PUBM - PubMatic: This Is Cheap But CPM Decline Is A Problem

2023-12-08 01:15:27 ET

Summary

- PubMatic's Q3 results exceeded expectations, leading to increased investor interest.

- The stock appears cheap, priced at only 3x next year's EBITDA, but there are nuanced concerns.

- Near-term challenges include declining CPMs and bad debt expenses, impacting performance and growth.

Investment Thesis

PubMatic's ( PUBM ) Q3 results were better than expected and investors were quick to move in and buy the dip.

On the surface, this stock is an absolute steal, after all, it's priced in the absolute bargain basement. Not only does PubMatic not hold any debt, but also, it's only priced at 3x next year's EBITDA.

That should make it an outright buy, right? Well, I don't believe. I believe it's more nuanced than this. Here's why I'm neutral on this stock.

Rapid Recap,

In my previous analysis back in September , I said,

[PubMatic's] growth rates appear to be pointed in the wrong direction. What's more, I don't believe there's enough that distinguishes PubMatic from its competitors. This means that this business operates in a commodity-like environment, where its main service competes on price and little else.

Author's work on PUBM

Since that time, its share price has been really volatile. And although this stock has the illusion of being cheap I make the argument that this is not a clear-cut buy.

Near-Term Prospects Don't Look Rosy

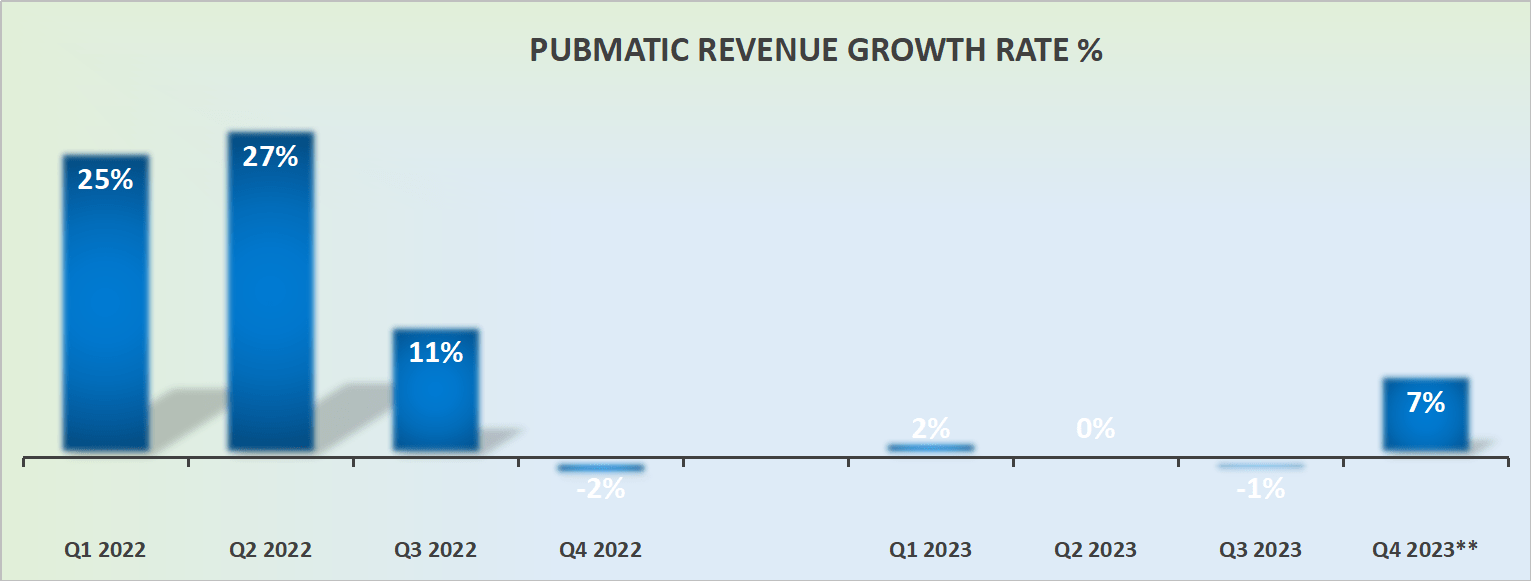

PubMatic currently faces several near-term challenges that impact its performance and growth. Firstly, the company is grappling with a decline in CPMs (cost per thousand impressions), particularly in high-value formats like video and CTV.

This trend is evident in the Q3 2023 results, where the company reported a 20% decrease in CPMs compared to the same period in the previous year. The macro pressures affecting CPMs are attributed to various factors, including a surge in alternative platforms such as fast channels, traditional streaming, Reels ( META ), and Shorts ( GOOG ).

This increased supply, coupled with relatively muted growth in ad budgets, puts downward pressure on CPMs. Additionally, PubMatic acknowledges the uncertainty surrounding the deprecation of third-party cookies, a key aspect of online advertising. While Google is pushing forward with its timeline for cookie deprecation, PubMatic is actively working on alternative solutions like contextual targeting and private marketplace deals. However, the industry's lack of clarity on the timeline and varying levels of participation by publishers and buyers present challenges in implementing and adopting these solutions effectively.

Secondly, PubMatic is contending with the impact of bad debt expenses, as highlighted in its Q3 2023 financial results. The company experienced challenges related to collectability, leading to increased bad debt expenses, which are expected to continue into the next few quarters, although this will become less impactful with time.

With this backdrop in mind, let's discuss its outlook for 2024.

Will 2024 See PubMatic's Growth Improve?

{kind=link}

To answer this question concretely, I believe that yes, PubMatic's revenue growth rates will grow. After all the comparables this year are much lower, so PubMatic should with ease deliver some topline growth.

But the question is where will PubMatic's pricing power stabilize? For now, PubMatic is facing a noteworthy decline in CPMs of 20% y/y which is indicative of the broader macroeconomic pressures impacting the digital advertising ecosystem. This downturn in CPMs is underscored by the increased availability of alternative platforms.

Essentially, there's an overabundance of advertising supply in the market, coupled with the restrained growth in ad budgets, which has created a scenario where there is " downward pressure on CPMs ."

This phenomenon is not a singular event but is characterized by incremental reductions in CPMs over the course of the past year.

In the context of real-time bidding dynamics, PubMatic acknowledges that a surplus of supply relative to demand leads to a "lower clearing price" for ad impressions.

Clearly, PubMatic is not satisfied with this performance and is seeking to invest in initiatives such as Supply Path Optimization (''SPO'') to explore "higher value opportunities" to secure resilience in the face of evolving market dynamics.

Given this context, I'm struggling to say that PubMatic could in fact see a 10% CAGR in 2024.

PUBM Stock Valuation -- 3x EBITDA

PubMatic's EBITDA is expected to reach approximately $220 million this year. However, the problem here is getting confident about what PubMatic's growth rates will be in 2024.

As discussed above, being able to build a convincing argument that PubMatic could deliver around 10% to 15% CAGR, has a dramatic impact on its underlying profitability.

Indeed, PubMatic, like most businesses, has a lot of inbuilt operating leverage. When its topline outpaces the majority of its fixed costs and some portion of its variable costs, its underlying profitability can shine.

However, I'm not sure that given the competitive market that PubMatic operates in, we can expect 15% topline growth in 2024.

That being said, I do believe that PubMatic could grow its EBITDA line by approximately 10% y/y in 2024.

To be more specific, assuming that PubMatic grows its EBITDA by 10% y/y, this would see PubMatic's EBITDA in 2024 reach approximately $240 to $250 million.

This would leave its stock priced at approximately 3x next year's EBITDA. A figure that doesn't appear expensive. Particularly when you keep in mind that PubMatic's cash on its balance sheet equates to approximately 20% of its market cap.

The Bottom Line

As I reflect on PubMatic's recent performance and future outlook, the Q3 results, surpassing expectations, initially paint a compelling picture of an undervalued stock, priced at merely 3x next year's EBITDA and free from debt.

However, a more nuanced analysis warrants a cautious, neutral stance. The significant 20% year-over-year decline in CPMs highlighted in Q3 2023, prompts a measured approach. This decline in CPMs, attributed to macroeconomic pressures and heightened competition from alternative platforms, poses a notable challenge.

Looking ahead to 2024, while there's potential for growth improvement, the persistent decline in CPMs requires careful consideration.

Despite a cautiously optimistic view of a 10% EBITDA growth in 2024, the competitive market environment introduces uncertainties. Thus, I remain neutral on this stock.

For further details see:

PubMatic: This Is Cheap, But CPM Decline Is A Problem