for his investors of around 23% (9x invested capital). It is also worth noting that Rick bought 50% of the outstanding shares between 2000 and 2007.

After his non-compete agreement with Lehman expired, Rick acquired NBN and soon began implementing the very same strategy he had used to run Capital Crossing. NBN’s early years under Rick were difficult, as the bank was small, inefficient, saddled with capital intensive businesses (such as an insurance operation) and also with regulatory commitments that Rick had to make in order to buy the bank (such as limiting purchased loans to 40% of total loans), but these have since been modified.

As the bank has grown in size its return on equity has also improved. Other notable milestones in recent years have been: i) the Paycheck Protection Program ((PPP)), where Northeast Bank was able to originate a huge amount of loans and earn the corresponding fees (as well as capital gains when these loans were later sold), allowing the bank to earn abnormal profits in the period 2021-2022,[1] and ii) two (unsuccessful) bids for Silicon Valley Bank and Signature Bank (I am not kidding!). In any case, Rick has more than proved that he is a shrewd capital allocator, that he is comfortable making big bets when the risk/reward proposition is favourable, and that he is as hungry as ever.

Today, NBN operates three business segments: the National Lending Division, Community Banking, and Small Business Administration (SBA) lending.

- National Lending Division ((NLD)): NBN’s core activity. It purchases and originates commercial loans on a nationwide basis. NBN purchases commercial real estate loans nationally at a discount, resulting in higher yields than those earned on originated loans. NBN has mentioned in the past that the pre-COVID environment (improving credit quality and a low interest rate environment) reduced the supply of loans available for purchase, thereby tightening discounts. The recent stress in the banking sector (and consolidation among the players) has created a better environment for opportunistic purchases. In terms of the originated portfolio, these loans are mostly to non-bank lenders. Most of these loans are floating rate. From a strategic point of view, this business line is a nice complement to the purchased business, as it is quite countercyclical: when origination activity is strong in the origination business, purchasing opportunities in the secondary dry up. Also, the underwriting skills are pretty much in both segments. Finally, the origination business allows them to retain some client relationships (after all, they are a bank), so they can improve their deposit franchise. At the end of 3Q’23 (quarter ending March’23), there were $2.4bn. in the NLD, $1.5bn purchased and $995M. originated. The NLD business accounted for more than 95% of NBN’s overall loan book.

- Community Banking: community lending is not the focus of NBN’s business model. Rather, it is a way to generate deposits, although NBN also generates deposits online via ableBanking. In any case, the strength of the deposit base is not one of NBN’s advantages: the quarterly cost of deposits was 3.4% in the 3Q’23 and a large chunk of these were certificates of deposit (49%). Although this deposit structure is more costly, it is also more flexible, allowing NBN to raise funds when opportunities arise.

- Small Business Administration (SBA) loans: NBN originates SBA loans nationally, but this business has been de-emphasised over time and it will not be discussed here.

The crucial part of the thesis is to understand why NBN has been able to carve out a niche position in the NLD business, leading to a superior performance relative to its peers (both banks and non-bank financial institutions, such as private equity). There are several reasons:

- NBN underwriting strategy is simple and based on common sense. NBN looks primarily at loans that are cash-flowing and current, with no problems and a solid credit history. They stay away from loans secured on assets such as land, construction, and condo development, which in their experience are more difficult to underwrite. Because they buy performing loans with a credit history, they usually have a better sense of the quality of the underlying asset than the original underwriter.

- NBN underwriting strategy is also conservative, only underwriting loans with conservative LTVs. The weighted average LTV of NBN’s loan portfolio at the end of 3Q’23 was 47%. This underwriting discipline has enabled the bank to achieve leading historical credit performance metrics. Cumulative net charge-offs from 2012 to 2022 have been only a paltry $5.3M – yes, you read that right.

- Its small size allows NBN to focus on the (relatively) underserved part of the market, where there is less competition for small borrowers (these relationships are less valuable to the big banks). At the end of 3Q’23, NBN’s loan portfolio was $2.5bn, spread across 4,656 loans, with an average loan size of $539k. Other players, such as private equity funds, typically do not compete for small balance commercial loans and tend to pursue larger, more bulky transactions.

- Most of the banks with which NBN competes are community banks looking to acquire loans in their market; these banks tend to have specific criteria for their acquisition activity and do not pursue pools with collateral or geographic diversity.

- Corporate culture is important in any industry, but even more so in banking, which is fundamentally a human capital business. In this regard, NBN’s culture is extremely strong. In addition to Rick, Patrick Dignan, the Chief Operating Officer, has been with the bank since the acquisition. The Chief Information Officer has also been with the bank since the acquisition. Finally, the Chairman of the Board (who has been director since 2010) was previously the Chief Investment Officer of BlackRock Alternative Investors, which is very rare for such a small bank.

However, I believe NBN’ most important competitive advantage is underappreciated by the market. And that is the unconventional way in which the company is structured. Although legally a bank, it is run as a credit fund, but one with superior structural features to a traditional credit fund. First, NBN’s cost of funds is lower (although, remember, higher than that of well-established regional banks) than that of private equity funds: the latter have higher return expectations, allowing NBN to outbid them on many good performing loans. Second, for some sellers, it is important to sell the loans to a bank rather than to a fund because of reputational (and execution) risk. Finally, and most crucially, NBN access to capital is better, as they can flex up their balance sheet quite dramatically when the opportunity arises (NBN’s only constraint is equity capital). We have seen this principle in action in recent months. In just nine months, NBN has grown its loan book from $1.3bn. to $2.5bn, thanks to its access to Federal Home Loan Bank advances and CDs. Conversely, when there are no opportunities to deploy capital intelligently, NBN allows its liabilities to run off, as they don’t have to be fully invested like most funds. Finally, NBN can retain its earnings and become a stronger institution.

Quality of the loan book

The crux of the thesis, apart from Rick and its team's ability to create value in the long run, is the current characteristics of the loan book. This is particularly important as the loan book has grown massively over the last 9 months. Unbridled growth is something that is a red flag when investing in financial institutions, as it may point out deteriorating credit standards. As I am about to show now, I don't think that is the case here at all.

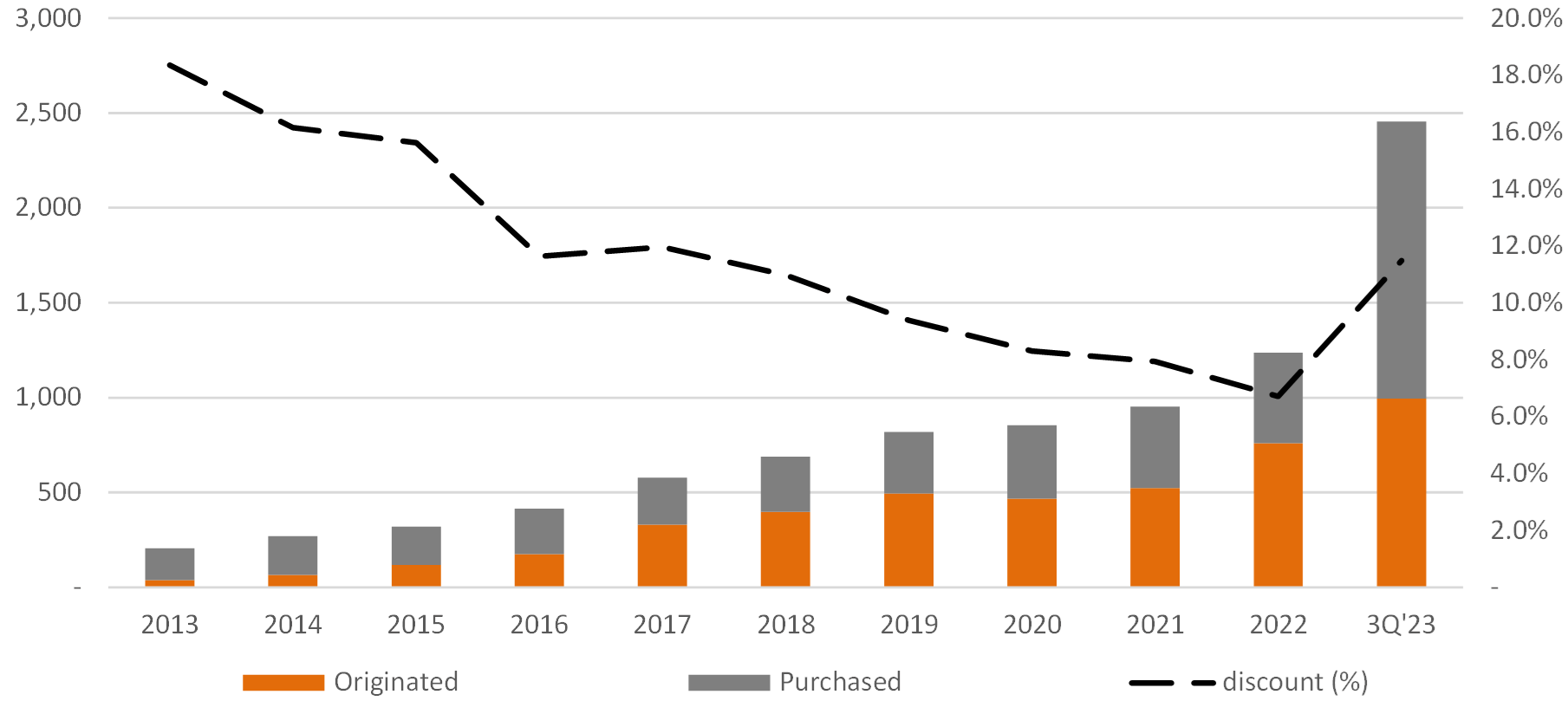

To put things in context, the following graph shows NBN’s loan book evolution:

Northeast Bank filings and own elaboration.

{kind=link}

We can see that NBN’s loan book grew gradually until this year, when the loan book exploded thanks to the purchases made in November and December of 2022. The average discount on the loan book is 11.5%, which has risen sharply after years of fewer opportunities (as discussed above). Since this is an average discount, it actually means that the discount on new loans is higher than this number: as NBN discloses in its filings, so far this year it has bought a $1.26bn. of unpaid principal balance for $1.1bn., representing a discount of 13.1%.

It is worth repeating again that Rick and his team could have easily deployed capital much earlier, thereby boosting near-term growth and profits, but at the same time compromising his underwriting standards. But they did not, waiting for more than a decade for the opportunity to present itself.

NBN has done a very good job of explaining the characteristics of its loan book in its 3Q’23 investor presentation (see here ). The loan portfolio totals $2.5bn, spread across 4,656 loans with a weighted average LTV of 47% (slide 4). Actually, the LTV of the purchased portion is slightly lower at 45%. In terms of the collateral, 20% is multifamily, 18% is lender finance, 16% is retail, 12% is office, 9% is industrial and the rest is spread across other end markets. NPLs (as a percentage of total loans) were 0.58% and the allowance for loan losses was (again) 0.58% at the end of the quarter.

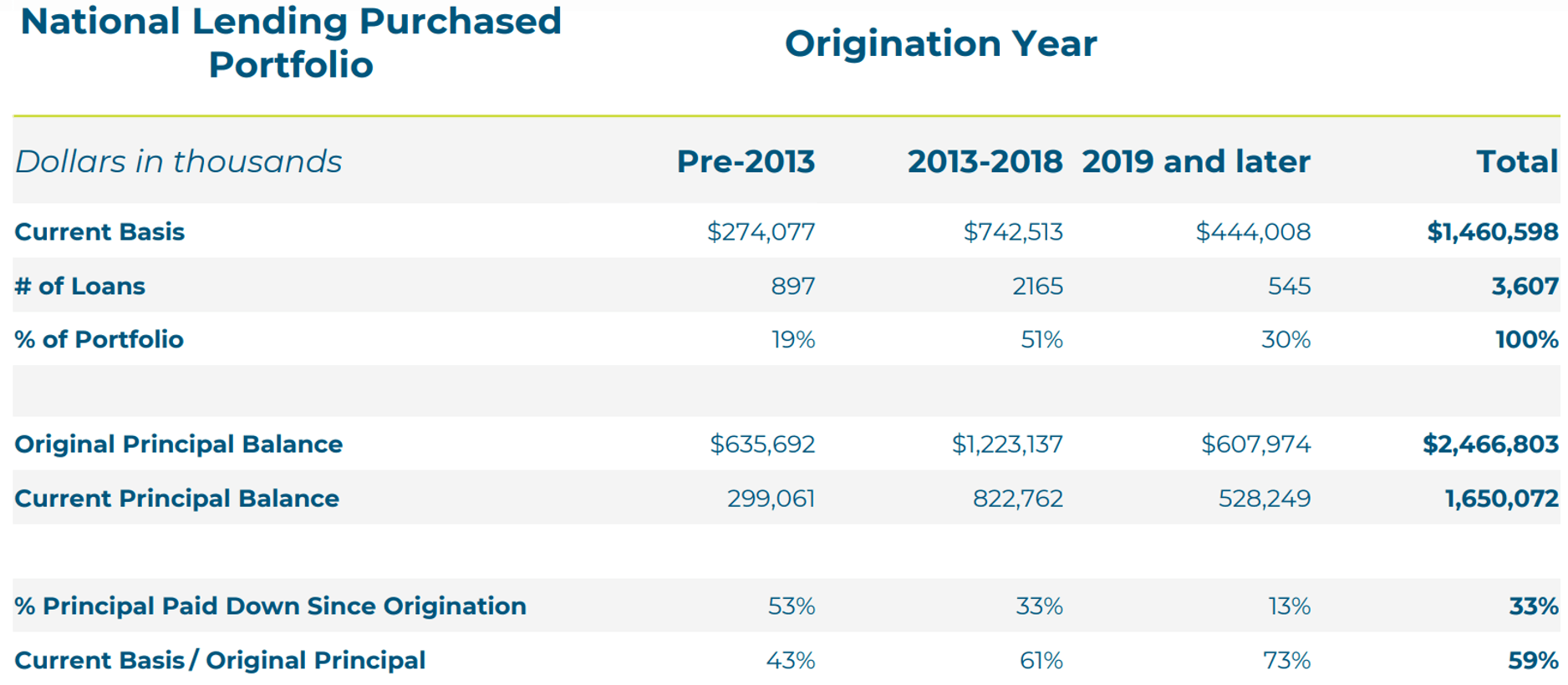

I think the more interesting part is the seasoning analysis of the portfolio (slide 13, reproduced below). The majority of the loans were originally originated prior to 2019: a total of $1.8bn of loans that now have a current principal balance of $1.1bn, suggesting a significant equity cushion and borrowers with a lot of skin in the game (borrowers who have repaid such a large amount of debt are less likely to default in the future). Looking at the 2019 vintage and beyond, while equity creation has been lower due to the short amount of time that has elapsed since then (only 13% of the loan has been repaid), the amount paid by NBN ($444M.) provides a significant margin of safety:

Northeast Bank Investor Presentation 3Q'23.

{kind=link}

To add some qualitative colour, management has mentioned that the recent CRE loan purchases were made in three tranches. First, the largest tranche (around $700M) was from a large US bank with liquidity needs, and the portfolio had LTVs of around 30%. The assets were located primarily in California, Oregon, and Washington State. The second tranche was $300M from another large bank, with LTVs of around 60%. And finally, a small $100M from a private group. In each case, the loans had no credit issues, and their discount was due to the higher interest rates.

Finally, it may be instructive to look at the earnings power brought from the newly acquired loans looking at the most recent quarter. Basic earnings per share were $1.7, which on an annualised basis would imply earnings power of $6.8 (implying a 6.2x P/E ratio). In the absence of additional credit losses, I think this is a good estimate of the bank’s current earnings power at the moment.

Valuation

Despite NBN’s track record of creating shareholder value over the past decade, the bank still trades at around 1x book value. It does not take much arithmetic to conclude that a well-capitalized bank, earning returns well above its cost of capital, with no liquidity issues, and with a strong corporate culture should be trading well above book. But by how much?

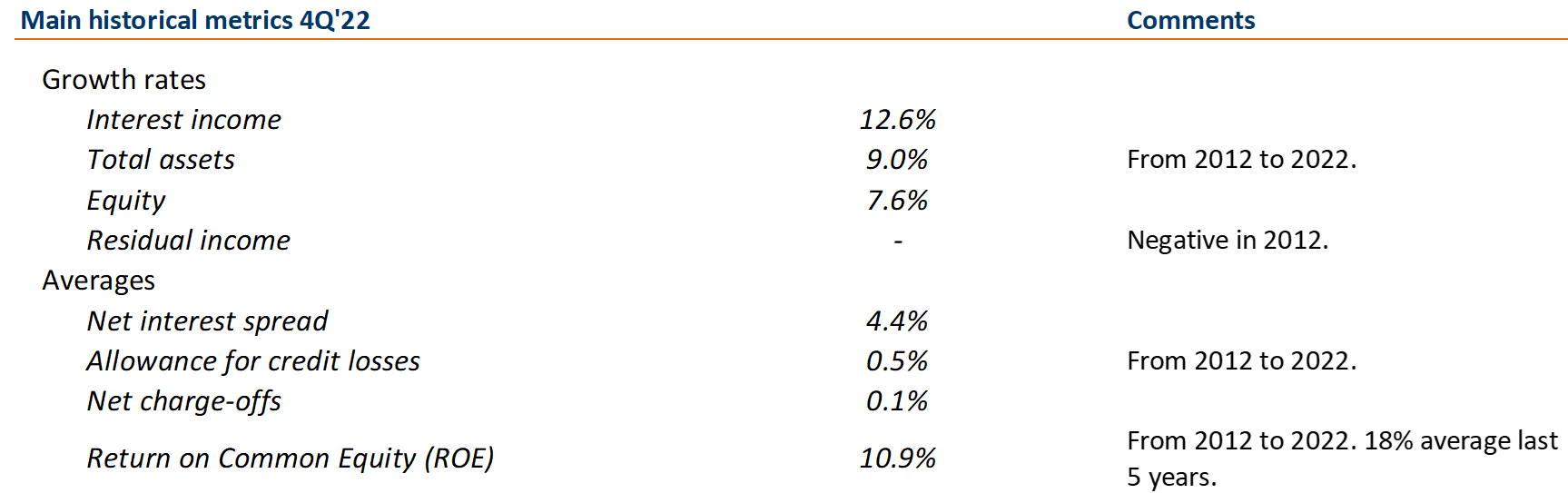

To frame the inputs to the valuation, the following table gives a nice sketch of what the company has delivered from 2012 to 2022. Two things are worth noting. First, as mentioned in the introduction, the bank was too small until around 2016, which depressed the efficiency ratios. And secondly, the table is up to 2022 (NBN’s accounting year ends in June), and it does not take into account the massive loan growth in the last three quarters:

Northeast Bank filings and own elaboration.

{kind=link}

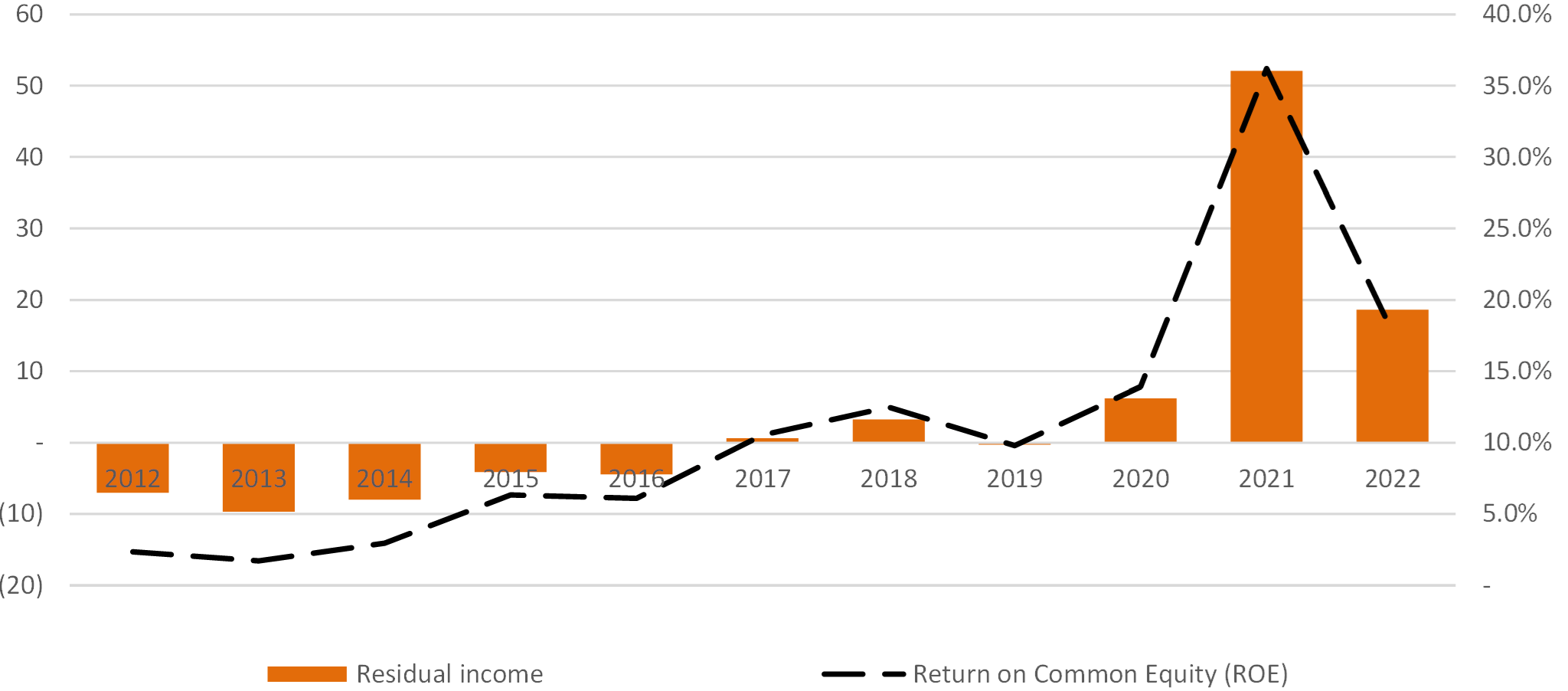

NBN’s track record in generating residual earnings (at a 10% discount rate) is shown in the graph below. Although the ROE in 2021 (35%) was heavily influenced by the PPP opportunity, the bank is clearly able to achieve returns above its hurdle rate:

Source: Northeast Bank filings and own elaboration. Numbers in millions. Rate of discount assumed: 10%.

{kind=link}

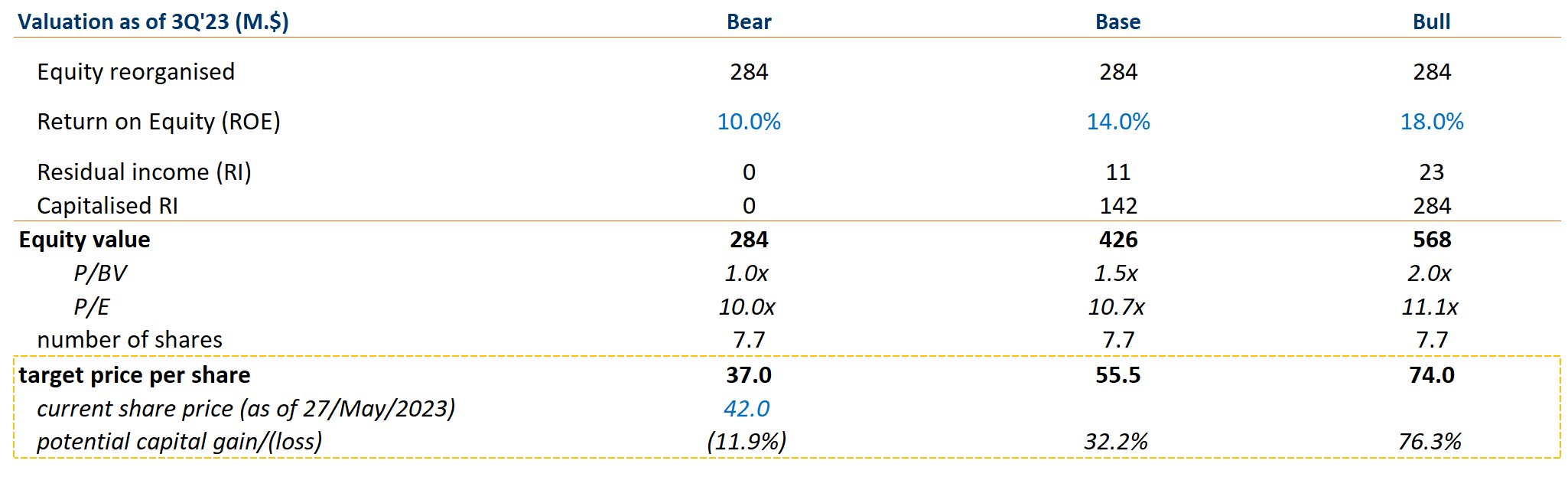

NBN’s historical metrics can give us a valuation range for the business. Using a discount rate of 10%, a modest residual earnings growth rate of 2%, and a 14% ROE (or $11M of economic profits annually) on NBN’s equity of $284M., the equity value would be around $430M., implying an upside of 32%, or $56 per share. At this price, NBN would trade at 1.5x P/BV and 10.7x P/E. On the other hand, if we assume economic profits of 23M, which is more in line with what I expect going forward, the target price would rise to $74 per share:

Source: Northeast Bank filings and own elaboration. Numbers in millions. Rate of discount assumed: 10%. Growth rate assumed: 2%.

{kind=link}

As useful as this one-year static valuation framework is, it misses the forest for the trees. First, earnings power is set to increase dramatically over the next few quarters; depending on the assumptions used for net charge-offs, interest margins and expense ratios, the bank is currently trading at 5-7x annualised earnings. These earnings will undoubtedly be reinvested, generating higher growth rates in the short term. And secondly, the above analysis does not take into account at all the ingenuity of Rick and his team; given the current macro environment, I have doubt that they will be able to create additional shareholder value, either in the form of opportunistic acquisitions or, if the price is right, in the form of share buybacks.

Downside risks

- Higher than expected loan losses.

- Key man risk.

- Difficult access to funding (unlikely, but possible).

Upside risks

- NBN is able to reinvest the coming earnings from the loan book at attractive rates.

- More stress and consolidation in the banking sector, creating opportunities for Northeast to buy more loans in the secondary market at attractive prices.

- A black swan event that Rick and his team can take advantage of.

[1] Over the course of the PPP, Northeast Bank originated $3.3bn. of loans and funded $11.2bn. of loans, incredible sums for such a small bank (around $1 billion in assets back then).

For further details see:

Primer Series: Northeast Bank - Partnering With One Of The Best Bankers In America